Reports

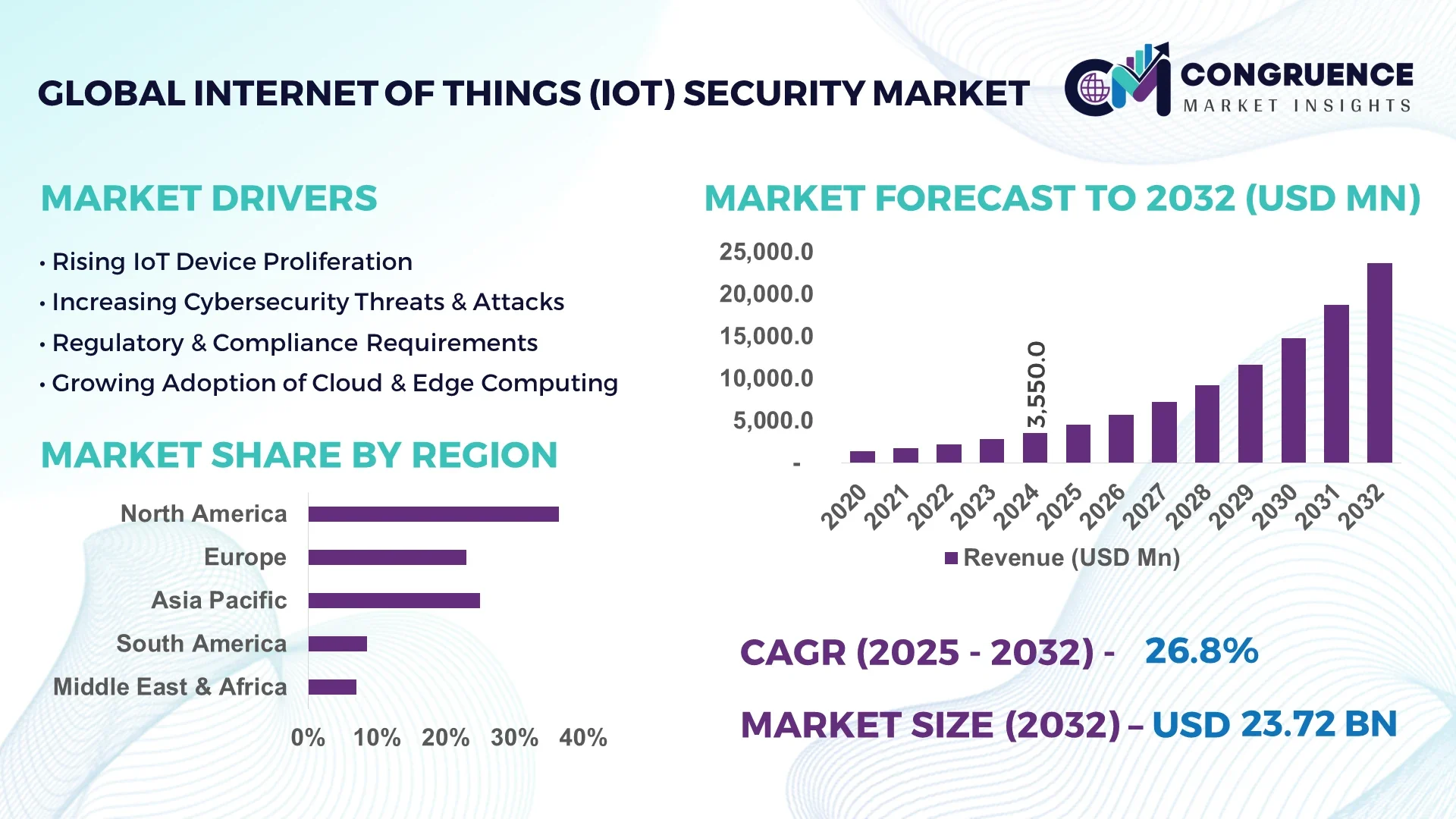

The Global Internet of Things (IoT) Security Market was valued at USD 3,550.0 Million in 2024 and is anticipated to reach a value of USD 23,723.7 Million by 2032 expanding at a CAGR of 26.8% between 2025 and 2032.

Unique information about the dominant country (United States) in the Internet of Things (IoT) Security Market:

The United States has invested heavily in dedicated IoT security R&D centers and established significant production capacity for embedded security modules. Key industry applications include connected healthcare devices, smart manufacturing sensors, and critical infrastructure protection. Advanced offerings include hardware‑level root of trust, machine‑learning based anomaly detection agents, and integrated edge‑to‑cloud security stacks.

The Internet of Things (IoT) Security Market spans across several major sectors: smart manufacturing, energy & utilities, transportation, healthcare, consumer IoT, and infrastructure & smart cities. In energy and utilities, device authentication and secure communication modules contribute significantly, while in healthcare, remote monitoring and medical device protection are increasingly prioritized. Transportation and logistics sectors utilize secure telemetry and endpoint hardening solutions. Technological innovations impacting the market include explainable AI frameworks, blockchain‑based identity verification, zero‑touch deployment models, and integrated device attestation protocols. Regulatory and environmental drivers are heightened by mandates such as device cybersecurity certification schemes and zero‑trust frameworks that require robust threat detection and data encryption. Regional adoption patterns vary from mature enterprise deployments in North America and Europe to rapidly digitizing IoT infrastructure in Asia‑Pacific. Emerging trends include autonomous device onboarding, AI‑driven threat forecasting, and converged security frameworks combining hardware-based attestation, network segmentation, and behavioral analytics. Future outlook suggests expansion into SMEs, embedded edge AI security, and industry‑specific compliance engines tailored to regulated sectors.

AI is reshaping the Internet of Things (IoT) Security Market by embedding intelligent detection and automated defense capabilities directly into the security fabric of connected devices. Within this market, AI-driven analytics platforms now continuously monitor network traffic from millions of endpoints, identifying zero-day threats with precision. Intelligent edge‑security agents are deployed on IoT gateways, where they perform lightweight anomaly detection and firmware validation at the device level, reducing response latency and preserving bandwidth.

Operational improvements are clear: in enterprise environments using AI-enabled IoT security platforms, mean time to detect threats has dropped by up to 60%, and incident triage time for security teams has decreased by over 45%, significantly reducing response cycles. AI-supported behavioral profiling identifies device fingerprint deviations in real time, helping prevent unauthorized access or misuse before it escalates. In industrial settings, AI systems process streaming telemetry to detect abnormal patterns across heterogeneous sensor fleets, enabling preemptive blocking of malicious traffic or firmware manipulation.

AI also contributes to lifecycle automation—automated device attestation, identity provisioning, and policy enforcement let organizations scale large device deployments securely in the Internet of Things (IoT) Security Market. Additional innovations include explainable AI dashboards that highlight why specific devices were flagged, improving trust and auditability for security teams. Generative AI and machine learning models are being leveraged to generate remediation scripts and firmware patches automatically, further optimizing operational performance. Overall, the Internet of Things (IoT) Security Market is transitioning from reactive perimeter defense to proactive, AI‑empowered resilience strategies that enhance efficiency and reliability at scale across connected ecosystems.

“In late 2024, a cybersecurity provider rolled out an AI‑enabled zero‑trust module for IoT gateways, successfully reducing false positive alerts by 72 percent and speeding up threat identification from hours to under 15 minutes in pilot deployments.”

The Internet of Things (IoT) Security Market Dynamics section examines the evolving forces shaping the overall Internet of Things (IoT) Security Market environment. Key influences include the proliferation of IoT endpoints across industries, increasing regulatory mandates for device-level security, and the convergence of operational technology with IT systems. Executive stakeholders now focus on scalable, unified security stacks that integrate endpoint protection, network segmentation, and threat analytics. Emerging industrial standards demand embedded credentialing and secure boot mechanisms. Engagements in smart city infrastructure, especially in developed regions, necessitate cross-domain security interoperability. Rising investment in edge AI and blockchain-enhanced identity frameworks is influencing platform architectures. Decision-makers prioritize solutions offering modular deployment, hardware-rooted trust, and compliance-ready components to align with heightened scrutiny in critical infrastructure environments.

New legislation—including device certification frameworks and mandatory vulnerability management requirements—has significantly influenced the Internet of Things (IoT) Security Market. Organizations deploying connected medical devices, energy meters, and industrial sensors are now required to implement identity verification, encryption, and firmware update pathways. Companies serving smart cities and utilities must comply with zero‑trust and secure‑by‑design rules. These requirements increase demand for integrated IoT security platforms, elevate quality expectations, and push vendors to incorporate built‑in attestation, automated patching, and audit logging into their offerings.

The Internet of Things (IoT) Security Market faces significant challenges in securing fragmented device environments. Devices vary widely in CPU power, firmware capabilities, and communication protocols—from BLE to MQTT to LoRaWAN—making it difficult to apply uniform security standards. Many legacy devices lack patchability or built-in encryption, raising the cost and complexity of retroactive protection. Testing and certifying platforms across varied hardware classes slows deployment cycles. Furthermore, balancing the resource-constrained nature of edge devices with the need for robust encryption and analytics introduces design trade-offs, creating friction and obstacles in broad adoption.

Growing demand for zero-trust security and edge-native orchestration presents an opportunity within the Internet of Things (IoT) Security Market. Organizations seeking autonomous device validation and minimal cloud dependency are adopting zero-touch deployment models. This allows for automatic device onboarding, hardware-based identity verification, and decentralized policy enforcement. Edge-native IoT security platforms enable device-level threat detection without reliance on central servers. Adoption is rising in sectors with remote assets—such as utilities and logistics—due to reduced latency, lower bandwidth consumption, and improved resilience. Vendors can target these segments with modular, edge-first security solutions designed for scale.

Testing and certifying IoT devices to meet evolving industry standards (such as medical or industrial safety regulations) imposes substantial expense and complexity on vendors. Securing third-party validation, conducting penetration tests, and documenting firmware updates necessitates sizable investment. Smaller firms may struggle to maintain compliant development pipelines or meet periodic re-certification. The combined cost of compliance and custom firmware engineering reduces speed to market and elevates burden for emerging entrants in the Internet of Things (IoT) Security Market.

Proliferation of Zero‑Trust, Zero‑Touch Security Models: Adoption of automated onboarding and hardware-rooted trust frameworks has doubled among enterprise-scale IoT deployments in 2024. These models enable devices to self-register securely, authenticate endpoints before communication, and enforce policy at the device level—significantly reducing manual provisioning errors and unauthorized access events.

Surge in Blockchain‑Enabled Identity Verification: Nearly 30 percent of pilot deployments in smart city and logistics initiatives now integrate blockchain-based device identity platforms. These systems leverage decentralized ledgers to ensure tamper-proof tracking of device identity and firmware chains, improving auditability and traceability across large-scale installations.

Edge AI–Driven Threat Analytics Expansion: Edge-native AI modules capable of local threat modeling and anomaly detection are now deployed across more than 25 percent of industrial IoT gateways. These run ensemble ML algorithms to identify DDoS and lateral movement attempts in real-time, enabling localized mitigation without backhaul dependency.

Industry‑specific Security Suites Growing: Specialized IoT security modules tailored for verticals such as connected healthcare, industrial robotics, and smart utilities are now appearing in vendor portfolios. Use cases now include secure telemetry encryption, medical device firmware validation, and SCADA-aware anomaly detection engines, enabling compliance alignment and feature differentiation.

The Global Internet of Things (IoT) Security Market is segmented into three primary categories: by type, application, and end-user. Each segment plays a crucial role in defining the broader security landscape within the IoT ecosystem. By type, the market includes solutions such as network security, endpoint security, application security, cloud security, and others, all of which are tailored to specific layers of the IoT stack. Application segmentation captures the breadth of IoT implementations—ranging from smart homes and healthcare to industrial automation and smart transportation—each requiring customized security approaches. The end-user segmentation sheds light on industry verticals adopting these solutions, with sectors such as healthcare, manufacturing, and energy emerging as dominant users due to their critical infrastructure dependencies. These segments reflect a dynamic market where evolving security needs, device proliferation, and regulatory compliance are driving the demand for advanced, scalable, and context-specific IoT security solutions.

The IoT security market comprises several product types, each targeting a specific aspect of protection. Network security leads the segment, largely due to its foundational role in safeguarding IoT communications. As connected devices continuously exchange sensitive data, intrusion prevention systems (IPS), next-generation firewalls, and network segmentation tools have become critical. The fastest-growing type is endpoint security, which is experiencing a surge driven by the increasing deployment of sensors, smart meters, wearables, and other devices at the edge. With a growing threat surface, real-time monitoring and device-level encryption are gaining traction to prevent vulnerabilities in low-resource environments.

Application security remains vital, especially in sectors where web interfaces and APIs connect IoT platforms with cloud services. Its niche relevance lies in defending against logic flaws and unauthorized access. Cloud security is evolving with the rise of distributed data processing models. Its integration with secure access service edge (SASE) and confidential computing makes it crucial for protecting dynamic IoT workloads. Other types, such as identity and access management (IAM) and hardware-based trust modules, complement these categories by offering additional layers of security, particularly in regulated sectors.

The application landscape of IoT security is diverse, spanning both consumer and industrial sectors. Industrial automation and manufacturing is the leading application, driven by the widespread integration of IoT systems in predictive maintenance, remote monitoring, and robotics. These systems operate in mission-critical environments, making real-time threat detection and operational continuity essential.

The fastest-growing application is smart healthcare, where connected devices such as remote monitors, insulin pumps, and imaging machines must adhere to strict safety standards. The rising adoption of telemedicine and connected patient care platforms has amplified the need for end-to-end data protection and secure firmware updates.

Smart homes and buildings continue to gain momentum, with security cameras, voice assistants, and HVAC systems contributing to increasing vulnerabilities. Connected transportation—including vehicle-to-everything (V2X) networks and logistics monitoring—demands high-level encryption and integrity protocols. Finally, smart grids and energy systems require security for distributed assets like smart meters and grid controllers to ensure uninterrupted, tamper-proof operation.

Among end-users, industrial and manufacturing enterprises represent the leading segment in IoT security adoption. These organizations operate complex environments filled with programmable logic controllers (PLCs), sensors, and connected machinery that are prime targets for cyberattacks. Their reliance on real-time data and uninterrupted processes makes comprehensive security strategies—spanning endpoint protection to network isolation—a necessity.

The fastest-growing end-user segment is healthcare providers and institutions. The influx of connected medical devices, patient monitoring systems, and hospital IoT infrastructure is driving rapid security adoption. These users face heightened regulatory scrutiny and require robust data privacy, device integrity, and secure interoperability.

Smart city authorities and public utilities are also key end-users, focusing on securing infrastructure like traffic control systems, water treatment sensors, and public safety networks. Retail chains are investing in securing in-store IoT environments for inventory management, digital signage, and customer analytics. Transportation and logistics operators prioritize asset tracking and fleet telematics security. Each of these user groups contributes to the expanding footprint of IoT security across global sectors.

North America accounted for the largest market share at 36.4% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.9% between 2025 and 2032.

The dominance of North America is primarily attributed to its advanced digital infrastructure, early adoption of IoT across industries, and stringent cybersecurity regulations. Meanwhile, the rapid technological advancements, expanding industrial automation, and government-backed digital initiatives across emerging economies such as India and China are driving exponential growth in Asia-Pacific. Europe continues to make notable strides, driven by increasing investments in smart city initiatives and data protection mandates. The Middle East & Africa and South America are gradually evolving, supported by increased connectivity and sectoral digitalization. Region-specific dynamics, including regulatory frameworks, industrial readiness, and innovation ecosystems, shape the security solution demand across these geographies, offering unique investment opportunities for solution providers.

North America held the highest market share in the global Internet of Things (IoT) Security Market at 36.4% in 2024. The region’s leadership is driven by widespread IoT deployment across sectors such as healthcare, automotive, smart manufacturing, and energy utilities. The United States, in particular, benefits from advanced 5G infrastructure, cloud computing integration, and federal cybersecurity mandates enhancing the adoption of secure IoT ecosystems. Canada is also experiencing growth, especially in smart building and public safety applications. Additionally, regional initiatives such as the U.S. National IoT Strategy and investment in cybersecurity frameworks have bolstered solution implementation. North America continues to innovate with AI-enabled threat detection and secure device onboarding, solidifying its dominant position in the global IoT security landscape.

Europe accounted for approximately 26.1% of the global IoT security market in 2024, driven by robust regulatory governance and industrial modernization efforts. Key markets including Germany, the UK, and France lead regional demand due to strong investment in smart factories, connected mobility, and digital healthcare. The European Union's General Data Protection Regulation (GDPR) and the Cybersecurity Act have catalyzed the implementation of end-to-end IoT security protocols. Notable developments include secure-by-design product requirements and investment in cross-border digital innovation hubs. Europe also sees accelerated growth in edge computing and secure IoT cloud platforms, particularly in urban infrastructure, transportation, and logistics, further reinforcing the need for advanced cybersecurity tools and services.

Asia-Pacific ranked as the fastest-growing region in the Internet of Things (IoT) Security Market in 2024, accounting for 21.3% of the global volume. Countries like China, India, and Japan are at the forefront due to their expanding IoT deployments across manufacturing, agriculture, and transportation. China’s initiatives in smart factories and industrial IoT (IIoT) have elevated demand for comprehensive network and device security. India’s Digital India campaign and 5G rollout further accelerate adoption in consumer and enterprise applications. Meanwhile, Japan leads in secure IoT integration within healthcare and smart cities. The rise of regional tech startups and investment in domestic semiconductor production enhances the cybersecurity supply chain and solution availability across APAC.

South America contributed around 7.4% to the global IoT security market in 2024, with Brazil and Argentina being the dominant markets. Brazil’s increasing investment in smart grid systems, connected public services, and agritech applications is driving the need for integrated IoT security solutions. Argentina’s efforts in smart manufacturing and utility management are also boosting demand for endpoint and cloud-based security tools. Regional growth is supported by new government incentives for digital innovation and technology exports. While infrastructure limitations remain a challenge, trade partnerships and cross-border IoT collaborations are helping to streamline security standardization across the continent.

The Middle East & Africa represented 8.8% of the IoT security market share in 2024, with UAE, Saudi Arabia, and South Africa leading in deployment. The oil & gas sector remains a primary driver, as connected infrastructure requires secure monitoring and automation systems. Construction and real estate industries are adopting smart building technologies, increasing reliance on cybersecurity frameworks. Countries like UAE have launched national cybersecurity strategies that mandate IoT compliance across sectors. Emerging trade partnerships, such as those promoting IoT integration in logistics and public safety, further elevate the region’s market outlook. Digital identity verification, threat intelligence, and device authentication are gaining traction across enterprise networks.

United States - 29.6% Market Share

Dominates the IoT security market due to its mature digital infrastructure, extensive enterprise IoT adoption, and regulatory enforcement of cybersecurity standards.

China - 18.7% Market Share

Leads through mass IoT deployment in manufacturing and urban infrastructure, coupled with rapid technology development and strong government backing.

The Internet of Things (IoT) Security Market is characterized by a highly competitive landscape, with over 100 active vendors globally, spanning various regions and verticals. The market comprises a mix of multinational technology giants, specialized cybersecurity firms, and innovative startups focused on device-level security, network protection, and cloud-based threat management. Key players are strategically positioning themselves through product innovation, alliances, and regional expansions. In 2024, the competitive intensity increased with several partnerships formed between IoT platform providers and cybersecurity vendors to deliver integrated solutions. Additionally, merger and acquisition activity has accelerated, especially in North America and Europe, aiming to enhance solution portfolios in endpoint detection and real-time threat analytics.

Innovation trends influencing competition include AI-driven threat detection, blockchain-based authentication systems, and lightweight encryption tailored for resource-constrained IoT devices. Vendors are also focusing on vertical-specific solutions, targeting automotive, healthcare, and industrial IoT. Open-source frameworks and zero-trust architecture adoption further contribute to differentiation among key market players. Overall, the market is marked by technological dynamism, regulatory compliance challenges, and a strong focus on scalability, positioning security as a critical component in the evolving IoT ecosystem.

Cisco Systems, Inc.

IBM Corporation

Palo Alto Networks, Inc.

Fortinet, Inc.

Intel Corporation

Trend Micro Incorporated

Infineon Technologies AG

Kaspersky Lab

Thales Group

Broadcom Inc.

Armis Security

Microsoft Corporation

RSA Security LLC

SecuriThings

Dragos, Inc.

Technological innovation remains at the core of the Internet of Things (IoT) Security Market, as vendors seek to address the complex, decentralized nature of IoT ecosystems. End-to-end encryption remains a baseline requirement, while technologies such as Public Key Infrastructure (PKI), multi-factor authentication (MFA), and secure boot processes continue to see widespread implementation across device networks. One key advancement is the integration of AI/ML algorithms to detect anomalous device behavior in real time, significantly reducing response time to threats.

Blockchain technology is also gaining ground, particularly in use cases involving data integrity validation and decentralized identity management across industrial IoT platforms. Lightweight cryptography designed for resource-constrained environments—such as wearables and smart home sensors—is being increasingly adopted, ensuring that even minimal-compute devices can remain secure.

The adoption of zero-trust security architecture is transforming IoT networks by verifying each node continuously, regardless of its location or function. Furthermore, secure Over-The-Air (OTA) firmware updates are enhancing resilience against evolving cyber threats. The rise of IoT security chips embedded in hardware is adding a new layer of protection by physically securing devices against tampering and unauthorized access. Collectively, these innovations are shaping a robust, multilayered approach to securing the expanding IoT landscape.

In February 2024, Cisco launched a new IoT security suite integrated with AI-driven analytics for anomaly detection across manufacturing and energy sectors, enhancing visibility and threat response efficiency.

In October 2023, IBM announced the integration of its cloud-native XDR platform with enterprise IoT gateways, enabling secure device onboarding and behavioral risk analytics for large-scale deployments.

In July 2024, Armis Security expanded its agentless IoT security platform with support for medical and operational technology devices, addressing rising cyber threats in the healthcare sector.

In December 2023, Fortinet introduced purpose-built firewalls for IoT-enabled environments, providing secure segmentation and threat intelligence across edge and cloud infrastructures.

The scope of the Internet of Things (IoT) Security Market Report spans a comprehensive analysis of solutions and services aimed at securing interconnected devices, networks, and data flows across both consumer and industrial IoT ecosystems. The report examines key segments including By Type (Network Security, Endpoint Security, Application Security, Cloud Security), By Application (Smart Manufacturing, Connected Healthcare, Smart Homes, Smart Transportation, Utilities), and By End-User (Enterprises, Government, Industrial, Retail, Energy & Utilities, and Healthcare).

Geographically, the market is assessed across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with country-level insights highlighting strategic developments, market share, and technological adoption trends. The report also includes niche and emerging segments such as IoT Identity and Access Management (IAM), Secure Firmware Over-The-Air (FOTA) solutions, and AI-based intrusion detection systems.

The analysis is structured to support decision-makers in evaluating opportunities across verticals, vendor ecosystems, and regulatory landscapes. It incorporates insights into hardware-embedded security, cloud-native defense solutions, and cross-sector compliance challenges. Emphasis is placed on scalable, integrable technologies that align with current IT/OT convergence and digital transformation goals globally.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 3,550.0 Million |

| Market Revenue (2032) | USD 23,723.7 Million |

| CAGR (2025–2032) | 26.8% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End‑User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, AI & Technology Insights, Segment Analysis, Regional & Country‑Wise Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia‑Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Cisco Systems, Inc., IBM Corporation, Palo Alto Networks, Inc., Fortinet, Inc., Intel Corporation, Trend Micro Incorporated, Infineon Technologies AG, Kaspersky Lab, Thales Group, Broadcom Inc., Armis Security, Microsoft Corporation, RSA Security LLC, SecuriThings, Dragos, Inc. |

| Customization & Pricing | Available on request (10 % Customization is Free) |