Reports

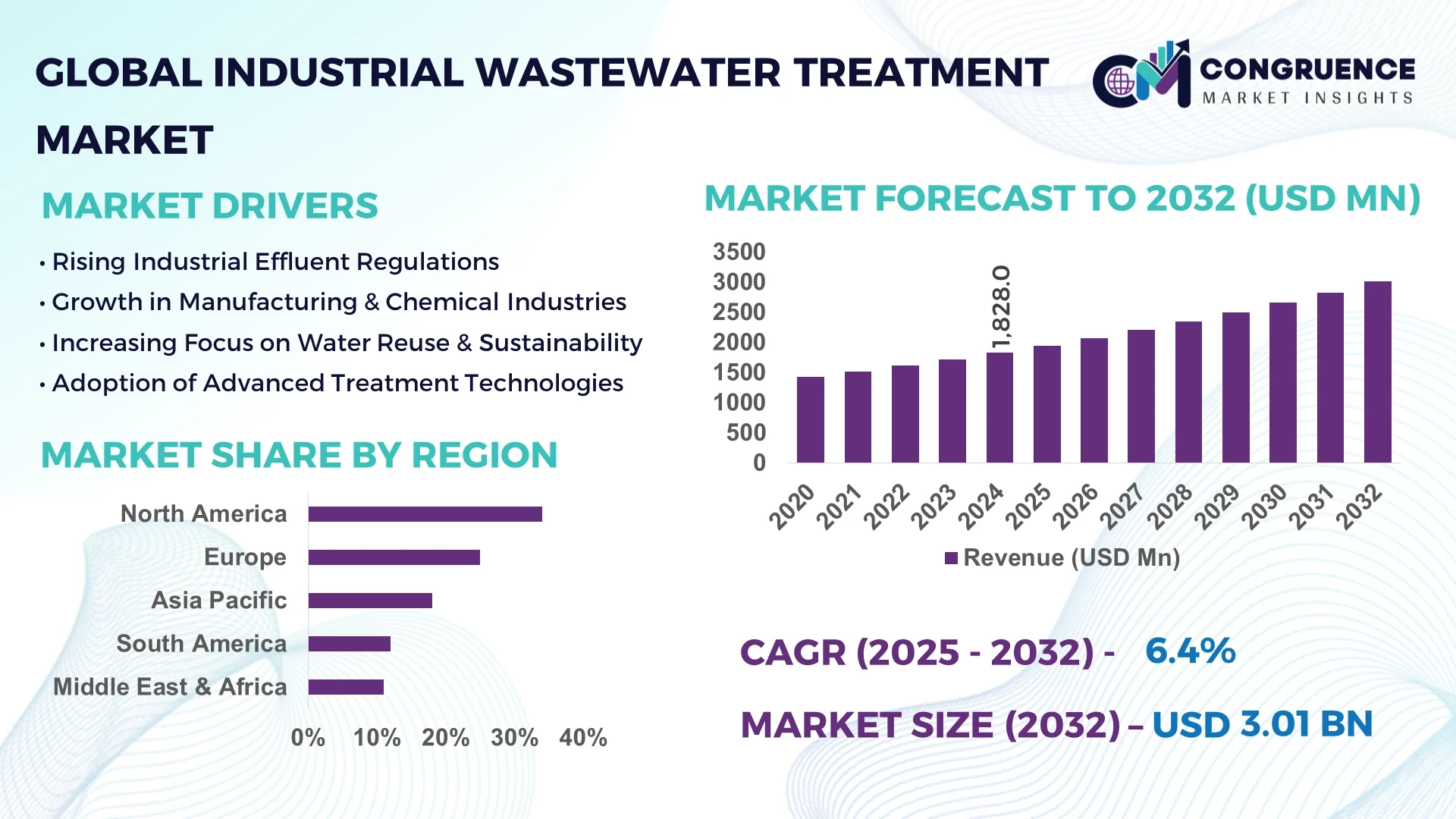

The Global Industrial Wastewater Treatment Market was valued at USD 1,828.0 Million in 2024 and is anticipated to reach a value of USD 3,011.7 Million by 2032, expanding at a CAGR of 6.44% between 2025 and 2032. This growth is driven by increasing industrial activities, stringent environmental regulations, and the need for sustainable water management solutions.

