Reports

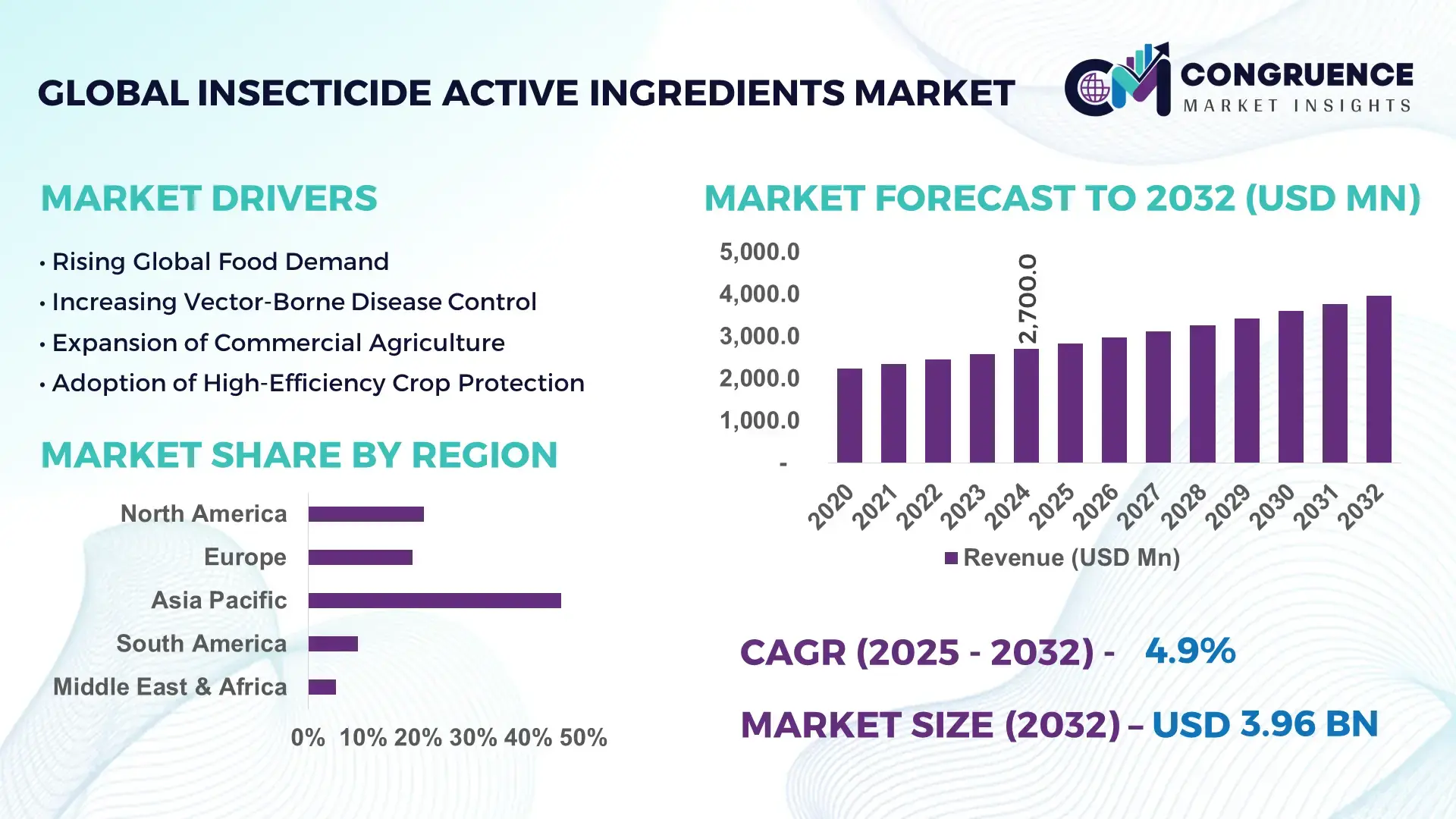

The Global Insecticide Active Ingredients Market was valued at USD 2,700.0 Million in 2024 and is anticipated to reach a value of USD 3,958.8 Million by 2032 expanding at a CAGR of 4.9% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is primarily driven by rising global food demand and increasing adoption of advanced crop protection chemistries to manage pest resistance and improve yield stability.

China dominates the global insecticide active ingredients landscape due to its extensive manufacturing ecosystem and integrated agrochemical value chain. The country hosts over 2,000 registered pesticide manufacturers, with insecticide actives accounting for a significant portion of output. China’s annual production capacity for key insecticide actives such as pyrethroids, organophosphates, and neonicotinoids exceeds 600,000 metric tons. Capital investment in agrochemical manufacturing facilities has surpassed USD 4 billion over the last five years, focusing on process automation, continuous-flow synthesis, and waste treatment upgrades. In agriculture, insecticide actives are widely applied across rice, cotton, maize, and horticulture crops, supporting both domestic consumption and exports. Technological advancements include large-scale adoption of high-efficiency catalytic processes and digital batch monitoring systems, reducing process variability by over 18% and improving active ingredient purity levels beyond 98.5%.

Market Size & Growth: Valued at USD 2,700.0 Million in 2024, projected to reach USD 3,958.8 Million by 2032, expanding at a CAGR of 4.9%, driven by rising pest resistance and higher crop protection intensity.

Top Growth Drivers: Adoption of integrated pest management increased 42%, crop yield efficiency improved by 18%, and demand for vector control solutions rose 27%.

Short-Term Forecast: By 2028, formulation efficiency improvements are expected to reduce active ingredient wastage by 22%.

Emerging Technologies: Microencapsulation, RNA-based insecticides, and precision-targeted synthesis platforms are gaining traction.

Regional Leaders: Asia Pacific projected at USD 1,720.0 Million by 2032 with high-volume agriculture; North America at USD 910.0 Million driven by premium formulations; Europe at USD 820.0 Million supported by regulatory-compliant innovation.

Consumer/End-User Trends: Large-scale farms account for 61% of usage, while controlled-environment agriculture adoption grew 19%.

Pilot or Case Example: In 2023, India deployed a pyrethroid optimization pilot reducing application frequency by 24%.

Competitive Landscape: BASF leads with ~18% share, followed by Bayer, Syngenta, FMC, and Corteva.

Regulatory & ESG Impact: Over 35% of new actives comply with low-toxicity and pollinator-safety standards.

Investment & Funding Patterns: Recent investments exceeded USD 1.6 Billion, focused on green chemistry and capacity upgrades.

Innovation & Future Outlook: AI-driven molecule screening and bio-synthetic hybrids are shaping next-generation pipelines.

The Insecticide Active Ingredients Market supports agriculture, public health, and vector control, with cereals contributing ~46% of consumption and fruits and vegetables ~28%. Innovations in selective toxicity molecules and controlled-release actives are improving efficacy while aligning with tightening environmental regulations. Asia Pacific leads consumption, while Europe drives regulatory-compliant innovation, and future growth is shaped by resistance management and sustainable chemistry adoption.

The Insecticide Active Ingredients Market holds strategic importance as global agriculture faces rising pest pressure, climate variability, and stricter regulatory oversight. Active ingredients form the technological core of crop protection strategies, directly influencing food security and farm productivity. Advanced synthesis technologies such as continuous-flow chemical processing deliver 22% higher production efficiency compared to conventional batch synthesis. Asia Pacific dominates in production volume, while Europe leads in adoption, with nearly 64% of agrochemical enterprises deploying low-toxicity or selective insecticide actives.

Over the next two to three years, by 2027, AI-enabled molecular screening is expected to cut new active ingredient development timelines by 30%, accelerating regulatory-ready innovation. ESG considerations are increasingly central, with manufacturers committing to solvent recovery improvements and targeting a 25% reduction in hazardous waste generation by 2030. Compliance with pollinator protection directives and residue limits is reshaping R&D priorities toward targeted modes of action.

In 2022, Japan achieved a 19% reduction in application rates through the deployment of precision-formulated insecticide actives integrated with smart spraying systems. Strategically, the market is shifting toward resilience through diversified chemistry portfolios, digital-enabled manufacturing, and sustainable compliance frameworks. As a result, the Insecticide Active Ingredients Market is positioned as a foundational pillar supporting regulatory alignment, environmental stewardship, and long-term agricultural productivity.

The Insecticide Active Ingredients Market is influenced by evolving agricultural practices, regulatory frameworks, and technological innovation. Increasing pest resistance is driving demand for novel modes of action, while climate change is expanding pest prevalence across new geographies. Regulatory pressure is simultaneously phasing out older chemistries, accelerating the transition toward selective and environmentally safer active ingredients. Manufacturing dynamics are shaped by capacity consolidation, backward integration of intermediates, and investment in cleaner synthesis routes. Demand patterns vary regionally, with high-volume usage in Asia Pacific and value-driven adoption in North America and Europe. Overall, the market reflects a balance between productivity enhancement, compliance requirements, and sustainability goals.

Increasing resistance has been documented in over 500 insect species globally, pushing growers toward newer active ingredients with differentiated modes of action. Resistance-related crop losses account for nearly 20% of yield reduction in major cereals, intensifying reliance on advanced insecticides. This has resulted in higher adoption of combination actives and rotational chemistry programs. Manufacturers are investing in resistance-breaking molecules, improving efficacy consistency and extending product lifecycles.

More than 40% of legacy insecticide actives face usage restrictions or phase-outs due to environmental and toxicological concerns. Compliance costs related to registration, testing, and reformulation have increased operational burdens, particularly for small and mid-sized producers. Regulatory uncertainty delays commercialization timelines and limits the availability of certain broad-spectrum actives in developed markets.

Bio-derived and selective insecticide actives are gaining momentum, with adoption rising 31% in integrated pest management systems. These actives offer reduced non-target impact and align with sustainability goals. Expanding horticulture and organic farming segments are creating new demand pockets for biologically inspired chemistries.

Active ingredient production depends on multi-step chemical intermediates, with over 60% sourced globally. Disruptions in raw material availability, energy costs, and logistics inflate production risks. Maintaining consistent quality and regulatory compliance across distributed supply chains remains a critical operational challenge.

Shift Toward Precision-Targeted Actives: Over 48% of new insecticide actives launched since 2021 feature selective modes of action, reducing non-target exposure by up to 35% and lowering application volumes by 21%.

Growth of Microencapsulation Technologies: Adoption of encapsulated actives increased 39%, improving field persistence by 28% and reducing volatilization losses by 18%.

Integration of Digital Manufacturing Controls: Smart reactors and real-time analytics are now used in 44% of large-scale facilities, cutting batch deviation rates by 26% and improving yield consistency.

Rising Use in Vector Control Programs: Public health applications expanded 23%, with insecticide actives contributing to a 32% reduction in vector density across monitored urban regions.

The Insecticide Active Ingredients Market is segmented by type, application, and end-user, reflecting varied agronomic needs, regulatory environments, and adoption behaviors across regions. By type, chemical classes differ in efficacy, persistence, and resistance profiles, shaping usage patterns across crops and climates. Application-wise, demand is closely tied to crop intensity, pest pressure, and public health priorities, with agriculture remaining the dominant consumption area. End-user segmentation highlights the role of large-scale commercial farming, government-led vector control programs, and professional pest management services. Across segments, regulatory compliance, resistance management, and sustainability targets increasingly influence purchasing decisions. Adoption trends indicate a gradual shift toward selective and lower-toxicity actives, while traditional broad-spectrum chemistries continue to play a role in high-pressure pest environments. This segmentation structure enables suppliers to align product portfolios with evolving agronomic practices, policy frameworks, and end-user performance expectations.

The market by type includes organophosphates, pyrethroids, neonicotinoids, carbamates, diamides, and other niche chemistries. Pyrethroids currently account for approximately 34% of total active ingredient usage due to their broad-spectrum efficacy, rapid knockdown action, and compatibility with multiple crop systems. Neonicotinoids represent around 27%, favored for systemic activity and seed treatment applications. However, adoption of diamide insecticides is rising fastest, expanding at an estimated 6.2% CAGR, driven by their novel modes of action and effectiveness against resistant lepidopteran pests. Organophosphates and carbamates together contribute a combined 29%, largely retained in regions with cost-sensitive farming and legacy pest control programs, though their use is increasingly regulated. Other emerging chemistries, including spinosyns and insect growth regulators, account for the remaining 10%, serving niche and resistance-management roles.

By application, agricultural crop protection dominates with nearly 72% of total usage, reflecting intensive insect pressure in cereals, oilseeds, fruits, and vegetables. Public health and vector control applications account for about 18%, driven by mosquito and disease-vector management programs, while household and commercial pest control represent roughly 10%. While crop protection leads, vector control applications are growing fastest at an estimated 5.8% CAGR, supported by expanding urban populations and climate-driven increases in vector-borne disease incidence. Within agriculture, cereals account for the largest application share, followed by fruits and vegetables, which show higher adoption of selective actives. In 2024, more than 41% of large farming enterprises globally reported increasing rotation of insecticide actives to manage resistance.

Commercial agriculture producers constitute the leading end-user group, representing approximately 64% of total demand, driven by large acreage cultivation and mechanized application practices. Government and municipal bodies engaged in vector control account for around 21%, while professional pest management companies contribute close to 15%. Among these, professional pest management services are the fastest-growing end-user segment, expanding at an estimated 5.5% CAGR, supported by rising urbanization and stricter hygiene regulations. Large-scale farms continue to prioritize cost-efficiency and resistance management, while government programs emphasize safety and long residual efficacy. In 2024, nearly 46% of professional pest control operators reported adopting newer-generation actives to meet regulatory and client safety requirements.

Asia-Pacific accounted for the largest market share at 46% in 2024 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 5.6% between 2025 and 2032.

Asia-Pacific’s leadership is supported by high agricultural intensity, with over 58% of global insecticide active ingredient consumption linked to staple crops such as rice, wheat, and cotton. North America followed with nearly 21% share, driven by technologically advanced farming systems and higher per-hectare chemical application rates. Europe represented approximately 19%, reflecting strong demand for regulatory-compliant and low-toxicity actives. South America accounted for close to 9%, supported by large-scale soybean and maize cultivation, while Middle East & Africa contributed around 5%, driven by vector control programs and expanding commercial agriculture. Regional differences in pest pressure, crop mix, regulatory frameworks, and manufacturing capacity continue to shape demand patterns and investment priorities globally.

North America holds an estimated 21% share of global insecticide active ingredient consumption, supported by large-scale commercial farming and high-input agricultural systems. Row crops such as corn, soybean, and cotton account for over 62% of regional usage. Regulatory initiatives emphasizing pollinator safety and residue limits are influencing product selection, accelerating the shift toward selective and reduced-risk actives. Digital agriculture adoption is high, with nearly 48% of large farms integrating precision application technologies that optimize active ingredient usage. Technological advances include data-driven resistance monitoring and automated formulation controls. A leading regional agrochemical producer has expanded domestic synthesis capacity by 15%, focusing on next-generation actives with improved environmental profiles. Consumer behavior shows strong preference for productivity-enhancing solutions, with higher adoption among large agribusiness operators compared to small farms.

Europe accounts for approximately 19% of the global market, with Germany, France, and Spain collectively contributing over 55% of regional demand. Stringent regulatory oversight has reduced reliance on older chemistries, increasing adoption of selective insecticide actives by 34% over the past five years. Sustainability initiatives emphasize reduced environmental persistence and lower toxicity thresholds. Emerging technologies such as microencapsulation and precision-dose formulations are increasingly adopted, improving field efficiency by 20%. A major regional manufacturer has transitioned more than 40% of its insecticide portfolio to low-residue formulations. Consumer behavior reflects regulatory pressure, with growers prioritizing compliance-ready products even at higher per-unit costs.

Asia-Pacific leads global consumption, representing nearly 46% of total market volume. China, India, and Japan together account for over 70% of regional demand. High cropping intensity, multiple annual harvest cycles, and persistent pest pressure drive sustained usage. Manufacturing capacity is extensive, with more than 600,000 metric tons of annual insecticide active ingredient output across the region. Innovation hubs in China and Japan are advancing continuous-flow synthesis and high-purity processing. A leading domestic producer recently improved production efficiency by 18% through digital batch optimization. Consumer behavior is shaped by cost sensitivity and scale, with widespread adoption among smallholder and commercial farmers alike.

South America contributes approximately 9% of global demand, led by Brazil and Argentina, which together represent over 75% of regional consumption. Soybean, maize, and sugarcane cultivation drives high seasonal usage. Infrastructure improvements in logistics and port connectivity have reduced distribution lead times by 14%. Government policies supporting agricultural exports encourage consistent insecticide application to protect yields. A regional agrochemical firm expanded formulation facilities to support locally sourced actives, improving supply reliability. Consumer behavior is closely tied to commodity price cycles, with adoption intensifying during peak planting seasons.

Middle East & Africa accounts for about 5% of the global market but shows the fastest expansion trajectory. Demand is driven by public health vector control programs and growing commercial agriculture in countries such as South Africa, Egypt, and the UAE. Government-led initiatives support insecticide usage to combat malaria and crop pests, covering over 120 million hectares of treated land annually. Technological modernization includes improved storage and application systems, reducing product loss by 16%. A regional distributor has partnered with global manufacturers to introduce longer-residual actives. Consumer behavior reflects strong institutional purchasing alongside gradual uptake by commercial farms.

China – 32% Market Share: Dominates the Insecticide Active Ingredients Market due to extensive manufacturing capacity and vertically integrated supply chains.

United States – 18% Market Share: Holds a leading position supported by high-intensity commercial agriculture and advanced adoption of precision pest management solutions.

The Insecticide Active Ingredients Market operates within a moderately consolidated yet highly competitive structure, shaped by scale-driven multinational corporations and a wide base of regional and specialty manufacturers. Globally, the market includes over 120 active producers of insecticide technicals, ranging from vertically integrated chemical majors to contract manufacturers and generic active ingredient suppliers. The top five companies collectively account for approximately 42–45% of the total market presence, indicating a balance between consolidation at the top and fragmentation at regional levels.

Large players maintain strong market positioning through diversified active ingredient portfolios spanning more than 50 registered molecules, global regulatory approvals across 80+ countries, and annual R&D pipelines exceeding 10–15 new formulations or actives under evaluation. Strategic initiatives include cross-border manufacturing partnerships, licensing agreements for patented molecules, and selective mergers aimed at expanding biological and resistance-management portfolios. Between 2023 and 2024, the industry recorded more than 18 notable product launches and reformulations, primarily targeting resistance mitigation and reduced environmental persistence.

Innovation is a critical competitive lever. Over 40% of leading manufacturers have integrated nano-formulation, controlled-release systems, or precision-application compatibility into their active ingredient strategies. At the same time, regional players compete aggressively on cost efficiency, local registrations, and supply reliability, particularly in Asia-Pacific and Latin America. Overall, competition is defined by innovation depth, regulatory readiness, manufacturing scale, and geographic reach, making the market resilient but continuously evolving.

BASF SE

Bayer AG

UPL Limited

Sumitomo Chemical Co., Ltd.

PI Industries Limited

Technology advancement is reshaping the Insecticide Active Ingredients Market, with strong emphasis on efficiency, selectivity, and regulatory compatibility. One of the most impactful developments is the adoption of controlled-release and microencapsulation technologies, now applied in approximately 45% of newly registered insecticide actives. These systems improve field persistence by 20–30% while reducing non-target exposure and volatilization losses.

Another key innovation area is novel modes of action, particularly diamide, isoxazoline, and peptide-inspired chemistries designed to address resistance in lepidopteran and sucking pests. Resistance-monitoring databases indicate that over 500 pest species globally show reduced sensitivity to legacy chemistries, accelerating demand for differentiated actives. Manufacturers are also investing in continuous-flow synthesis and digital reactor control, which have reduced batch variability by 15–20% and improved purity consistency beyond 98% technical grade.

Biologically derived and RNA-interference-based insecticide actives are emerging as strategic additions to synthetic portfolios. Although still representing less than 10% of total volume, these technologies are expanding rapidly due to favorable environmental profiles and compatibility with integrated pest management programs. Additionally, precision agriculture compatibility is becoming standard, with more than 50% of new active ingredients designed for drone or sensor-assisted application systems. Collectively, these technologies are redefining competitiveness by aligning performance gains with sustainability and compliance objectives.

In February 2025, BASF initiated global registration of Prexio Active, a new Group 4E insecticide active ingredient designed for comprehensive control of rice hopper species, with regulatory dossiers submitted across key Asia-Pacific markets ahead of commercial rollout. Source: www.basf.com

In December 2025, Syngenta secured EPA registration for its PLINAZOLIN® technology, enabling use in multiple crop types including corn, cotton, vegetables, and cereals and marking a significant regulatory milestone for resistance management solutions. Source: www.syngenta-us.com

In 2023, FMC India’s Rynaxypyr® active insect control technology was recognized at the Best Brands Conclave for its performance across 16 major crops, reinforcing its position as a leading active ingredient in agricultural pest management. Source: www.ag.fmc.com

In May 2024, BASF launched Efficon® insecticide powered by the novel active ingredient Axalion® Active, introducing a new IRAC Group 36 chemistry with no known cross-resistance and long-lasting systemic control against aphids, jassids, and whiteflies for cotton and vegetables in India and Australia, addressing pests that cause 35–40 % yield losses. Source: www.basf.com

The Insecticide Active Ingredients Market Report delivers a comprehensive evaluation of the global landscape for technical insecticidal compounds used in agricultural and public health applications. The scope encompasses major chemical classes such as pyrethroids, neonicotinoids, organophosphates, carbamates, diamides, and emerging bio-inspired actives, analyzing their functional roles, regulatory status, and deployment environments.

Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, assessing regional production footprints, consumption intensity, and policy-driven adoption patterns. Application coverage includes cereal crops, oilseeds, fruits and vegetables, plantation crops, and vector control programs, with detailed insights into pest categories and treatment methods such as foliar, soil, and seed-applied actives.

The scope further extends to technology integration, including formulation science, controlled-release systems, digital manufacturing, and precision-application compatibility. Industry focus areas include resistance management strategies, sustainability-aligned chemistry, and supply chain resilience. By combining segmentation, competitive structure, innovation pathways, and regional analysis, the report provides decision-makers with a clear understanding of current positioning and future strategic opportunities within the Insecticide Active Ingredients Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 2,700.0 Million |

| Market Revenue (2032) | USD 3,958.8 Million |

| CAGR (2025–2032) | 4.9% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Syngenta AG, Corteva Agriscience, FMC Corporation, BASF SE, Bayer AG, UPL Limited, Sumitomo Chemical Co., Ltd., PI Industries Limited |

| Customization & Pricing | Available on Request (10% Customization Free) |