Reports

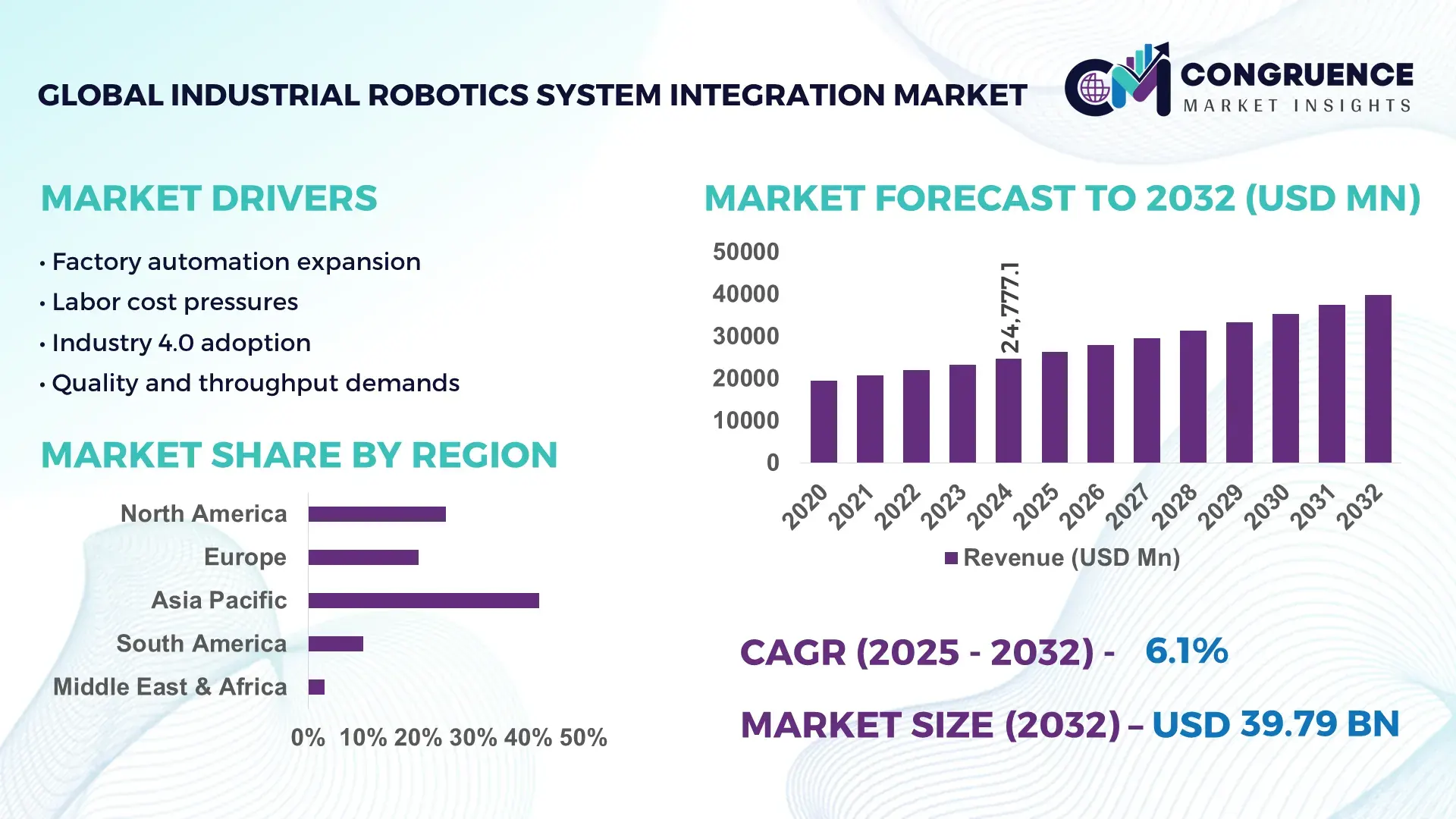

The Global Industrial Robotics System Integration Market was valued at USD 24777.11 Million in 2024 and is anticipated to reach a value of USD 39789.99 Million by 2032 expanding at a CAGR of 6.1% between 2025 and 2032. This growth is driven by accelerating automation adoption across smart manufacturing and Industry 4.0 initiatives.

Japan leads the Industrial Robotics System Integration market with robust production capacity exceeding 300,000 units annually and sustained capital investments surpassing USD 15 billion in automation infrastructure in 2024. The country’s integration of collaborative robots in automotive and electronics sectors has achieved productivity gains of up to 25% in precision assembly lines. Japan’s focus on advanced robotic vision systems and AI-based control platforms has resulted in the deployment of over 50,000 integrated robotic systems in high-mix, low-volume manufacturing environments.

Market Size & Growth: Valued at USD 24,777.11 Million in 2024, projected to reach USD 39,789.99 Million by 2032 at a 6.1% CAGR driven by enhanced automation efficiency and digital transformation across industries.

Top Growth Drivers: Industrial automation adoption improvement 42%, operational efficiency gains 35%, reduction in unplanned downtime 28%.

Short-Term Forecast: By 2028, robotic integration is expected to deliver a 30% reduction in cycle times across discrete manufacturing applications.

Emerging Technologies: AI-driven motion control, edge computing for real-time system analytics, collaborative robotics with adaptive sensing.

Regional Leaders: Asia Pacific ~USD 16B by 2032 with advanced automation adoption; North America ~USD 10B with smart factory upgrades; Europe ~USD 7B driven by precision manufacturing.

Consumer/End-User Trends: Automotive OEMs focusing on automated assembly lines, electronics contract manufacturers increasing robotics deployment for micro-precision tasks.

Pilot or Case Example: In 2025, a major electronics manufacturer’s pilot reduced rework rates by 22% and increased throughput 18% through integrated vision-guided robotics.

Competitive Landscape: Market leader approx. 32% share; key competitors include Fanuc, ABB, KUKA, Yaskawa, and Mitsubishi Electric.

Regulatory & ESG Impact: Industry safety standards and energy efficiency mandates accelerating adoption of compliant, low-energy robotic systems.

Investment & Funding Patterns: Over USD 4.2 billion in recent investments targeting mid-sized system integrators and AI-enabled automation ventures.

Innovation & Future Outlook: Growing integration of digital twin technologies, predictive maintenance platforms, and cross-industry robotics ecosystems shaping future deployments.

Industrial Robotics System Integration continues to transform key sectors including automotive, electronics, pharmaceuticals, and food & beverage, where automated inspection, precise material handling, and adaptive control systems are critical. Recent innovations in AI-assisted path planning and sensor fusion have improved uptime and reduced operational costs. Regulatory emphasis on workplace safety and energy efficiency supports broader deployment, while demand in emerging markets and integration with IoT platforms indicates continued expansion and technological advancement through 2032.

The strategic relevance of the Industrial Robotics System Integration Market lies in its central role in enabling automated, resilient, and compliant manufacturing ecosystems. Industrial robotics system integration accelerates production throughput while enhancing precision, quality, and operational efficiency. As manufacturers strive to balance flexibility with high productivity, the deployment of AI‑enabled motion control delivers 28% improvement compared to traditional rule‑based robotic coordination in adaptive assembly environments. Regionally, Asia Pacific dominates in volume, while North America leads in adoption with over 62% of enterprises deploying advanced robotics system integration solutions in smart factories. Over the short term, by 2027, edge AI analytics is expected to improve asset utilization by 35% through real‑time performance optimization across heterogeneous equipment. ESG compliance also significantly shapes investment strategies, with global firms committing to 15–20% reductions in energy intensity and waste generation by 2028 through integrated robotic process controls and predictive maintenance protocols. In a micro‑scenario, in 2025, a leading electronics manufacturer achieved a 22% reduction in rework and a 19% increase in throughput through cloud‑native robotics orchestration platforms. Looking forward, the Industrial Robotics System Integration Market will serve as a pillar of operational resilience, regulatory compliance, and sustainable growth, underpinning future‑ready industrial transformations worldwide.

The demand for smart manufacturing and precision assembly is a major driver of the Industrial Robotics System Integration Market, as industries such as automotive electronics, semiconductors, and medical devices seek automated solutions to achieve high consistency and low defect rates. Automotive manufacturers deploy integrated robotic welding, painting, and inspection cells to standardize output across global plants, responding to consumer expectations for quality and customization. In semiconductor fabrication, robotics system integration enables sub‑micron level handling and contamination‑free environments, supporting wafer throughput improvements critical for advanced node production. Precision assembly applications in electronics have elevated the importance of integrated vision systems and force‑feedback robotics, which can detect and correct anomalies in real time, reducing scrap rates by double digits. Smart manufacturing strategies also incorporate robotics integration with MES and ERP suites to enhance production visibility, reduce cycle times, and optimize workforce allocation. Together, these use cases underscore how system integration enhances operational performance and flexibility in complex, high‑mix manufacturing environments.

High upfront integration costs and a persistent skills gap act as restraints on the Industrial Robotics System Integration Market. Advanced robotics system integration involves substantial capital expenditure for equipment, software, and infrastructure reconfiguration, which can deter small and medium‑sized enterprises with constrained budgets. Procurement costs for high‑precision sensors, safety‑certified controllers, and interoperable communication modules remain significant, creating a barrier to entry for lower‑margin operations. Additionally, the availability of skilled automation engineers and systems integrators lags behind demand, with many regions reporting a shortage of professionals certified in robotics programming, OT/IT convergence, and industrial networking. This skills scarcity can delay project deployments, increase commissioning times, and inflate operational costs due to reliance on external consultants. Furthermore, integration complexity increases with heterogeneous legacy equipment, requiring custom interfaces and extensive validation cycles that extend time‑to‑value and elevate risk profiles for automation initiatives.

Digital twin technology and predictive analytics present significant opportunities for the Industrial Robotics System Integration Market by enabling real‑time simulation, performance forecasting, and proactive maintenance. Digital twins replicate physical systems in virtual environments, allowing engineers to evaluate integration strategies, identify bottlenecks, and optimize workflows before hardware deployment, reducing commissioning time and minimizing disruptions. Predictive analytics leverages sensor data from integrated robotic cells to forecast component wear, avoid unplanned downtime, and schedule maintenance with precision. These capabilities empower manufacturers to transition from reactive to proactive operations, enhancing uptime and equipment lifespan. In complex assembly lines, digital twin models can simulate variations in part tolerances and sequencing, enabling rapid reconfiguration and reducing changeover times. Furthermore, advancements in cloud‑native analytics and edge computing create scalable, cost‑effective platforms that democratize access to these tools for midsize enterprises. This convergence of digital technologies with robotics system integration elevates operational intelligence and unlocks incremental value across the production lifecycle.

Interoperability and cybersecurity concerns present material challenges for the Industrial Robotics System Integration Market, as manufacturing environments increasingly rely on interconnected hardware and software ecosystems. Robotics integration often involves linking components from multiple vendors, legacy PLCs, vision systems, and enterprise software, which can result in compatibility issues and data silos. Lack of standardized protocols and inconsistent implementation of industrial communication stacks can complicate integration efforts, driving up engineering hours and delaying deployments. Cybersecurity vulnerabilities emerge when integrated systems are exposed to networks without adequate segmentation, encryption, or threat detection measures. Sophisticated attacks targeting industrial control systems can disrupt production, compromise sensitive data, and impose regulatory liabilities. Protecting integrated robotics environments demands specialized security frameworks, continuous monitoring tools, and regular patch management, all of which require investment and expertise that some manufacturers may lack. These interoperability and cybersecurity hurdles complicate the path to fully realizing the strategic benefits of robotics system integration in modern industrial settings.

• Expansion of Collaborative Robotics in Manufacturing: The integration of collaborative robots (cobots) is accelerating across automotive and electronics production lines. In 2024, over 38,000 cobots were deployed globally, with adoption rising by 27% in North American smart factories. These systems allow humans and robots to share workspaces safely, increasing assembly line efficiency by up to 22% while reducing ergonomic-related injuries.

• AI-Driven Predictive Maintenance: Manufacturers are increasingly employing AI-powered predictive maintenance within integrated robotics systems. Real-time sensor analytics have enabled up to a 30% reduction in unplanned downtime and a 25% extension of equipment life in high-volume automotive plants. Predictive algorithms detect anomalies early, allowing corrective actions without interrupting production cycles, thereby optimizing overall operational performance.

• Integration of Digital Twin Technology: Digital twins are transforming process planning and system optimization in industrial robotics. Approximately 42% of large-scale electronics manufacturers now utilize digital twin models to simulate complex assembly processes, reducing testing time by 18% and ensuring faster deployment of new lines. This trend enhances production accuracy while minimizing waste and rework in high-precision industries.

• Adoption of Modular and Prefabricated Robotics Systems: Modular and prefabricated robotic solutions are gaining momentum, particularly in Europe and North America. Around 55% of recent industrial integration projects reported measurable cost savings by using pre-assembled robotic modules. These solutions reduce installation times by 35% and allow flexible scaling of production lines, supporting rapid adaptation to changing manufacturing demands and minimizing reliance on skilled labor for on-site assembly.

The Industrial Robotics System Integration market is segmented across types, applications, and end-users to reflect the diverse use cases and technological variations in automated environments. By type, segmentation covers hardware elements such as industrial robotic arms, controllers, sensors, and end-effectors; software modules for programming, simulation, and control; and integration services from design through maintenance. Each type aligns with different technical requirements and deployment strategies. For application segmentation, critical areas include assembly, material handling, inspection and testing, and packaging, each with distinct performance benchmarks and operational needs. End-user segmentation highlights how manufacturing, logistics, electronics, food & beverage, and pharmaceuticals leverage integrated robotics to optimize throughput, quality, and compliance. These segmentation layers collectively provide decision-makers with a structured view of where integration investments deliver specific operational value and how technology adoption varies by industry and task complexity. Robust segmentation helps align system capabilities with practical business goals and resource planning.

The type segment of the Industrial Robotics System Integration market includes hardware, software, and services. Hardware is the leading type, accounting for approximately 60% share of demand, driven by widespread deployment of industrial robotic arms, controllers, sensors, and end‑of‑arm tooling essential for core automation tasks such as material handling and welding. Hardware prominence is supported by installations exceeding 400,000 robotic arms globally that form the backbone of integrated systems. Software integration tools represent around 25% share, encompassing programming interfaces, simulation platforms, and real-time monitoring systems that enhance flexibility and adaptive control. Despite its smaller share, software is critical for enabling advanced functionalities such as AI‑based path planning and vision system coordination. Services, including design, consulting, commissioning, and maintenance, constitute the remaining 15% share, supporting long-term uptime and operational optimization. Adoption of modular simulation software has grown by 18%, allowing virtual testing of workflows prior to physical implementation, which reduces deployment risk and accelerates go‑live timelines.

Application segmentation in Industrial Robotics System Integration encompasses automotive, electrical and electronics, metal industry, chemical/plastics, food/beverage/pharma, and more. The automotive segment leads with a 38% share, as robotics system integration is core to welding, painting, assembly, and precise quality inspection tasks that require high repeatability and uptime; over 120,000 robots were installed in automotive facilities in 2024 to support these integrated workflows. The electrical and electronics sector holds a significant portion, with about 23% share, driven by PCB handling, micro-assembly, and device testing processes requiring high-precision integration. Food, beverage, and pharmaceuticals account for notable integration activity too, with 75,000 robots deployed to improve packaging speed by up to 40% through coordinated vision-guided pick-and-place systems. Other applications such as metals and chemical industries contribute meaningful shares, focused on hazardous material handling and robust automated processing.

End‑user segmentation in the Industrial Robotics System Integration market reveals that manufacturing is the predominant user, representing over 55% share, because discrete and process manufacturers rely heavily on integrated robotic solutions to boost quality, consistency, and throughput across high-volume production lines. Within manufacturing, automotive OEMs and electronics manufacturers are the most active, leveraging robotics for assembly, inspection, and material handling. Logistics and warehousing end-users contribute around 30% share, driven by e-commerce growth and the need for automated storage, retrieval, and inventory handling solutions that integrate robotics with warehouse management systems. Emerging end-users include healthcare and retail, where robotics integration improves laboratory automation, material transport, and supply chain responsiveness. Collectively, these segments illustrate how integration delivers differentiated operational value across diverse sectors while highlighting sectors with high automation uptake and evolving use cases.

Asia Pacific accounted for the largest market share at 42% in 2024, however, North America is expected to register the fastest growth, expanding at a CAGR of 6.5% between 2025 and 2032.

Asia Pacific’s dominance is fueled by high-volume manufacturing in China, Japan, and South Korea, with over 350,000 industrial robotic units deployed in system integration projects in 2024. North America follows closely with 28% market share, driven by automotive, electronics, and healthcare sectors. Europe holds 18% market share, led by Germany and France. South America and Middle East & Africa contribute 7% and 5%, respectively, supported by emerging industrial investments and infrastructure modernization. Across regions, adoption of AI-enabled control, vision-guided robotics, and modular integration solutions is reshaping production efficiency, reducing cycle times by up to 25%, and supporting sustainable manufacturing initiatives.

How are enterprises accelerating automated integration in production lines?

North America accounts for 28% of the Industrial Robotics System Integration market, with significant activity in the automotive, healthcare, and electronics sectors. Regulatory initiatives and government incentives for Industry 4.0 adoption are driving investments in smart factory upgrades. Technological advancements such as AI-driven predictive maintenance, cloud-based orchestration platforms, and collaborative robotics are transforming operational efficiency. Local players like Rockwell Automation are expanding digital twin and robotics integration solutions to streamline assembly and inspection workflows. Enterprise adoption patterns show higher deployment in healthcare logistics and finance-related robotic process automation, enhancing throughput and compliance monitoring. Investment in modular and prefabricated robotic solutions reduces installation time by up to 30% in high-volume plants, reflecting strong consumer preference for scalable, flexible integration.

What factors are shaping industrial automation adoption across European facilities?

Europe represents 18% of the Industrial Robotics System Integration market, with Germany, the UK, and France being key contributors. Sustainability mandates and regulatory pressures encourage the use of explainable robotics systems and energy-efficient automation. Advanced AI-driven control platforms and vision systems are increasingly integrated into high-precision industries such as automotive and electronics. Local players, including KUKA AG, are enhancing modular robotics solutions and predictive maintenance software for factories. Regional consumer behavior emphasizes compliance and energy reduction, driving demand for integrated systems that balance performance with regulatory adherence. Approximately 65% of industrial plants in Germany have adopted AI-assisted robotic integration tools to optimize production processes and reduce operational waste.

Why is automated system integration rapidly expanding across Asia-Pacific manufacturers?

Asia-Pacific holds the largest market volume at 42%, driven primarily by China, Japan, and India. Industrial sectors are rapidly upgrading manufacturing lines with robotics integration, focusing on automotive, electronics, and consumer goods. Infrastructure investments, combined with smart factory initiatives, support high-volume deployment of vision-guided and AI-enhanced robotic systems. Regional innovation hubs in Japan and South Korea advance collaborative robotics and cloud-based system integration, enhancing productivity by up to 25%. Local players such as Fanuc Corporation are deploying over 50,000 integrated robotic cells annually across automotive and electronics facilities. Consumer behavior trends favor high-speed, precision-enabled automation, supporting continuous adoption in e-commerce fulfillment centers and high-tech assembly lines.

How are industrial robotics integrations evolving across Latin American markets?

South America represents approximately 7% of the Industrial Robotics System Integration market, with Brazil and Argentina leading adoption. Infrastructure modernization and energy sector investments are increasing demand for automated material handling and assembly solutions. Government incentives promoting industrial automation, coupled with regional trade partnerships, encourage deployment of robotics system integration projects. Local players are implementing robotics solutions to optimize assembly lines and warehouse logistics. Consumer behavior is influenced by media-driven awareness and language localization requirements, prompting manufacturers to integrate adaptive robotics capable of handling multiple operational scenarios. Over 15,000 industrial robotic units were deployed across key manufacturing hubs in 2024 to enhance efficiency.

What is driving robotics adoption in emerging industrial hubs?

Middle East & Africa contributes 5% to the Industrial Robotics System Integration market, led by the UAE and South Africa. Oil & gas, construction, and high-tech manufacturing sectors are primary drivers of integrated robotics adoption. Technological modernization, including IoT-connected robotic systems and AI-based monitoring, is accelerating deployment. Local regulations incentivize energy-efficient automation and compliance with safety standards. Companies such as regional automation integrators are introducing modular robotic platforms to support flexible manufacturing and reduce operational downtime. Consumer behavior trends prioritize solutions that improve labor efficiency and operational resilience while addressing sustainability objectives in high-demand industrial sectors.

Japan – 21% market share; strong production capacity and advanced integration of collaborative robotics in automotive and electronics industries.

China – 18% market share; extensive end-user demand across high-volume manufacturing and investment in AI-driven system integration solutions.

The Industrial Robotics System Integration market exhibits a moderately consolidated competitive structure, with over 120 active global competitors offering diverse hardware, software, and system integration solutions. The top five players—including Fanuc, ABB, KUKA, Yaskawa, and Mitsubishi Electric—collectively account for approximately 62% of total market share, reflecting strong influence over technology standards, production capacity, and strategic investments. Competitive dynamics are shaped by continuous innovation in AI-driven robotics control, collaborative robotics, and digital twin-enabled integration platforms. Key strategic initiatives in 2024–2025 include cross-industry partnerships, multi-region product launches, and acquisitions aimed at enhancing automation capabilities and expanding regional footprints. For instance, several leading integrators have deployed cloud-based orchestration platforms and modular robotics kits, improving deployment speed by 25% in complex manufacturing lines. The market remains attractive for both established firms and emerging players, with smaller specialized integrators capturing niche demand for high-precision applications, predictive maintenance solutions, and sustainable automation systems. Regional competition is pronounced, with Asia-Pacific maintaining volume dominance, North America leading adoption in healthcare and electronics, and Europe prioritizing compliance-focused, energy-efficient system integration. The ongoing innovation race is further accelerating robotics adoption and differentiation across sectors.

Yaskawa Electric Corporation

Mitsubishi Electric Corporation

Rockwell Automation

Omron Corporation

Bosch Rexroth

Denso Corporation

Comau S.p.A

The Industrial Robotics System Integration market is being profoundly shaped by both current and emerging technologies, driving efficiency, precision, and operational flexibility across multiple sectors. Collaborative robotics (cobots) are increasingly deployed, with over 38,000 units integrated into North American and European production lines in 2024, enabling safe human-robot interaction and reducing ergonomic-related injuries by up to 22%. AI-driven motion control and predictive maintenance are enabling real-time monitoring of robotic systems, allowing manufacturers to cut unplanned downtime by 30% and extend equipment lifespan by 25%. Vision-guided robotics are widely adopted in high-precision assembly and inspection, with over 75,000 units deployed in electronics, automotive, and pharmaceutical manufacturing, improving defect detection rates by up to 18%.

Emerging technologies such as digital twin platforms are gaining traction, enabling virtual simulation of integrated robotic systems prior to physical deployment, which reduces commissioning time by 20% and allows rapid scenario testing. Edge computing and IoT-enabled integration allow for decentralized processing and data-driven decision-making, enhancing throughput optimization across heterogeneous equipment. Modular robotic architectures and prefabricated system units are also expanding, with 55% of new integration projects in Europe and North America leveraging pre-assembled modules to reduce installation time by 35%.

Additionally, AI-powered vision-language interfaces and cloud-based orchestration platforms are improving operational transparency and multi-line coordination, allowing real-time adjustments across production floors. In smart factory environments, integrated sensor fusion, adaptive control algorithms, and collaborative AI enable simultaneous handling of complex assembly tasks, reducing cycle times by up to 25% and improving overall production quality. These technology trends are positioning Industrial Robotics System Integration as a strategic enabler of sustainable, high-efficiency manufacturing.

• In March 2024, ABB introduced the IRB 1300 industrial robot, designed for precision assembly and material handling in confined and high‑speed electronics production environments, enabling integration with advanced vision systems that improve cycle efficiency by approximately 15% and boost process reliability in dense production layouts.

• In April 2024, FANUC America launched the enhanced ROBOGUIDE V10 simulation and offline programming software, offering improved performance and user experience that significantly accelerates programming workflows and reduces commissioning times for integrated robotics systems across automotive and logistics applications. (fanucamerica)

• In December 2023, Yaskawa Electric rolled out the MOTOMAN NEXT autonomous robot series, featuring adaptive control and open‑platform automation capabilities for unstructured environments, aimed at expanding automation into previously hard‑to‑automate tasks in food, logistics, and general manufacturing. (yaskawa-global.com)

• In July 2024, FANUC opened its 650,000‑square‑foot West Campus in Michigan, reinforcing North American manufacturing and automation capacity with advanced production, specialized automation systems, and a 6,000‑robot parts and inventory hub to better support system integration and deployment capabilities.

The Industrial Robotics System Integration Market Report encompasses a comprehensive analysis of technological, functional, and regional aspects of robotic automation solutions integrated into industrial operations. The report delineates a wide spectrum of product types including industrial robotic arms, collaborative robots, controllers, vision systems, end‑of‑arm tooling, and integration software platforms that enable programming, simulation, monitoring, and IoT connectivity. Segmentation by application covers assembly, material handling, inspection & testing, packaging, and logistics automation, offering insights into use‑case‑specific performance metrics such as precision requirements, cycle time improvements, and safety benchmarks. End‑user segments span automotive, electronics, food & beverage, pharmaceuticals, chemicals, and logistics, with emphasis on how integration drives operational flexibility, quality consistency, and workforce augmentation.

Geographically, the report evaluates demand patterns across Asia Pacific, North America, Europe, South America, and Middle East & Africa, highlighting consumption volumes, industrial transformation initiatives, and regional adoption trends. It also examines emerging technologies such as AI‑enabled motion control, digital twin platforms, edge computing for real‑time analytics, and modular prefabricated integration units that reduce installation time and operational risk. Additionally, the report explores innovation themes including autonomous robotic platforms, vision‑guided systems, and cloud‑native orchestration for multi‑line synchronization. Strategic considerations, such as integration with enterprise systems, regulatory compliance, and workforce skill enhancement, further contextualize the deployment landscape for decision‑makers seeking optimized automation investments.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 24777.11 Million |

Market Revenue in 2032 | USD 39789.99 Million |

CAGR (2025 - 2032) | 6.1% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Fanuc Corporation, ABB Ltd, KUKA AG, Yaskawa Electric Corporation, Mitsubishi Electric Corporation, Rockwell Automation, Omron Corporation, Bosch Rexroth, Denso Corporation, Comau S.p.A |

Customization & Pricing | Available on Request (10% Customization is Free) |