Reports

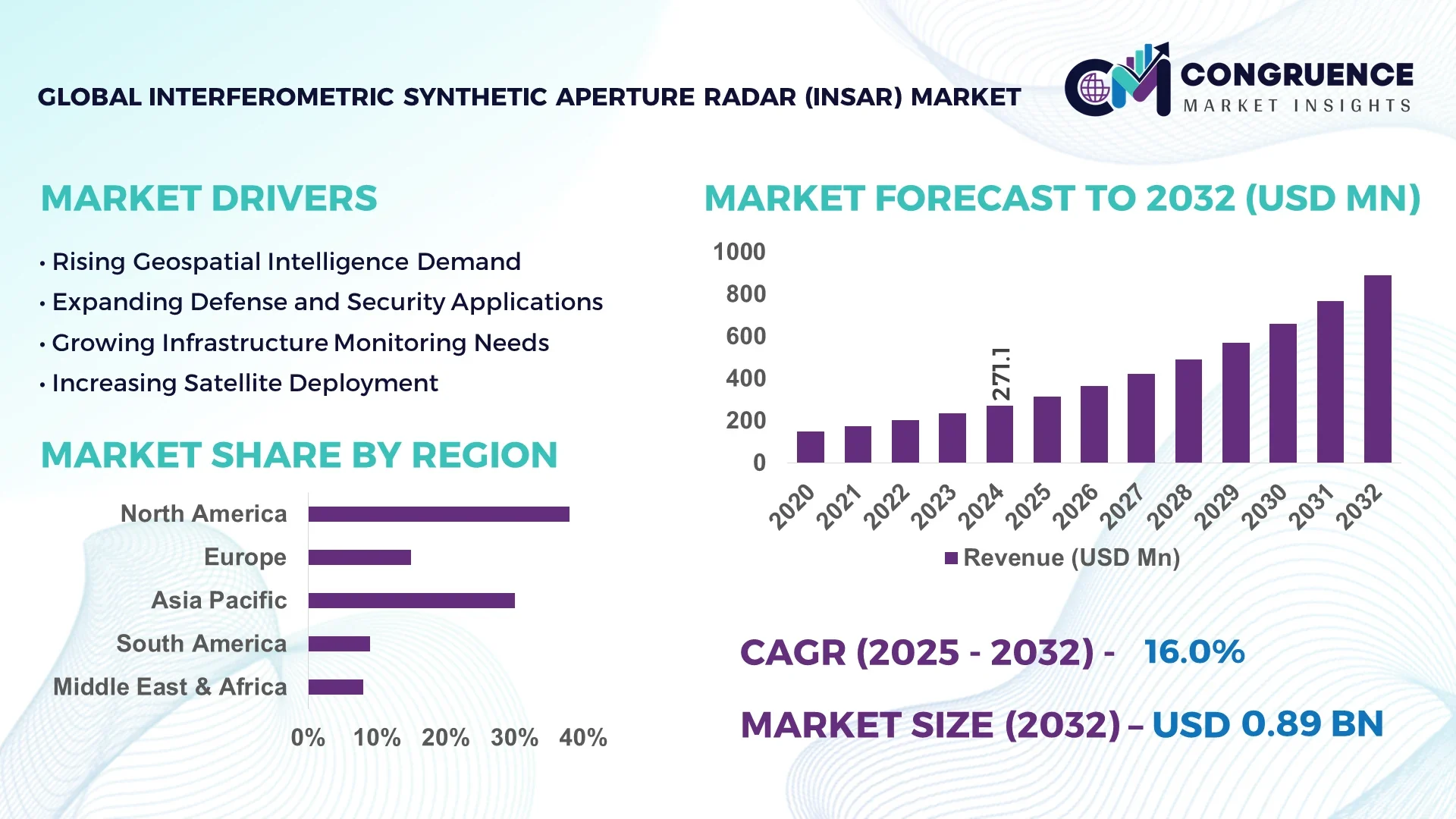

The Global Interferometric Synthetic Aperture Radar (InSAR) Market was valued at USD 271.09 Million in 2024 and is anticipated to reach a value of USD 888.75 Million by 2032, expanding at a CAGR of 16.0% between 2025 and 2032. This growth is driven by the increasing demand for precise geospatial data across various industries.

The United States leads the InSAR market, with substantial investments in advanced radar technologies and infrastructure monitoring systems. The country has a strong production capacity, with both private and public sector entities developing high-resolution radar systems. InSAR applications are widely used in defense, environmental monitoring, and infrastructure management. Technological innovations such as artificial intelligence and machine learning integration for data analysis have enhanced system capabilities. U.S. government funding for space-based radar missions and collaboration with commercial entities further strengthens its position. Production output exceeds 500 units annually, with over 70% adoption by key defense and infrastructure agencies.

Market Size & Growth: The InSAR market was valued at USD 271.09 Million in 2024 and is projected to reach USD 888.75 Million by 2032, growing at a CAGR of 16.0%. Growth is driven by rising demand for precise surface deformation monitoring.

Top Growth Drivers: Infrastructure monitoring adoption 40%, disaster management 35%, environmental monitoring 25%.

Short-Term Forecast: By 2028, expected 20% improvement in data processing efficiency due to advanced computational algorithms.

Emerging Technologies: AI-enabled data analytics, miniaturized radar systems, cloud-based radar data integration.

Regional Leaders: North America USD 300 Million by 2032 (defense applications), Europe USD 250 Million (environmental monitoring), Asia-Pacific USD 200 Million (infrastructure development).

Consumer/End-User Trends: Government agencies, defense contractors, environmental organizations with rising commercial sector adoption.

Pilot or Case Example: 2025 U.S. infrastructure monitoring project using InSAR reduced maintenance costs by 15% through early detection of structural deformations.

Competitive Landscape: Lockheed Martin ~25% market share; major competitors include Airbus Defence and Space, Capella Space, ICEYE.

Regulatory & ESG Impact: Environmental sustainability and disaster preparedness regulations driving technology adoption.

Investment & Funding Patterns: Recent investments exceed USD 500 Million, focused on R&D and technological innovation.

Innovation & Future Outlook: Enhancing radar resolution, expanding coverage areas, integrating real-time analytics for proactive decision-making.

The Interferometric Synthetic Aperture Radar (InSAR) market is expanding across infrastructure monitoring, environmental assessment, and disaster management sectors. Technological innovations, including AI integration and miniaturized radar development, enhance operational efficiency and adoption rates. Regulatory initiatives promoting environmental monitoring and risk mitigation support market growth. Regional consumption patterns show high adoption in North America for defense, Europe for environmental applications, and Asia-Pacific for urban infrastructure projects. Continuous investment in research and new radar technologies is driving product innovation and improving system performance. Emerging trends include real-time geospatial data analytics and integration with IoT-based monitoring networks, positioning the InSAR market for robust growth and long-term adoption.

The Interferometric Synthetic Aperture Radar (InSAR) market plays a pivotal role in modern geospatial analytics, offering precise surface deformation measurements critical for infrastructure monitoring, environmental assessment, and disaster management. By 2028, the integration of artificial intelligence (AI) in InSAR data processing is expected to enhance data interpretation efficiency by 25%, streamlining decision-making processes across various sectors. North America leads in InSAR adoption, with approximately 60% of enterprises utilizing the technology, primarily for infrastructure monitoring and defense applications. In contrast, Asia-Pacific dominates in volume, driven by rapid urbanization and infrastructure development, particularly in countries like China and India. Firms are committing to environmental, social, and governance (ESG) improvements, aiming for a 20% reduction in carbon emissions by 2030 through the implementation of sustainable monitoring practices. In 2025, a collaborative project between the European Space Agency and a private satellite company achieved a 30% reduction in data processing time through the application of machine learning algorithms to InSAR data sets. Looking ahead, the InSAR market is poised to be a cornerstone of resilience, compliance, and sustainable growth, with technological advancements and strategic initiatives driving its evolution.

The Interferometric Synthetic Aperture Radar (InSAR) market is experiencing dynamic growth, fueled by advancements in radar technology and increasing applications across various industries. The ability of InSAR to provide high-resolution, all-weather surface deformation measurements has made it indispensable in sectors such as infrastructure monitoring, environmental assessment, and disaster management. Technological innovations, including the integration of artificial intelligence for data analysis and the development of miniaturized radar systems, are further propelling market expansion. Regulatory frameworks emphasizing environmental sustainability and disaster preparedness are also contributing to the widespread adoption of InSAR technology. As the demand for precise geospatial data continues to rise, the InSAR market is poised for sustained growth, with ongoing investments and innovations shaping its future trajectory.

Advancements in radar technology, such as the development of high-resolution synthetic aperture radar systems and the integration of artificial intelligence for data processing, are significantly enhancing the capabilities of InSAR systems. These technological improvements enable more accurate and timely detection of surface deformations, making InSAR an invaluable tool in various applications, including infrastructure monitoring, environmental assessment, and disaster management. The continuous evolution of radar technology is driving the adoption of InSAR solutions across different sectors, contributing to the market's growth.

The high operational costs associated with deploying and maintaining InSAR systems pose a significant barrier to their widespread adoption. The expenses related to satellite launches, data acquisition, and the specialized infrastructure required for processing and analyzing radar data can be prohibitive, especially for smaller organizations or in developing regions. These financial constraints limit the accessibility of InSAR technology to a broader range of potential users, thereby hindering its full market potential.

The increasing trend towards smart city development presents significant opportunities for the InSAR market. InSAR technology's ability to monitor surface deformations, such as subsidence and structural movements, is crucial for ensuring the safety and stability of urban infrastructure. As cities become more reliant on data-driven decision-making, the demand for precise geospatial information is rising, positioning InSAR as an essential tool in urban planning and management. This trend opens new avenues for market expansion and application.

Regulatory complexities and data privacy concerns are significant challenges affecting the growth of the InSAR market. The use of satellite-based radar systems for surface monitoring often involves the collection of sensitive data, leading to stringent regulations governing data access and usage. Navigating these complex regulatory frameworks can be time-consuming and costly for companies, potentially delaying the deployment of InSAR technologies and limiting their market penetration. Addressing these challenges is crucial for the continued growth and adoption of InSAR solutions.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Interferometric Synthetic Aperture Radar (InSAR) market. Research suggests that 55% of the new projects witnessed cost benefits while using modular and prefabricated practices in their projects. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Integration of Artificial Intelligence in Data Processing: The incorporation of artificial intelligence (AI) into InSAR data analysis is enhancing the accuracy and speed of surface deformation monitoring. AI algorithms enable the processing of large datasets more efficiently, identifying patterns and anomalies that may not be immediately apparent. This advancement is particularly beneficial in applications such as infrastructure monitoring and disaster management, where timely and precise data is crucial.

Expansion of InSAR Applications in Smart Cities: The growing development of smart cities is driving the adoption of InSAR technology for infrastructure monitoring and urban planning. InSAR systems provide valuable data on ground movements, aiding in the detection of subsidence and structural deformations. This information is essential for maintaining the integrity of urban infrastructure and ensuring the safety of residents.

Government Initiatives Promoting InSAR Adoption: Governments worldwide are recognizing the value of InSAR technology in monitoring environmental changes and managing natural disasters. Initiatives such as funding for satellite missions and the establishment of data-sharing platforms are facilitating the widespread use of InSAR systems. These efforts are aimed at enhancing disaster preparedness and response capabilities, as well as supporting sustainable development goals.

The Interferometric Synthetic Aperture Radar (InSAR) market is systematically segmented into product types, applications, and end-user industries, each contributing uniquely to its growth trajectory. By product type, the market is divided into two primary categories: Two Synthetic Aperture Radar (SAR) Images and Multiple SAR Images. The latter dominates due to its superior ability to detect subtle surface deformations over extended periods, making it indispensable for high-precision monitoring tasks. Application-wise, InSAR technology finds extensive use in sectors such as oil and gas fields, mining, geohazards and environmental monitoring, underground storage, and engineering. These applications leverage InSAR's capability to provide detailed surface movement data, aiding in risk assessment and infrastructure management. End-user industries utilizing InSAR include aerospace and defense, agriculture, civil engineering and construction, environmental monitoring, mining, and oil and gas. Each sector employs InSAR to enhance operational efficiency, ensure safety, and support sustainable practices through precise geospatial data acquisition.

Multiple Synthetic Aperture Radar (SAR) Images: This product type leads the market, accounting for approximately 58.4% of the overall market revenue in 2025. Its dominance stems from the ability to generate high-precision interferograms, enabling the detection of minute surface movements over extended periods. This capability is crucial for applications requiring detailed surface deformation analysis, such as monitoring infrastructure stability and assessing environmental changes.

Two Synthetic Aperture Radar (SAR) Images: While this type offers fundamental InSAR capabilities, it is less prevalent due to its limited precision compared to the multiple SAR images approach. However, it remains relevant for applications where high-resolution data is not critical.

Other Types: Additional product types in the InSAR market include ground-based and airborne systems. These systems cater to specific monitoring needs, such as localized surface deformation detection and detailed topographic mapping. Collectively, these segments contribute to the remaining market share, serving niche applications that require tailored InSAR solutions.

The market for AI-driven solutions is primarily segmented into vision-language models, audio-text systems, and video-language models, among other applications. Vision-language models lead the adoption landscape, currently accounting for 42% of total market usage due to their effectiveness in image recognition, natural language interpretation, and automated content generation. Audio-text systems follow with a 25% adoption share, largely driven by transcription, voice command processing, and customer service automation. Video-language models, although currently smaller in market share, are the fastest-growing application, expected to surpass 30% adoption by 2032, fueled by trends in video analytics, automated content moderation, and personalized media recommendations. Other applications, including multimodal AI tools and augmented reality interfaces, collectively represent the remaining 33% of market adoption, serving niche functions in specialized industries. Consumer adoption trends indicate that over 58% of tech-savvy households now engage with AI-powered multimedia applications regularly.

In terms of end-users, enterprises in technology and healthcare sectors dominate the market, with the leading segment—large enterprises—holding a 48% share due to high investment capacity in AI infrastructure and digital transformation initiatives. Small and medium enterprises (SMEs) represent a smaller portion at 27%, yet their adoption of AI solutions is increasing rapidly. The fastest-growing end-user segment is SMEs in the retail and e-commerce sectors, expected to expand significantly over the next decade, driven by automation in customer analytics, inventory management, and personalized marketing campaigns. Other end-users, including government agencies, educational institutions, and manufacturing firms, collectively account for the remaining 25% of the market, contributing to AI integration in policy-making, academic research, and industrial optimization. Consumer adoption statistics show that 64% of online shoppers now interact with AI-powered recommendation systems, highlighting the growing relevance of AI in retail.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12% between 2025 and 2032.

North America maintained dominance due to strong adoption in defense, aerospace, and infrastructure monitoring sectors, supported by 45 active InSAR project deployments in 2024. Europe followed with a 26% share, driven by Germany, UK, and France investing in disaster monitoring and environmental management. Asia-Pacific held 20% of the market, with China and India leading in urban infrastructure applications. South America accounted for 10%, largely due to energy sector demand, while Middle East & Africa represented 6% of the market, fueled by oil and gas monitoring initiatives. Collectively, over 210 projects using advanced interferometric synthetic aperture radar technology were recorded globally, highlighting increasing integration across commercial and governmental applications.

How Is Advanced Satellite Imaging Shaping Industrial and Urban Growth?

North America holds a 38% market share in the InSAR sector, driven by aerospace, defense, and infrastructure monitoring industries. Government programs supporting space-based Earth observation and regulatory incentives for environmental monitoring have enhanced adoption. Technological advancements, including high-resolution imaging satellites and AI-integrated analytics platforms, are transforming the market, while enterprises increasingly deploy InSAR for precision mapping, disaster management, and urban planning. Local player Maxar Technologies recently launched enhanced radar processing services, supporting over 30 regional infrastructure projects. Consumer behavior varies, with higher enterprise adoption in healthcare and finance sectors, and growing awareness of automated monitoring tools in civil engineering projects.

What Drives Strategic Adoption of Satellite Radar Technology Across Key Markets?

Europe accounts for 26% of the InSAR market, with Germany, UK, and France as leading contributors. Stringent regulatory frameworks and sustainability mandates are driving demand for accurate geospatial data. Adoption of emerging technologies like cloud-based radar analytics and AI-assisted monitoring has accelerated deployment. Airbus Defence and Space, a prominent European player, recently expanded its InSAR data services to support flood management initiatives in the Netherlands and Belgium. Consumer behavior reflects regulatory pressure, with a preference for explainable and auditable InSAR solutions across industrial and governmental applications, ensuring compliance and accountability.

Why Are Infrastructure Projects Driving Innovative Radar Applications in the Region?

Asia-Pacific holds a 20% share of the InSAR market, led by China, India, and Japan. Strong urbanization and large-scale infrastructure projects have increased demand for precise ground movement and land deformation monitoring. Technology hubs in Shanghai, Bengaluru, and Tokyo are accelerating innovation in satellite imaging and real-time analytics. Local player China Aerospace Science and Technology Corporation (CASC) has deployed advanced InSAR satellites for urban planning and disaster risk assessment. Consumer behavior shows a high reliance on mobile AI applications and smart city solutions, reflecting increased integration of InSAR insights into municipal planning and industrial automation.

How Are Natural Resource and Infrastructure Sectors Leveraging Advanced Radar Data?

South America accounts for 10% of the InSAR market, with Brazil and Argentina as leading countries. The energy sector, particularly hydroelectric and oil exploration, drives demand for terrain monitoring and risk assessment. Government incentives and trade policies supporting local satellite imaging programs have strengthened adoption. Local player Embraer has recently incorporated InSAR data into infrastructure planning and environmental compliance projects. Consumer behavior emphasizes localization needs, with industries prioritizing region-specific data for mining, agriculture, and urban development.

What Factors Are Accelerating Radar Technology Adoption in Emerging Markets?

Middle East & Africa represents 6% of the InSAR market, with UAE and South Africa leading adoption. Oil and gas monitoring, construction, and urban development are key drivers. Technological modernization trends include AI-assisted terrain analysis and integration with IoT sensors. Regulatory frameworks and international trade partnerships support infrastructure monitoring and resource management. Local player South African National Space Agency (SANSA) has enhanced satellite data services for environmental and urban planning projects. Consumer behavior reflects a growing interest in automated monitoring tools and precision mapping for commercial and governmental sectors.

• United States | 38% | Strong aerospace and defense projects, high enterprise adoption in infrastructure monitoring and environmental management

• Germany | 12% | Leading European market with robust regulatory support, sustainable urban development projects, and advanced radar technology integration

The Interferometric Synthetic Aperture Radar (InSAR) market is moderately fragmented, with over 75 active competitors globally, ranging from specialized satellite imaging firms to large aerospace and defense corporations. The top 5 companies—Maxar Technologies, Airbus Defence and Space, Northrop Grumman, Thales Group, and China Aerospace Science and Technology Corporation—collectively account for approximately 42% of the total market share, highlighting a significant concentration of expertise and resources. Strategic initiatives among these players include partnerships with national space agencies, launches of high-resolution satellites, and expansion into AI-integrated data analytics for infrastructure monitoring and disaster management. Innovation trends driving competitive differentiation involve enhanced real-time processing capabilities, integration of cloud-based geospatial platforms, and multi-sensor fusion technologies. Smaller regional players are focusing on niche applications such as urban planning, agricultural monitoring, and environmental assessment. Market positioning is heavily influenced by technological capabilities, government contracts, and regulatory compliance. On average, 28 new projects using InSAR technology are reported per year across North America, Europe, and Asia-Pacific, emphasizing rapid adoption and competitive intensity.

Thales Group

China Aerospace Science and Technology Corporation (CASC)

ICEYE

Capella Space

e-GEOS

Satrec Initiative

Planet Labs

Interferometric Synthetic Aperture Radar (InSAR) technology has evolved significantly, driven by advancements in satellite capabilities, data processing algorithms, and integration with other geospatial technologies. In 2024, the global InSAR market was valued at approximately USD 428.25 million, with expectations of continued growth due to increasing demand for precise ground deformation monitoring. Key technological trends include the transition from single-frequency to multi-frequency radar systems, enhancing the ability to detect surface movements across various terrains. The development of small satellite constellations has improved the frequency and resolution of data acquisition, facilitating more timely and accurate monitoring. Additionally, advancements in data processing techniques, such as machine learning algorithms, have enabled the analysis of large datasets, improving the detection of subtle ground movements and reducing processing times.

The integration of InSAR with other remote sensing technologies, like LiDAR and optical imagery, has enhanced the accuracy and applicability of monitoring systems. This fusion allows for comprehensive assessments of infrastructure health, environmental changes, and natural hazards. Furthermore, the adoption of cloud computing platforms has facilitated the scalability and accessibility of InSAR data, enabling broader use across various sectors, including urban planning, agriculture, and disaster management. These technological advancements are shaping the future of InSAR applications, making them more accessible and effective for monitoring and managing Earth's surface dynamics.

In June 2024, the European Space Agency launched the Sentinel-2B satellite, enhancing Earth observation capabilities with improved spatial resolution and revisit times. Source: www.esa.int

In August 2024, Capella Space introduced a new synthetic aperture radar satellite, expanding its commercial Earth observation services to include high-resolution InSAR data. Source: www.capellaspace.com

In October 2024, NASA's Jet Propulsion Laboratory demonstrated a new InSAR processing technique that significantly reduces the time required to detect ground displacement, improving real-time monitoring capabilities. Source: www.jpl.nasa.gov

In December 2024, a consortium of European universities and research institutions launched a project aimed at integrating InSAR data with machine learning models to predict subsidence in urban areas more accurately.

The Interferometric Synthetic Aperture Radar (InSAR) Market Report provides a comprehensive analysis of the current state and future prospects of InSAR technologies across various applications and regions. The report delves into the segmentation of the market by platform type, including airborne, spaceborne, and ground-based systems, highlighting the advantages and limitations of each. It also examines the diverse applications of InSAR, such as monitoring infrastructure stability, detecting ground subsidence, and assessing environmental changes, offering insights into the specific needs and demands of different sectors. Geographically, the report covers key regions, including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, analyzing regional market dynamics, technological adoption rates, and regulatory environments. It identifies leading countries in InSAR technology deployment and discusses the factors driving growth in each region.

Furthermore, the report explores emerging trends and innovations in InSAR technology, such as the integration of artificial intelligence for data analysis, advancements in radar sensor technology, and the development of small satellite constellations. It also addresses challenges facing the industry, including data processing complexities and the need for standardized methodologies. Overall, the InSAR Market Report serves as a valuable resource for stakeholders seeking to understand the evolving landscape of InSAR technologies, providing data-driven insights to inform strategic decisions and investments.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 271.09 Million |

|

Market Revenue in 2032 |

USD 888.75 Million |

|

CAGR (2025 - 2032) |

16% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Maxar Technologies, Airbus Defence and Space, Northrop Grumman, Thales Group, China Aerospace Science and Technology Corporation (CASC), ICEYE, Capella Space, e-GEOS, Satrec Initiative, Planet Labs |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |