Reports

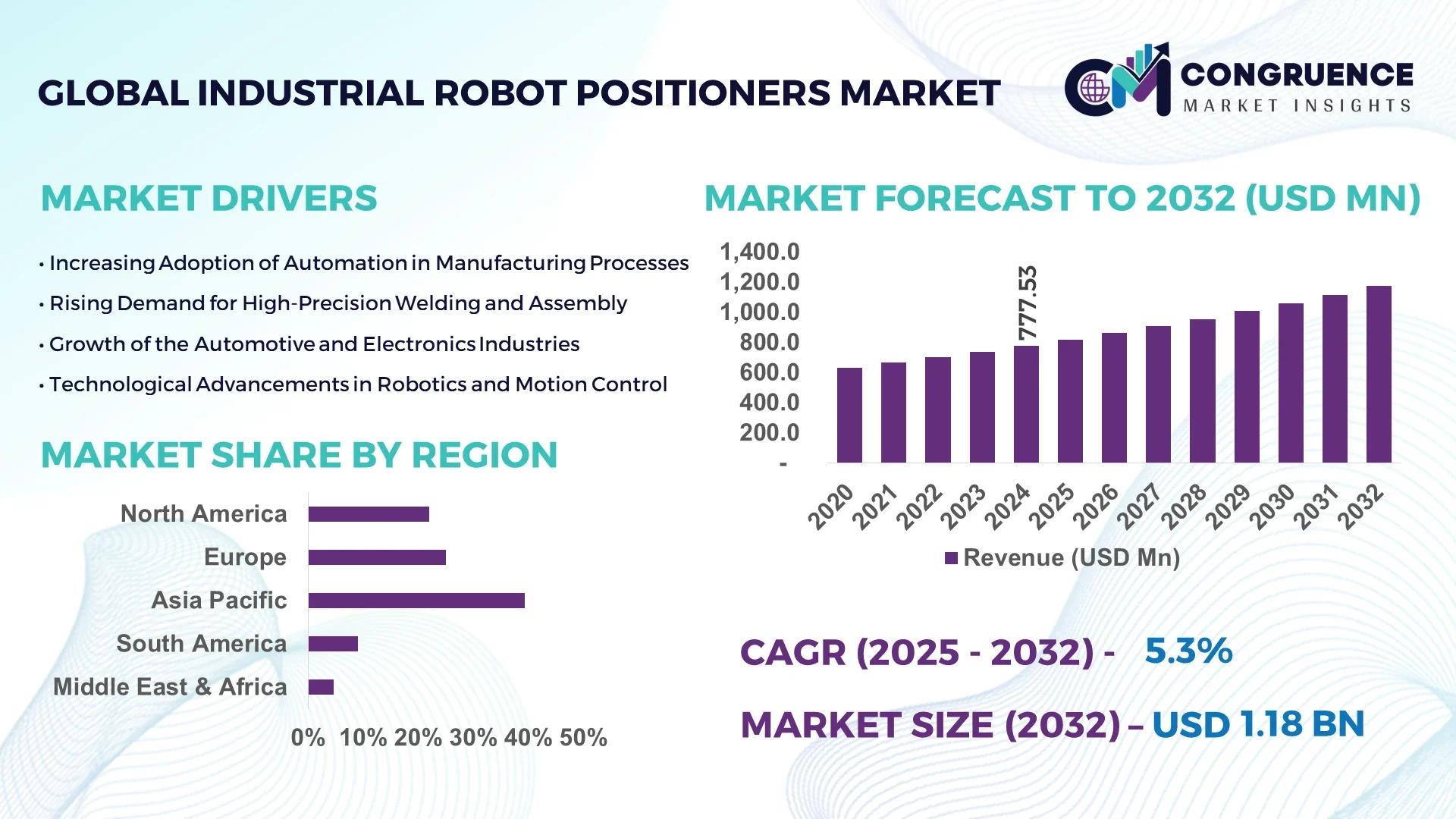

The Global Industrial Robot Positioners Market was valued at USD 777.53 Million in 2024 and is anticipated to reach a value of USD 1175.29 Million by 2032 expanding at a CAGR of 5.3% between 2025 and 2032.

Industrial robot positioners are playing a crucial role in enhancing automation and precision across manufacturing sectors worldwide. These devices are designed to hold and rotate workpieces into exact positions, boosting welding, assembly, and material handling accuracy. The rising demand for robotic welding and the integration of robotic arms in high-speed production lines is driving their adoption in automotive, aerospace, and heavy machinery industries. Industrial robot positioners are key to increasing productivity while ensuring consistent product quality and minimizing human error. The global focus on smart factories and Industry 4.0 is encouraging manufacturers to deploy multi-axis robotic systems, which is further propelling the market forward. Additionally, increased labor shortages and high labor costs are prompting businesses to adopt robotic systems for efficiency and scalability. The combination of robotic arms with positioners ensures seamless, high-precision movement, ultimately optimizing workflow. With significant advancements in sensor technologies and AI integration, industrial robot positioners are becoming smarter, more compact, and highly energy efficient—catering to a broad spectrum of industries across the global automation landscape.

Artificial Intelligence (AI) is significantly transforming the industrial robot positioners market by enabling greater precision, flexibility, and automation intelligence across production floors. AI-driven robot positioners are now capable of learning from past operations, adjusting movement patterns autonomously, and making real-time positioning decisions with minimal human intervention. These systems are being adopted for complex processes such as arc welding, laser cutting, and robotic polishing—where even slight deviations can affect performance. AI integration also enhances vision systems, enabling robots to detect flaws or variations in components and make immediate adjustments. This is especially valuable in industries like electronics and aerospace, where microscopic precision is mandatory.

Moreover, AI enhances predictive maintenance capabilities in industrial robot positioners. Through constant monitoring of performance data, AI algorithms predict potential failures and schedule maintenance proactively, significantly reducing downtime. AI also assists in energy consumption optimization, ensuring operational efficiency without compromising output quality. As AI-based analytics and edge computing evolve, robot positioners can respond faster to production changes, improving agility in lean manufacturing environments. The rise of AI-powered collaborative robots that use advanced positioners further enables shared workspace interactions, reducing the need for physical barriers and increasing flexibility in small-to-medium production units. This dynamic synergy between AI and robot positioners is redefining next-gen industrial automation strategies.

"In May 2024, Universal Robots launched the UR20 and UR30 collaborative robots at Automate 2024, featuring expanded reach and payloads tailored for integration with AI systems in welding and packaging tasks, offering superior automation flexibility."

The dynamics of the industrial robot positioners market are shaped by evolving technological innovations, rising automation demands, and the shift toward smart manufacturing ecosystems. Industrial robot positioners are central components in robotic systems used for welding, assembly, and precise material positioning across automotive, aerospace, electronics, and heavy engineering industries. Manufacturers are focusing on increasing speed, accuracy, and flexibility, driving investment in advanced multi-axis robot positioners and collaborative robot integrations. Additionally, real-time data monitoring and adaptive motion control technologies are influencing system upgrades, contributing to dynamic changes in buyer preferences and procurement strategies. While automation maturity in North America and Europe is stabilizing, emerging economies in Asia-Pacific are experiencing rapid market expansion due to government-led industrial digitization programs and rising manufacturing output. The push for cost reduction, energy efficiency, and improved safety standards are compelling enterprises to re-evaluate their automation infrastructure—positioners being a key component. Despite these strong drivers, cost-related restraints and technical challenges still pose barriers to full-scale adoption.

Increasing Adoption in the Automotive Sector

One of the strongest drivers for the industrial robot positioners market is the growing demand from the automotive industry. Automotive manufacturers extensively utilize robotic welding systems, where precision and repeatability are critical. Two-axis and multi-axis positioners are used to rotate large vehicle frames and components during welding, allowing robots to access difficult angles with ease. In 2024, over 55% of robotic positioner deployments were recorded in automotive and auto component manufacturing, driven by the rising demand for electric vehicles and lightweight vehicle components. Automotive OEMs are rapidly modernizing their facilities to improve production throughput, reduce human error, and maintain consistency in high-volume operations. The use of robot positioners enables seamless integration with robotic arms, minimizing cycle time and maximizing operational efficiency. Additionally, the automotive industry's push toward modular assembly lines and scalable robotic systems is boosting the sales of reprogrammable and flexible positioners. As more car manufacturers implement lean and smart manufacturing principles, robotic positioners will remain vital to enabling process automation and digital transformation.

High Installation and Maintenance Costs

Despite the growing popularity of industrial robot positioners, high capital expenditure remains a significant barrier for many small and medium-sized enterprises. The initial cost of setting up robotic workstations, including advanced positioners and controllers, can be prohibitive. Moreover, the cost of system integration, training, and customization often adds up, delaying the return on investment for many companies. Maintenance of industrial robot positioners also demands specialized technical expertise. If not maintained correctly, even slight misalignments in positioners can lead to quality defects or production halts. In regions with limited access to robotics service providers, downtime due to malfunctioning positioners can stretch significantly, disrupting operations. Many businesses are also concerned about the recurring costs associated with component replacement, software upgrades, and calibration tools. The fear of obsolescence in fast-evolving automation environments discourages some manufacturers from making upfront investments in robot positioner solutions. These financial and operational concerns are limiting adoption, especially in cost-sensitive markets.

Industry 4.0 and Smart Factory Integration

The ongoing transformation of traditional manufacturing into smart factories is creating lucrative opportunities for the industrial robot positioners market. With the rise of Industry 4.0, manufacturers are increasingly adopting connected systems and data-driven production environments. Industrial robot positioners are now equipped with sensors and IoT capabilities that allow real-time data sharing with cloud-based platforms, enabling seamless coordination between multiple robots and systems. This enhances operational visibility, predictive maintenance, and energy optimization. The demand for highly adaptable, programmable positioners that can work across different product lines is increasing in flexible production settings. Integration with digital twins and AI further improves cycle time analysis, fault detection, and dynamic reprogramming. As smart factory initiatives gain momentum in Asia-Pacific, Europe, and North America, investments in industrial robotics—including robot positioners—are expected to surge. Sectors like electronics, metal fabrication, and medical device manufacturing are exploring modular robot positioner units that offer scalability and quick deployment in automated cells. The ability to reconfigure production without major retooling is a major value proposition in modern smart factories.

Shortage of Skilled Workforce for Robotic Systems

One of the major challenges hampering the industrial robot positioners market is the shortage of skilled workforce capable of installing, programming, and maintaining advanced robotic systems. While automation demand is rising, the supply of technicians and engineers trained in multi-axis robotics, motion planning, and system calibration remains insufficient. As robot positioners become more complex with AI and machine vision integration, the knowledge gap is becoming more pronounced. Many manufacturers struggle to recruit talent capable of designing and troubleshooting automated systems, especially in developing economies where robotics training infrastructure is limited. Additionally, training programs often lag behind current technology trends, leaving even experienced staff underprepared for newer robotic platforms. This talent shortfall impacts deployment timelines, increases reliance on third-party integrators, and raises the total cost of ownership. Companies are now investing in upskilling programs and collaborating with technical institutions, but the pace of training does not yet match market demand. This ongoing workforce challenge is slowing the transition to fully automated operations in several industries.

The industrial robot positioners market is experiencing rapid evolution in 2024 due to advancements in multi-axis configurations, demand for compact and flexible designs, and deeper integration with smart factory ecosystems. One of the key trends is the increasing adoption of dual-axis and three-axis robot positioners to accommodate complex and precise movement requirements across automotive and heavy engineering sectors. These advanced positioners allow enhanced reach, load handling, and rotational freedom, making them ideal for robotic welding, painting, and laser cutting applications.

Another significant trend is the growth of collaborative robot (cobot) positioners. These are specifically designed for safer interaction with human operators and are being rapidly adopted in SMEs and flexible production environments. Manufacturers are now deploying mobile robot positioners that can be reprogrammed and relocated, offering unprecedented agility in production lines. Integration of positioners with AI, machine vision, and real-time feedback systems is driving smart positioning capabilities, allowing self-correction and adaptive alignment during operation.

Digital twin technology is also making waves in the industrial robot positioners market. Companies are simulating robot positioning scenarios before deployment, reducing trial-and-error in production. There is also a clear shift toward energy-efficient robot positioners with optimized motor performance and regenerative braking systems. These trends indicate a strong push toward intelligent, sustainable, and flexible automation in 2025 and beyond.

The industrial robot positioners market is segmented by type, application, and end-user, each playing a critical role in shaping overall demand trends. Among types, Two-Axis and Three-Axis positioners dominate due to their rotational flexibility and use in complex welding operations, while Single-Axis positioners remain vital for basic tasks requiring precision in one direction. On the application front, welding leads due to widespread automation in automotive and metal fabrication industries. Assembly and material handling also hold significant shares owing to increased demand in electronics and packaging. When segmented by end-user, the automotive industry leads the market, driven by high-volume production requirements, followed by the metal fabrication and aerospace sectors, where high precision and heavy-duty robotics are essential. Each segment reflects distinct growth dynamics and adoption patterns across different industrial verticals, demonstrating the market’s complexity and opportunities.

Two-Axis Positioners: Two-axis robot positioners are among the most demanded systems in industrial automation, especially in welding applications where rotation along two axes is required for full part coverage. These positioners are commonly used in automotive and heavy machinery plants due to their ability to tilt and rotate simultaneously. In 2024, two-axis positioners accounted for more than 40% of new installations in the welding automation sector. Their modularity, load-bearing capacity, and compatibility with robotic welding arms make them essential for flexible manufacturing. Industries deploying multi-robot cells also prefer two-axis models due to ease of synchronization and motion control. Manufacturers are investing in digital twin integration for two-axis systems to optimize design simulations and real-time adjustments.

Three-Axis Positioners: Three-axis positioners provide comprehensive movement across tilt, rotation, and swing, making them indispensable in complex fabrication tasks like turbine blade welding or aerospace part assembly. In 2024, three-axis systems saw increased adoption in aerospace, marine, and defense sectors where positional accuracy and multi-directional access are vital. Their ability to accommodate heavy and irregular components makes them ideal for large workpieces. Technological enhancements such as real-time feedback systems and programmable logic controllers (PLCs) are standard in modern three-axis models. These positioners also support multiple part clamping configurations, improving throughput in high-mix manufacturing setups. Growth is expected to continue with advanced variants offering servo-driven control and automated part orientation.

Single-Axis Positioners: Single-axis positioners remain popular in industries with simple yet repetitive operations such as part flipping, arc welding, and pick-and-place tasks. These positioners offer reliable rotational motion and are ideal for small-to-medium-sized components. In 2024, single-axis models were widely used in electronics and general fabrication plants, representing over 30% of global demand by volume. Cost-effective and space-efficient, these positioners are often selected by SMEs and job shops transitioning into robotic automation. Recent trends show integration with low-payload collaborative robots, making them a go-to solution for high-mix, low-volume production lines. Their simplicity allows for fast deployment and minimal programming, making them suitable for entry-level automation setups.

Welding: Welding remains the leading application for industrial robot positioners, accounting for over 45% of total installations in 2024. Positioners are critical for achieving high-quality, consistent welds, especially in applications requiring access to multiple angles and surfaces. Automotive and metal fabrication sectors are the largest users, where positioners reduce cycle times and improve joint strength. Two-axis and three-axis positioners dominate this segment, integrated with arc and spot welding robots. The adoption of robotic MIG and TIG welding systems with synchronized positioners is becoming increasingly common. Welding applications now also feature real-time seam tracking and adaptive path control, driving demand for smart positioner models.

Assembly: In robotic assembly lines, positioners enhance productivity by accurately rotating components for fastener insertion, part fitting, or glue application. Their role is especially significant in electronics, home appliances, and automotive dashboard assembly. In 2024, assembly-related robot positioner sales grew by 18% year-on-year, largely driven by the demand for precision and repeatability in complex assemblies. Positioners paired with machine vision systems enable robotic arms to align and secure small or delicate parts with high precision. Servo-driven single-axis models are common in these tasks due to their responsiveness. Assembly cells using programmable positioners also benefit from quick changeovers for different SKUs, essential in lean manufacturing.

Painting: Painting applications demand smooth and consistent part rotation, which is efficiently delivered by robotic positioners. In 2024, the adoption of robot positioners in painting booths rose significantly in the automotive aftermarket and aerospace coating sectors. These positioners are used to rotate components for uniform paint application, ensuring complete surface coverage and reducing overspray. Anti-static and corrosion-resistant positioner variants are popular in this segment. Painting positioners are often synchronized with robotic sprayers and enclosed in explosion-proof environments. The use of lightweight, high-speed single-axis units in painting lines helps improve cycle time and minimize downtime during color changes or part swaps.

Material Handling: Material handling applications such as loading/unloading, sorting, and transferring parts utilize robot positioners to orient and move items with precision. This is particularly important in packaging, warehouse automation, and logistics centers. In 2024, demand for positioners in this segment increased due to the rise in e-commerce and fast-moving consumer goods (FMCG). Dual-axis positioners are often used to reposition items for palletizing or further robotic processing. Their integration with conveyor belts and AGVs (automated guided vehicles) allows seamless operation in dynamic warehouse setups. High-speed response and load adaptability are critical features sought in material-handling positioners.

Inspection: Inspection processes rely on robot positioners to orient products for vision systems, laser scanners, or measurement probes. In 2024, this application saw growing relevance in semiconductor, aerospace, and precision engineering sectors where accuracy is paramount. Robot positioners enable 360-degree component visibility, allowing detailed quality control from all angles. Single-axis and rotary table positioners are popular in inspection lines. Some advanced systems feature automatic calibration and barcode scanning integration. As quality standards become more stringent, robot positioners in inspection setups are being designed with micron-level precision and compatibility with AI-based defect detection software.

Automotive Industry: The automotive industry remains the dominant end-user of industrial robot positioners, accounting for nearly 50% of the market share by unit volume in 2024. Automotive OEMs and Tier 1 suppliers use positioners extensively in welding, assembly, and coating operations. Multi-axis robot positioners enhance workflow efficiency, reduce production downtime, and ensure consistent output across vehicle variants. The shift toward electric vehicle (EV) manufacturing has led to greater demand for flexible positioners that can accommodate varied body frame sizes. Robotic positioners are integral to robotic welding cells used for chassis and drivetrain production, as well as painting lines for precision coating.

Electronics and Electrical Industry: In the electronics and electrical manufacturing sectors, robot positioners are used for tasks that require high accuracy and repeatability, such as PCB assembly, wire placement, and inspection. In 2024, adoption surged due to miniaturization of components and the need for fault-free production. These industries favor compact, high-speed single-axis positioners for cleanroom environments and micro-assembly lines. Integration with machine vision and real-time quality control systems enhances functionality. As demand for consumer electronics, smartphones, and EV battery modules increases, so does the reliance on robotic positioners for scaling production without compromising precision.

Metal and Machinery Fabrication: Metal and machinery fabrication industries use robot positioners for welding, cutting, and surface finishing of metal structures and machine components. These industries demand heavy-duty, high-load positioners capable of handling large parts like metal frames, tanks, and beams. In 2024, three-axis positioners saw strong growth in fabrication shops and shipyards. Customizable clamping systems, synchronized motion with industrial robots, and improved torque capacity are key features. The emphasis on structural integrity and reduced rework in welding applications is driving increased investment in intelligent robotic positioners equipped with adaptive feedback systems.

Aerospace & Defense: Aerospace and defense sectors rely on precision robotics for assembling aircraft components, turbine blades, and fuselage structures. Industrial robot positioners are critical in ensuring precise alignment, minimal variation, and repeatable accuracy in high-stakes manufacturing environments. In 2024, demand rose for three-axis positioners equipped with safety certifications and real-time diagnostics. Robotic systems in this industry must comply with strict quality control standards, and positioners are increasingly being integrated with data logging and AI-powered anomaly detection systems. Their use in composite part handling and advanced material inspections further supports demand in this highly regulated sector.

Other Industries: Other industries such as medical device manufacturing, construction equipment, white goods, and renewable energy sectors are emerging as important consumers of industrial robot positioners. These segments are leveraging automation to improve product uniformity and reduce manual intervention. For example, wind turbine manufacturing uses heavy-duty two-axis positioners to weld tower sections, while the medical sector relies on high-precision single-axis units for surgical tool fabrication. Growth in these sectors is supported by rising automation budgets and increasing complexity in production requirements, leading to a diverse range of applications for robot positioners in custom setups.

Asia-Pacific accounted for the largest market share at 39.4% in 2024, however, North America is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2025 and 2032.

The Asia-Pacific region's dominance is attributed to the massive adoption of industrial automation across China, Japan, South Korea, and India, driven by the automotive, electronics, and metalworking sectors. Rising investments in smart manufacturing and government-backed initiatives supporting Industry 4.0 have led to increased demand for robot positioners. North America’s rapid growth is fueled by a strong manufacturing base, high demand for advanced welding systems, and adoption of collaborative robotics. Europe remains a steady contributor due to stringent safety and efficiency standards, particularly in Germany, Italy, and France. The Middle East & Africa region is experiencing a surge in adoption due to infrastructure growth and new industrial projects, especially in the UAE and Saudi Arabia. Region-wise growth highlights the global diversification of the industrial robot positioners market, supported by automation-led productivity strategies and smart factory integration across continents.

Rising Automation Investments Driving U.S. Positioner Demand

In 2024, North America contributed to 27.6% of the global industrial robot positioners market, with the United States leading regional consumption. Growth in this region is largely driven by increased adoption of robotic welding systems across automotive and aerospace manufacturing hubs in Michigan, Texas, and California. Demand for two-axis and three-axis positioners surged due to their deployment in EV chassis fabrication, with over 2,000 units installed in automotive plants alone during the year. Canada and Mexico also saw growth, with positioners being integrated into assembly and inspection lines in the consumer electronics and appliance sectors. Smart factories, driven by AI and IoT adoption, are transforming production models, especially in defense and aerospace sectors. U.S. manufacturers are also shifting toward compact, mobile positioners to meet flexible, low-volume, high-variety production needs. Increased government support for reshoring manufacturing is another key driver boosting demand for robotic positioners.

Germany and Italy Spearheading Positioner Usage in Precision Engineering

Europe accounted for 23.8% of the global industrial robot positioners market in 2024, with Germany alone representing over 40% of regional demand. The strong industrial automation base, especially in automotive and precision engineering, drives the demand for high-accuracy robot positioners. Germany, Italy, and France have emerged as top consumers, particularly of three-axis positioners used in complex welding and assembly tasks. In 2024, more than 1,500 robot positioners were deployed across German automotive plants for body-in-white assembly and underbody welding. Meanwhile, the aerospace sector in France and the marine engineering segment in Italy heavily invested in servo-controlled positioners. European manufacturers also demand positioners with integrated safety systems to meet CE certification requirements. The rise in energy-efficient automation solutions and the emphasis on digital twin simulation tools are further strengthening the adoption of advanced robot positioners in the region.

China and Japan Leading Automation-Driven Positioner Expansion

The Asia-Pacific region dominated the global industrial robot positioners market with a 39.4% share in 2024. China and Japan are at the forefront, with massive deployments in automotive, electronics, and heavy machinery manufacturing. China alone installed over 3,500 new robot positioners in 2024, particularly in EV battery assembly and robotic welding lines. Japan continues to lead in compact, high-precision single-axis positioners tailored for electronics and semiconductor fabrication. South Korea’s positioner demand is being driven by the surge in smart manufacturing investments in electronics and shipbuilding. India is an emerging market, witnessing increased deployment of positioners in SME-driven welding and fabrication workshops. The region’s growth is supported by government automation schemes, lower manufacturing costs, and rising foreign investments in high-tech manufacturing zones. High-volume production facilities prefer multi-axis robot positioners to boost throughput and reduce error margins, contributing to the region’s technological leap in industrial automation.

Industrial Expansion in GCC Region Fueling Positioner Adoption

The Middle East & Africa region held a modest 9.2% share of the global industrial robot positioners market in 2024 but is quickly emerging as a growth hotspot. The UAE and Saudi Arabia are leading investments in industrial automation through national transformation plans like Vision 2030, resulting in growing adoption of robot positioners in sectors like construction equipment, automotive assembly, and energy infrastructure. In 2024, over 600 units were deployed across major Gulf-based manufacturing zones, with dual-axis positioners favored for welding applications in heavy steel fabrication. South Africa showed increased usage in mining equipment production, while Egypt and Nigeria are witnessing early adoption in small-scale assembly and materials handling lines. Companies in this region prefer durable and high-load capacity positioners to handle large parts in high-temperature environments. Expansion of logistics hubs and free economic zones is attracting industrial robot integrators, boosting market penetration of robotic positioners.

The industrial robot positioners market is highly competitive, featuring a wide range of global players offering advanced products to cater to diverse industrial needs. Key players like ABB, FANUC, and KUKA continue to dominate the market with their innovative product offerings in the multi-axis positioner space. FANUC's positioners are well-integrated with its robotic arms, providing seamless automation solutions in automotive assembly and heavy manufacturing. Companies like Yaskawa and Kawasaki Robotics also offer advanced positioners, especially suited for welding and handling large parts in automotive production lines. The increasing adoption of collaborative robots and the integration of AI-driven solutions are enhancing the competitive dynamics in this space. Furthermore, several smaller, regional players are gaining traction by offering customized robotic positioners for niche applications such as medical device manufacturing and consumer electronics. Competitive strategies include product innovation, mergers and acquisitions, and strategic partnerships to enhance market presence across regions like North America, Europe, and Asia-Pacific.

ABB

FANUC

KUKA

Yaskawa

Kawasaki Robotics

NACHI Robotics

Mitsubishi Electric

Comau

Stäubli Robotics

Universal Robots

Denso Robotics

Technological advancements in the industrial robot positioners market are reshaping automation across various sectors. The integration of AI, machine learning, and the Industrial Internet of Things (IIoT) into robot positioners has significantly enhanced their capabilities. These technologies enable positioners to offer higher precision, flexibility, and productivity by allowing real-time feedback and adjustments during operations. For example, AI-powered algorithms are being used to optimize the positioning process in welding and painting applications, improving consistency and quality. The development of collaborative robots (cobots) that work alongside human operators is also boosting market growth. These robots utilize advanced sensors, vision systems, and machine learning to ensure safety and enhance operational efficiency. Additionally, there is an increasing focus on energy-efficient robot positioners, which are contributing to cost savings and environmental sustainability. Moreover, the rise in the adoption of modular, lightweight positioners is making it easier for manufacturers to set up flexible, reconfigurable automation systems. These technological shifts are setting the stage for a future where industrial robot positioners will be central to smart factories.

In May 2024, FANUC unveiled its latest line of high-performance positioners, designed to integrate seamlessly with its robotic arms. These positioners feature AI-driven precision controls, allowing for faster and more accurate welding in automotive production lines.

In April 2024, KUKA introduced a new collaborative robot positioner, enabling human-robot collaboration in automotive assembly lines. This technology integrates advanced sensors to improve safety while maintaining high throughput.

In March 2024, ABB launched a new line of energy-efficient positioners, targeting the packaging industry. These positioners are designed to handle a variety of packaging formats and offer lower energy consumption, contributing to more sustainable production lines.

In January 2024, Yaskawa Robotics expanded its portfolio by incorporating AI-enhanced positioners for metalworking and machining applications. These positioners use machine learning to optimize tool handling and reduce cycle times.

In December 2023, Kawasaki Robotics introduced a new series of positioners for use in the electronics sector. These positioners are engineered for precision and can handle delicate components in assembly and testing environments.

The scope of the industrial robot positioners market report includes a detailed analysis of the various types of positioners, including two-axis, three-axis, and single-axis robots. The report covers all major applications, including welding, assembly, painting, material handling, and inspection. In-depth insights into end-user industries such as automotive, electronics, aerospace, and metal and machinery fabrication are provided to help stakeholders understand current trends and growth opportunities. The report also delves into regional markets, identifying key drivers and challenges specific to North America, Europe, Asia-Pacific, and the Middle East & Africa. Technological advancements, such as AI integration and energy-efficient designs, are discussed to highlight their impact on product innovation and operational efficiency. Additionally, recent developments in the market are covered, offering a snapshot of how the industry is evolving in terms of automation, robotics, and digital integration. This comprehensive scope allows businesses to make informed decisions and capitalize on emerging trends in the industrial robot positioners market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 777.53 Million |

|

Market Revenue in 2032 |

USD 1,175.29 Million |

|

CAGR (2025 - 2032) |

5.3% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User Insights

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

ABB, FANUC, KUKA, Yaskawa, Kawasaki Robotics, NACHI Robotics, Mitsubishi Electric, Comau, Stäubli Robotics, Universal Robots, Denso Robotics |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |