Reports

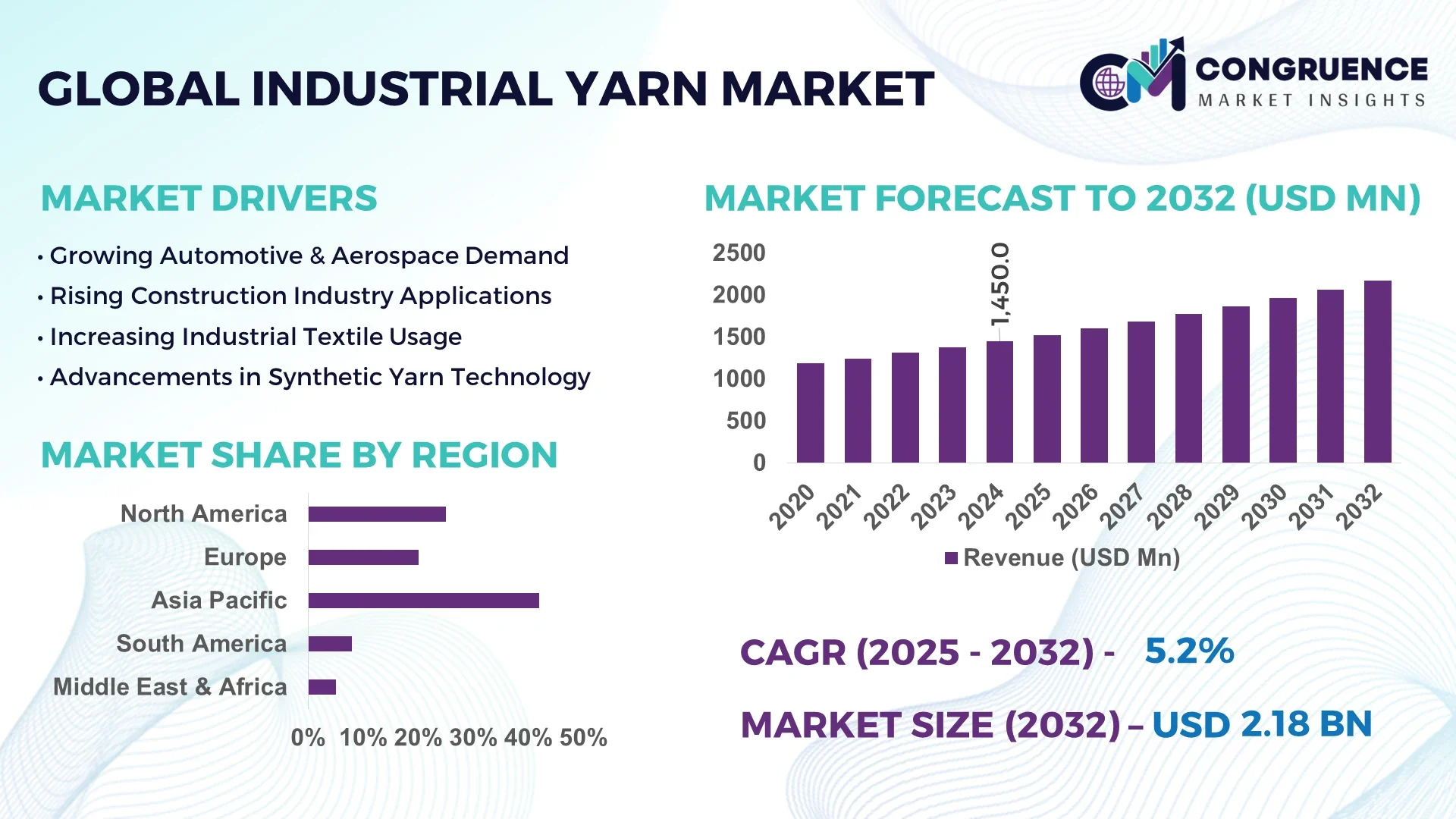

The Global Industrial Yarn Market was valued at USD 1,450.0 Million in 2024 and is anticipated to reach a value of USD 2,175.2 Million by 2032 expanding at a CAGR of 5.2% between 2025 and 2032.

China dominates the Industrial Yarn Market with extensive production capacities and high-volume manufacturing infrastructure. The country has invested significantly in advanced textile machinery, automated spinning lines, and high-strength yarn production facilities, catering to applications in automotive, construction, and technical textiles. Continuous innovation in synthetic fiber blends and industrial-grade reinforcements has further strengthened China’s position as a global leader in industrial yarn production.

The Industrial Yarn Market is witnessing strong adoption across key sectors such as automotive, construction, aerospace, and manufacturing, each contributing to overall demand patterns. Technological advancements, including high-tenacity polyester and aramid yarns, are improving performance characteristics such as tensile strength, chemical resistance, and abrasion durability. Regulatory measures emphasizing fire safety, environmental compliance, and worker safety are influencing material selection and production standards. Regional consumption patterns highlight significant growth in Asia-Pacific due to infrastructure expansion, while North America and Europe maintain stable demand supported by industrial and automotive applications. Emerging trends such as eco-friendly yarn formulations, integration with composites, and smart textiles indicate a forward-looking market poised for continued innovation and diversified applications.

Artificial intelligence (AI) is transforming the Industrial Yarn Market by enabling optimized production processes, predictive maintenance, and real-time quality monitoring. Manufacturers are increasingly deploying AI-driven systems to track fiber properties, automate spinning processes, and reduce production waste. AI-powered analytics facilitate precise adjustments in tension, twist, and fiber blending, enhancing operational efficiency and consistent product quality. In high-performance applications such as automotive and aerospace textiles, AI ensures that yarn specifications meet stringent safety and performance standards.

Additionally, AI tools are being integrated into supply chain management to forecast demand patterns and optimize inventory levels, reducing stockouts and production delays. Digital twins of production lines allow manufacturers to simulate process changes before implementation, minimizing downtime and energy consumption. The Industrial Yarn Market benefits from these technologies by increasing throughput, lowering operational costs, and improving the overall quality of industrial-grade yarns. AI-driven design platforms also allow rapid prototyping of customized yarn compositions for specialized applications, accelerating innovation cycles. As adoption of smart manufacturing and predictive analytics grows, AI is becoming a central driver of efficiency, reliability, and innovation across the Industrial Yarn Market.

“In March 2024, a leading Chinese industrial yarn manufacturer implemented an AI-powered quality control system across three production plants, resulting in a 17% reduction in defective yarn output and a 12% increase in throughput efficiency within the first six months of deployment.”

The Industrial Yarn Market is shaped by increasing demand for high-strength and durable yarns across multiple industrial applications. Innovations in synthetic fibers, including polyester, nylon, and aramid blends, have enhanced yarn performance, expanding their use in construction, automotive, and technical textile sectors. Market dynamics are also influenced by environmental regulations promoting sustainable production methods and energy-efficient machinery. Supply chain optimization, growing investments in automated production facilities, and regional infrastructure development in Asia-Pacific contribute to expanding market opportunities. In addition, shifts in industrial manufacturing standards, coupled with the need for lightweight and high-performance materials, are driving adoption of advanced industrial yarns globally.

The Industrial Yarn Market is experiencing accelerated growth due to the increased utilization of industrial yarns in automotive components, construction reinforcements, and technical textiles. High-strength polyester and aramid yarns are increasingly used in tires, seat belts, composites, and conveyor belts, enhancing durability and performance. Industrial yarns provide critical reinforcement in infrastructure projects such as bridges and tunnels, ensuring structural integrity and longevity. The growing focus on lightweight materials in transportation and manufacturing has expanded the scope for specialized yarn types. Investments in production capacity and adoption of advanced manufacturing technologies further support market expansion, enabling manufacturers to meet the evolving requirements of industrial and automotive sectors.

Fluctuations in polyester, nylon, and aramid fiber prices pose significant challenges to the Industrial Yarn Market. Raw material costs impact profit margins for manufacturers and influence pricing strategies. Dependence on petroleum-based raw materials exposes the market to supply chain disruptions due to geopolitical tensions, logistics issues, or environmental policies. Additionally, fluctuations in global energy costs affect production expenses in energy-intensive spinning and weaving processes. Small and medium-scale manufacturers face difficulties absorbing these cost variations, which can hinder operational efficiency. Consequently, price volatility remains a critical restraint impacting strategic planning and long-term growth in the Industrial Yarn Market.

The Industrial Yarn Market presents opportunities for eco-conscious and high-performance product lines. Demand for recycled polyester and bio-based fibers is rising in construction, automotive, and consumer industrial applications. Manufacturers are exploring innovative blends that reduce environmental impact while maintaining tensile strength, chemical resistance, and thermal stability. Additionally, growth in technical textiles and composite applications offers avenues for specialty yarn development. Adoption of digitalized production methods, such as automated spinning and AI-assisted quality monitoring, allows efficient manufacturing of customized yarns. This convergence of sustainability, performance, and technological innovation is expected to open new revenue streams and differentiate manufacturers in a competitive market.

Manufacturers in the Industrial Yarn Market face challenges associated with increasing operational expenditures and regulatory compliance. Upgrades to production lines for higher efficiency, adoption of eco-friendly raw materials, and adherence to stringent safety and environmental standards incur significant capital investment. Energy-intensive processes, coupled with stringent emission regulations, require additional monitoring and control systems. Furthermore, global trade policies, tariffs, and import-export restrictions can disrupt supply chains and increase procurement costs. These operational and regulatory pressures demand strategic planning, efficient resource allocation, and technological adaptation to maintain competitiveness while ensuring compliance across industrial and international markets.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Industrial Yarn Market. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Growth of Technical Textiles: Technical textiles, including high-strength composites and protective materials, are increasingly driving demand for specialty industrial yarns. Applications in automotive, aerospace, and industrial reinforcements are requiring tailored yarn compositions with enhanced tensile strength and chemical resistance.

Digital Integration and Smart Manufacturing: Manufacturers are increasingly implementing AI-driven process controls, digital twins, and predictive maintenance systems in production lines, enhancing consistency, reducing waste, and improving overall operational efficiency in the Industrial Yarn Market.

Sustainability and Eco-Friendly Materials: The Industrial Yarn Market is witnessing increased use of recycled polyester and bio-based fibers. These environmentally conscious materials are being integrated into construction, automotive, and industrial textile applications, aligning with global sustainability initiatives and regulatory guidelines.

The Industrial Yarn Market is segmented into three key categories: type, application, and end-user. By type, the market includes products such as polyester, nylon, aramid, and specialty synthetic yarns, each tailored for specific industrial requirements. Application segments cover automotive components, construction reinforcement, industrial textiles, and technical fabrics, reflecting diverse end-use industries. End-user segmentation identifies sectors that consume industrial yarns, including automotive, construction, aerospace, manufacturing, and packaging. This structured segmentation allows manufacturers and decision-makers to understand demand patterns, tailor product offerings, and optimize production for targeted industries. Regional consumption patterns further influence segment prioritization, with high-performance yarns often directed toward technical applications requiring durability and chemical resistance.

The Industrial Yarn Market encompasses several types, including polyester yarn, nylon yarn, aramid yarn, and specialty synthetic yarns. Polyester yarn is the leading type, widely used due to its high tensile strength, durability, and versatility across automotive, construction, and technical textile applications. Aramid yarn represents the fastest-growing segment, driven by its superior heat resistance, abrasion durability, and increasing adoption in protective gear, composites, and aerospace components. Nylon yarn continues to maintain relevance in high-strength applications, while specialty synthetic yarns serve niche needs such as medical textiles, filtration fabrics, and environmentally resistant products. Together, these types provide a broad range of performance characteristics, enabling the market to meet diverse industrial requirements efficiently and reliably.

The Industrial Yarn Market serves multiple application areas, with automotive and construction being the dominant applications. Automotive applications, including tire reinforcement, seat belts, and airbags, rely on high-strength yarns for safety and performance, making this the leading segment. The fastest-growing application is technical textiles for industrial and protective equipment, fueled by rising demand for high-performance fabrics in aerospace, defense, and energy sectors. Other applications include industrial fabrics for conveyor belts, filtration systems, and packaging materials, which support specialized manufacturing processes. The widespread adoption of advanced composites and reinforced materials in construction projects further broadens application potential, ensuring the market meets evolving industrial standards and performance expectations.

The Industrial Yarn Market caters to a diverse set of end-users, with automotive being the leading segment due to the extensive use of yarns in tire cords, belts, airbags, and composite components. The fastest-growing end-user is the construction industry, driven by the increasing adoption of reinforced materials, geotextiles, and industrial fabrics in infrastructure projects. Other significant end-users include aerospace, manufacturing, and packaging sectors, each demanding tailored yarn types for specific performance characteristics. Industrial yarns are critical in meeting mechanical strength, chemical resistance, and environmental durability requirements across applications, enabling manufacturers to serve specialized end-user needs while maintaining consistent quality and reliability. Regional variations in end-user demand also influence product development and distribution strategies.

Asia-Pacific accounted for the largest market share at 42% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2025 and 2032.

The region’s Industrial Yarn Market is driven by rapid industrialization, increasing demand from automotive, construction, and manufacturing sectors, and substantial investments in textile production technologies. China, India, and Japan are the major contributors, supported by expanding infrastructure projects and growing export opportunities. Increasing adoption of high-performance and eco-friendly yarns, combined with advanced manufacturing capabilities, positions Asia-Pacific as both the largest consumer and the fastest-growing regional market.

North America accounted for approximately 25% of the Industrial Yarn Market in 2024, driven largely by the automotive, aerospace, and construction industries. The United States and Canada are the leading contributors within the region. Regulatory initiatives promoting safety standards, environmental compliance, and industrial efficiency have encouraged the adoption of high-performance yarns. Technological advancements such as AI-enabled process optimization, automated spinning, and digital twins in production facilities are increasing operational efficiency. North American manufacturers are also investing in R&D for specialty yarns that meet demanding mechanical and thermal requirements, ensuring the region remains competitive in global markets.

Europe holds a market share of around 20% in 2024, with Germany, the United Kingdom, and France as the key markets. The Industrial Yarn Market in Europe is supported by stringent environmental regulations and sustainability initiatives, prompting manufacturers to adopt bio-based and recycled fibers. Technological advancements, including high-tenacity aramid yarns and nanofiber integration, are creating innovative solutions for construction, automotive, and industrial textiles. Regional policies encouraging energy-efficient manufacturing, coupled with digitalization and automation, have enhanced productivity and reduced waste. Europe continues to focus on high-quality production standards and innovative applications, reinforcing its role as a significant market for industrial yarns.

Asia-Pacific represents approximately 42% of the Industrial Yarn Market in 2024, making it the largest and fastest-growing region. China, India, and Japan are the top-consuming countries, driven by automotive, infrastructure, and textile manufacturing needs. Large-scale industrial yarn production facilities are being established to meet domestic demand and export requirements. Technological advancements, including automated spinning systems, AI-based quality monitoring, and nanocomposite yarn development, are enhancing production efficiency and product performance. Regional innovation hubs are emerging in China and India, promoting research in high-strength, eco-friendly, and specialty yarns. Infrastructure expansion, industrial modernization, and government support further strengthen market growth.

South America accounted for around 8% of the Industrial Yarn Market in 2024, with Brazil and Argentina as the leading countries. Demand is primarily driven by infrastructure projects, energy sector applications, and the growing construction industry. Regional manufacturers are increasingly adopting advanced spinning and weaving technologies to improve product quality. Government incentives for local production, trade agreements, and industrial development policies are boosting market activity. Energy-efficient production practices and the integration of high-performance yarns in automotive and industrial applications are contributing to market growth. South America presents opportunities for both domestic expansion and regional exports of industrial yarns.

Middle East & Africa held a market share of approximately 5% in 2024, with the UAE and South Africa as major contributors. Demand is driven by the oil & gas, construction, and automotive industries, requiring high-strength and durable yarns. Technological modernization, including automated production lines and AI-based monitoring systems, is improving efficiency and quality. Local regulations supporting industrial growth, trade partnerships, and infrastructure projects are enhancing market development. Investment in specialty yarn production and adoption of eco-friendly fibers are emerging trends, positioning the region for incremental growth in both industrial and construction-related applications.

The Industrial Yarn Market is highly competitive with over 50 active global manufacturers, ranging from established multinational corporations to specialized regional producers. Leading players are strategically positioning themselves through mergers, acquisitions, and partnerships to expand production capabilities and enter new regional markets. Product innovation remains a critical competitive factor, with companies investing in high-strength polyester, aramid, and eco-friendly synthetic yarns. Several manufacturers have introduced AI-enabled production lines and automated spinning technologies, enhancing efficiency and quality control. Strategic initiatives also include collaborations with automotive, construction, and aerospace firms to develop customized yarn solutions for technical applications. Companies are increasingly leveraging digital platforms for supply chain optimization, predictive maintenance, and process monitoring, driving operational excellence. Continuous R&D in fiber blends, thermal stability, and chemical resistance is shaping competitive dynamics, ensuring differentiation through specialized product offerings. Emerging players focus on niche markets, such as sustainable and recycled yarns, creating additional competitive pressure. Overall, market competition revolves around innovation, operational efficiency, technological integration, and responsiveness to industrial end-user demands.

Toray Industries

Hyosung Corporation

DuPont de Nemours, Inc.

Reliance Industries Limited

Indorama Ventures Public Company Limited

Sinopec Yizheng Chemical Fibre Company

Teijin Limited

Zhejiang Hengyi Group

Lanxess AG

RadiciGroup

Technological advancements are transforming the Industrial Yarn Market through automation, AI, and material innovations. Automated spinning and weaving machines increase throughput while reducing labor dependency, allowing precise control over yarn tension, twist, and fiber blending. AI-driven quality control systems monitor fiber uniformity and detect defects in real-time, minimizing production waste and improving overall efficiency. Digital twin technologies are increasingly employed to simulate production processes, enabling manufacturers to test changes virtually and optimize operations before physical implementation.

Material innovations are also reshaping the market, with high-tenacity polyester, aramid, and hybrid yarns providing enhanced tensile strength, abrasion resistance, and chemical stability. Specialty yarns incorporating nanofibers or bio-based fibers are gaining traction for advanced applications in aerospace, automotive, and construction. Additionally, real-time monitoring of energy usage and emissions aligns with sustainability and environmental compliance initiatives, promoting energy-efficient production. Integration of smart manufacturing systems allows manufacturers to adapt quickly to end-user requirements, customize yarn properties, and streamline supply chains, reinforcing competitiveness in a rapidly evolving Industrial Yarn Market.

In February 2024, Toray Industries launched a high-strength aramid yarn line designed for aerospace and automotive applications, featuring 15% higher tensile strength compared to conventional aramid yarns.

In August 2023, Reliance Industries expanded its industrial yarn production capacity by 20,000 tons per year with the installation of automated spinning machinery at its Maharashtra facility.

In December 2023, Hyosung Corporation introduced eco-friendly polyester yarns produced using recycled PET bottles, reducing environmental impact while maintaining mechanical performance for construction and industrial applications.

In May 2024, DuPont implemented AI-enabled quality monitoring across two production facilities, improving defect detection rates by 18% and reducing material waste in industrial yarn manufacturing.

The Industrial Yarn Market Report provides a comprehensive analysis of the global market, covering product types such as polyester, nylon, aramid, and specialty synthetic yarns. It examines applications across automotive, construction, aerospace, industrial textiles, and packaging, offering insights into end-user sectors, including automotive manufacturers, construction companies, aerospace firms, and industrial fabric producers. The report includes regional perspectives, covering North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting production capacities, consumption patterns, and technological adoption in each region.

The report also explores current and emerging technologies, including AI-driven quality control, automated spinning, digital twins, and nanofiber integration, providing a forward-looking view of innovation trends. Sustainability initiatives, such as recycled and bio-based fibers, are emphasized, reflecting regulatory and environmental influences on the market. Additionally, the report identifies competitive dynamics, strategic initiatives, and growth opportunities for manufacturers, enabling decision-makers to assess market potential, plan investments, and tailor product strategies. Niche segments, including high-performance and specialty yarns, are highlighted to inform targeted business decisions across diverse industrial applications.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 1,450.0 Million |

| Market Revenue (2032) | USD 2,175.2 Million |

| CAGR (2025–2032) | 5.2% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Toray Industries, Hyosung Corporation, DuPont de Nemours, Inc., Reliance Industries Limited, Indorama Ventures Public Company Limited, Sinopec Yizheng Chemical Fibre Company, Teijin Limited, Zhejiang Hengyi Group, Lanxess AG, RadiciGroup |

| Customization & Pricing | Available on Request (10% Customization is Free) |