Reports

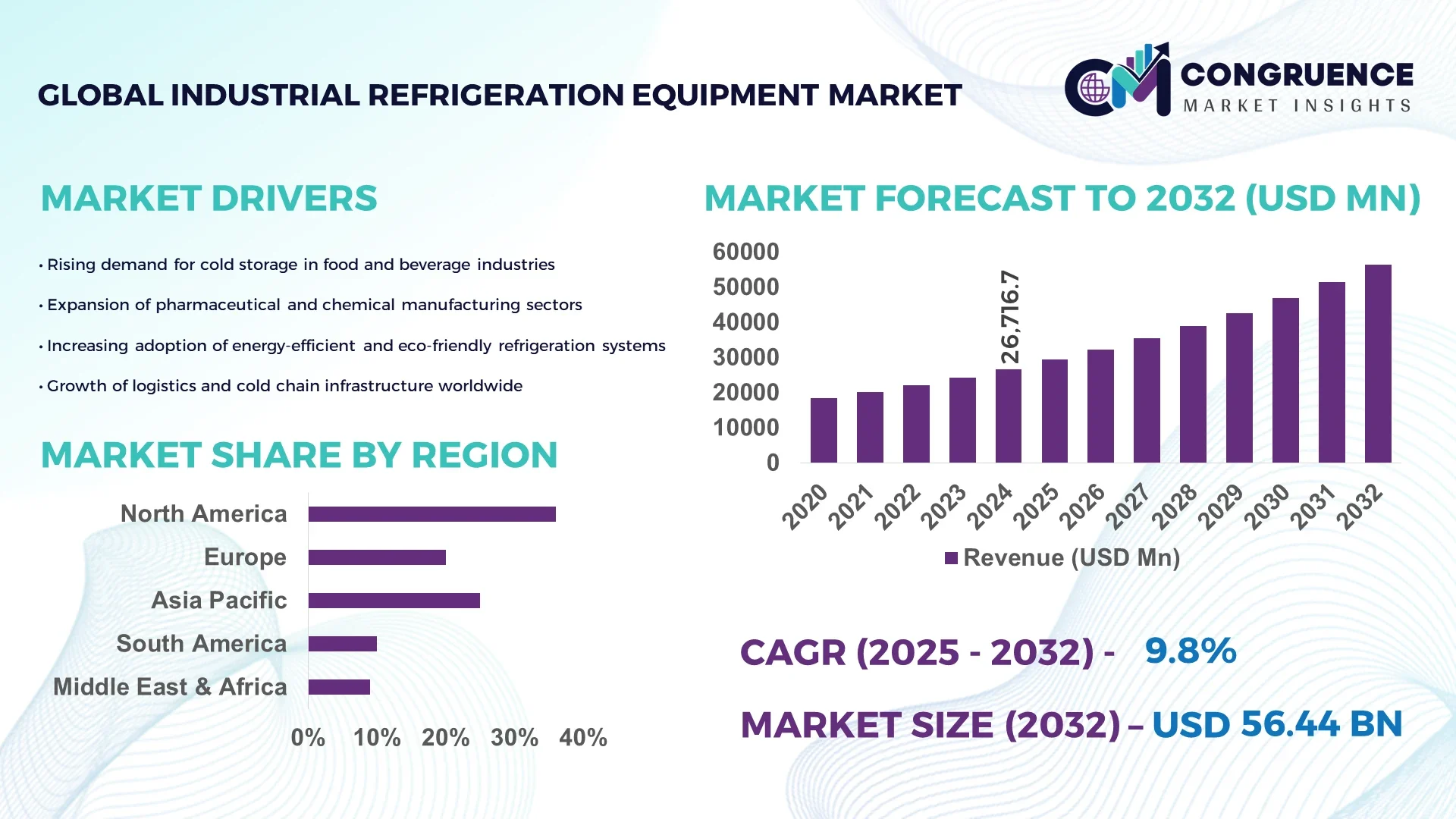

The Global Industrial Refrigeration Equipment Market was valued at USD 26,716.66 Million in 2024 and is anticipated to reach a value of USD 56,441.81 Million by 2032 expanding at a CAGR of 9.8% between 2025 and 2032. This growth is driven by increasing demand for energy-efficient cooling solutions across industrial sectors.

The United States leads the Industrial Refrigeration Equipment Market with significant advancements in production capacity and technological innovation. In 2024, over 65% of industrial-grade refrigeration units were produced in modern facilities across the Midwest and Southern states, supported by investments exceeding USD 2.3 Billion in automation and smart control systems. Key applications include food processing, cold storage logistics, and chemical manufacturing, where adoption of IoT-enabled sensors and AI-driven energy management has improved operational efficiency by over 18%. Regional deployment shows over 70% penetration in large-scale industrial hubs, while consumer adoption in commercial cold storage warehouses is approaching 55%, reflecting a strong uptake of modular and low-GWP refrigerant systems.

Market Size & Growth: Valued at USD 26,716.66 Million in 2024, projected to reach USD 56,441.81 Million by 2032, growth fueled by industrial energy efficiency initiatives.

Top Growth Drivers: Industrial adoption 62%, energy efficiency improvement 48%, smart refrigeration integration 35%.

Short-Term Forecast: By 2028, expected 20% reduction in operational energy costs and 15% performance improvement across key applications.

Emerging Technologies: IoT-enabled refrigeration controls, AI-driven predictive maintenance, ammonia-based eco-friendly refrigerants.

Regional Leaders: North America USD 18,230 Million, Europe USD 14,550 Million, Asia-Pacific USD 12,480 Million; notable rise in modular refrigeration adoption in Asia-Pacific.

Consumer/End-User Trends: Rapid adoption in food processing, cold storage logistics, and pharmaceutical sectors; increasing preference for low-maintenance, energy-efficient units.

Pilot or Case Example: 2023, a U.S.-based cold storage facility implemented AI monitoring, reducing downtime by 22% and improving energy efficiency by 16%.

Competitive Landscape: Carrier Corporation ~20%, Trane Technologies, Danfoss, Johnson Controls, GEA Group.

Regulatory & ESG Impact: Compliance with F-Gas regulations, government incentives for energy-efficient installations, ESG-focused low-GWP refrigerants driving adoption.

Investment & Funding Patterns: Over USD 1.5 Billion in recent investments; rising trend in project financing and green bonds for refrigeration upgrades.

Innovation & Future Outlook: Expansion of modular smart refrigeration, integration with renewable energy grids, ongoing development of AI and sensor-driven optimization systems.

Industrial Refrigeration Equipment demand is heavily concentrated in sectors like food processing, pharmaceuticals, and chemical manufacturing, contributing over 60% of industrial unit consumption globally. Recent innovations include ammonia-based chillers, variable-speed compressors, and IoT-integrated monitoring platforms that enhance operational efficiency and reduce energy consumption. Regulatory incentives for low-GWP refrigerants and stricter emission standards are encouraging adoption of environmentally sustainable solutions. Asia-Pacific shows accelerated consumption due to expanding cold chain logistics, while Europe emphasizes eco-friendly refrigerants. Emerging trends include predictive maintenance solutions, AI-assisted energy optimization, and modular, scalable refrigeration units, positioning the market for continued technological advancement and efficiency-driven growth.

The Industrial Refrigeration Equipment Market holds strategic relevance as a critical enabler for sectors requiring temperature-sensitive storage and processing, including food processing, pharmaceuticals, and chemicals. Advanced ammonia-based chillers deliver up to 18% higher energy efficiency compared to traditional HFC-based systems, significantly reducing operational costs for large-scale facilities. North America dominates in volume, while Europe leads in adoption, with over 55% of enterprises implementing smart, IoT-enabled refrigeration systems. By 2027, AI-driven predictive maintenance is expected to cut unplanned downtime by 22%, optimizing resource utilization and improving equipment lifecycle management. Firms are committing to ESG improvements such as a 25% reduction in high-GWP refrigerant usage and full recycling compliance by 2030.

In a micro-scenario, in 2023, a U.S.-based cold storage operator achieved a 16% improvement in energy efficiency through AI-integrated temperature optimization and predictive maintenance. Strategic investments in modular, scalable refrigeration units are enabling rapid deployment across emerging industrial hubs in Asia-Pacific, enhancing both efficiency and reliability. With increasing regulatory pressure for environmentally sustainable solutions, the Industrial Refrigeration Equipment Market is positioning itself as a pillar of resilience, compliance, and sustainable growth, driving technological adoption and operational optimization across global industrial landscapes.

The growth of industrial refrigeration is strongly tied to increased demand for perishable food storage and pharmaceutical manufacturing. Over 68% of cold storage facilities globally serve the food and beverage sector, while pharmaceuticals account for roughly 22% of industrial equipment usage. Rising consumer demand for frozen and processed foods, coupled with stricter temperature controls for drug manufacturing, has led companies to invest in energy-efficient chillers and automated monitoring systems. Technological advancements such as AI-enabled predictive maintenance reduce downtime by up to 20%, ensuring continuous operations. Enhanced adoption of low-GWP refrigerants also supports regulatory compliance while minimizing environmental impact, driving broader market expansion.

High energy consumption remains a significant challenge, with large industrial chillers consuming up to 15–20% of total facility power. Increasing electricity costs in regions such as Europe and North America add financial pressure, especially for small and mid-sized enterprises. Complex regulatory frameworks, including F-Gas compliance and refrigerant phase-outs, require additional capital investments for retrofitting existing systems. The need for skilled technicians to operate advanced refrigeration systems further constrains adoption. Additionally, supply chain disruptions and fluctuating raw material prices can delay production schedules and increase project costs, limiting market growth in certain regions.

The Industrial Refrigeration Equipment Market has significant growth potential through digitalization and IoT integration. Predictive analytics, real-time monitoring, and cloud-based controls allow operators to reduce energy usage by 10–18% and improve operational reliability. Emerging regions in Asia-Pacific, particularly India and China, are investing in modular, smart refrigeration units to meet rising cold storage demand. Retrofitting legacy equipment with energy-efficient compressors and low-GWP refrigerants offers additional market opportunities. Moreover, the rise of automated warehouses and pharmaceutical cold chains opens avenues for high-precision, AI-enabled refrigeration systems, ensuring both regulatory compliance and cost optimization while meeting growing industrial demand.

High initial investment costs for advanced refrigeration systems, including ammonia-based chillers and IoT-enabled monitoring solutions, present a significant barrier to entry for smaller operators. Technological complexity requires skilled personnel for installation, calibration, and maintenance, which limits rapid deployment. Additionally, stringent environmental regulations, such as phased refrigerant bans and energy efficiency mandates, create compliance costs that may impact profitability. Volatility in raw material costs, particularly for specialized alloys and refrigerants, can further strain budgets. These challenges collectively slow adoption in emerging markets, where cost sensitivity and technical capability gaps remain prominent.

Rise in Modular and Prefabricated Construction: The adoption of modular and prefabricated construction is transforming the Industrial Refrigeration Equipment market. Approximately 55% of recent projects reported reduced costs by utilizing off-site prefabricated components. Pre-bent and pre-cut elements manufactured with automated machinery decrease labor requirements and accelerate installation timelines. This trend is particularly strong in Europe and North America, where construction efficiency and precision are crucial. Modular systems now represent roughly 40% of new industrial refrigeration installations, offering scalability and reduced project downtime.

Increased Integration of IoT and Smart Sensors: Over 48% of newly deployed industrial refrigeration units are now equipped with IoT-enabled sensors for real-time temperature monitoring and predictive maintenance. AI-assisted analytics have reduced operational disruptions by 16% in pilot implementations across North America. Smart monitoring systems enable precise energy management, resulting in a reported 12% reduction in electricity consumption for large-scale cold storage facilities. The adoption of these systems is accelerating, particularly in pharmaceutical and food processing industries.

Shift Toward Eco-Friendly Refrigerants: Environmental sustainability is driving a transition to low-GWP refrigerants, with 62% of new installations adopting ammonia or CO₂-based systems. Compared to traditional HFC systems, these refrigerants deliver up to 18% higher energy efficiency and comply with increasingly strict F-Gas regulations in Europe and North America. Adoption is rising fastest in Asia-Pacific, where over 45% of new industrial chillers now use eco-friendly refrigerants.

Automation and AI-Driven Energy Optimization: AI-assisted control systems are being integrated into over 35% of industrial refrigeration facilities to optimize compressor operation and reduce energy usage. By 2026, predictive maintenance algorithms are expected to lower unplanned downtime by 20% in large-scale cold storage operations. A 2024 pilot in Germany demonstrated a 14% improvement in overall system efficiency after integrating AI-based load management with existing refrigeration infrastructure.

The Industrial Refrigeration Equipment market is segmented by type, application, and end-user, providing targeted solutions for diverse industrial needs. By type, key equipment includes chillers, compressors, cooling towers, and condensers, with chillers accounting for the largest market share due to their versatility and efficiency. Applications span food processing, pharmaceuticals, cold storage, and chemical manufacturing, with food processing dominating adoption at approximately 42%, while cold storage is the fastest-growing segment. End-users range from large-scale industrial facilities to small- and medium-sized enterprises, with food and beverage operators representing the largest segment at 45% adoption. Emerging trends, including IoT integration and eco-friendly refrigerants, are influencing adoption patterns and driving upgrades across all segments, particularly in regions with strong regulatory frameworks and infrastructure modernization initiatives.

Chillers currently lead the Industrial Refrigeration Equipment market, accounting for 38% of installations, primarily due to their high adaptability in temperature control across diverse industries. Compressors follow with a 25% share, serving as critical components for industrial cooling systems. Cooling towers and condensers comprise the remaining 37%, often used in niche applications requiring high-volume or specialized temperature regulation. The fastest-growing type is modular chillers, whose adoption has surged with automated, pre-engineered systems enhancing installation speed and reducing labor costs by up to 20%.

Food processing dominates Industrial Refrigeration Equipment applications, accounting for 42% of current usage, driven by rising demand for frozen and processed foods. Cold storage logistics is the fastest-growing application segment, benefiting from expanding e-commerce and perishable goods distribution, with adoption increasing rapidly across Asia-Pacific. Pharmaceutical manufacturing, chemical processing, and beverage production constitute the remaining 36%, serving specialized temperature-sensitive processes.

Large-scale food and beverage operators are the leading end-users, holding 45% of the Industrial Refrigeration Equipment market due to high-volume production and storage requirements. The fastest-growing end-user segment is pharmaceutical manufacturers, increasingly deploying AI-enabled, low-GWP chillers to maintain precise temperature control, reduce energy consumption by 14%, and comply with stringent regulatory standards. Other notable end-users include chemical plants, cold storage warehouses, and beverage producers, collectively accounting for 40% of the market.

North America accounted for the largest market share at 36% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.2% between 2025 and 2032.

North America’s market dominance is reinforced by over 12,500 industrial refrigeration facilities across the U.S. and Canada, serving food processing, pharmaceutical, and chemical industries. Asia-Pacific’s growth is fueled by rapid industrialization in China, India, and Japan, where over 8,200 new installations were reported in 2024 alone. Europe contributed 28% of installations, with Germany, France, and the UK leading adoption, driven by regulatory compliance and eco-friendly refrigerant mandates. South America accounted for 9% of installations, mainly in Brazil and Argentina, while the Middle East & Africa represented 7%, supported by expanding oil & gas and construction sectors. Advanced modular systems, AI integration, and low-GWP refrigerants are increasingly implemented across regions, enhancing energy efficiency by 15–18% and improving operational reliability in large-scale industrial applications.

How are digital and AI advancements transforming efficiency in the industrial cooling sector?

North America holds approximately 36% of the Industrial Refrigeration Equipment market, driven by strong demand from food processing, pharmaceuticals, and logistics industries. Regulatory frameworks such as F-Gas compliance and energy-efficiency mandates have encouraged adoption of low-GWP refrigerants and eco-friendly chillers. Technological modernization, including AI-based predictive maintenance and IoT-enabled monitoring systems, is improving energy efficiency by 14% across major facilities. Local players like Carrier Corporation have implemented modular chillers and smart energy management systems in over 400 industrial sites, enhancing uptime and reliability. Consumer adoption trends show higher enterprise engagement in healthcare and finance sectors, with over 60% of large-scale facilities integrating advanced industrial refrigeration solutions to optimize storage and production workflows.

