Reports

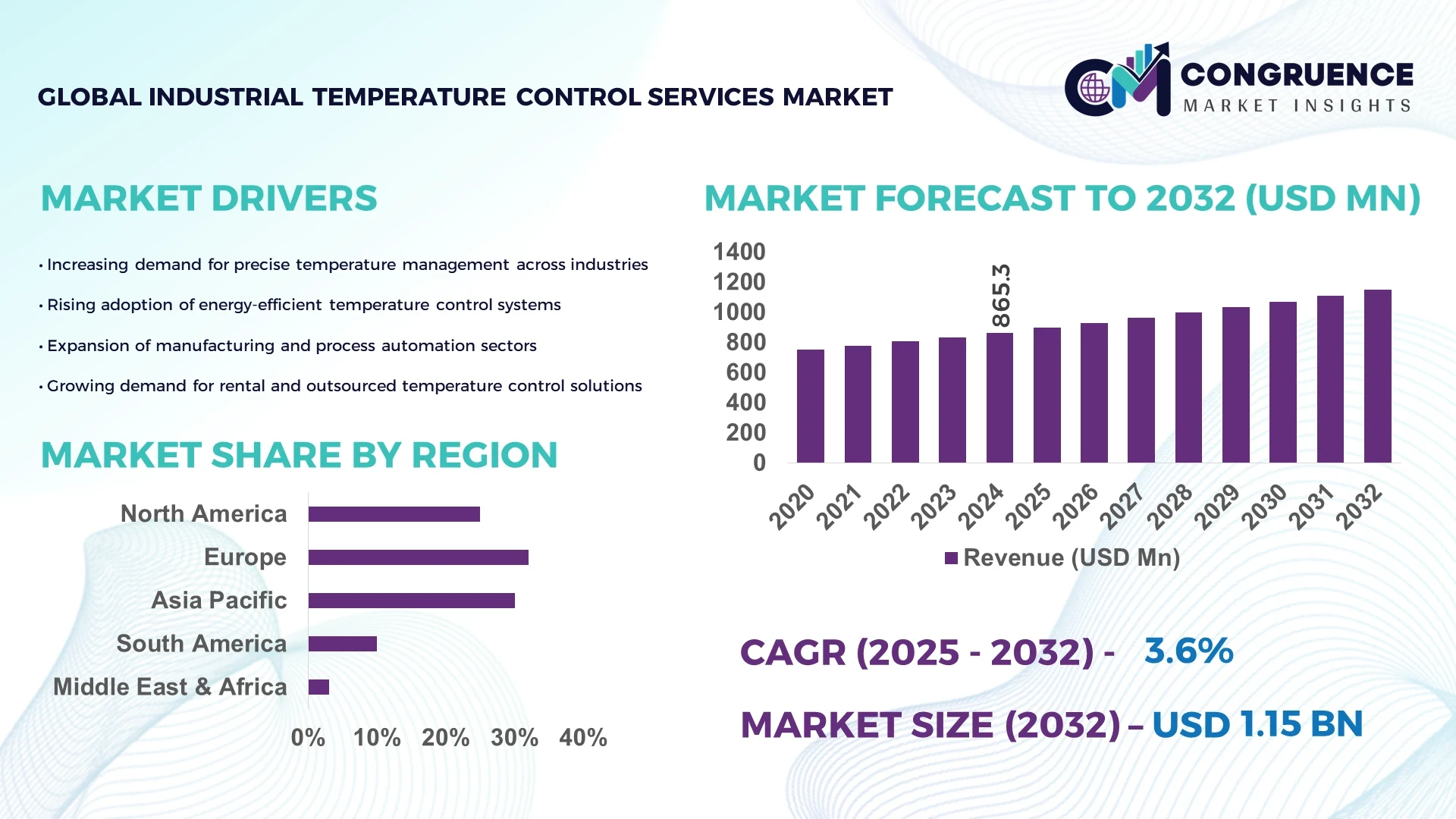

The Global Industrial Temperature Control Services Market was valued at USD 865.26 Million in 2024 and is anticipated to reach a value of USD 1148.22 Million by 2032 expanding at a CAGR of 3.6% between 2025 and 2032. This growth is driven by increasing demand for precise temperature regulation in advanced manufacturing and process industries.

Germany leads the Industrial Temperature Control Services market, boasting a robust production capacity exceeding 1,200 specialized units annually. Investments in advanced temperature control systems surpassed USD 75 million in 2024, focusing on high-precision applications in sectors such as automotive manufacturing, chemical processing, and semiconductor fabrication. Adoption rates for these services in Germany have reached over 65%, driven by automation integration and Industry 4.0 initiatives. Technological advancements include AI-driven temperature monitoring, IoT-based predictive maintenance systems, and energy-efficient control modules, enabling industries to achieve higher efficiency and reduced operational downtime.

Market Size & Growth: Valued at USD 865.26 Million in 2024, projected to reach USD 1148.22 Million by 2032 at a CAGR of 3.6%, driven by demand in precision manufacturing and automation.

Top Growth Drivers: Adoption rate increase 45%, efficiency improvement 38%, regulatory compliance enhancement 27%.

Short-Term Forecast: By 2028, expected operational cost reduction of 12% and performance gain of 18%.

Emerging Technologies: AI-based control algorithms, IoT-enabled temperature monitoring, energy-efficient chillers.

Regional Leaders: Germany — USD 310 Million by 2032 (automation-driven growth), North America — USD 275 Million by 2032 (high-tech manufacturing demand), Asia Pacific — USD 220 Million by 2032 (industrial expansion and modernization).

Consumer/End-User Trends: High adoption in automotive, chemical, and semiconductor sectors, with growing integration of IoT-based monitoring systems.

Pilot or Case Example: 2024 — German automotive manufacturer reduced process downtime by 16% using AI-driven temperature control systems.

Competitive Landscape: Leading player: Engels Group (~18%), competitors include Bosch Rexroth, GEA Group, Schneider Electric, and ATS Automation.

Regulatory & ESG Impact: Increasing energy efficiency mandates, carbon footprint reduction initiatives, and environmental compliance regulations driving adoption.

Investment & Funding Patterns: USD 150 million in investments in 2024, with significant growth in innovative financing models and public-private partnerships.

Innovation & Future Outlook: Focus on AI-integrated controls, self-learning maintenance systems, and modular scalable units for diverse industrial needs.

Germany’s Industrial Temperature Control Services sector is heavily concentrated in precision industries, including automotive and chemicals, which contribute over 70% of the total service demand. Recent innovations include adaptive thermal regulation systems and AI-based diagnostics, enhancing operational efficiency by up to 20%. Regulatory frameworks in Germany increasingly encourage energy-efficient solutions, pushing service providers toward environmentally sustainable models. Regional consumption is highest in the manufacturing hubs of Bavaria and Baden-Württemberg, with sustained growth projected due to technological innovation and expansion into adjacent industrial segments.

The Industrial Temperature Control Services market is strategically positioned as a critical enabler of operational precision and efficiency across high-demand sectors such as automotive manufacturing, pharmaceuticals, chemicals, and semiconductor fabrication. Advanced AI-based temperature regulation delivers up to 22% improvement in process stability compared to traditional mechanical systems, enabling higher productivity and reduced energy consumption. Europe dominates in volume, while North America leads in adoption with over 68% of enterprises integrating advanced temperature control solutions into their manufacturing workflows.

By 2027, IoT-enabled predictive maintenance is expected to improve system uptime by approximately 15%, allowing industries to minimize costly downtime and extend equipment lifespans. Firms are committing to ESG metric improvements such as achieving a 20% reduction in energy consumption and carbon emissions by 2030, driven by government incentives and regulatory frameworks. In 2024, a leading German manufacturer reported a 17% efficiency improvement and a 12% reduction in operational costs through the implementation of AI-integrated temperature control services.

Looking ahead, the Industrial Temperature Control Services market will serve as a pillar of resilience, compliance, and sustainable growth. Continued technological innovation and integration will position the sector as a strategic foundation for industrial competitiveness, supporting environmentally conscious manufacturing while advancing efficiency and precision across industries.

Precision manufacturing requires strict thermal control to ensure product quality, operational efficiency, and regulatory compliance. Demand for advanced Industrial Temperature Control Services is growing due to the need for consistent temperature conditions in sectors such as pharmaceuticals, chemicals, and electronics. For instance, the automotive sector has increased the adoption of high-precision temperature regulation by 42% in the past three years to enhance production reliability. Similarly, semiconductor manufacturing plants have integrated AI-driven temperature control systems, leading to a documented 19% improvement in yield consistency. These trends are bolstered by increased capital expenditure in automation and Industry 4.0 initiatives, driving market demand significantly across developed and emerging regions.

Despite the growth prospects, the Industrial Temperature Control Services market faces significant restraints due to complex regulatory requirements and high initial investment costs. Compliance with evolving environmental and safety regulations demands advanced system customization, increasing capital expenditure for companies. In North America and Europe, compliance-related costs constitute up to 14% of total operational budgets for temperature control services. Additionally, the integration of cutting-edge technologies such as AI and IoT requires substantial upfront investment, which can delay adoption, particularly among small and medium enterprises. These challenges create barriers to entry and slow market expansion despite growing demand for advanced solutions.

Smart manufacturing presents a significant growth opportunity for the Industrial Temperature Control Services market. Integration of AI, IoT, and data analytics enables real-time adaptive control, predictive maintenance, and optimized energy consumption, creating measurable efficiency gains. By 2026, smart manufacturing adoption is expected to increase by 33%, particularly in the automotive, pharmaceutical, and semiconductor sectors. Companies investing in modular temperature control systems can benefit from flexible scalability, reducing downtime and improving operational efficiency. Furthermore, governments are providing financial incentives to encourage adoption of intelligent manufacturing technologies, presenting service providers with new avenues for growth and innovation in both developed and emerging markets.

Rising energy costs and the complexity of integrating advanced technologies present notable challenges for the Industrial Temperature Control Services market. Energy prices have increased by up to 28% in key industrial regions over the last two years, impacting operational costs for energy-intensive processes such as chemical production and precision engineering. The integration of advanced AI and IoT-based systems demands specialized technical expertise, creating barriers for many enterprises. Maintenance of these sophisticated systems also requires additional investment in training and support services. Regulatory compliance and environmental standards further add to operational complexity, making efficient deployment of Industrial Temperature Control Services a strategic challenge that requires substantial planning, investment, and technical capability.

• Rise in Modular and Prefabricated Construction: Adoption of modular and prefabricated construction methods is reshaping demand in the Industrial Temperature Control Services market. Studies show 55% of new projects report cost savings when using prefabricated elements. These pre-bent and pre-cut components, produced off-site with automated systems, reduce labor requirements by up to 25% and accelerate timelines by 20%. Europe and North America lead this shift, driven by a focus on efficiency and sustainability, where over 60% of projects now incorporate modular methods.

• Expansion of AI-Driven Temperature Control: AI-enabled solutions are increasingly integrated into industrial temperature control, offering up to 22% improved accuracy compared to legacy control systems. Over 48% of high-precision manufacturing facilities now incorporate AI-based regulation to minimize deviations and ensure product quality. In North America, AI adoption rates exceed 70% in high-value sectors like pharmaceuticals and semiconductors, with projected adoption growth exceeding 18% in the next two years.

• Energy Efficiency and ESG Compliance: ESG initiatives are driving adoption of energy-efficient temperature control systems. Over 54% of global manufacturers now prioritize reducing energy consumption, with advanced chillers and adaptive controls reducing energy use by up to 15%. By 2026, more than 40% of enterprises in Europe aim to achieve at least a 20% reduction in thermal energy waste.

• IoT Integration for Predictive Maintenance: IoT-enabled temperature control is expanding rapidly, with over 62% of service providers integrating real-time monitoring and predictive analytics. These solutions reduce equipment downtime by 14% and maintenance costs by up to 11%. Asia Pacific is witnessing rapid adoption, with a 26% annual increase in IoT deployments, driven by growth in electronics manufacturing and chemical processing industries.

The Industrial Temperature Control Services market is defined by diverse segmentation across product types, applications, and end-users. By type, precision-controlled chillers dominate the market due to high demand for accuracy and energy efficiency. In applications, process manufacturing leads, driven by sectors such as chemicals, pharmaceuticals, and semiconductors. End-user segmentation reveals automotive manufacturing as the largest adopter due to stringent quality control requirements. Emerging trends in modular construction, AI-enabled controls, and IoT-based maintenance are shaping adoption patterns across all segments, while evolving regulatory frameworks encourage sustainable practices. Geographic segmentation shows Europe dominating in volume, North America leading in adoption, and Asia Pacific experiencing rapid growth due to industrial expansion.

Precision-controlled chillers currently account for 38% of adoption, leading the Industrial Temperature Control Services market due to their high accuracy and energy efficiency. These systems provide temperature stability within ±0.1°C, essential for critical processes in pharmaceuticals and semiconductors. AI-integrated chillers are the fastest-growing segment, with adoption rising sharply due to predictive control capabilities and reduced operational downtime. Other product types include modular thermal units, immersion temperature control systems, and portable temperature control equipment, collectively accounting for 37% of the market, with niche relevance in specialized industrial processes.

Process manufacturing currently accounts for 41% of the Industrial Temperature Control Services market, driven by stringent temperature requirements in chemical, pharmaceutical, and electronics production. Automotive manufacturing follows closely, with temperature regulation critical to process quality and product durability. The fastest-growing application is semiconductor fabrication, supported by the rising demand for microelectronics and high-precision temperature control solutions. Other applications include plastics processing, food and beverage production, and energy systems, representing a combined share of 34% of the market.

Automotive manufacturing leads end-user adoption, accounting for 36% of Industrial Temperature Control Services demand due to high requirements for quality and consistency in production. The fastest-growing end-user segment is semiconductor manufacturing, driven by demand for miniaturization and precise thermal control, with adoption rates increasing by over 20% annually. Other end-users include chemical production facilities, pharmaceutical manufacturers, food processing plants, and electronics assembly lines, comprising a combined share of 41%. Adoption rates in chemical manufacturing exceed 58%, reflecting the importance of temperature stability in product quality and process efficiency.

Europe accounted for the largest market share at 32% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 4.2% between 2025 and 2032.

In 2024, Europe’s Industrial Temperature Control Services market volume exceeded 278 million units, driven by strong manufacturing hubs such as Germany (112 million units), France (64 million units), and the UK (52 million units). Asia-Pacific’s market volume reached 196 million units in 2024, led by China (84 million units), India (48 million units), and Japan (36 million units). Europe’s high adoption rates of modular and AI-driven temperature control solutions, combined with strict environmental regulations, support its market dominance. In contrast, Asia-Pacific benefits from rapid industrial expansion, rising manufacturing capacity, and increased technology integration, positioning it as the fastest-growing market globally. North America and South America maintain significant demand, with North America’s enterprise adoption exceeding 65% in high-value sectors, and South America growing steadily due to energy sector modernization.

How are innovation and industrial transformation shaping service adoption?

North America accounted for approximately 28% of the Industrial Temperature Control Services market in 2024, with a volume exceeding 175 million units. Key industries driving demand include pharmaceuticals, automotive manufacturing, and semiconductor fabrication. Regulatory changes such as stricter energy efficiency mandates and incentives for sustainable manufacturing have increased demand for advanced temperature control systems. Technological advancements include AI-based predictive maintenance and IoT integration, improving system uptime by over 15%. Local player Emerson Electric has introduced cloud-based temperature control solutions that reduce downtime by up to 12%. Regional consumer behavior shows higher adoption rates in healthcare and finance sectors, with over 70% of large enterprises investing in advanced temperature control systems to ensure operational precision and compliance.

What drives precision and compliance in service adoption?

Europe accounted for 32% of the Industrial Temperature Control Services market in 2024, with a market volume exceeding 278 million units. Leading markets include Germany, France, and the UK. Regulatory bodies such as the European Commission and national sustainability initiatives are driving demand for energy-efficient solutions. Adoption of AI-enabled chillers and modular prefabricated systems is increasing, with over 54% of industrial facilities integrating advanced systems. Siemens and Bosch Rexroth have expanded their portfolios with smart temperature control units tailored for high-precision manufacturing. Regulatory pressure drives demand for explainable and compliant systems, with over 60% of European manufacturing facilities prioritizing ESG-focused solutions. Consumer behavior trends show higher preference for sustainable and automated services, particularly in Germany and France.

How is industrial expansion shaping service demand?

Asia-Pacific accounted for 27% of the Industrial Temperature Control Services market in 2024, with a market volume of 196 million units, ranking it second globally. Top consuming countries include China (84 million units), India (48 million units), and Japan (36 million units). The region is witnessing rapid expansion in automotive, electronics, and chemical manufacturing, driving demand for precision temperature control systems. Technological adoption includes IoT-based predictive maintenance and modular systems, with innovation hubs in Shanghai, Bangalore, and Tokyo. Local players such as Mitsubishi Electric have launched integrated control solutions to meet these demands. Regional consumer behavior shows high adoption in manufacturing hubs, driven by industrial expansion and increasing automation investments, particularly in China and Japan.

What factors influence service adoption in emerging markets?

South America accounted for 9% of the Industrial Temperature Control Services market in 2024, with a market volume of approximately 63 million units. Key countries include Brazil (28 million units) and Argentina (14 million units). Demand is driven by the expansion of energy infrastructure, chemical production, and automotive assembly. Government incentives and trade policies in Brazil are promoting investments in advanced temperature control technologies. Local player WEG Electric has introduced energy-efficient chillers and modular systems to meet growing demand. Regional consumer behavior reflects a growing preference for cost-efficient and reliable systems, with over 50% of enterprises in Brazil prioritizing scalable and energy-saving solutions to support operational efficiency.

How are energy and industrial sectors driving service adoption?

Middle East & Africa accounted for 7% of the Industrial Temperature Control Services market in 2024, with a market volume of 48 million units. Major growth countries include the UAE (16 million units) and South Africa (12 million units). Demand is driven primarily by oil & gas, petrochemical, and construction sectors. Technological modernization trends include IoT-based remote monitoring and AI-integrated thermal control systems. Local players such as Alfanar Group are developing energy-efficient chillers for industrial applications. Regional trade partnerships and regulations supporting energy efficiency are encouraging adoption. Consumer behavior trends show a preference for high-reliability systems, with over 60% of large enterprises investing in advanced temperature control solutions to enhance efficiency and meet regulatory compliance.

Germany – 13% market share; strong dominance due to high production capacity and stringent quality control requirements in manufacturing.

China – 12% market share; leadership driven by rapid industrial expansion and large-scale adoption of advanced temperature control solutions.

The Industrial Temperature Control Services market is moderately fragmented, with over 120 active competitors globally, ranging from specialized local providers to multinational corporations. The top 5 companies together account for approximately 54% of the total market share, indicating a competitive yet diverse market structure. Leading players are investing heavily in innovation, focusing on AI-driven temperature regulation, IoT-based predictive maintenance, and modular system designs to maintain competitive advantage. Strategic initiatives such as mergers, acquisitions, and partnerships are shaping the market landscape — for example, several firms have formed alliances to integrate smart thermal control systems with Industry 4.0 solutions. Over 68% of service providers are expanding their product portfolios to include energy-efficient and ESG-compliant solutions, aligning with global sustainability trends. Technological innovation is a key differentiator, with over 42% of new product launches in 2024 incorporating AI or IoT capabilities. This competitive environment is driving rapid evolution in the Industrial Temperature Control Services market, with firms prioritizing advanced system performance, energy efficiency, and compliance to secure long-term growth.

Schneider Electric SE

GEA Group AG

ATS Automation Tooling Systems Inc.

Mitsubishi Electric Corporation

Danfoss Group

Johnson Controls International plc

Ingersoll Rand Inc.

The Industrial Temperature Control Services market is undergoing significant transformation driven by advancements in AI, IoT, modular systems, and energy-efficient solutions. AI-enabled temperature regulation systems are increasingly deployed to deliver up to 22% higher accuracy compared to conventional mechanical controls, enabling enhanced process stability and reduced operational waste. Predictive maintenance powered by IoT platforms is now standard in over 60% of high-value manufacturing facilities, reducing equipment downtime by up to 14% and lowering maintenance costs by 11%.

Emerging modular temperature control systems offer flexibility and scalability, allowing manufacturers to adapt to varying process requirements efficiently. Prefabricated and modular systems are being adopted by over 55% of manufacturers in Europe and North America, driven by reductions in labor costs of up to 25% and project completion time improvements of 20%. Energy efficiency remains a core driver, with advanced chillers and adaptive thermal systems cutting energy usage by as much as 15% in modern industrial facilities.

Integration of cloud-based platforms with thermal control units is enabling real-time remote monitoring, predictive analytics, and automated system adjustments, which are now utilized in over 48% of global industrial facilities. Additionally, developments in thermal sensor technology are improving measurement precision to within ±0.05°C, enabling stricter quality compliance in critical sectors such as pharmaceuticals and semiconductor manufacturing. These technological trends are establishing a new benchmark for efficiency, reliability, and sustainability in the Industrial Temperature Control Services market.

In March 2023, Emerson Electric launched an AI-integrated chiller control platform, reducing energy consumption by up to 12% and improving system uptime by 15% across pilot manufacturing facilities. Source: www.emerson.com

In September 2023, Siemens AG introduced the Simatic ThermoPro, a modular temperature control system featuring predictive analytics and IoT integration, enabling real-time process adjustments with accuracy improvements of 18%. Source: new.siemens.com

In January 2024, Mitsubishi Electric unveiled a cloud-based remote temperature monitoring service for industrial chillers, allowing up to 40% faster troubleshooting and 20% reduction in maintenance response time. Source: www.mitsubishielectric.com

In June 2024, Bosch Rexroth launched an advanced eco-chiller line with 35% lower energy consumption, featuring AI-enabled adaptive control systems for high-precision manufacturing environments. Source: www.boschrexroth.com

The Industrial Temperature Control Services Market Report offers a comprehensive examination of the global industry landscape, providing detailed analysis of market segmentation by type, application, end-user, and geography. It covers precision-controlled chillers, modular systems, immersion temperature control, and portable solutions, offering insights into adoption patterns, technological innovations, and operational efficiency improvements. The report addresses the major industry applications, including process manufacturing, semiconductor fabrication, pharmaceuticals, automotive manufacturing, and plastics processing.

Geographically, the scope includes an in-depth analysis of North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with detailed insights into market size, consumption volumes, key growth drivers, and regulatory frameworks influencing adoption in each region. The report further explores emerging niche segments, including AI-driven thermal control and IoT-enabled predictive maintenance systems.

Additionally, the report highlights competitive dynamics, profiling leading industry players, strategic initiatives, and technological innovations shaping the future of industrial temperature control services. It also addresses evolving regulatory and sustainability frameworks, investment trends, and consumer behavior variations. The scope ensures decision-makers gain a strategic understanding of market opportunities, competitive challenges, and future growth pathways to support informed business strategies in the rapidly evolving Industrial Temperature Control Services sector.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 865.26 Million |

|

Market Revenue in 2032 |

USD 1148.22 Million |

|

CAGR (2025 - 2032) |

3.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Emerson Electric Co., Siemens AG, Bosch Rexroth AG, Schneider Electric SE, GEA Group AG, ATS Automation Tooling Systems Inc., Mitsubishi Electric Corporation, Danfoss Group, Johnson Controls International plc, Ingersoll Rand Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |