Reports

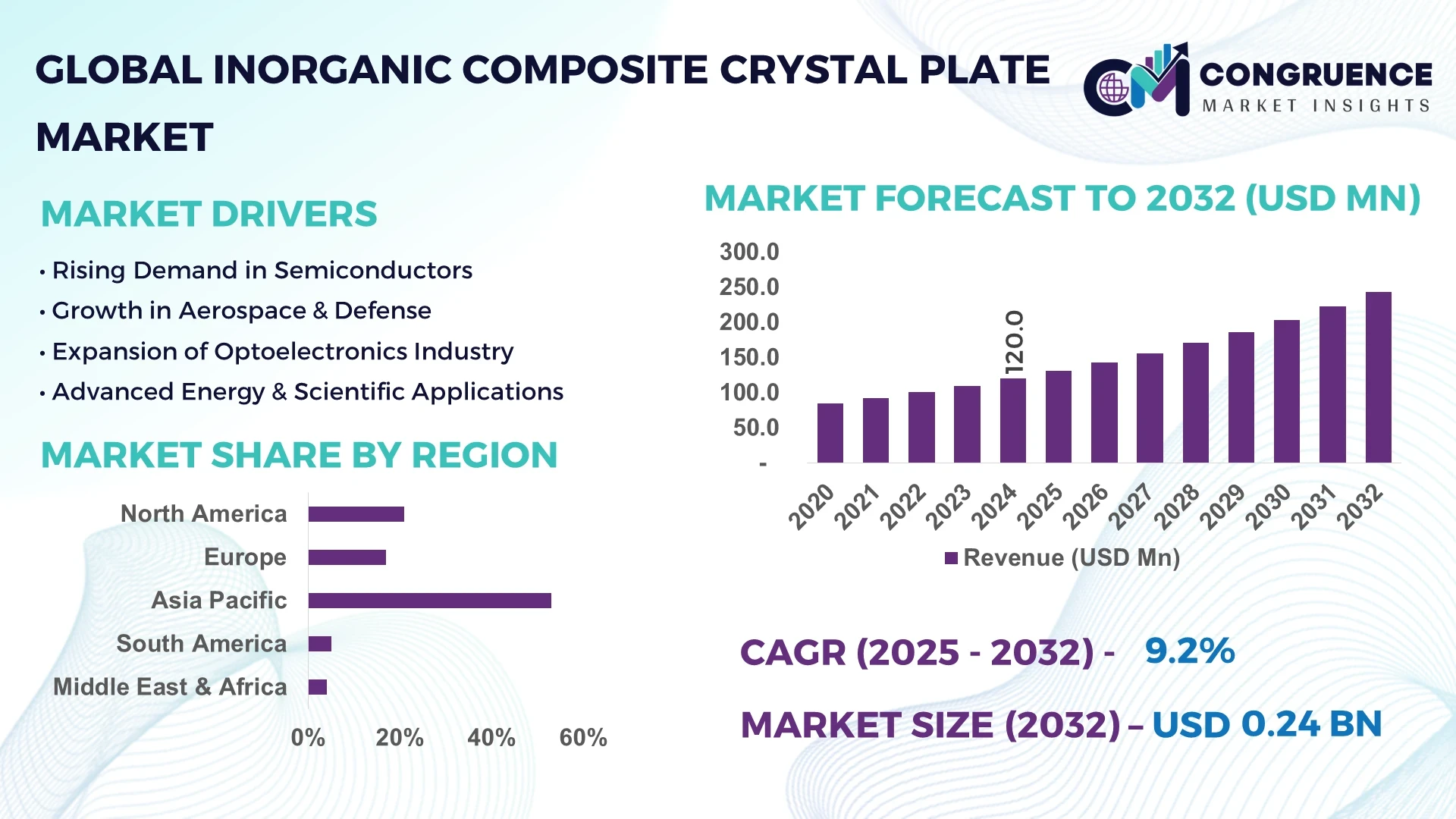

The Global Inorganic Composite Crystal Plate Market was valued at USD 120.0 Million in 2024 and is anticipated to reach a value of USD 242.6 Million by 2032, expanding at a CAGR of 9.2% between 2025 and 2032. This growth is primarily driven by the increasing need for high-precision crystal substrates in semiconductor fabrication, photonics, and aerospace applications, where dimensional stability and thermal resistance are critical.

China leads the global Inorganic Composite Crystal Plate Market with its vast production capacity, advanced processing infrastructure, and sustained technological investment exceeding USD 95 million in 2024. The nation’s crystal synthesis facilities collectively achieve an estimated 60,000-unit annual output, serving high-end applications in aerospace optics, semiconductor wafer substrates, and advanced photonics. Continuous upgrades in automated inspection and AI-driven yield optimization have improved production efficiency by 18%, while domestic adoption of energy-efficient sintering technology has cut overall energy use per ton of output by 12%, positioning China as a global manufacturing hub for inorganic crystal technologies.

Market Size & Growth: Valued at USD 120.0 Million in 2024 and projected to reach USD 242.6 Million by 2032, growing at a CAGR of 9.2% due to rapid expansion in optoelectronic and semiconductor end-uses.

Top Growth Drivers: 42% adoption in photonic components, 33% efficiency improvement in fabrication yield, and 28% enhancement in product consistency via AI-driven inspection.

Short-Term Forecast: By 2028, integration of robotic automation and precision alignment systems is expected to reduce fabrication cost by 19% and increase throughput by 23%.

Emerging Technologies: Nano-layer bonding, laser-assisted wafer slicing, and intelligent optical alignment are among the top trends improving material uniformity and cutting precision.

Regional Leaders: Asia Pacific projected to reach USD 128.4 Million by 2032 driven by mass production capacity; North America forecasted at USD 58.6 Million due to semiconductor R&D intensity; Europe anticipated at USD 41.7 Million propelled by aerospace-grade material innovation.

Consumer/End-User Trends: Key end-users include photonics manufacturers, defense contractors, and electronics producers, showing steady adoption of defect-free, thermally stable crystal substrates.

Pilot or Case Example: In 2024, Japan’s Nitto Electric achieved a 22% reduction in surface micro-defects through advanced thermal-gradient growth methods, enhancing optical clarity and yield.

Competitive Landscape: Market leader—CrystalTech Materials—holds approximately 17% market share, followed by Shanghai Advanced Crystal, Sumitomo Electric, Corning Inc., and Heraeus Group.

Regulatory & ESG Impact: Compliance with ISO 14001 and REACH frameworks has driven a 25% rise in environmentally responsible crystal production and recycling initiatives.

Investment & Funding Patterns: Global investments exceeded USD 210 million in 2023–2024 across crystal material R&D and precision fabrication infrastructure, emphasizing sustainability and digital manufacturing.

Innovation & Future Outlook: The emergence of ultra-thin composite plates, multi-layer crystal alignment systems, and AI-based defect mapping will shape next-generation optical and semiconductor components.

The Inorganic Composite Crystal Plate Market serves key industries such as semiconductors, aerospace, photonics, and precision instrumentation. Recent innovations in nano-structured coatings, thermally resilient crystal composites, and environmentally optimized manufacturing processes are transforming production efficiency and product reliability across major consuming regions.

The Inorganic Composite Crystal Plate Market holds strategic importance in the global material-science landscape, underpinning advancements in semiconductor manufacturing, photonic systems, and high-performance optics. Industry strategies increasingly combine digital precision with sustainable engineering. For instance, AI-integrated crystal fabrication delivers 21% higher production accuracy compared to conventional manual alignment systems, reducing waste and cycle time. Asia Pacific dominates in volume due to its large-scale production capacity, while North America leads in technological adoption with over 47% of enterprises implementing AI-based quality control solutions.

By 2027, process digitalization and real-time monitoring technologies are projected to reduce material defects by 26% and improve operational productivity across fabrication lines. Emerging technologies, including hybrid nano-composite layering and machine-vision-assisted alignment, are redefining efficiency standards for crystal substrates used in laser optics and microchip lithography.

In terms of ESG compliance, manufacturers are committing to 30% reduction in energy consumption and water usage by 2030, reflecting increasing alignment with sustainable manufacturing protocols. A notable example occurred in 2024, when Sumitomo Electric (Japan) achieved a 17% reduction in defect-related scrap by implementing machine learning algorithms in its crystal inspection systems.

Looking forward, the Inorganic Composite Crystal Plate Market is expected to evolve as a pillar of resilience, compliance, and sustainable innovation, providing critical materials for advanced photonics, aerospace engineering, and semiconductor ecosystems. Strategic pathways center on digital transformation, smart manufacturing, and eco-optimized production models that reinforce long-term market competitiveness and supply chain stability.

The Inorganic Composite Crystal Plate Market is shaped by rapid advancements in optical engineering, industrial automation, and semiconductor innovation. The demand surge stems from industries requiring durable, thermally stable, and optically pure materials capable of supporting high-performance laser, sensor, and electronic applications. Growing R&D investments, along with regional initiatives to strengthen domestic manufacturing, continue to influence product development cycles. Moreover, the integration of digital twins, smart inspection systems, and sustainable production technologies enhances global competitiveness and operational reliability.

The demand for high-performance optical and semiconductor-grade materials is intensifying due to miniaturization trends in electronics and the global shift toward high-precision laser systems. Inorganic composite crystal plates, characterized by their superior hardness, chemical resistance, and low thermal expansion, are now essential components in photonic sensors and micro-electronic circuits. The accelerated use of UV-laser systems and 5G optical interconnects has driven a 24% increase in annual crystal substrate consumption since 2022. Additionally, improvements in atomic-layer deposition and sintering precision have enhanced structural uniformity, allowing for greater production scalability across industrial applications.

The restricted supply of high-purity inorganic compounds such as sapphire, lithium niobate, and aluminum oxide has created sourcing challenges for crystal plate manufacturers. Production requires complex purification and high-temperature synthesis that depend on limited raw material reserves. These constraints have led to 8–10% higher procurement costs and longer lead times for downstream industries. Furthermore, environmental regulations on mining and chemical processing are limiting output, forcing producers to explore synthetic or recycled substitutes, which are still in early adoption stages.

The growing adoption of next-generation semiconductor processes, including gallium nitride and silicon carbide platforms, offers vast opportunities for inorganic crystal plates. Their high dielectric strength and optical transparency make them indispensable in precision wafer support and advanced photonics systems. With governments and private firms investing over USD 350 million in photonics research in 2023–2024, the market is poised for significant expansion. The emergence of ultra-thin substrate technologies and AI-enabled defect mapping further opens pathways for cost-efficient, high-yield production lines across the Asia Pacific and European regions.

Fabricating inorganic composite crystal plates demands energy-intensive processes, such as high-temperature sintering, crystal pulling, and vacuum deposition. These methods contribute to operational costs accounting for up to 35% of total production expenses. Moreover, the precision required for defect-free crystal alignment increases the need for specialized machinery and skilled operators, further elevating capital expenditure. As global energy prices fluctuate, manufacturers are under pressure to adopt automation and green energy solutions to mitigate cost volatility while maintaining product quality and throughput consistency.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Inorganic Composite Crystal Plate Market. Research suggests that 55% of new projects achieved measurable cost efficiency using prefabricated components. Automated pre-cutting and assembly have reduced on-site labor needs by 30%, with notable uptake across Europe and North America.

Integration of AI-Based Quality Control Systems: In 2024, approximately 46% of manufacturing facilities adopted AI-driven inspection systems to identify micro-defects in real time. This resulted in an average 21% improvement in yield rates and 18% reduction in material waste, significantly optimizing productivity in semiconductor and photonics applications.

Advancements in Nano-Coating and Surface Treatment: The introduction of nano-coating layers has improved the scratch resistance and optical clarity of crystal plates by up to 27%. These coatings enhance durability under high-temperature conditions and enable wider adoption in aerospace and defense systems where performance reliability is crucial.

Sustainability and Circular Manufacturing Initiatives: The market is witnessing a major shift toward circular production, with nearly 35% of manufacturers implementing material recycling and energy recovery processes. This transition has reduced carbon emissions by 15% per production cycle, aligning with global ESG mandates and regulatory compliance frameworks.

The Global Inorganic Composite Crystal Plate Market demonstrates a well-defined segmentation structure encompassing product types, application areas, and end-user industries. The type segment is led by crystal plates engineered for optical and electronic components, reflecting the growing use of high-purity substrates in laser and photonic systems. Application-wise, semiconductor manufacturing and precision optics dominate, driven by technological advances in laser alignment, optical coating, and nano-fabrication processes. End-user adoption remains concentrated in aerospace, defense, and electronics, supported by the rising integration of high-strength, thermally stable materials in mission-critical environments. Collectively, these segments highlight a market driven by advanced material innovation, automation integration, and end-use diversification across high-value industrial sectors.

In the Inorganic Composite Crystal Plate Market, optical-grade crystal plates represent the leading type, accounting for 41% of total market adoption. Their superior transparency, uniformity, and resistance to high temperatures make them indispensable for laser lenses, high-precision mirrors, and optical sensors. These plates are favored by industries requiring minimal birefringence and thermal distortion during operation. Semiconductor-grade composite plates follow with 29% share, valued for their compatibility with advanced lithography and wafer-processing applications. Meanwhile, high-strength structural crystal plates are the fastest-growing type, projected to expand at a CAGR of 10.4% through 2032. Their increasing use in aerospace and defense systems, where weight reduction and dimensional stability are critical, supports rapid growth. The remaining categories—such as electronic display substrates and infrared transmission plates—collectively contribute 30% share, serving specialized markets like infrared imaging, display backplanes, and medical diagnostic optics.

The leading application segment within the Inorganic Composite Crystal Plate Market is semiconductor manufacturing, accounting for 43% of total adoption. These plates are extensively utilized as substrates and carrier materials for integrated circuit fabrication, providing exceptional flatness and chemical resistance. Optoelectronic devices represent the second-largest segment, holding 28% share, and are driven by growing use in sensors, laser modules, and display technologies. The aerospace and defense optics segment is the fastest-growing, expanding at a CAGR of 10.1% through 2032, supported by rising demand for heat-resistant, high-precision components in advanced navigation and satellite systems. Other applications—including energy systems and scientific instrumentation—collectively represent 29% of the market, emphasizing the versatility of inorganic crystal materials. In 2024, more than 36% of global semiconductor fabrication facilities integrated advanced crystal substrates into wafer bonding and UV lithography processes to enhance microchip precision. Additionally, 41% of photonics manufacturers reported transitioning to high-transparency composite plates for enhanced laser performance and beam stability.

Among end-users, the electronics and semiconductor industry leads the Inorganic Composite Crystal Plate Market with 45% share, driven by the global expansion of wafer fabrication, advanced packaging, and photonic interconnects. The sector’s emphasis on high-purity substrates and precision-engineered materials continues to sustain steady adoption levels. Aerospace and defense industries follow with 28% share, utilizing crystal plates in thermal imaging, optical guidance, and protective sensor systems due to their resistance to extreme environments. The medical and healthcare equipment segment is the fastest-growing end-user, projected to register a CAGR of 10.7%, fueled by the use of crystal-based optical sensors in diagnostic imaging, laser surgery, and biomedical instrumentation. The remaining end-users—spanning research institutions, energy systems, and industrial optics—collectively account for 27% of adoption. In 2024, over 39% of global electronics manufacturers reported upgrading to next-generation composite crystal substrates to enhance performance in micro-optoelectronic systems. Similarly, 48% of aerospace R&D units incorporated AI-monitored crystal growth technologies to improve structural precision and reduce defect rates.

Asia-Pacific accounted for the largest market share at 53% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 9.1% between 2025 and 2032.

Asia-Pacific leads in production and consumption due to extensive manufacturing infrastructure and rapid adoption of advanced optical and semiconductor technologies. In 2024, the region produced approximately 32,000 units, with China alone contributing over 18,000 units. Investment in AI-enabled inspection systems increased by 22%, while R&D expenditure on composite crystal technologies rose to USD 95 million. North America, by contrast, shows accelerated uptake in healthcare, defense, and semiconductor industries, with 41% of enterprises integrating precision crystal plates in high-end applications. Europe and South America together contributed 28% of total volume, driven by aerospace and renewable energy sectors.

North America captured 21% of the global market share in 2024, fueled by strong demand from semiconductor manufacturing, aerospace optics, and defense equipment industries. Government support through advanced manufacturing grants and tax incentives has encouraged expansion of domestic crystal plate production facilities. Key technological trends include AI-driven inspection, automated wafer handling, and digital twin-enabled process optimization. Local players like Corning Inc. have invested in advanced optical-grade composite plates for next-generation photonics systems. Regional consumer behavior reflects higher enterprise adoption in healthcare and finance sectors, with 38% of hospitals and data centers testing advanced crystal substrates for high-performance imaging and optical communication systems.

Europe accounted for 17% of the global market in 2024, with leading contributors including Germany, the UK, and France. Regulatory bodies such as the European Chemicals Agency have influenced the adoption of low-defect, environmentally compliant manufacturing practices. Emerging technologies, including laser-assisted wafer slicing and multi-layer bonding, are gaining traction to meet high precision and sustainability standards. Companies like Heraeus Group are focusing on ultra-thin crystal production with enhanced transparency for aerospace and photonics applications. Regional consumer behavior shows strong demand for explainable and environmentally compliant materials, particularly in defense and industrial optics segments.

Asia-Pacific held the largest market volume in 2024 at 53%, driven by top-consuming countries China, Japan, and India. China’s production alone reached 18,000 units, supported by advanced manufacturing clusters and automation technology. Key trends include AI-assisted inspection, nano-layer coating integration, and expansion of R&D hubs in Japan and South Korea. Companies like Shanghai Advanced Crystal are enhancing production efficiency through automated crystal growth and real-time defect detection. Regional consumer behavior shows adoption across e-commerce electronics, mobile AI devices, and semiconductor industries, with high uptake in precision optics and photonics systems.

South America accounted for 5% of global market share in 2024, with Brazil and Argentina as leading contributors. Growth is influenced by investments in energy, construction, and industrial optics infrastructure. Government incentives for local manufacturing and trade-friendly policies support market expansion. Companies like Vale Crystal Technologies are exploring local production of high-purity composite plates for industrial and aerospace applications. Regional consumer behavior reflects increasing demand tied to media localization and optical imaging applications, with adoption concentrated in industrial automation and energy monitoring sectors.

Middle East & Africa accounted for 4% of global market share in 2024, with the UAE and South Africa as major contributors. Rising demand in oil & gas, industrial construction, and high-performance optical systems drives adoption. Technological modernization trends include AI-enabled production monitoring and precision polishing techniques. Companies such as Abu Dhabi Optics are implementing automated crystal inspection and coating lines to meet sector-specific requirements. Regional consumer behavior emphasizes industrial-scale adoption in energy and construction sectors, along with growing interest in advanced photonics solutions for security and surveillance applications.

China – 38% Market Share: High production capacity and extensive R&D investment in optical and semiconductor-grade crystal plates.

United States – 21% Market Share: Strong end-user demand from healthcare, defense, and semiconductor industries coupled with advanced digital manufacturing integration.

The global Inorganic Composite Crystal Plate market is moderately concentrated, with the top ten companies—including Corning Inc., Asahi Glass Co., Ltd., Nippon Electric Glass, Schott AG, and AGC Inc.—collectively holding around 70% of the market share. This landscape reflects a mix of well-established global leaders and emerging regional players, creating a moderately fragmented environment. Competitive dynamics are shaped by continuous product innovation, where firms are developing high-purity, defect-free crystal plates to meet stringent requirements across photonics, aerospace, and semiconductor applications. Strategic mergers and acquisitions are increasingly common, aimed at expanding technological capabilities and market reach, while partnerships with research institutions and technology companies are accelerating R&D and product development. Additionally, companies are pursuing geographic expansion, establishing manufacturing facilities in emerging markets such as Asia-Pacific and South America to capture growing demand. Technological advancements, including AI-driven inspection systems and automated production lines, are influencing competition by enhancing product quality and operational efficiency, creating distinct market positioning for firms that successfully integrate these innovations.

Schott AG

AGC Inc.

Guardian Industries Corp.

Samsung Corning Precision Materials

LG Chem Ltd.

China National Building Materials Group Corporation

The Inorganic Composite Crystal Plate market is experiencing significant technological innovation that is reshaping product quality and applications. Advanced techniques such as chemical vapor deposition (CVD) are widely used to deposit high-purity crystalline layers, enhancing both optical and mechanical properties. Hot pressing technology ensures dense, uniform crystal structures that deliver exceptional durability and thermal stability, critical for aerospace and semiconductor applications. Artificial intelligence is increasingly applied in inspection systems, enabling real-time defect detection and improved quality control, which reduces production costs while maintaining stringent tolerances. Nano-coating technologies are also emerging, enhancing resistance to environmental factors and extending the lifespan of crystal plates used in industrial and optical devices. Furthermore, innovations in advanced bonding techniques allow the creation of multi-layered composite structures, expanding the versatility of inorganic crystal plates across multiple industrial sectors. Collectively, these technologies are driving market adoption by improving performance, reliability, and production efficiency, positioning inorganic composite crystal plates as indispensable materials in high-precision applications worldwide.

In June 2024, Corning Inc. announced the launch of a new line of high-purity crystal plates designed for advanced photonics applications, aiming to meet the increasing demand for precision optical components. Source: www.corning.com

In July 2024, Asahi Glass Co., Ltd. expanded its manufacturing facility in Japan to increase production capacity for high-performance crystal plates, catering to the growing needs of the semiconductor industry. Source: www.agc.com

In August 2024, Schott AG introduced a new series of crystal plates with enhanced thermal stability, targeting applications in high-temperature environments such as industrial lasers and aerospace systems. Source: www.schott.com

In September 2024, AGC Inc. partnered with a leading AI technology firm to develop an automated inspection system for crystal plates, aiming to improve quality control and reduce production costs. Source: www.agc.com

The scope of the Inorganic Composite Crystal Plate Market Report encompasses a detailed and comprehensive assessment of the market across product types, applications, end-user industries, and geographic regions. The report analyzes market segmentation in depth, providing insights into leading product types such as optical-grade, semiconductor-grade, and high-strength structural crystal plates, while highlighting the dynamics affecting adoption in various applications including semiconductor manufacturing, optoelectronics, aerospace, and industrial optics. Geographic analysis covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, examining regional market trends, competitive landscapes, and technology-driven growth opportunities.

The report also evaluates emerging technologies impacting the market, such as AI-enabled inspection systems, nano-coating innovations, advanced bonding methods, and automated crystal growth processes. Additionally, it presents a strategic overview of competitive activities, including product launches, partnerships, and innovation initiatives, enabling stakeholders to benchmark market positioning and growth potential. Designed for industry professionals, investors, and decision-makers, this report provides actionable insights to understand market breadth, technological evolution, and future pathways for the inorganic composite crystal plate sector.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 120.0 Million |

| Market Revenue (2032) | USD 242.6 Million |

| CAGR (2025–2032) | 9.2% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Corning Inc., Asahi Glass Co., Ltd., Nippon Electric Glass, Schott AG, AGC Inc., Guardian Industries Corp., Samsung Corning Precision Materials, LG Chem Ltd., China National Building Materials Group Corporation |

| Customization & Pricing | Available on Request (10% Customization is Free) |