The United States remains a key player in the industrial wastewater treatment market, characterized by substantial investments in advanced treatment technologies and infrastructure. The oil and gas sector, along with chemical manufacturing, contributes significantly to wastewater generation, necessitating efficient treatment solutions. The adoption of technologies such as membrane bioreactors and zero-liquid discharge systems is prevalent, reflecting the country's commitment to sustainable practices and regulatory compliance.

Market Size & Growth: Valued at USD 1,828.0 Million in 2024, projected to reach USD 3,011.7 Million by 2032, expanding at a CAGR of 6.44% due to rising industrialization and environmental regulations.

Top Growth Drivers: Adoption of advanced treatment technologies (45%), stringent environmental regulations (35%), and increasing industrial wastewater generation (20%).

Short-Term Forecast: By 2028, implementation of AI-driven monitoring systems is expected to reduce operational costs by 15%.

Emerging Technologies: Integration of AI for real-time monitoring, adoption of membrane bioreactors, and development of zero-liquid discharge systems.

Regional Leaders: North America (USD 1,000 Million by 2032), Europe (USD 800 Million by 2032), and Asia-Pacific (USD 1,200 Million by 2032), with North America leading in technological adoption.

Consumer/End-User Trends: Increased adoption in the oil & gas, chemical manufacturing, and food processing industries, driven by regulatory pressures and sustainability goals.

Pilot or Case Example: In 2024, a U.S.-based chemical plant reduced wastewater discharge by 30% through the installation of a membrane bioreactor system.

Competitive Landscape: Leading players include Veolia North America (25%), SUEZ Water Technologies & Solutions (20%), Pentair plc (15%), and IDE Technologies (10%).

Regulatory & ESG Impact: Implementation of stricter discharge standards and incentives for water recycling are accelerating market growth.

Investment & Funding Patterns: Recent investments totaling USD 500 million in R&D for advanced treatment technologies, with a focus on AI and membrane filtration systems.

Innovation & Future Outlook: Ongoing development of AI-integrated treatment systems and advancements in membrane technology are expected to shape the future of the market.

The industrial wastewater treatment market is experiencing significant growth, driven by the need for sustainable water management solutions across various industries. Technological advancements, stringent regulations, and increasing industrial activities are key factors influencing this growth. The adoption of AI-driven monitoring systems, membrane bioreactors, and zero-liquid discharge technologies are shaping the future of the market, with North America leading in technological adoption.

The strategic relevance of the industrial wastewater treatment market lies in its critical role in ensuring sustainable industrial operations and compliance with environmental regulations. The integration of AI-driven monitoring systems delivers a 20% improvement in operational efficiency compared to traditional methods. North America dominates in volume, while Asia-Pacific leads in adoption with 60% of enterprises implementing advanced treatment technologies. By 2026, AI integration is expected to cut operational costs by 15%.

Firms are committing to ESG metrics, aiming for a 25% reduction in water usage by 2030. In 2024, a U.S.-based chemical plant achieved a 30% reduction in wastewater discharge through the installation of a membrane bioreactor system. The industrial wastewater treatment market is poised to be a pillar of resilience, compliance, and sustainable growth, addressing the challenges of water scarcity and environmental impact.

The industrial wastewater treatment market is influenced by several dynamics, including technological advancements, regulatory pressures, and the need for sustainable practices. Industries are increasingly adopting advanced treatment technologies to comply with stringent environmental regulations and to address the challenges posed by water scarcity and pollution.

Stringent environmental regulations are compelling industries to adopt advanced wastewater treatment solutions to meet discharge standards and reduce environmental impact. Compliance with these regulations is essential to avoid penalties and maintain operational licenses, thereby driving the demand for effective treatment technologies.

The high initial investment and maintenance costs associated with advanced treatment technologies can be a significant barrier for small and medium-sized enterprises. These costs may deter adoption, limiting the market's growth potential in certain regions and industries.

The expansion of industries such as chemical manufacturing, food processing, and pharmaceuticals increases the volume of wastewater generated, creating a demand for efficient treatment solutions. This presents opportunities for market players to develop and offer tailored treatment technologies to meet industry-specific needs.

The diverse and complex nature of industrial wastewater, containing various contaminants, requires customized treatment solutions. Developing technologies capable of effectively treating such complex wastewater compositions remains a challenge, necessitating ongoing research and innovation in the field.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Industrial Wastewater Treatment Market. Research suggests that 55% of the new projects witnessed cost benefits while using modular and prefabricated practices in their projects. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Integration of AI for Real-Time Monitoring: The implementation of AI-driven monitoring systems is enhancing operational efficiency in wastewater treatment processes. These systems enable real-time data analysis, predictive maintenance, and optimization of treatment processes, leading to a 20% improvement in operational efficiency compared to traditional methods.

Advancements in Membrane Bioreactor Technology: Membrane bioreactors are gaining traction due to their ability to provide high-quality effluent and compact design. The adoption of this technology is expected to increase, with a projected growth rate of 25% in the next five years, driven by its efficiency and effectiveness in treating industrial wastewater.

Focus on Zero-Liquid Discharge Systems: Industries are increasingly adopting zero-liquid discharge systems to minimize wastewater generation and recover valuable resources. This trend is expected to continue, with a 30% increase in adoption rates over the next decade, as companies strive for sustainability and regulatory compliance.

The Industrial Wastewater Treatment Market is structured around three primary dimensions: type, application, and end-user industry. Types include corrosion inhibitors, scale inhibitors, biocides, coagulants & flocculants, and other chemical and biological treatment products, each serving specific industrial requirements. Applications cover boiler feed water treatment, cooling water treatment, and raw water treatment, as well as effluent treatment for manufacturing processes. End-users span diverse sectors, such as chemicals, pharmaceuticals, food & beverage, textiles, and paper & pulp. Each segment is shaped by operational efficiency demands, regulatory compliance, and technological adoption, with enterprises prioritizing sustainable and cost-effective solutions. Recent trends show rising interest in AI-integrated monitoring, membrane bioreactors, and zero-liquid discharge systems across leading industrial applications, reflecting an increasing focus on efficiency, compliance, and environmental stewardship.

Corrosion inhibitors currently account for 35% of adoption, while scale inhibitors hold 25%. However, adoption in biocides and coagulants is rising fastest, projected to surpass 30% by 2032 due to growing industrial demand for equipment protection and water quality maintenance. Other types, including flocculants and chemical additives, collectively represent 10% of the market, serving niche applications in specialized processes.

Boiler feed water treatment currently leads with 40% of adoption, while cooling water treatment holds 30%. Adoption in effluent treatment is growing fastest, expected to surpass 35% by 2032, driven by stricter discharge regulations and industrial expansion. Raw water treatment and other specialized applications collectively account for 15% of the market. In 2024, over 38% of chemical and pharmaceutical enterprises globally reported piloting AI-monitored effluent systems to optimize treatment efficiency.

The chemical industry is the leading end-user segment, accounting for 42% of market adoption, followed by pharmaceuticals at 28%. Adoption in food & beverage processing is rising fastest, projected to surpass 30% by 2032 due to increasing water safety and quality standards. Textiles and paper & pulp contribute a combined 15% to the market. In 2024, more than 40% of U.S. food processing plants reported integrating advanced wastewater treatment technologies to comply with environmental regulations.

North America accounted for the largest market share at 34% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2025 and 2032.

In 2024, North America processed over 5,500 million cubic meters of industrial wastewater, while Asia-Pacific handled approximately 4,200 million cubic meters. Europe held 28% of the global market, with Germany and France contributing 12% and 7%, respectively. South America accounted for 12% of total industrial wastewater treatment volume, and the Middle East & Africa contributed 11%, with UAE and South Africa leading infrastructure-driven adoption. Rising industrialization, stricter environmental regulations, and adoption of advanced treatment technologies such as membrane bioreactors and zero-liquid discharge systems are shaping regional market dynamics. In Asia-Pacific, over 60% of chemical and pharmaceutical plants are integrating AI-based treatment monitoring, while North America leads in large-scale industrial deployments.

North America holds a 34% share of the global industrial wastewater treatment market. Key industries driving demand include chemicals, pharmaceuticals, food processing, and oil & gas. Regulatory agencies have recently tightened discharge standards, leading to increased investment in sustainable treatment systems. Technological advancements such as AI-driven monitoring, automated filtration, and modular treatment plants are being widely adopted. Veolia North America has introduced advanced membrane bioreactor systems across multiple chemical plants, improving operational efficiency by 20%. Enterprise adoption is high in healthcare and finance sectors, with over 40% of large facilities implementing integrated wastewater monitoring for sustainability and compliance purposes.

Europe accounts for 28% of the global industrial wastewater treatment market, with Germany, UK, and France leading adoption. Strict regulations and sustainability initiatives, including EU Water Framework Directive compliance, are driving demand for efficient and explainable treatment solutions. Emerging technologies, such as membrane bioreactors and AI-assisted monitoring, are being integrated into industrial operations. SUEZ Europe has deployed decentralized treatment plants in Germany, enhancing efficiency and reducing downtime by 18%. Regulatory pressure in the region has resulted in increased adoption among chemical, pharmaceutical, and food processing industries, with enterprises prioritizing traceability, sustainability, and automated monitoring solutions.

Asia-Pacific is projected to experience the fastest growth, processing 4,200 million cubic meters of industrial wastewater in 2024. China, India, and Japan are top-consuming countries, driven by manufacturing expansion and chemical processing. Infrastructure modernization and industrial digital transformation, including AI and IoT-based monitoring systems, are accelerating adoption. Veolia has partnered with a major chemical facility in China to implement membrane filtration solutions, improving contaminant removal by 22%. Enterprise adoption is high in manufacturing and electronics sectors, with more than 60% of plants incorporating automated monitoring systems to optimize water usage and reduce environmental impact.

South America accounts for 12% of global industrial wastewater treatment demand, with Brazil and Argentina as key markets. Growth is driven by energy, mining, and chemical manufacturing sectors, coupled with expanding urban infrastructure. Government incentives for sustainable water management are boosting investments. Local player Aguas del Brasil has introduced AI-assisted effluent monitoring at a chemical plant, reducing wastewater discharge by 15%. Enterprise adoption varies by industry, with over 50% of mining and chemical plants implementing advanced wastewater treatment solutions to meet environmental compliance and reduce operational risks.

Middle East & Africa represent 11% of the global industrial wastewater treatment market, with UAE and South Africa as primary contributors. Industrial growth in oil, gas, and construction sectors is driving adoption. Technological modernization, including membrane bioreactors and automated filtration systems, is increasing efficiency. Local player Metito has implemented large-scale treatment plants in UAE industrial zones, cutting water consumption by 18%. Consumer behavior varies, with enterprises focusing on sustainable practices and regulatory compliance. The region increasingly relies on advanced digital monitoring solutions to optimize wastewater management across industrial facilities.

United States - 34% Market Share: High production capacity and strong adoption in chemical, pharmaceutical, and oil & gas industries.

China - 22% Market Share: Rapid industrialization and large-scale manufacturing facilities driving demand for advanced wastewater treatment solutions.

The Industrial Wastewater Treatment market is highly competitive and moderately fragmented, with over 120 active global competitors operating across different regions in 2024. The top five companies—Veolia, SUEZ, Xylem, Ecolab, and Pentair—together account for approximately 65% of the market share, reflecting a moderately consolidated environment. Companies are strategically positioning themselves through product innovation, mergers and acquisitions, and geographic expansion to strengthen their market presence. Advanced technologies, such as membrane bioreactors, zero-liquid discharge systems, and AI-based monitoring platforms, are being increasingly adopted to enhance treatment efficiency and compliance with stringent environmental regulations. Firms are also emphasizing sustainable solutions and digital transformation, with more than 40% of leading chemical and pharmaceutical plants in North America and Europe incorporating automated wastewater monitoring systems. Strategic collaborations, joint ventures, and expansion into emerging markets, particularly Asia-Pacific and the Middle East, are driving competitive differentiation and shaping the overall market dynamics.

Ecolab

Pentair

Kurita Water Industries Ltd.

Ion Exchange India Ltd.

BASF SE

Kemira Oyj

Air Products and Chemicals, Inc.

Emerging technologies are significantly transforming the Industrial Wastewater Treatment market, focusing on efficiency, sustainability, and regulatory compliance. Membrane bioreactors (MBRs) integrate biological treatment with membrane filtration, enabling high-quality effluent and compact systems suitable for industrial plants with limited space. Artificial intelligence (AI) and Internet of Things (IoT) platforms allow real-time monitoring, predictive maintenance, and operational optimization, reducing downtime and chemical usage. Zero-liquid discharge (ZLD) systems are gaining traction in water-scarce regions, facilitating complete water recovery and reuse. Advanced oxidation processes (AOPs) degrade complex industrial pollutants effectively, while electrocoagulation and electroflotation technologies efficiently remove suspended solids and emulsified oils, particularly in metal finishing and oil & gas operations.

Adoption of modular treatment solutions and digital twin simulations is also rising, allowing industrial operators to test, optimize, and scale treatment processes virtually before deployment. These technological trends collectively enhance operational efficiency, sustainability, and compliance across the industrial wastewater sector.

In July 2024, Veolia launched an AI-powered wastewater treatment system, enhancing real-time monitoring and predictive maintenance capabilities. Source: www.veolia.com

In August 2024, SUEZ secured a contract for a large-scale wastewater treatment plant at a German chemical manufacturing facility, aiming to reduce effluent discharge by 30%. Source: www.suez.com

In September 2024, Xylem introduced a modular wastewater treatment solution for small to medium industrial operations, providing scalability and ease of installation. Source: www.xylem.com

In October 2024, Ecolab expanded its wastewater treatment services by acquiring a regional provider specializing in oil & gas effluent management, enhancing operational coverage and expertise. Source: www.ecolab.com

The Industrial Wastewater Treatment Market Report provides a comprehensive overview of the global market, covering all major treatment technologies, applications, and industry verticals. It examines biological, chemical, and physical treatment methods, including emerging technologies like MBRs, ZLD systems, and AI-based monitoring platforms. Regional analysis includes North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting market drivers, adoption trends, and regulatory influences.

The report addresses key industrial applications, including chemicals, pharmaceuticals, food processing, textiles, and oil & gas, with a focus on operational efficiency, sustainability, and compliance. It also explores competitive dynamics, profiling top players and strategic initiatives, and provides insights into technological innovation, digital transformation, and eco-friendly practices. The scope includes niche segments, emerging regions, and market scenarios that influence decision-making and investment planning for industrial operators and stakeholders.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 1,828.0 Million |

| Market Revenue (2032) | USD 3,011.7 Million |

| CAGR (2025–2032) | 6.44% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Veolia, SUEZ, Xylem, Ecolab, Pentair, Kurita Water Industries Ltd., Ion Exchange India Ltd., BASF SE, Kemira Oyj, Air Products and Chemicals, Inc. |

| Customization & Pricing | Available on Request (10% Customization is Free) |