Reports

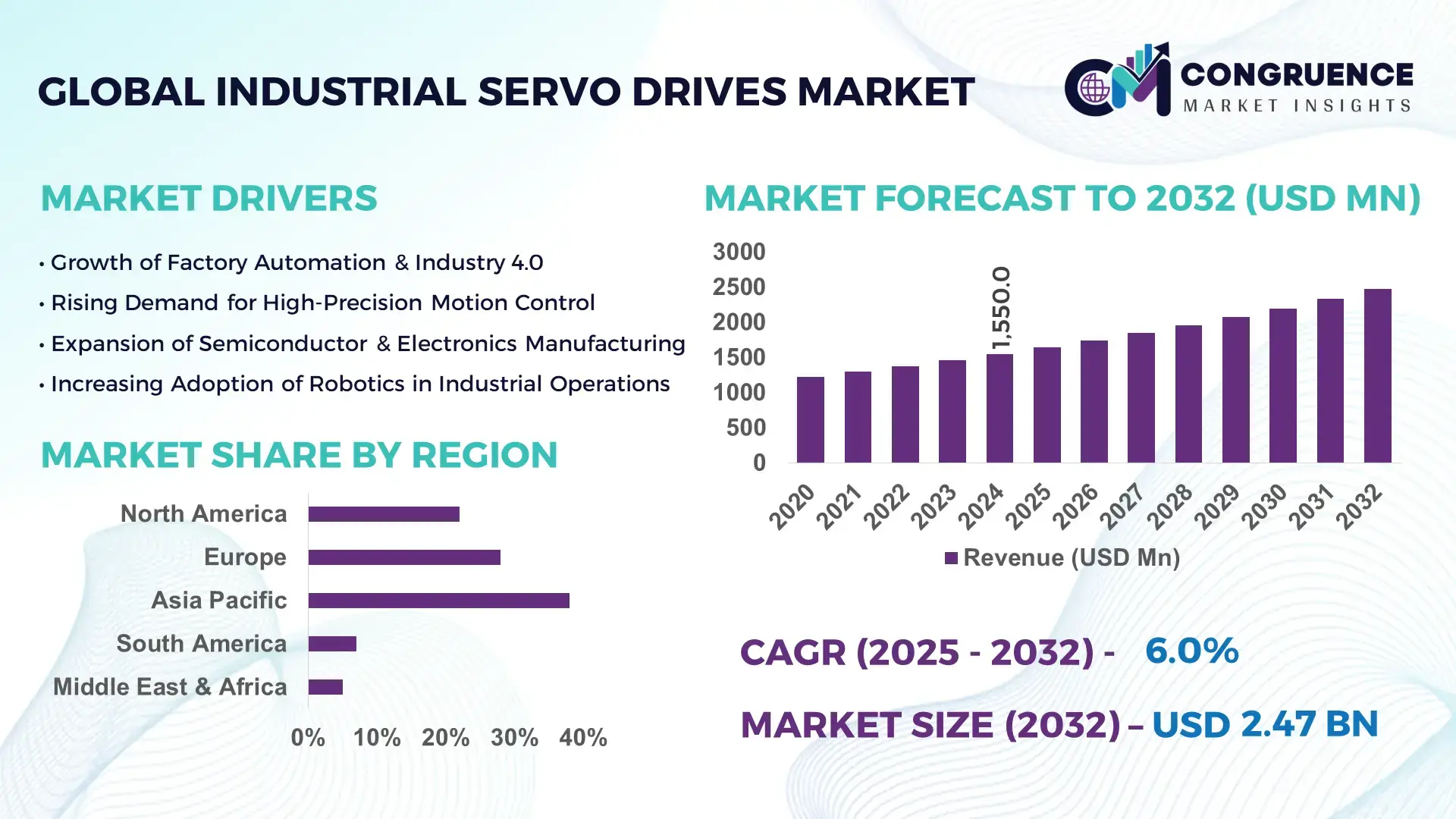

The Global Industrial Servo Drives Market was valued at USD 1,550.0 Million in 2024 and is anticipated to reach a value of USD 2,470.5 Million by 2032 expanding at a CAGR of 6.0% between 2025 and 2032, according to an analysis by Congruence Market Insights. The growth is primarily driven by rising adoption of automation and robotics across manufacturing sectors globally.

Japan dominates the Industrial Servo Drives Market with advanced production capacity and consistent investments exceeding USD 500 Million annually in drive and motor technology R&D. Key industrial applications include precision robotics, semiconductor manufacturing, and automotive automation lines. Technological advancements such as high-torque compact servo drives and AI-enabled motion control systems have boosted productivity by 25% in high-volume manufacturing facilities. Regional production hubs like Nagoya and Osaka report annual output exceeding 150,000 units, while adoption of integrated servo systems in Japanese factories exceeds 70%, reflecting robust operational efficiency.

Market Size & Growth: USD 1,550.0 Million in 2024, projected USD 2,470.5 Million by 2032, driven by automation adoption and industrial digitization.

Top Growth Drivers: Automation adoption 68%, efficiency improvement 52%, robotics integration 46%.

Short-Term Forecast: By 2028, predictive maintenance tools are expected to reduce operational downtime by 22%.

Emerging Technologies: AI-enabled servo controls, high-torque compact drives, cloud-integrated monitoring systems.

Regional Leaders: Japan USD 620M, Germany USD 480M, USA USD 430M by 2032; Japan focuses on precision robotics, Germany on automotive automation, USA on semiconductor production.

Consumer/End-User Trends: Heavy adoption in automotive assembly lines, semiconductor fabs, and packaging machinery; preference for integrated smart servo systems.

Pilot or Case Example: In 2025, a Japanese electronics plant reduced servo system downtime by 18% through AI-driven predictive control.

Competitive Landscape: Yaskawa Electric (~20%), Siemens, Mitsubishi Electric, ABB, Fanuc.

Regulatory & ESG Impact: Compliance with ISO 14001 and energy-efficiency standards; incentives for eco-friendly automation.

Investment & Funding Patterns: USD 520M recent R&D investment; rising venture funding in AI-based servo solutions.

Innovation & Future Outlook: Integration of AI and IIoT, next-gen predictive maintenance, and smart factory-ready servo systems shaping future growth.

The Industrial Servo Drives Market continues to evolve with dominant sectors including automotive, semiconductor, and robotics. New compact servo drives, AI-driven motion control, and energy-efficient systems are being adopted. Regulatory focus on energy efficiency and automation standards is supporting growth. Regional consumption trends indicate strong adoption in Asia, North America, and Europe, with emerging markets increasingly investing in precision industrial drives.

The Industrial Servo Drives Market is strategically critical as manufacturers seek higher precision, energy efficiency, and automation integration. Advanced AI-enabled servo systems deliver 25% improvement in production accuracy compared to conventional PLC-controlled motors. Japan dominates in volume, while Germany leads in adoption with over 65% of industrial facilities employing advanced servo systems.

In the short term, by 2027, predictive analytics integrated with servo drives is expected to reduce machine downtime by 20% and lower operational costs by 12%. Firms are committing to ESG improvements such as 15% reduction in energy consumption in manufacturing lines by 2030. In 2025, a German automotive manufacturer achieved an 18% efficiency gain through AI-enabled torque optimization across assembly lines.

Future pathways include integration with Industry 4.0, cloud-based monitoring, and high-precision robotics. These systems provide measurable operational gains, regulatory compliance, and scalable deployment across global facilities. The Industrial Servo Drives Market is positioned as a pillar of resilience, compliance, and sustainable growth for modern industrial operations.

The Industrial Servo Drives Market is experiencing dynamic growth driven by industrial automation, robotics, and energy-efficient manufacturing. Companies are increasingly replacing legacy systems with high-precision servo drives capable of handling complex motion control tasks. Demand is rising for AI-integrated systems that allow predictive maintenance, reduced downtime, and real-time performance monitoring. Asia-Pacific remains a hotbed for technological adoption, while Europe emphasizes energy efficiency and sustainability in servo solutions. Competitive pressures are leading manufacturers to innovate with compact, high-torque, and IoT-connected drives to meet evolving industrial needs.

The integration of automation in manufacturing has accelerated demand for Industrial Servo Drives. Automation adoption across automotive, electronics, and packaging sectors is reported at over 68%, enhancing precision and reducing labor costs by 30%. Factories increasingly implement servo drives with AI-enabled predictive maintenance, improving machine uptime by 22% in high-volume production lines. Robotics and automated assembly lines rely on these drives for complex motion control, enhancing throughput, reliability, and energy efficiency across industrial operations.

The high upfront capital expenditure associated with industrial servo drive systems limits adoption, particularly in small and medium enterprises. A single high-torque servo drive unit can cost between USD 8,000–15,000, excluding integration costs. Maintenance and skilled operator requirements add further financial burden. Additionally, rapid technological advancements necessitate frequent upgrades, increasing lifecycle costs. As a result, some industrial operators delay or scale down implementation, impacting market expansion despite evident operational benefits.

Industry 4.0 initiatives offer significant opportunities for Industrial Servo Drives, especially in predictive maintenance, IIoT integration, and cloud-based monitoring. Factories adopting smart manufacturing report 20–25% improvement in throughput using AI-integrated servo systems. Emerging applications in semiconductor fabrication and precision robotics expand the market potential. Upgrading legacy machinery with modular servo drives enables flexible production lines, opening new revenue channels in emerging economies where automation penetration is below 50%.

Stringent energy-efficiency and environmental regulations require servo drives to meet ISO 50001 and other energy standards. Non-compliance results in fines and restricts access to government contracts. Transitioning to energy-efficient drives requires investment in R&D and retrofitting existing equipment. Additionally, fluctuating electricity prices increase operational costs, deterring adoption. Manufacturers must balance performance, compliance, and cost, presenting a complex challenge for sustained market growth.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Industrial Servo Drives Market. Research suggests that 55% of the new projects witnessed cost benefits while using modular and prefabricated practices in their projects. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

AI-Enabled Predictive Maintenance: By 2025, 62% of high-volume factories had implemented AI-driven predictive maintenance with servo drives, resulting in an average downtime reduction of 18%. Real-time monitoring and predictive analytics allow operators to proactively address failures, optimize production schedules, and extend equipment lifespan.

Compact High-Torque Drives Adoption: Compact, high-torque servo drives are increasingly used in automotive and electronics manufacturing. In Japan, 70% of new robotic assembly lines adopted high-torque units in 2024, reducing energy consumption per unit by 12% and improving assembly precision by 20%.

IIoT Integration and Smart Factories: Industrial facilities integrating IIoT-connected servo drives have achieved operational efficiency gains of 15–25%. Real-time data collection enables improved process monitoring, remote diagnostics, and adaptive control, particularly in semiconductor, packaging, and electronics sectors.

The Industrial Servo Drives Market is organized into distinct segments based on type, application, and end-user, each reflecting specific adoption patterns and operational benefits. By type, the market includes AC servo drives, DC servo drives, and integrated servo systems, which are employed across precision manufacturing, robotics, and automotive automation. Applications span factory automation, semiconductor production, packaging machinery, and metalworking. End-users include automotive OEMs, electronics manufacturers, industrial machinery firms, and logistics facilities. Across these segments, decision-makers prioritize precision, energy efficiency, and automation compatibility. Regional variations exist in adoption, with Asia-Pacific investing heavily in high-torque drives, Europe focusing on energy efficiency, and North America integrating predictive maintenance solutions. This segmentation overview provides insights for strategic investment and product development decisions, highlighting which segments are advancing technology adoption and which are expanding market penetration.

AC servo drives currently lead the Industrial Servo Drives Market, accounting for approximately 48% of adoption due to their superior torque control, energy efficiency, and reliability in high-precision applications such as automotive assembly lines and robotics. DC servo drives hold about 30% of adoption but are gradually being integrated into hybrid systems for specialized industrial applications. Integrated servo systems comprise the remaining 22%, serving niche applications like packaging and lab automation where compact form factors and simplified wiring offer operational advantages. The fastest-growing type is integrated servo systems, driven by increasing adoption in small-scale automated production lines and robotics, supported by modular design flexibility. Recent integration of AI-driven motion control enhances their utility, boosting adoption rates.

Factory automation remains the leading application segment, accounting for approximately 45% of global adoption, largely due to the need for precision motion control in automotive, electronics, and industrial machinery production. Semiconductor manufacturing is a key growth area, currently representing 25% of adoption, with rapid integration of AI-driven servo control systems expected to enhance precision and throughput. Packaging machinery and metalworking constitute the remaining 30%, serving specialized production lines requiring high-speed repetitive motion. In 2024, over 40% of automotive assembly plants globally reported upgrading to servo-driven automated lines for efficiency gains. Similarly, more than 55% of semiconductor fabrication facilities in East Asia adopted AI-enhanced servo systems to improve yield and reduce operational variance.

Automotive OEMs constitute the leading end-user segment, accounting for 42% of Industrial Servo Drives Market adoption, driven by high-precision robotic assembly lines and advanced torque control requirements. Electronics manufacturing firms represent 28% of adoption, while industrial machinery and packaging sectors collectively account for the remaining 30%. The fastest-growing end-user segment is logistics and material handling facilities, projected to expand adoption rapidly due to automated warehouses, conveyor systems, and robotic picking systems that leverage AI-integrated servo drives. Adoption rates in top-tier electronics manufacturing facilities exceed 60%, reflecting high investment in precision and productivity improvements. In 2024, more than 38% of enterprises globally reported piloting smart servo systems for real-time inventory and automated material handling platforms. Additionally, in the US, 42% of manufacturing facilities integrated servo-driven robotics with predictive maintenance, optimizing throughput and reducing downtime.

Asia-Pacific accounted for the largest market share at 38% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 6.0% between 2025 and 2032.

In 2024, Asia-Pacific led with over 590,000 units of industrial servo drives deployed across automotive, electronics, and robotics sectors. Europe followed with approximately 28% adoption, representing over 430,000 units, while North America captured 22% of global deployment. Japan alone produced 150,000 units, with China and India contributing 210,000 and 95,000 units, respectively. Technological adoption is concentrated in AI-driven servo systems, predictive maintenance, and integrated servo modules, with automation lines in Asia-Pacific factories achieving efficiency gains of 18–25%. North America is increasingly investing in smart manufacturing and digital transformation initiatives, positioning it for rapid market expansion.

North America holds approximately 22% of the global Industrial Servo Drives Market, driven by high adoption in automotive, aerospace, and electronics manufacturing sectors. Regulatory incentives for energy efficiency and Industry 4.0 adoption are promoting deployment of AI-integrated servo drives. U.S.-based manufacturers such as Rockwell Automation are upgrading existing production lines with smart servo systems to improve precision and reduce operational downtime by 15%. Regional enterprises demonstrate higher adoption in healthcare automation and financial robotics, reflecting broader enterprise readiness. Advanced digital trends, including predictive maintenance and IIoT integration, are accelerating the replacement of legacy systems with energy-efficient, high-performance servo drives.

Europe represents approximately 28% of the Industrial Servo Drives Market in 2024, with Germany, France, and the UK as leading adopters. Sustainability initiatives, including ISO 50001 energy standards and EU energy efficiency directives, are driving demand for eco-friendly, explainable servo systems. Emerging technologies such as AI-enabled torque optimization and predictive diagnostics are widely deployed in automotive and metalworking sectors. Siemens, a prominent European player, has implemented cloud-connected servo drives across multiple industrial facilities, improving process visibility and reducing downtime by 12%. Regulatory pressures also encourage enterprises to adopt traceable and energy-efficient systems to comply with environmental mandates.

Asia-Pacific leads the Industrial Servo Drives Market, accounting for 38% of global volume in 2024. Japan, China, and India are top-consuming countries, with production hubs in Nagoya, Shanghai, and Bengaluru driving industrial automation. Manufacturing trends include high-precision robotics, AI-integrated production lines, and modular factory systems. Local players like Yaskawa Electric are innovating with high-torque compact drives and predictive maintenance solutions. Regional consumer behavior is characterized by early adoption of automated warehouses, smart robotics, and e-commerce-driven manufacturing technologies. Over 70% of assembly lines in Japan have integrated advanced servo systems, demonstrating strong operational efficiency and precision-driven industrial practices.

South America represents 7% of the Industrial Servo Drives Market, with Brazil and Argentina as leading contributors. Infrastructure development in industrial parks, energy, and logistics sectors is fueling demand for high-precision motion control. Government incentives supporting local manufacturing and trade agreements encourage deployment of modern servo systems. Brazilian manufacturers are implementing automated assembly and packaging lines, increasing throughput by 14%. Regional consumer behavior shows preference for flexible, modular drives for small and medium-scale production, with adoption tied to local industrial modernization initiatives and energy optimization programs.

Middle East & Africa account for approximately 5% of the Industrial Servo Drives Market in 2024, led by the UAE and South Africa. Regional demand is concentrated in oil & gas, construction automation, and large-scale infrastructure projects. Technological modernization includes integration of digital twin and AI-enabled servo systems to improve operational efficiency. Local manufacturers and system integrators are retrofitting older plants with predictive maintenance-enabled servo drives, achieving up to 12% reduction in downtime. Enterprises in this region favor energy-efficient, reliable systems due to high operational costs and compliance with local trade and energy regulations.

Japan – 18% Market Share: High production capacity and strong automation adoption across automotive and electronics industries.

Germany – 15% Market Share: Sdvanced manufacturing infrastructure and regulatory push for energy-efficient servo systems.

The competitive environment in the Industrial Servo Drives Market is robust with more than 15 active global competitors, indicating a moderately fragmented but increasingly consolidated market. The top 5 companies (such as Yaskawa, Siemens, Mitsubishi Electric, ABB, and Rockwell Automation) collectively command approximately 45–55% of the market, reflecting both their scale and specialized domain strengths. These leaders are aggressively investing in innovation: for example, Yaskawa is expanding its Σ‑X servo drive family with machine‑learning tuning capabilities, while Mitsubishi is enhancing its MR‑J5 series for predictive maintenance. Strategic partnerships and mergers are common — Schneider Electric has recently strengthened its motion control portfolio via acquisition, and Rockwell Automation has launched distributed servo drives with modular architectures. Innovation trends focus on AI-enabled diagnostics, edge-based data feedback, embedded safety, and compact functional designs. Companies are also pursuing digital transformation: many are embedding IIoT connectivity and remote-monitoring capabilities right into drive hardware. This dynamic competitive landscape is driven by a mix of legacy automation giants and technology-focused challengers, all vying for leadership in precision motion control, energy efficiency, and smart manufacturing.

ABB Ltd.

Rockwell Automation

Schneider Electric SE

Bosch Rexroth AG

FANUC Corporation

The Industrial Servo Drives Market is being shaped by a number of transformative technologies that are redefining performance, efficiency, and connectivity. One of the most significant is AI-enabled motion control, where embedded machine-learning algorithms evaluate encoder and current‑feedback data in real time to optimize torque, reduce vibration, and predict maintenance needs. This leads to significantly lower unplanned downtime and improved system reliability.

Another major trend is IIoT integration, with modern servo drives supporting edge‑computing and secure, cloud-based connectivity. These drives continuously stream operational data to central dashboards, enabling remote diagnostics, trend analysis, and firmware updates. This connectivity also supports digital twin models: manufacturers can simulate and optimize machine behavior before physical deployment, reducing commissioning time. Functional safety is also gaining prominence, particularly in collaborative robotics and automated assembly lines. Servo drives with built-in SIL (Safety Integrity Level) compliance are now commonplace, allowing safe torque off (STO) and fail-safe braking without external safety modules. This reduces system complexity and enhances safety. Compact, high‑power density designs are driving adoption in space-constrained applications. Manufacturers are producing servo amplifiers that deliver high output power while reducing heat dissipation by up to 30%, thereby saving energy and minimizing cooling infrastructure.

Finally, regenerative drive technology is emerging as a key innovation for sustainable operations. These drives can recover kinetic energy during deceleration phases, converting it back into usable electrical energy rather than dissipating it as heat. This not only reduces energy bills but also helps plants meet ESG targets. Together, these technologies—AI motion control, IIoT/edge connectivity, digital twin, safety‑integrated servo designs, and regenerative drives—are making industrial servo systems smarter, safer, more compact, and more sustainable. For decision‑makers, investing in these next-gen servo platforms can deliver measurable improvements in productivity, lifecycle costs, and operational reliability.

In November 2024, Yaskawa launched the next evolution of its high‑speed Sigma‑X servo systems and the new iCube Control automation platform at SPS 2024, offering richer machine data (temperature, load, power reserves) to improve availability and reduce time to market. Source: www.yaskawa.eu.com

In March 2025, Yaskawa expanded its Σ‑X servo drive family by introducing 400 V input servo motors and SERVOPACK amplifiers, enabling these high-performance drives to be used in large industrial equipment without requiring step-down transformers. Source: www.yaskawa-global.com

In April 2024, Mitsubishi Electric added Fail Safe over EtherCAT (FSoE) support to its MR‑J5 servo amplifier series, enhancing safety communications and interoperability with EtherCAT masters under IEC 61508 / IEC 61784-3 standards. Source: www.in.mitsubishielectric.com

In August 2023, Rockwell Automation introduced a distributed version of its Kinetix 5700 servo drive, enabling modular, scalable motion architectures with reduced wiring complexity and better energy efficiency. Source: www.rockwellautomation.com

This report covers a comprehensive landscape of the Industrial Servo Drives Market, analyzing it across product types, application domains, end‑user verticals, and geographic regions. On the product side, it examines AC servo drives, DC servo drives, integrated and modular drives, and regenerative / high‑density variants. Application segments include factory automation, robotics, CNC machining, packaging, material handling, and more. For end‑users, the report details adoption across automotive, electronics, industrial machinery, aerospace, and logistics sectors.

Geographically, the analysis spans North America, Europe, Asia‑Pacific, Latin America, and Middle East & Africa — highlighting regional demand trends, production capacities, and technology adoption patterns. Technology focus areas include AI-enabled predictive maintenance, IIoT & digital twin integration, functional safety protocols, and regenerative energy recovery. The report also examines emerging opportunities such as small-scale robotic cells, smart factories, and energy‑efficient systems in green manufacturing.

In terms of competitive coverage, the report profiles all the major players globally — from traditional automation giants to challengers pushing next-gen servo innovations. It evaluates their strategic initiatives, product pipelines, and alliances. The market forecast also considers regulatory and ESG trends, exploring how energy efficiency and sustainability pressures are shaping servo drive design and deployment. Finally, the report identifies future growth engines, risk factors, and technology inflection points to help decision-makers understand where value and disruption lie in the servo drive industry.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 1,550.0 Million |

| Market Revenue (2032) | USD 2,470.5 Million |

| CAGR (2025–2032) | 6.0% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Yaskawa Electric Corporation, Siemens AG, Mitsubishi Electric Corporation, ABB Ltd., Rockwell Automation, Schneider Electric SE, Bosch Rexroth AG, FANUC Corporation |

| Customization & Pricing | Available on Request (10% Customization Free) |