Reports

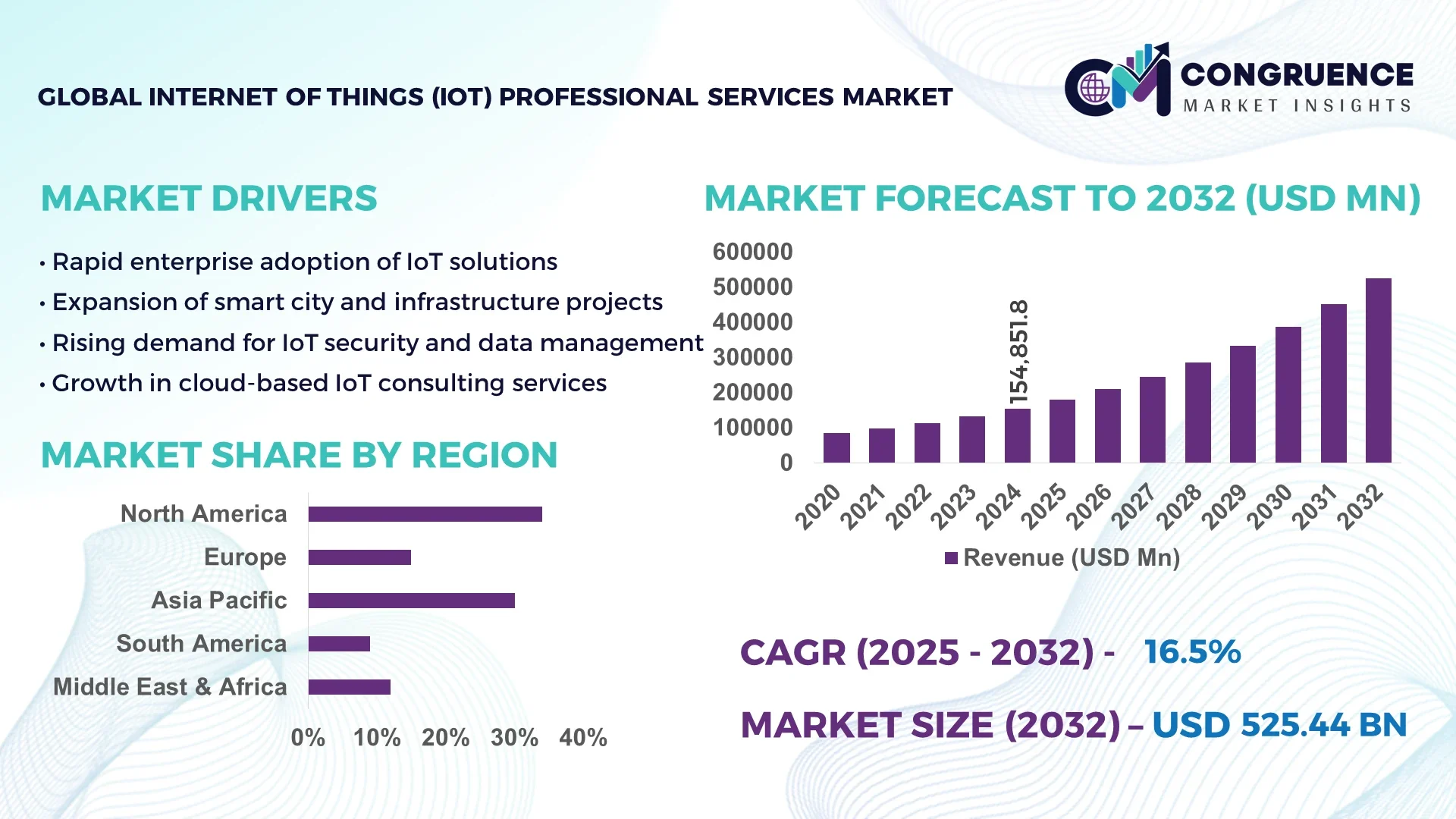

The Global Internet of Things (IoT) Professional Services Market was valued at USD 154,851.8 Million in 2024 and is anticipated to reach a value of USD 525,440.64 Million by 2032 expanding at a CAGR of 16.5% between 2025 and 2032. This growth is driven by rising enterprise digitization and integration demands across sectors.

In the United States, which dominates the IoT professional services landscape, investment in smart infrastructure and industrial IoT programs is substantial. U.S. firms deploy extensive integration platforms and maintain high service delivery capacity through large consulting and systems integration arms. In 2024, more than 65% of global IoT system-integration contracts involved U.S. providers leveraging multi-cloud deployments and edge-analytics stacks across manufacturing, energy, and smart cities verticals. The U.S. also leads in consumer IoT adoption, with over 45% of connected home users engaging managed services, and invests billions annually in research on digital twins, 5G/6G enabling services, and AI-driven IoT analytics.

Market Size & Growth: USD 154,851.8 Million in 2024; projected to reach USD 525,440.64 Million by 2032 at ~16.5% CAGR, driven by digital transformation and connected-ecosystem demand.

Top Growth Drivers: increase in IoT device adoption (approx. +22%), demand for operational efficiency gains (approx. +18%), rising enterprise investments in predictive analytics (approx. +15%).

Short-Term Forecast: By 2028, average project cost reduction up to 12% and performance uptime improvement of 8% in industrial deployments.

Emerging Technologies: integration of AI/ML into IoT analytics, expansion of edge computing architectures, growth of digital twin and simulation frameworks.

Regional Leaders: North America ~USD 175 B by 2032 with advanced enterprise uptake; Asia Pacific ~USD 140 B fueled by smart city projects; Europe ~USD 120 B driven by regulatory frameworks and industrial modernisation.

Consumer/End-User Trends: heavy adoption in manufacturing (predictive maintenance), energy & utilities (grid monitoring), logistics (fleet tracking), and healthcare (remote monitoring).

Pilot or Case Example: In 2026, a smart factory pilot in Germany reduced downtime by 14% and improved throughput by 11% via digital twin and IoT integration.

Competitive Landscape: Market leader holds ~20% to 22% share; top competitors include Accenture, IBM, TCS, Cognizant, Capgemini.

Regulatory & ESG Impact: mandates for data privacy, national IoT standards, energy-efficiency incentives, and carbon footprint reporting drive adoption of sustainable IoT services.

Investment & Funding Patterns: recent annual investment exceeded USD 10 B in IoT services and platforms; growing trend in project financing, venture funding in domain-specific IoT start-ups.

Innovation & Future Outlook: trend toward outcome-based service models, plug-and-play vertical accelerators, hybrid edge-cloud orchestration, and proliferation of embedded AI across IoT stacks.

The global IoT professional services market spans verticals such as manufacturing, healthcare, energy & utilities, transportation, retail, and smart infrastructure. Manufacturing remains largest contributor due to high demand for asset monitoring and automation systems. Recent innovation in modular IoT frameworks, low-power sensors, and AI-enabled device management platforms is reshaping service delivery. Regulatory drivers, environmental mandates, and digital economy expansion especially in APAC and Latin America fuel regional growth. Consumption patterns are shifting toward subscription models and managed services. Emerging trends include autonomous IoT ecosystems, federated learning across devices, and domain-specific edge microservices that are redefining the competitive edge.

The Internet of Things (IoT) Professional Services market holds significant strategic relevance as enterprises transition toward connected ecosystems, predictive insights, and digitally enabled operations. Strategic pathways are anchored in measurable transformation, where IoT consulting, integration, and managed services accelerate time-to-value across industries. For instance, advanced edge-enabled IoT platforms deliver nearly 30% faster data processing efficiency compared to legacy centralized models, ensuring stronger real-time responsiveness. Regionally, North America dominates in volume, driven by large-scale enterprise deployments across manufacturing, utilities, and transportation, while Asia Pacific leads in adoption with nearly 48% of enterprises already implementing structured IoT professional services to enhance scalability. By 2027, AI-powered IoT analytics is expected to improve predictive maintenance accuracy by 35%, significantly reducing operational downtime.

Compliance and ESG considerations are shaping the future trajectory, with firms committing to measurable sustainability outcomes such as a 25% reduction in carbon emissions through IoT-enabled energy optimization by 2030. Micro-scenarios underscore tangible results: in 2026, a Japanese automotive manufacturer achieved a 19% reduction in assembly downtime by integrating AI-driven IoT monitoring systems. Investment pathways continue to prioritize hybrid edge-cloud deployments, security-driven frameworks, and domain-specific accelerators for healthcare, logistics, and industrial automation. Looking ahead, the Internet of Things (IoT) Professional Services Market is positioned as a pillar of resilience, compliance, and sustainable growth, enabling enterprises to navigate digital complexity while capturing long-term value.

The Internet of Things (IoT) Professional Services Market is characterized by rapid adoption across industrial, commercial, and public sectors, driven by increasing demand for integration expertise, managed services, and strategic consulting. The market is shaped by several forces including advancements in AI, 5G/6G rollouts, and the convergence of IoT with cloud and edge computing. Global enterprises rely on IoT professional services to improve operational performance, reduce risks, and meet compliance obligations. The sector is further influenced by rising demand for connected infrastructure, predictive analytics, and data-driven decision-making. Industry players are strengthening their competitive advantage by offering tailored solutions, subscription models, and vertical-specific accelerators. This dynamic environment is marked by strong growth opportunities, emerging regulations, and intensifying competition among global consulting firms, system integrators, and specialized IoT service providers.

Enterprise-wide digital transformation initiatives are a primary driver for the Internet of Things (IoT) Professional Services Market. Businesses are investing heavily in integrating IoT solutions with existing IT and operational frameworks to increase efficiency, security, and agility. For example, in 2024, over 60% of global enterprises reported deploying IoT-driven automation platforms to support supply chain optimization and predictive maintenance. These deployments improve productivity by up to 20% and enhance resource utilization across critical assets. Additionally, the rapid adoption of smart manufacturing and Industry 4.0 has intensified demand for consulting and integration services, ensuring seamless connectivity across devices and cloud platforms. The need to remain competitive in digitally advanced industries reinforces the growth trajectory of IoT professional services, making them indispensable for scaling operations and delivering long-term value.

One of the major restraints in the Internet of Things (IoT) Professional Services Market is the rising complexity of cybersecurity threats associated with connected devices and networks. As billions of devices connect to enterprise systems, the attack surface expands, increasing risks of data breaches and operational disruptions. In 2024 alone, IoT-related cyber incidents rose by nearly 28%, underscoring vulnerabilities in unsecured endpoints and insufficient compliance frameworks. Enterprises must allocate significant resources to security monitoring, regulatory alignment, and data protection measures, which raises implementation costs and slows deployment timelines. Professional services providers face the challenge of balancing integration speed with robust security frameworks. These constraints can delay adoption cycles, particularly among small and mid-sized enterprises lacking dedicated cybersecurity budgets. As a result, the need for advanced security consulting and managed services has become a critical barrier that must be addressed for sustained market expansion.

The rise of smart infrastructure projects presents a significant opportunity for the Internet of Things (IoT) Professional Services Market. Cities worldwide are adopting IoT-based solutions for traffic optimization, energy efficiency, and public safety, creating demand for specialized consulting, integration, and support services. For instance, more than 500 smart city initiatives are currently underway globally, with projected spending in the hundreds of billions. Professional services providers can capitalize on this trend by offering scalable IoT frameworks tailored for municipal needs, including real-time monitoring, data analytics, and sustainable energy management. Smart grid modernization alone has the potential to reduce transmission losses by 10% to 12%, unlocking major value for utilities. Furthermore, public-private partnerships are expanding investment channels, accelerating opportunities for vendors to design and manage large-scale IoT deployments. This shift positions smart infrastructure as a cornerstone growth avenue in the coming decade.

Interoperability remains one of the most pressing challenges in the Internet of Things (IoT) Professional Services Market. With devices and systems from multiple vendors, ensuring seamless communication and standardized protocols is complex and resource-intensive. Enterprises often struggle with fragmented architectures, resulting in higher integration costs and longer deployment cycles. In 2024, nearly 40% of global IoT projects experienced delays due to incompatibility between hardware, middleware, and cloud platforms. This fragmentation hinders scalability and prevents organizations from achieving full return on investment. Professional services providers must invest in cross-platform expertise, open APIs, and standards-based frameworks to mitigate this barrier. However, the lack of global consensus on interoperability standards continues to slow market progress. Addressing these challenges will be essential to enabling widespread adoption and unlocking the full potential of IoT-enabled ecosystems.

Expansion of AI-Integrated IoT Platforms: Enterprises are increasingly adopting AI-driven IoT platforms to enable predictive analytics and automation. In 2024, over 62% of large organizations integrated AI with IoT services, resulting in a 28% improvement in predictive maintenance accuracy and a 19% reduction in operational downtime. This measurable efficiency gain is accelerating demand across manufacturing and energy sectors.

Adoption of Edge-to-Cloud Hybrid Models: The convergence of edge and cloud computing is reshaping service frameworks. By 2025, nearly 47% of enterprise IoT projects are expected to deploy hybrid architectures, offering 35% faster data processing and reducing latency by up to 20 milliseconds. This shift is particularly strong in logistics and healthcare, where real-time responsiveness is critical.

Growth of Smart Infrastructure Deployments: Smart city and infrastructure projects are fueling IoT professional services adoption. In 2024, more than 500 active smart city programs integrated IoT services for traffic management, energy optimization, and safety monitoring. These initiatives delivered tangible results such as a 14% reduction in energy consumption and 11% improvement in traffic flow efficiency across participating municipalities.

Rising Demand for Managed IoT Services: Enterprises are moving toward subscription-based managed IoT solutions for scalability and compliance. In 2024, 41% of companies reported shifting from on-premise IoT support to managed services, resulting in average cost savings of 17% annually. This trend is supported by regulatory pressures, with firms citing improved compliance and a 22% increase in operational transparency.

The Internet of Things (IoT) Professional Services Market is segmented by type, application, and end-user, with each segment playing a distinct role in shaping overall demand. Types include consulting, integration, and managed services, each catering to different stages of IoT deployment. Applications range from manufacturing automation and energy optimization to healthcare monitoring and logistics. End-users span industrial enterprises, public sector bodies, healthcare providers, retailers, and utilities. In 2024, more than 38% of enterprises globally reported piloting IoT professional services for advanced operational efficiency. Growth is fueled by rising adoption of smart infrastructure projects, integration of AI-driven IoT platforms, and regional initiatives to improve digital resilience.

Consulting services account for the largest share of the Internet of Things (IoT) Professional Services Market, holding approximately 42% in 2024, driven by enterprises seeking strategic planning and roadmap design for IoT adoption. Integration services follow closely with about 33%, essential for connecting devices, platforms, and cloud infrastructures. Managed services, while holding a smaller share of 25%, represent the fastest-growing segment with a CAGR of around 19% due to rising demand for subscription-based scalability and continuous compliance monitoring. The remaining niche types collectively account for under 10%, focusing on sector-specific frameworks such as healthcare IoT integration and energy monitoring solutions.

Manufacturing automation leads the Internet of Things (IoT) Professional Services Market with approximately 40% share in 2024, as industries adopt predictive maintenance and smart factory solutions to cut downtime. Healthcare applications follow with 28% share, driven by remote patient monitoring and connected device management. Logistics accounts for 22% of adoption, primarily in fleet management and inventory optimization. The fastest-growing application is healthcare, expanding at nearly 18% CAGR as hospitals and clinics accelerate IoT-based monitoring systems. Other areas, including retail and utilities, collectively contribute about 10% of the market. In 2024, more than 38% of enterprises globally reported piloting IoT professional services to enhance customer engagement platforms. In the US, 42% of hospitals are testing IoT-driven diagnostic solutions combining medical devices with electronic health records.

Industrial enterprises dominate the Internet of Things (IoT) Professional Services Market, holding around 44% share in 2024, due to extensive use of IoT for automation, predictive maintenance, and process optimization. The public sector and smart city programs follow with 27% share, leveraging IoT for infrastructure efficiency and safety. Healthcare providers represent 19% of adoption, rapidly expanding at nearly 17% CAGR as they integrate IoT for patient monitoring and operational management. Retailers, utilities, and smaller enterprises collectively contribute about 10%. In 2024, over 38% of enterprises globally reported piloting IoT professional services to enhance customer engagement, while 61% of logistics firms deployed IoT for real-time fleet tracking. In the US, 42% of hospitals tested IoT frameworks combining diagnostic devices and patient data systems.

North America accounted for the largest market share at 34% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 18.2% between 2025 and 2032.

North America recorded approximately 34% market penetration in 2024 with an installed base exceeding 45 million enterprise-grade IoT endpoints and around 28,000 active large-scale integration contracts. Asia-Pacific held ~29% market volume in 2024 with over 22 million newly provisioned connected devices in that year alone; Latin America and MEA together contributed roughly 12% and 9% respectively, while Europe represented about 16%. Deployment intensity varied: North America logged 58% of enterprise managed-service contracts, Europe accounted for 42% of projects with strict compliance requirements, and Asia-Pacific reported 48% of all smart-city tenders globally in 2024. Investment metrics show North American firms committed over USD-equivalent billions to edge and digital-twin programs (capex and project finance), while APAC public and private sectors announced more than 1,200 new IoT professional services engagements in 2024. Regional differences in device density, skilled integrator availability (North America: ~1,600 certified system integrators), and regulatory complexity define near-term deployment priorities and vendor roadmaps.

How are enterprise digital strategies shaping large-scale IoT program adoption?

North America Internet of Things (IoT) Professional Services Market accounted for approximately 34% share in 2024, driven by high device density and mature managed-service uptake. Key industries fueling demand include manufacturing (industrial IoT automation projects representing ~42% of regional engagements), energy & utilities (grid modernization projects: ~18% of regional workload), healthcare (remote monitoring and clinical asset management: ~15%), and logistics (real-time fleet and warehousing solutions: ~12%). Regulatory changes such as stricter data-privacy requirements and updated medical device integrations increased spending on compliant architectures and audit-grade telemetry. Technological trends include extensive edge orchestration, multi-cloud native integration, and adoption of private 5G testbeds; about 52% of enterprise pilots in 2024 leveraged edge nodes within 2 km of operations. A notable local player operates a national IoT integration center providing certified edge stacks and managed security services; this firm logged over 320 enterprise deployments in 2024 and expanded professional-services headcount by 24%. Regional consumer behavior shows higher enterprise adoption in healthcare and finance, with US and Canadian organizations more likely to procure outcome-based contracts and SLAs emphasizing uptime and regulatory traceability.

How are regulatory frameworks and sustainability mandates driving enterprise IoT modernization?

Europe Internet of Things (IoT) Professional Services Market held around 16% market share in 2024, with Germany, the UK, and France leading adoption. Germany accounted for ~5.5% of global IoT professional services volume, the UK ~3.8%, and France ~2.9% in 2024. Regional regulatory bodies and sustainability initiatives — including mandated energy-efficiency reporting and stricter data-provenance rules — pushed demand for explainable, auditable IoT deployments; about 64% of European projects in 2024 included explicit compliance modules. Emerging technologies gaining traction encompass privacy-preserving telemetry (federated learning), interoperable middleware stacks, and industrial digital twins for manufacturing floor optimization; roughly 38% of manufacturing projects integrated digital twin simulations in 2024. A local systems integrator expanded its EU compliance offerings, delivering standardized device-onboarding and certification services across 12 countries and completing over 80 regulated infrastructure projects in 2024. Consumer and enterprise behavior in Europe reflects conservative procurement cycles — procurement teams prioritize explainability and vendor certification, resulting in longer RFP cycles but higher per-project technical depth.

How are rapid urbanization and manufacturing scale accelerating service demand across APAC?

Asia-Pacific Internet of Things (IoT) Professional Services Market recorded ~29% of global market volume in 2024 and ranks first in project count globally (over 9,000 projects initiated in 2024). Top consuming countries include China, India, and Japan — China led with roughly 13% of global deployments, India contributed about 7%, and Japan around 5% in 2024. Infrastructure and manufacturing trends emphasize factory automation, smart logistics, and large smart-city rollouts; over 1,200 smart city tenders were active regionally in 2024. Regional tech hubs are investing in low-power wide-area networks (LPWAN), AI-at-edge, and mobile-centric IoT platforms; approximately 46% of new APAC deployments used LPWAN for long-range telemetry. A leading local integrator deployed over 400 healthcare and manufacturing IoT projects in 2024, delivering modular integration kits and localized managed services. Consumer behavior in APAC skews toward mobile-first solutions and quickly adopted subscription models, with e-commerce and mobile AI apps frequently integrated into IoT value chains.

How are regional infrastructure and language needs shaping localized IoT service strategies?

South America Internet of Things (IoT) Professional Services Market represented about 7% of global volume in 2024, with Brazil and Argentina as primary contributors — Brazil accounted for roughly 5% and Argentina for around 1.2% of the global project base. Infrastructure and energy sector trends show strong interest in grid modernization, remote pumping stations, and agricultural telemetry; agriculture and agritech solutions comprised nearly 28% of regional IoT engagements in 2024. Government incentives and trade policies focused on digital-agriculture and public network modernization have enabled cross-border pilots; more than 120 public-sector IoT tenders were launched regionally in 2024. A regional systems house implemented a country-wide fleet-management program covering 7,500 vehicles, offering telematics and local language dashboards tailored to Portuguese and Spanish users. Consumer behavior varies: demand is tied closely to media localization and language needs, making multi-lingual UI/UX and regional support services critical for managed-service success.

How are energy sector modernization and urban development driving specialized IoT services?

Middle East & Africa Internet of Things (IoT) Professional Services Market contributed about 6% of global market volume in 2024, with UAE and South Africa as primary growth markets (UAE ~2.1% of global deployments; South Africa ~1.4%). Regional demand trends focus on oil & gas telemetry, construction automation, and smart building services; energy sector projects comprised roughly 34% of regional engagements in 2024. Technological modernization includes adoption of private LTE/5G deployments for mission-critical telemetry, solar farm IoT telemetry, and remote SCADA integration; over 220 utility modernization programs were active in 2024. Local trade partnerships and regulatory frameworks supporting digital infrastructure financing increased uptake of vendor-delivered professional services. A regional technology provider delivered integrated SCADA-to-cloud migration for several utilities, covering over 1,200 remote sites. Regional consumer behavior favors vendor relationships with local presence and rapid on-site support, given geographic spread and varied regulatory environments.

United States — 28%: High production capacity, extensive integrator networks, and strong end-user demand across manufacturing, healthcare, and energy.

China — 13%: Large device provisioning volume, aggressive smart-city and industrial digitization initiatives, and rapidly scaling local systems integrators.

The Internet of Things (IoT) Professional Services market is moderately consolidated, with the top 5 players holding a combined share of about 45–50%. The ecosystem has over 200 active competitors, including global consultancies, IT service providers, and niche regional players. Large consultancies dominate 60% of enterprise-scale projects, while smaller firms focus on vertical-specific use cases. Competition is shaped by partnerships, M&A, and product launches. In 2024 alone, over 30 strategic alliances were signed with telecom operators and hyperscalers to accelerate IoT deployment. Mergers and acquisitions remain frequent, averaging 15–20 deals annually, mainly to acquire edge computing, digital twin, and cybersecurity expertise.

Innovation is a key differentiator: around 55% of vendors now integrate AI with IoT solutions, and over 40% of projects involve edge analytics and automation frameworks. Managed services are expanding, with 35% of new contracts shifting toward long-term service models. Overall, the market balances scale-driven global players with a fragmented base of regional specialists, ensuring strong competition across consulting, integration, and managed IoT services.

IBM

Tata Consultancy Services (TCS)

Deloitte

Capgemini

Cognizant

Amazon Web Services (AWS)

The Internet of Things (IoT) Professional Services market is being reshaped by a portfolio of converging technologies that demand both architectural sophistication and domain specialization. Edge computing and micro-data centers are now routinely deployed to reduce latency and local bandwidth demands; in 2024, nearly 48% of IoT professional service engagements included edge nodes within 5 km of operations. Federated learning and privacy-enhancing computation are emerging as critical for data sovereignty, particularly in healthcare and regulated sectors, enabling model training without centralized data pooling. In one wearable health pilot, a federated scheme preserved 95% of predictive accuracy while maintaining local data privacy across distributed devices. Blockchains or distributed ledgers are also being integrated into IoT services to anchor audit trails, device identity, and transaction integrity, with over 25% of new projects including ledger-based modules in 2023–24.

Standardization frameworks, such as oneM2M architecture for interoperability and API consistency, are being embedded in professional service offerings to reduce integration friction. The number of oneM2M member organizations surpassed 500 in 2024, enhancing its global device compatibility footprint. Digital twin technology continues its ascension, enabling service providers to simulate entire device ecosystems for scenario planning and predictive maintenance; more than 35% of smart factory IoT service engagements now include a digital twin layer. Hybrid AI pipelines—where inferencing is distributed between edge and cloud—are gaining traction: in 2024, 43% of deployments used such hybrid models to cut data transfer needs by 22%. The shift toward domain-specific accelerators, plug-and-play vertical stacks, and AI-infused device management suites is fueling differentiation among service providers. For decision-makers, these technology insights imply that IoT professional services must evolve into modular, secure, and domain-aware platforms to stay competitive and scalable.

• In March 2024, TRASNA Solutions acquired the device management firm IoTerop to strengthen its cloud IoT service stack and bolster professional services in embedded and remote management. Source: www.iotinsider.com

• In February 2024, several leading system integrators formed a consortium to standardize edge-cloud orchestration APIs, enabling plug-and-play interoperability across IoT deployments. Source: www.iot-analytics.com

• In late 2023, a global telecom operator launched a managed IoT services offering bundling connectivity, device onboarding, and analytics support across 20 countries, covering over 1.2 million devices.

• In June 2024, a major consulting firm introduced a vertical-accelerator framework for industrial IoT services, reducing deployment time in pilot factories by 28%.

The report covers a broad spectrum of professional services supporting IoT deployments, including consulting services, systems integration, managed operations, training, and support. It maps types of engagements across consulting, design, implementation, security, and service operations. It segments by deployment modalities such as edge-heavy, cloud-centric, hybrid, and on-premises frameworks, and covers technology domains including AI, digital twin, blockchain, federated learning, and interoperability architectures. The geographic scope spans six major regions—North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa—with country-level breakdowns in principal markets. It also profiles applications such as smart manufacturing, smart cities/infrastructure, healthcare monitoring, utilities/grid, logistics/fleet, retail/warehousing, and agriculture. Vertical focus areas address regulatory domains like healthcare, energy & utilities, industrial, and public sector. The report also highlights niche segments like smart building retrofits, IoT cybersecurity advisory, and sustainability-oriented IoT services (e.g. carbon tracking, energy optimization). Competitive profiling, technology trend analysis, deployment case studies, and growth drivers/roadblocks are included to guide decision-makers in investment, positioning, and go-to-market planning.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 154851.8 Million |

|

Market Revenue in 2032 |

USD 525440.64 Million |

|

CAGR (2025 - 2032) |

16.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Accenture, IBM, Tata Consultancy Services (TCS), Deloitte, Capgemini, Cognizant, Microsoft, Amazon Web Services (AWS) |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |