Reports

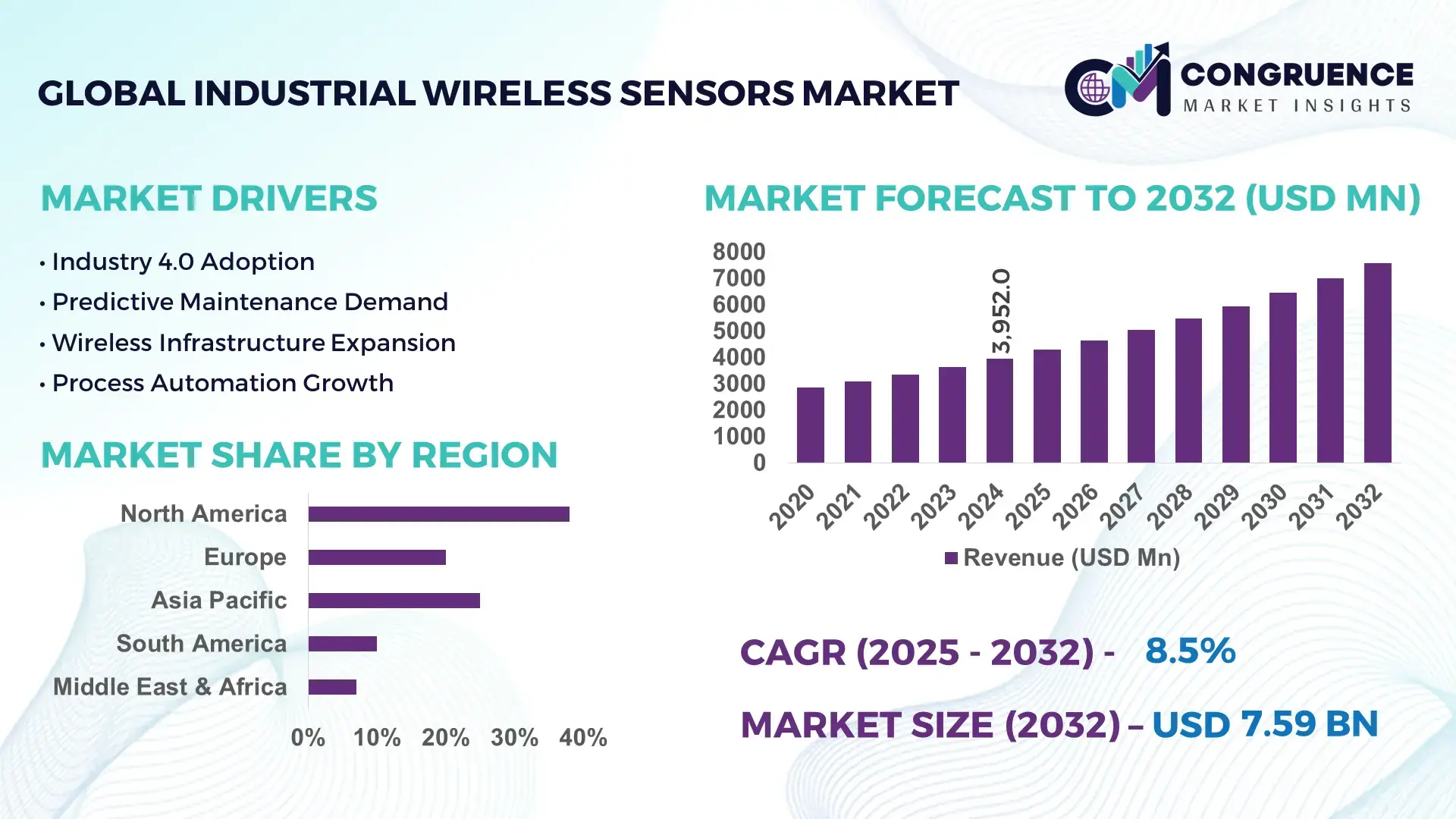

The Global Industrial Wireless Sensors Market was valued at USD 3952 Million in 2024 and is anticipated to reach a value of USD 7590.23 Million by 2032 expanding at a CAGR of 8.5% between 2025 and 2032. Growth is supported by rising automation intensity across manufacturing, energy, and process industries seeking real-time, low-latency operational data without complex cabling.

The United States represents the most influential national market in industrial wireless sensors in terms of production scale, investment volume, and technological leadership. In 2024, over 35 large-scale sensor manufacturing and integration facilities operated across California, Texas, Ohio, and Michigan, with combined annual output capacity exceeding 480 million industrial-grade sensing units including pressure, vibration, flow, and temperature sensors. Industrial IoT investments in the U.S. surpassed USD 22 billion in 2024, with approximately 18% directed toward wireless sensing, edge connectivity, and factory networking upgrades. Wireless sensors are deployed across more than 62% of U.S. discrete manufacturing plants, 58% of energy generation facilities, and 46% of oil and gas installations for predictive maintenance and remote monitoring. Over 70% of new industrial sensor deployments in the U.S. now support protocols such as WirelessHART, ISA100, or 5G-enabled industrial private networks, reflecting advanced integration into smart factories, digital twins, and AI-driven asset management systems.

• Market Size & Growth: USD 3,952 million in 2024, projected USD 7,590.23 million by 2032, CAGR 8.5%, driven by automation, predictive maintenance, and digital transformation

• Top Growth Drivers: Smart factory adoption 41%, predictive maintenance penetration 36%, industrial IoT integration 44%

• Short-Term Forecast: By 2028, unplanned downtime reduced by 28% through wireless condition monitoring

• Emerging Technologies: 5G-enabled private industrial networks, edge-AI embedded sensors, digital twin integration

• Regional Leaders: North America USD 2,750 million by 2032 with high smart factory density; Europe USD 2,120 million with strong energy and chemical adoption; Asia-Pacific USD 2,400 million with rapid manufacturing automation

• Consumer/End-User Trends: Manufacturers shift toward battery-free and ultra-low-power sensors for large-scale deployments

• Pilot or Case Example: 2026 automotive plant pilot achieved 31% downtime reduction using wireless vibration and thermal sensors

• Competitive Landscape: Market leader approximately 18%, followed by Siemens, Honeywell, ABB, Emerson, and Yokogawa

• Regulatory & ESG Impact: Energy efficiency mandates and digital safety compliance accelerating sensor deployment in heavy industry

• Investment & Funding Patterns: Over USD 6.8 billion invested globally since 2022 into industrial IoT and sensor infrastructure

• Innovation & Future Outlook: Expansion of AI-enabled sensing, cloud-edge convergence, and autonomous maintenance systems

Industrial wireless sensors are increasingly embedded across manufacturing, oil and gas, power generation, chemicals, water treatment, and logistics, with manufacturing contributing approximately 38% of total demand, energy and utilities around 27%, and process industries roughly 22%. Innovations such as self-powered energy-harvesting sensors, AI-enabled edge analytics, and multi-protocol connectivity modules are improving reliability and lowering total deployment costs. Regulatory pressure on energy efficiency, workplace safety, and emissions monitoring is driving adoption, while economic priorities around productivity and asset utilization strengthen investment momentum. Regionally, Asia-Pacific is expanding fastest due to automation in electronics, automotive, and heavy machinery, while Europe emphasizes sustainability-driven digital upgrades. Future growth is shaped by convergence of wireless sensing with digital twins, predictive analytics, and autonomous industrial control, positioning the market as a core enabler of next-generation smart industrial ecosystems.

The Industrial Wireless Sensors Market plays a strategic role in enabling data-driven operations, asset visibility, and real-time decision-making across manufacturing, energy, utilities, chemicals, and logistics. Wireless sensing infrastructure reduces installation time by over 45% compared to wired systems and lowers maintenance labor by nearly 30%, making it a core component of modern industrial digitization strategies. Technologies such as edge-AI embedded sensors deliver approximately 35% improvement in anomaly detection accuracy compared to traditional rule-based threshold monitoring. Asia-Pacific dominates in shipment volume due to large-scale manufacturing deployments, while Europe leads in adoption with nearly 61% of large enterprises integrating wireless industrial sensors into their operational technology environments. By 2027, AI-driven predictive maintenance platforms combined with wireless sensing are expected to reduce unplanned downtime by 32% across asset-intensive industries. From an ESG perspective, industrial firms are committing to energy efficiency improvements such as 18% reduction in electricity consumption per unit of output by 2030 through real-time monitoring and optimization. In 2025, a German automotive manufacturer achieved a 29% reduction in maintenance-related stoppages through deployment of wireless vibration and thermal sensors integrated with machine learning diagnostics. Looking ahead, the Industrial Wireless Sensors Market is positioned as a structural pillar for industrial resilience, regulatory compliance, and sustainable growth by supporting transparency, automation, and continuous performance optimization across global production networks.

Smart factory deployment is expanding rapidly, with over 55% of large manufacturers implementing some level of digital automation by 2024. Wireless sensors enable flexible reconfiguration of production lines, reducing setup time by approximately 40% compared to hard-wired instrumentation. Predictive maintenance programs using wireless vibration and thermal sensors have reduced equipment failure rates by 25–30% in automotive and heavy machinery plants. In process industries, wireless pressure and flow sensors improve yield stability by up to 12% through continuous process optimization. As manufacturers prioritize operational efficiency, throughput reliability, and data-driven quality control, wireless sensing becomes a foundational layer supporting advanced robotics, autonomous inspection, and closed-loop manufacturing control.

Industrial operators remain cautious about wireless deployments due to perceived risks related to network security, signal interference, and data integrity. Surveys indicate that nearly 48% of industrial firms cite cybersecurity as a primary barrier to expanding wireless infrastructure. Concerns include vulnerability to unauthorized access, potential disruption from electromagnetic interference, and reliability issues in harsh environments such as high-temperature or high-vibration zones. In regulated industries, data loss or corruption can lead to compliance violations and safety risks. These concerns increase spending on security layers, encryption, and redundancy, raising total system costs and slowing adoption among conservative operators.

Predictive maintenance adoption is expected to reach over 60% of asset-intensive enterprises within the next few years, creating significant demand for wireless sensing networks. Continuous monitoring enables early fault detection, extending asset life by up to 20% and reducing maintenance costs by approximately 25%. Wireless sensors allow coverage of previously inaccessible or mobile equipment, expanding monitoring scope without costly infrastructure. Integration with AI analytics further enhances diagnostic accuracy and enables autonomous maintenance scheduling. This evolution creates opportunities for vendors offering energy-efficient sensors, AI-ready platforms, and secure industrial networking solutions.

The market remains fragmented across multiple communication protocols, vendor ecosystems, and software platforms, creating integration complexity for end users. Approximately 42% of industrial firms report difficulties integrating new wireless sensors with legacy control systems and SCADA platforms. Lack of universal standards increases deployment time, customization costs, and long-term maintenance complexity. Additionally, global regulatory variations in radio frequency usage and industrial safety certifications complicate cross-border deployments. These challenges require coordinated industry standards, vendor collaboration, and regulatory harmonization to support seamless scaling of wireless sensing infrastructure across multinational industrial operations.

• Rapid expansion of AI-enabled predictive maintenance platforms is reshaping sensor deployment priorities, with over 64% of large industrial plants now integrating wireless vibration and thermal sensors directly into AI-based maintenance systems. These deployments have reduced unplanned equipment failures by 27% and extended average asset life by 18%. More than 52% of new sensor installations now include embedded edge analytics, enabling local anomaly detection with 35% faster response times compared to cloud-only monitoring architectures.

• Shift toward ultra-low-power and battery-free wireless sensors is accelerating large-scale adoption, with energy-harvesting devices now representing approximately 31% of new industrial sensor rollouts. These sensors achieve operating lifespans of 10–12 years without battery replacement and reduce maintenance interventions by 42%. Adoption is particularly high in hazardous and remote environments, where maintenance access costs are up to 38% higher than standard industrial facilities.

• Integration of 5G private networks and industrial-grade wireless protocols is transforming connectivity standards, with 5G-enabled industrial sites increasing by 46% over the last two years. Latency levels have fallen below 10 milliseconds in controlled industrial environments, improving real-time control precision by 29%. Over 58% of newly built smart factories now support multi-protocol wireless infrastructure combining 5G, WirelessHART, and ISA100 for resilient and redundant sensor communication.

• Rise in modular and prefabricated construction driving flexible sensor deployment models is changing demand patterns, as 55% of new industrial construction projects now use modular or prefabricated structures. These projects reduce on-site installation time by 33% and lower labor requirements by 28%, increasing reliance on pre-configured wireless sensor modules. Demand for plug-and-play wireless sensor kits has risen by 41%, particularly in Europe and North America, where standardized factory construction and rapid commissioning are strategic priorities.

The Industrial Wireless Sensors market is segmented by type, application, and end-user industry, reflecting how wireless sensing supports different operational objectives across sectors. By type, the market spans pressure, temperature, vibration, flow, gas, and multi-parameter sensors, each aligned with specific monitoring and control needs. By application, condition monitoring and predictive maintenance dominate, followed by process optimization, asset tracking, safety monitoring, and environmental compliance. By end user, manufacturing, energy and utilities, oil and gas, chemicals, and logistics account for the majority of deployments, while healthcare infrastructure and smart infrastructure projects represent emerging demand pools. These segments reflect a transition from reactive maintenance toward continuous monitoring, automation, and data-driven asset management. Increasing use of AI analytics, digital twins, and remote operations is influencing the type and performance requirements of sensors, while regulatory compliance and sustainability goals are shaping application priorities and industry adoption patterns.

Industrial wireless sensors are primarily classified into vibration, temperature, pressure, flow, gas, and multi-parameter sensors. Vibration sensors currently account for approximately 34% of total adoption, as they are critical for detecting mechanical wear, imbalance, and early-stage equipment faults in rotating machinery across manufacturing, mining, and energy facilities. Temperature sensors follow with about 27% adoption, supporting thermal management in furnaces, reactors, and electrical systems. However, multi-parameter sensors are the fastest-growing type, expanding at approximately 14% annually due to their ability to combine vibration, temperature, and humidity into a single device, reducing installation and maintenance complexity. Pressure and flow sensors together represent roughly 22% of deployments, primarily in oil and gas, chemicals, and water treatment, while gas sensors contribute around 7% in safety-critical environments.

Condition monitoring and predictive maintenance represent the largest application segment, accounting for approximately 41% of industrial wireless sensor usage, as companies seek to reduce downtime and extend asset life. Process optimization follows at about 29%, supporting yield improvement and energy efficiency in chemicals, food processing, and metals. Safety and compliance monitoring accounts for roughly 18%, particularly in hazardous industrial environments. Asset tracking and logistics monitoring together represent around 12%. Predictive maintenance is also the fastest-growing application, expanding at roughly 15% annually as AI-driven analytics mature and become more accessible. This growth is supported by the expansion of digital twins and machine learning platforms that rely on high-frequency sensor data.

Manufacturing is the largest end-user segment, representing approximately 38% of total deployments, driven by automotive, electronics, and heavy machinery producers implementing smart factory initiatives. Energy and utilities account for about 27%, using wireless sensors for grid monitoring, turbine diagnostics, and remote asset inspection. Oil and gas follows with around 19%, focused on safety, leak detection, and pipeline integrity. Logistics, chemicals, and water treatment together contribute approximately 16%. Logistics and warehousing are the fastest-growing end-user segment, expanding at roughly 16% annually as autonomous material handling and real-time inventory tracking gain traction.

North America accounted for the largest market share at 38% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12.6% between 2025 and 2032.

North America deployed more than 210 million industrial wireless sensors across manufacturing, energy, and logistics in 2024, while Asia-Pacific exceeded 195 million units driven by factory automation and infrastructure digitization. Europe followed with 27% share supported by regulatory-driven digital upgrades, while South America and the Middle East & Africa together accounted for 12% driven by energy, mining, and transport infrastructure projects. Industrial wireless sensor density reached 4.8 devices per production line in North America compared to 4.1 in Europe and 3.9 in Asia-Pacific. Over 64% of new smart factory projects in China, 58% in Germany, and 55% in the United States included wireless sensing infrastructure, highlighting regional variation in deployment maturity and industrial digitalization strategies.

This region accounts for approximately 38% of global industrial wireless sensor deployments, driven by manufacturing, energy, logistics, and utilities. Over 62% of large manufacturers have integrated wireless sensors into predictive maintenance systems, while 48% of utilities use them for grid and substation monitoring. Government-backed infrastructure modernization programs and industrial cybersecurity frameworks support adoption. Advanced use of 5G private networks and edge computing has improved sensor response latency by 29%. Local players are expanding AI-integrated sensor platforms to enable autonomous diagnostics. Enterprises show higher adoption in healthcare infrastructure and financial data centers for environmental and asset monitoring, reflecting diversified demand patterns.

Europe represents around 27% of global demand, with Germany, the UK, and France accounting for over 61% of regional deployments. Energy efficiency regulations and industrial emissions monitoring policies are driving adoption across chemicals, manufacturing, and utilities. Over 54% of new industrial projects integrate wireless environmental and process sensors to support compliance reporting. Digital twin adoption in manufacturing has increased by 34%, relying heavily on wireless data feeds. Regional suppliers are expanding low-power and recyclable sensor designs. Regulatory pressure encourages demand for transparent, auditable, and explainable sensing systems supporting operational and ESG reporting.

Asia-Pacific ranks second by volume and first by growth momentum, with China, Japan, and India accounting for nearly 68% of deployments. China alone installed over 78 million industrial wireless sensors in 2024 driven by electronics and automotive manufacturing. India increased deployments by 26% across logistics, power, and metro infrastructure. Smart industrial parks and manufacturing hubs are embedding wireless sensing as standard infrastructure. Local players focus on cost-efficient, scalable sensor manufacturing. Growth is driven by automation, e-commerce logistics, and mobile-first industrial management platforms.

South America contributes about 7% of global demand, led by Brazil and Argentina. Mining, oil and gas, and renewable energy projects account for over 62% of regional deployments. Government incentives for renewable integration and grid stability support sensor usage in wind and hydro projects. Local integrators are expanding wireless monitoring for remote assets to reduce maintenance travel by 35%. Demand is closely tied to infrastructure and resource sector modernization, with growing use in port logistics and transport networks.

This region holds approximately 5% of global demand, with the UAE, Saudi Arabia, and South Africa leading adoption. Oil and gas facilities represent over 46% of deployments, followed by construction and utilities. Smart city and industrial zone programs are integrating wireless sensors into energy and water management systems. Local regulations supporting digital oilfields and infrastructure resilience are encouraging deployment. Enterprises prioritize remote monitoring to address workforce constraints and harsh environmental conditions.

• United States – 24% share – High production capacity, advanced industrial automation, and early adoption of smart factory systems

• China – 21% share – Large-scale manufacturing base and rapid deployment of industrial digital infrastructure

The Industrial Wireless Sensors market is moderately fragmented, with more than 45 active global and regional vendors competing across hardware manufacturing, connectivity platforms, and analytics software. The top five companies together account for approximately 52% of total global deployments, indicating a semi-consolidated structure where scale, ecosystem partnerships, and technology depth are key competitive advantages. Large players focus on full-stack offerings combining sensors, gateways, cybersecurity, and analytics, while smaller specialists compete through niche innovations in ultra-low-power design, hazardous-environment sensing, or AI-enabled edge processing.

Strategic initiatives are heavily oriented toward partnerships with industrial automation providers, cloud platform vendors, and telecom operators. Over 38 strategic alliances and technology partnerships were announced between 2023 and 2025 to integrate wireless sensors with digital twin platforms, 5G private networks, and enterprise asset management systems. Product innovation is centered on multi-parameter sensing, edge AI integration, and battery-free energy harvesting, with more than 60 new industrial-grade wireless sensor models launched globally in the last two years. Mergers and acquisitions are focused on software analytics, cybersecurity, and interoperability capabilities, with over 14 transactions aimed at strengthening platform ecosystems and reducing integration complexity.

Competition increasingly revolves around reliability, security certification, interoperability with legacy systems, and total cost of ownership. Vendors differentiate through extended battery life exceeding 10 years, latency below 10 milliseconds, and compliance with industrial safety and data standards. As industrial buyers prioritize scalable, secure, and future-proof infrastructure, competitive positioning is shifting from standalone devices toward integrated, lifecycle-based industrial intelligence solutions.

Emerson Electric Co.

Yokogawa Electric Corporation

Schneider Electric SE

Rockwell Automation, Inc.

Endress+Hauser Group

TE Connectivity Ltd.

The Industrial Wireless Sensors market is being transformed by a combination of connectivity, intelligence, and energy-efficiency innovations. WirelessHART, ISA100, and 5G private networks are now deployed in over 58% of newly built smart factories, enabling low-latency, reliable communication for real-time monitoring of critical assets. Edge computing integration allows 42% of sensor data to be processed locally, reducing latency by up to 35% and enabling immediate anomaly detection without relying solely on cloud infrastructure. Multi-parameter sensors are increasingly common, representing roughly 31% of new deployments, combining vibration, temperature, and humidity measurements into a single device to reduce installation complexity and total maintenance interventions.

Energy-harvesting wireless sensors, capable of operating without battery replacement for 10–12 years, now account for nearly 28% of industrial deployments, particularly in remote or hazardous environments. AI-enabled sensor analytics is being adopted in more than 36% of predictive maintenance programs, improving fault detection accuracy by up to 33% compared with traditional threshold-based monitoring. Digital twin integration is another emerging trend, with over 40% of advanced manufacturing and energy facilities utilizing wireless sensors to feed real-time data into virtual replicas of physical assets, enhancing process optimization and resource allocation.

Cybersecurity and interoperability are also major technology considerations. More than 45% of industrial operators implement encrypted wireless protocols and redundant network architectures to ensure data integrity. Vendors are focusing on plug-and-play sensor modules with built-in edge analytics, low-power wireless communication, and environmental robustness, enabling rapid deployment across complex industrial environments. The convergence of AI, 5G, and edge computing positions industrial wireless sensors as critical enablers of operational efficiency, predictive maintenance, and digital transformation across manufacturing, energy, utilities, and logistics sectors.

• In July 2023, Honeywell launched its HPWF Series wireless pressure sensors featuring ultra‑low power consumption, long‑range LoRaWAN connectivity, and real‑time data transmission capabilities designed for remote and hazardous industrial environments, enhancing predictive maintenance and safety monitoring in oil & gas and utilities.

• In Q2 2024, Siemens introduced a new industrial wireless sensor platform optimized for Industrial IoT integration, enabling real‑time equipment monitoring and enhanced predictive analytics across manufacturing and process industries, expanding its IIoT product portfolio.

• In Q3 2024, Emerson expanded its Plantweb™ ecosystem with a new line of wireless vibration sensors targeting advanced asset health monitoring in process industries, integrating edge processing for faster fault detection and operational insight.

• In Q4 2024, Yokogawa Electric launched the Sushi Sensor, a rugged industrial wireless sensor designed for harsh operating environments, supporting remote monitoring and predictive maintenance across energy, petrochemical, and industrial automation applications.

The Industrial Wireless Sensors Market Report offers a comprehensive analysis of the industrial sensing ecosystem, covering a wide range of product types such as temperature, pressure, vibration, flow, gas, and multi‑parameter wireless sensors. It examines how these sensors integrate into broader Industrial IoT (IIoT) frameworks and edge analytics platforms, highlighting varied deployment scenarios from condition monitoring and predictive maintenance to asset tracking and environmental compliance. The report addresses key application segments including manufacturing automation, energy and utilities, oil & gas, chemicals, water treatment, and logistics, capturing detailed insights into usage patterns, performance requirements, and adaptation drivers across industries.

Geographically, the report evaluates regional markets including North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, offering in‑depth analysis of regional adoption trends, infrastructure readiness, regulatory influences, and technological preferences. Market segmentation includes connectivity technologies such as WirelessHART, ISA100, 5G private networks, LoRaWAN, NB‑IoT, and other LPWAN protocols, illustrating deployment variation and technical trade‑offs. The report also explores ancillary technologies like edge computing, embedded AI, and cloud platforms that enhance sensor data usability.

Beyond mainstream segments, the scope covers emerging niches such as energy‑harvesting devices, battery‑less sensors, modular sensor networks, and digital twin integration. It assesses buyer behavior, procurement criteria, system interoperability concerns, and performance benchmarks vital for decision‑makers. Strategic insights into competitive positioning, innovation trends, ecosystem partnerships, and barriers to adoption provide a holistic view enabling executives, product strategists, and technology planners to navigate current and future market opportunities effectively.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 3952 Million |

Market Revenue in 2032 | USD 7590.23 Million |

CAGR (2025 - 2032) | 8.5% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Siemens AG, Honeywell International Inc., ABB Ltd., Emerson Electric Co., Yokogawa Electric Corporation, Schneider Electric SE, Rockwell Automation, Inc., Endress+Hauser Group, TE Connectivity Ltd. |

Customization & Pricing | Available on Request (10% Customization is Free) |