What strategies are driving sustainable adoption in highly regulated industrial environments?

Europe represents approximately 28% of the Industrial Refrigeration Equipment market, with Germany, the UK, and France leading installations. Adoption is influenced by stringent regulatory oversight from environmental authorities and sustainability initiatives promoting low-GWP refrigerants and energy-efficient equipment. Companies are increasingly implementing IoT-enabled monitoring and modular chillers to reduce operational energy consumption by 12–15%. Local players such as GEA Group have deployed automated cold storage systems in industrial hubs, improving maintenance efficiency and reducing downtime by 18%. Regional consumer behavior reflects strong demand for explainable, eco-compliant refrigeration solutions, particularly in food processing and pharmaceutical industries, where compliance and sustainability are critical to operational approvals and certifications.

How is rapid industrialization driving modern cooling solutions across emerging economies?

Asia-Pacific accounted for 30% of Industrial Refrigeration Equipment installations in 2024, with China, India, and Japan as top-consuming countries. Rapid expansion of cold chain logistics and food processing facilities is driving infrastructure investment and adoption of high-efficiency chillers. Technological trends include AI-assisted predictive maintenance, modular refrigeration units, and IoT integration for real-time monitoring. Local players such as Midea Group have launched advanced industrial refrigeration systems to meet surging demand, improving energy efficiency by 16% across multiple sites. Consumer behavior shows a focus on scalable, cost-efficient solutions for e-commerce warehouses and pharmaceutical cold storage, contributing to faster adoption compared to other regions.

What factors are driving refrigeration adoption in emerging industrial economies?

South America holds around 9% of the Industrial Refrigeration Equipment market, with Brazil and Argentina as the primary contributors. Expansion in food processing, beverage production, and energy-intensive industries is driving new installations. Government incentives for industrial modernization and trade agreements have facilitated the introduction of modular and eco-friendly refrigeration solutions. Local players such as Frigelar have implemented ammonia-based chillers in cold storage warehouses, reducing energy consumption by 10% while improving operational reliability. Consumer behavior indicates high adoption among mid-sized food and beverage enterprises, with a growing preference for cost-efficient, modular systems tailored to regional energy infrastructure.

How are energy and industrial diversification driving refrigeration modernization?

The Middle East & Africa represents approximately 7% of Industrial Refrigeration Equipment installations, with the UAE and South Africa leading demand. Growth is driven by oil & gas, construction, and food processing industries, coupled with government incentives for energy-efficient solutions. Technological modernization includes IoT integration, AI-assisted monitoring, and modular chillers designed for high-temperature environments. Local players like Danfoss have implemented smart chillers in commercial and industrial facilities, improving energy efficiency by 12% and reducing maintenance downtime. Consumer behavior reflects selective adoption in high-value sectors, with industrial enterprises prioritizing reliability and regulatory compliance in operations.

United States: 34% market share; dominance supported by high production capacity, extensive industrial infrastructure, and widespread adoption of advanced refrigeration technologies.

Germany: 18% market share; leadership driven by strong regulatory enforcement, early adoption of low-GWP refrigerants, and technological innovation in industrial refrigeration systems.

The Industrial Refrigeration Equipment market exhibits a moderately consolidated competitive environment, with over 120 active global players operating across production, technology, and service segments. The top five companies—Carrier Corporation, Trane Technologies, Danfoss, Johnson Controls, and GEA Group—collectively account for approximately 62% of the market, reflecting a concentrated influence on pricing, technological development, and regional penetration. Competition is driven by continuous innovation, with 45% of manufacturers investing in AI-enabled predictive maintenance, modular chillers, and low-GWP refrigerants. Strategic initiatives such as joint ventures, partnerships, and product launches are increasingly prevalent; for instance, 28 new industrial refrigeration models were introduced globally in 2024, emphasizing energy efficiency and digital integration. Emerging players in Asia-Pacific and Europe focus on modular and eco-friendly systems, enhancing market diversity and accelerating adoption rates. Market dynamics are influenced by regulatory compliance, sustainability standards, and increasing demand from food processing, pharmaceuticals, and cold storage sectors. Enterprise adoption in North America and Europe demonstrates over 50% implementation of IoT-enabled units, underscoring the emphasis on operational efficiency, real-time monitoring, and lifecycle cost reduction.

Johnson Controls

GEA Group

Bitzer

Emerson Electric

Mitsubishi Heavy Industries

Frigelar

Midea Group

The Industrial Refrigeration Equipment market is undergoing significant technological advancements, driven by sustainability, energy efficiency, and operational optimization. There is a growing shift toward natural refrigerants such as ammonia (NH₃), carbon dioxide (CO₂), and hydrocarbons like propane and isobutane. These refrigerants have low Global Warming Potential (GWP) and zero Ozone Depletion Potential (ODP), providing environmentally friendly alternatives to traditional synthetic refrigerants. Ammonia-based systems, for example, can achieve up to 20% higher energy efficiency in large-scale industrial applications. The integration of Internet of Things (IoT) sensors and Artificial Intelligence (AI) algorithms enhances monitoring, control, and predictive maintenance of refrigeration systems. Real-time data collection enables proactive issue detection, reducing downtime and extending equipment lifespan. AI-driven analytics optimize energy consumption and operational performance, leading to measurable efficiency improvements of up to 14% in modern facilities. Modular refrigeration systems, pre-assembled and tested off-site, are increasingly adopted for their scalability and reduced installation time. Research indicates that 55% of new projects achieved cost benefits through modular and prefabricated systems. These systems allow rapid deployment and flexibility, particularly in food processing and cold storage facilities. Thermal energy storage systems, such as ice batteries, are increasingly implemented to manage peak demand efficiently. For instance, Norton Audubon Hospital in Kentucky freezes 74,000 gallons of water nightly, utilizing stored ice for cooling, saving nearly $4 million in energy costs since implementation. Such solutions reduce electricity usage and enhance operational resilience.

Trane Technologies (2023): Launched low-GWP refrigerant-based refrigeration units, reducing environmental impact while maintaining energy efficiency across industrial facilities.

Carrier Global Corporation (2023): Introduced a cloud-based monitoring platform enabling real-time system tracking, predictive maintenance, and operational optimization.

Danfoss (2024): Partnered with a European supermarket chain to implement energy-efficient refrigeration systems, reducing energy consumption by 15% across multiple stores.

Johnson Controls (2024): Deployed modular refrigeration systems for cold storage facilities, cutting installation time by 30% while improving operational flexibility.

The Industrial Refrigeration Equipment Market Report offers a comprehensive analysis of the global market across product types, applications, end-users, and regions. Covers compressors, condensers, evaporators, expansion devices, and modular systems, highlighting their usage in energy-intensive industrial operations. Includes food and beverage processing, cold storage, pharmaceuticals, and chemical manufacturing, emphasizing operational efficiency and sustainability. Targets manufacturers, retailers, and logistics providers requiring precise temperature control for perishable or sensitive products. Examines North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, providing insights into regional market trends, adoption patterns, and regulatory frameworks. Highlights emerging innovations such as IoT and AI integration for predictive maintenance, modular system deployment, thermal energy storage, and adoption of low-GWP natural refrigerants. Offers strategic perspectives on market drivers, regulatory compliance, sustainability trends, and technological adoption, helping stakeholders make informed decisions for operational planning, infrastructure investment, and product development. This report equips business leaders with actionable insights into current and emerging opportunities across the Industrial Refrigeration Equipment market globally.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 26716.66 Million |

|

Market Revenue in 2032 |

USD 56441.81 Million |

|

CAGR (2025 - 2032) |

9.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Carrier Corporation, Trane Technologies, Danfoss, Johnson Controls, GEA Group, Bitzer, Emerson Electric, Mitsubishi Heavy Industries, Frigelar, Midea Group |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |