Reports

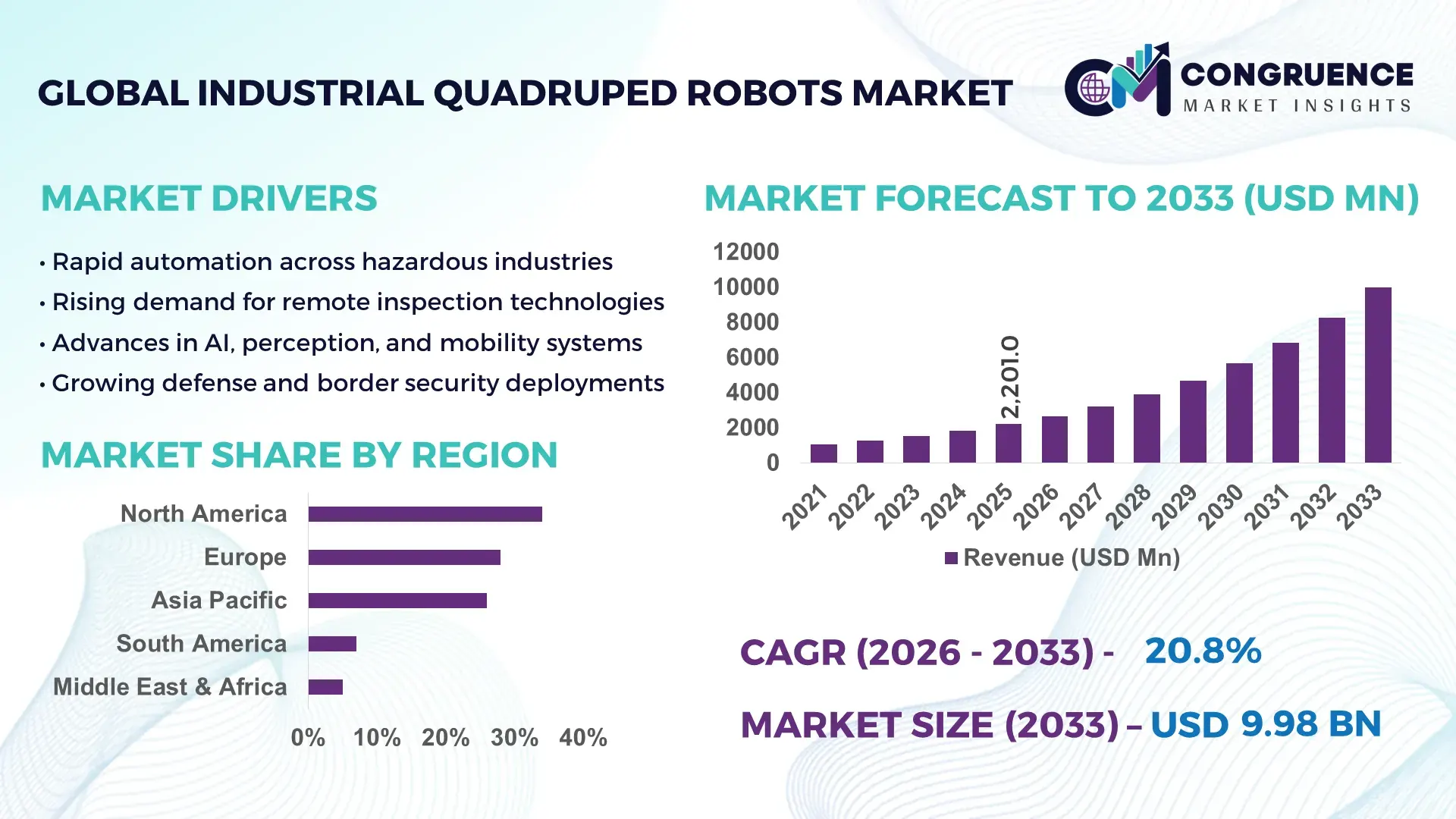

The Global Industrial Quadruped Robots Market was valued at USD 2,201 Million in 2025 and is anticipated to reach USD 9,980.6 Million by 2033, expanding at a CAGR of 20.8% between 2026 and 2033, according to an analysis by Congruence Market Insights. This rapid expansion is being propelled by accelerating automation in hazardous and remote industrial environments where traditional wheeled robots cannot operate effectively.

The United States anchors the global industrial quadruped ecosystem through deep manufacturing capability, sustained public–private investment, and advanced robotics R&D infrastructure. U.S. facilities are estimated to assemble 6,000–8,000 units annually, supported by over USD 250 million in federal and defense-linked robotics funding since 2022. More than 40 testbeds across energy, defense, and logistics sites actively deploy quadrupeds for inspection, mapping, and maintenance. U.S. firms lead in autonomy software, ruggedized hardware, and edge-AI processors, while large utilities and petrochemical operators routinely integrate quadrupeds into digital twin workflows and predictive maintenance platforms.

Market Size & Growth: USD 2,201 Mn (2025) to USD 9,980.6 Mn (2033); 20.8% CAGR driven by automation in hazardous sites.

Top Growth Drivers: 38% faster inspection cycles; 32% reduction in manual exposure risk; 27% lower downtime from autonomous monitoring.

Short-Term Forecast: By 2028, predictive AI diagnostics could cut unplanned shutdowns by 25% across heavy industry.

Emerging Technologies: Multi-modal SLAM, edge AI chips, 5G/Private LTE connectivity, and cloud-robot orchestration.

Regional Leaders (2033): North America ~USD 3.2 Bn (defense-energy integration); Europe ~USD 2.6 Bn (safety-first regulation); Asia-Pacific ~USD 2.9 Bn (manufacturing scale).

End-User Trends: Rapid uptake in energy, chemicals, mining, and intralogistics for round-the-clock patrols.

Pilot Example: In 2024, a refinery pilot reduced inspection time by 45% using autonomous quadrupeds.

Competitive Landscape: Leading player ~18% share; key competitors include Boston Dynamics, Ghost Robotics, ANYbotics, Unitree Robotics, and AgileX.

Regulatory & ESG Impact: Stricter worker-safety rules and emissions monitoring standards accelerating adoption.

Investment Patterns: Over USD 1.1 Bn invested globally since 2021 via VC, defense grants, and industrial pilots.

Innovation & Outlook: Tighter integration with digital twins, autonomous charging docks, and mixed human-robot teams.

Quadruped robots are gaining traction in energy & utilities (≈35% use cases), chemicals (≈25%), and manufacturing/logistics (≈22%), supported by rugged hardware, longer-life batteries, and thermal imaging payloads. New standards on hazardous-area robotics and methane monitoring are shaping procurement, while Asia-Pacific factories and European safety-centric plants are emerging as high-growth adopters. Future momentum centers on fleet management software, autonomous charging, and AI-based anomaly detection.

Industrial quadruped robots are becoming a foundational layer of modern asset-intensive industries by combining mobility, sensing, and autonomy in environments where traditional automation fails. Strategically, they enable continuous operations in refineries, power plants, mines, and chemical facilities—sites characterized by uneven terrain, extreme temperatures, and safety risks that limit human access. Companies increasingly view quadrupeds not as experimental tools but as core infrastructure for digital operations and risk management.

From a technology benchmark perspective, vision-based SLAM fused with lidar delivers ~35% better localization accuracy compared to lidar-only navigation, reducing drift in cluttered industrial sites and improving reliability of autonomous patrol routes. Sensor modularity and standardized payload bays also shorten deployment cycles, allowing firms to repurpose the same robot across inspection, mapping, and gas-leak detection missions.

Regionally, Asia-Pacific dominates in deployment volume, driven by large-scale manufacturing and petrochemicals, while Europe leads in adoption intensity with roughly 42% of major industrial enterprises running regular quadruped programs, reflecting stringent safety and emissions rules. North America remains the innovation hub for autonomy software, edge computing, and defense-adjacent applications.

In the short term, by 2028, next-generation edge-AI analytics are expected to reduce asset inspection downtime by 28% through real-time anomaly detection and automated work orders. Connectivity via private 5G networks will further enable multi-robot coordination across sprawling facilities.

On the ESG front, many firms are committing to 30% reductions in fugitive emissions by 2030, using quadrupeds equipped with methane sensors to perform continuous monitoring without shutting down operations. The robots also cut worker exposure to heat and toxic gases, strengthening corporate safety metrics.

A practical micro-scenario illustrates the value: in 2024, a Siemens-operated chemical site deployed autonomous quadrupeds for night inspections and achieved a 40% reduction in manual patrol hours while improving fault-detection speed by 33%.

Overall, the Industrial Quadruped Robots Market is evolving into a pillar of resilient, compliant, and sustainable industrial operations—where autonomy, data, and physical mobility converge to keep critical infrastructure safer, cleaner, and more productive.

The Industrial Quadruped Robots Market is shaped by rapid digitalization of asset-heavy sectors, stricter workplace safety regulations, and the need for continuous, low-risk inspection in hazardous environments. Demand is accelerating in energy, chemicals, mining, and utilities, where rugged terrain and confined spaces limit traditional automation. Advances in AI perception, edge computing, and battery systems are expanding functional use cases from simple patrols to autonomous diagnostics and collaborative tasks with human workers. At the same time, procurement is becoming more standardized as enterprises move from pilots to fleet-scale deployments supported by robot management software, private 5G networks, and digital twins. Competitive dynamics are intensifying as hardware innovators, software startups, and industrial automation giants converge, while integration costs, interoperability, and workforce reskilling remain central market considerations.

Rising incidents of industrial accidents and stricter safety mandates are pushing operators to minimize human exposure in high-risk zones such as refineries, chemical plants, and power stations. Quadruped robots can navigate stairs, debris, and uneven surfaces where wheeled systems fail, enabling continuous monitoring without shutting down operations. In energy facilities, autonomous patrols have been shown to cut manual inspection hours by 30–50%, while improving detection of thermal anomalies and gas leaks. Mining and heavy manufacturing sites increasingly rely on robots for confined-space mapping, reducing the need for dangerous human entry. Additionally, insurers and regulators are incentivizing robotic inspections through lower premiums and compliance credits, further embedding quadrupeds into routine maintenance workflows across critical infrastructure.

Despite strong potential, adoption is constrained by upfront hardware costs, specialized software requirements, and complex integration with legacy industrial systems. Many facilities lack standardized digital infrastructure, forcing firms to invest heavily in private networks, sensor retrofits, and data platforms before robots can operate effectively. Battery limitations—typically 2–4 hours of intensive use—require frequent charging cycles and additional docking infrastructure. Workforce resistance and skill gaps also slow deployment, as technicians need training in robotics operations and cybersecurity. Furthermore, interoperability issues between different robot platforms and enterprise asset management systems create friction, lengthening pilot phases and delaying full-scale rollouts in conservative, risk-averse industries.

The shift toward lights-out facilities and remote operations opens significant opportunities for quadruped robots to handle internal logistics, inspection, and emergency response. In large industrial campuses, robots can autonomously transport tools, spare parts, and sensor payloads across kilometers of complex terrain, reducing vehicle traffic and emissions. Utilities are exploring continuous substation monitoring, where quadrupeds equipped with thermal cameras can replace manual checks and prevent transformer failures. The expansion of hydrogen and renewable projects—often located in remote or harsh environments—creates new demand for rugged autonomous systems. As battery technology improves and autonomous charging docks proliferate, robot fleets can operate nearly continuously, enabling scalable subscription-based monitoring services across multiple sites.

Industrial sites treat operational data as highly sensitive, making cybersecurity a major barrier to robot deployment. Concerns over wireless control, cloud connectivity, and potential system breaches require costly hardened networks and compliance certifications. Regulatory approval for autonomous operations in hazardous zones remains fragmented across regions, slowing cross-border deployments. Battery performance also limits mission duration, particularly in extreme heat or cold where efficiency can drop by 15–25%. Additionally, ruggedizing hardware against dust, moisture, and chemical exposure increases manufacturing complexity and maintenance costs, complicating large-scale fleet expansion in heavy industries.

Rise in Modular and Prefabricated Construction: Modular and prefabricated practices are reshaping demand for high-precision industrial robotics. Around 55% of recent projects report cost benefits from off-site fabrication, where automated machines cut and pre-bend components with millimeter accuracy. Quadrupeds are increasingly used inside factories and construction yards for quality inspection and material tracking, reducing manual checks by roughly 30% while accelerating project timelines across Europe and North America.

Autonomous Navigation and Edge AI Maturity: New multi-sensor navigation stacks combining vision, lidar, and inertial systems have lifted autonomous success rates to about 92% in cluttered facilities. Edge AI processors now perform real-time anomaly detection on-board, cutting cloud dependency by 40% and enabling faster safety responses during gas-leak or overheating events.

Expansion of Human–Robot Collaboration: Collaborative workflows are rising as quadrupeds carry tools, guide workers, or map sites in real time. Pilot programs show 25–35% productivity gains when mixed teams conduct inspections, while reducing worker exposure to hazardous zones by nearly 30%.

Longer Endurance and Ruggedization: Next-generation batteries and thermal management systems have extended active mission time to 4–6 hours, up from roughly 2–3 hours earlier. Manufacturers are also improving dust- and water-resistance to IP66/IP67 levels, lowering maintenance downtime by about 20% in harsh industrial environments.

The Industrial Quadruped Robots Market is structured around distinct types, applications, and end-user segments that reflect varying operational needs across industrial environments. By type, differentiation is driven by autonomy levels, payload capacity, and mobility features, ranging from inspection-focused units to logistics-enabled platforms. Application segmentation centers on use cases such as inspection, surveillance, mapping, and material handling, with adoption shaped by terrain complexity, safety requirements, and digital integration maturity. End-user demand is concentrated in asset-heavy industries—particularly energy, chemicals, mining, and manufacturing—where continuous monitoring and risk reduction are priorities. Increasing use of sensor payloads, edge computing, and fleet management software is blurring boundaries between segments, while customization for sector-specific workflows (e.g., methane detection in utilities or confined-space mapping in mining) is deepening specialization across the market.

Industrial quadruped robots are broadly categorized by design capability and autonomy architecture. Autonomous inspection quadrupeds currently represent the leading type with approximately 38% share, driven by their ability to navigate complex terrain while carrying thermal, gas, and visual sensors for real-time diagnostics. Their dominance stems from proven reliability in refineries, substations, and chemical plants, where continuous monitoring reduces manual risk and unplanned downtime.

The fastest-growing type is logistics-enabled quadrupeds, expanding at roughly 24% CAGR, fueled by rising demand for autonomous intra-plant transport of tools, samples, and spare parts across sprawling industrial campuses. Improvements in load stability, collaborative navigation, and docking systems are accelerating their uptake in manufacturing and energy sites.

Hybrid multi-mission quadrupeds (combining inspection, mapping, and transport) account for about 17%, gaining traction as enterprises seek flexible platforms rather than single-purpose machines. Surveillance-optimized quadrupeds contribute roughly 12%, favored in defense, perimeter security, and critical infrastructure protection. Research and experimental units make up the remaining 13%, serving testing, academia, and pilot deployments with modular architectures.

• In 2024, a major U.S. national laboratory demonstrated long-duration autonomous patrols using inspection quadrupeds across a 12-km energy corridor, validating multi-day mission reliability in extreme temperatures.

Inspection and monitoring is the leading application at about 36% share, as operators prioritize continuous asset health checks in hazardous environments using thermal imaging, gas detection, and visual analytics. This use case dominates in refineries, power plants, and chemical facilities where terrain complexity and safety risks limit human access.

The fastest-growing application is autonomous material handling, rising at roughly 22% CAGR, supported by advances in load-bearing stability, collaborative navigation, and automated docking within smart factories and large industrial campuses.

Mapping and digital twin integration represents about 18%, enabling high-resolution site models for predictive maintenance and planning. Perimeter surveillance and security contributes roughly 14%, particularly around energy infrastructure and sensitive facilities. Emergency response and disaster inspection makes up the remaining 12%, used in fire, flood, or chemical incidents where human entry is unsafe. In 2025, more than 41% of large industrial enterprises reported piloting quadruped robots for routine site inspections and anomaly detection. Around 58% of safety managers in energy and chemicals indicate higher confidence in facilities that deploy autonomous inspection robots.

• In 2024, a European grid operator used quadruped robots for substation monitoring across 120 sites, reducing manual patrol frequency while improving fault detection accuracy during peak heat conditions.

The energy and utilities sector leads with roughly 34% share, driven by the need for continuous monitoring of substations, pipelines, and renewable installations located in remote or hazardous terrain. Quadrupeds reduce human exposure to heat, toxic gases, and high-voltage environments while enabling real-time asset analytics.

The fastest-growing end-user is manufacturing and logistics, expanding at about 21% CAGR, as smart factories adopt autonomous robots for internal transport, quality checks, and facility surveillance within Industry 4.0 ecosystems.

Chemicals and petrochemicals account for around 22%, where robots perform leak detection, confined-space inspections, and equipment diagnostics. Mining and heavy industry contribute roughly 14%, using quadrupeds for underground mapping and conveyor monitoring. Defense and critical infrastructure security represent the remaining 10%, emphasizing rugged mobility and autonomous patrols. In 2025, about 44% of energy companies tested quadruped robots for predictive maintenance programs. Nearly 36% of large manufacturers integrated autonomous robots into facility safety workflows.

• In 2024, a North American refinery deployed autonomous quadruped fleets for night inspections, cutting manual patrol hours by 40% while improving early fault detection across high-risk units.

North America accounted for the largest market share at 34% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 22.9% between 2026 and 2033.

Europe followed North America with a 28% share, supported by strong regulatory alignment and industrial automation maturity. Asia-Pacific held 26% share in 2025, driven by manufacturing scale and rapid industrial digitization. South America and the Middle East & Africa represented 7% and 5%, respectively, reflecting early-stage adoption concentrated in energy, mining, and infrastructure projects. Collectively, these regional shares, indicating a balanced global distribution with clear leadership in developed markets and accelerated momentum in emerging industrial economies. Rising deployment volumes, expanding industrial robot fleets, and increasing public–private investments are reshaping regional demand patterns across all five geographies.

North America held approximately 34% of the global market share in 2025, making it the leading regional contributor. Demand is primarily driven by energy & utilities, oil & gas, defense, chemicals, and advanced manufacturing, where autonomous inspection and safety compliance are mission-critical. Federal and state-level support for robotics R&D, coupled with defense modernization programs and industrial safety regulations, continues to accelerate deployment. Technologically, the region leads in edge AI, autonomous navigation software, digital twins, and private 5G integration. Local players are actively commercializing fleet-level deployments; for example, U.S.-based robotics firms are expanding multi-robot orchestration platforms across refineries and substations. Regional adoption behavior shows higher enterprise-scale deployments, with over 45% of large industrial operators favoring long-term robotic service contracts rather than single-unit purchases.

Europe accounted for nearly 28% of the global market share in 2025, with Germany, the UK, and France serving as core demand centers. Strong worker safety directives, emissions monitoring mandates, and ESG compliance frameworks are major adoption catalysts. European industries are integrating quadruped robots into predictive maintenance, methane detection, and smart factory initiatives. The region emphasizes explainable AI, certified autonomy, and interoperability standards, aligning robotics deployment with regulatory oversight. Local robotics firms and system integrators are customizing platforms for chemical plants and utilities. Consumer behavior reflects compliance-driven purchasing, where industrial buyers prioritize certified, auditable robotic systems over experimental deployments.

Asia-Pacific represented around 26% of global market share in 2025, ranking second by volume. China, Japan, South Korea, and India are the largest consuming countries, supported by large-scale manufacturing, mining, and infrastructure development. The region benefits from dense robot manufacturing ecosystems, cost-efficient component supply chains, and strong government-backed automation programs. Innovation hubs in China and Japan are advancing battery efficiency, actuator miniaturization, and AI vision systems. Regional adoption behavior is characterized by high-volume deployments, particularly in logistics parks and industrial zones, where enterprises favor rapid scalability and cost efficiency over customization.

South America captured approximately 7% of the global market share in 2025, led by Brazil, Chile, and Argentina. Adoption is concentrated in mining operations, oil & gas facilities, and large infrastructure assets, where terrain complexity favors legged robotics. Government incentives tied to industrial modernization and mining safety standards are supporting gradual adoption. Local system integrators are piloting quadruped robots for tailings dam monitoring and pipeline inspection. Regional buyer behavior shows project-based adoption, with robots typically deployed for specific operational risks rather than continuous fleet usage.

The Middle East & Africa region accounted for about 5% of global market share in 2025, with demand centered in the UAE, Saudi Arabia, and South Africa. Key use cases include oil & gas facility inspection, construction site monitoring, and critical infrastructure security. National digital transformation agendas and smart city initiatives are encouraging the adoption of autonomous robotics. Industrial buyers in this region prioritize ruggedization, heat tolerance, and long-range communication. Adoption behavior is largely government- and enterprise-led, with pilot programs expanding into multi-site deployments.

United States – 22% Market Share: Strong production capability, high defense and energy-sector adoption, and advanced robotics R&D infrastructure.

China – 18% Market Share: Large-scale manufacturing base, rapid industrial automation, and strong government support for robotics deployment.

The competitive environment in the Industrial Quadruped Robots Market is moderately fragmented yet increasingly dynamic, with over 30 active global competitors offering platforms tailored to various industrial use cases such as inspection, surveillance, autonomous transport, and rugged terrain navigation. Established players maintain strong brand positioning, proprietary software ecosystems, and extensive service networks, while emerging firms aggressively pursue differentiated technology and strategic partnerships to expand their market footprint. The combined share of the top 5 companies—including Boston Dynamics, Unitree Robotics, ANYbotics, Ghost Robotics, and Deep Robotics—accounts for approximately 57–62% of global deployments, underscoring a concentrated leadership yet leaving meaningful space for niche specialists and regional innovators.

Strategic initiatives vary across the competitive set: Boston Dynamics recently secured enterprise-scale logistics contracts and expanded its service offerings, while Unitree Robotics inked distribution partnerships to boost market reach in North America and Europe. Ghost Robotics launched next-generation rugged platforms designed for outdoor industrial environments, enhancing autonomy and payload capacity. ANYbotics strengthened vertical solutions through collaboration with offshore operators, capturing specialized inspection workflows. Meanwhile, precision motion and actuator suppliers such as Moog Inc. are vertically integrating to supply core components, intensifying competition over hardware capabilities.

Innovation trends strongly influence competitive dynamics. Multi-sensor perception stacks combining LiDAR, thermal, and vision inputs are becoming baseline expectations, while modular design architectures enabling rapid payload swaps and maintenance turnaround are gaining traction across the industry. Edge-AI navigation, fleet orchestration software, and private network integration are emerging as differentiators. Competitive pressure is also driving more frequent product launches and iterative upgrades, with over 15 new quadruped models introduced recently featuring higher endurance, advanced autonomy, and enhanced environmental tolerance.

Overall, the market balances established incumbents with deep industrial credentials and a wave of agile challengers pushing boundaries in autonomy, perception, and deployment scenarios—creating a robust competitive landscape tailored to evolving industrial automation demands.

ANYbotics

Deep Robotics

Agility Robotics

Clearpath Robotics

Diligent Robotics

Festo

Bionic Robotics

Agility Robotics

Adept MobileRobots

PAL Robotics

Kawasaki Heavy Industries

Honda Motor Co

SEER Robotics

Nex Robotics

The Industrial Quadruped Robots Market is heavily shaped by rapid advancements in autonomy, perception, mobility, and software orchestration that collectively enhance operational effectiveness in industrial environments. Modern quadrupeds increasingly integrate multi-sensor perception stacks—combining LiDAR, RGB cameras, thermal imaging, and ultrasonic sensors—to deliver robust environment awareness across light conditions, dust, and cluttered spaces. Approximately 42% of newer models now incorporate triple-sensor fusion, enabling precise obstacle avoidance and terrain mapping.

Autonomous navigation and control technologies leveraging edge AI, reinforcement learning, and real-time SLAM (Simultaneous Localization And Mapping) have significantly reduced reliance on tethered supervision. These systems support adaptive path planning across complex industrial sites, while advanced locomotion controllers improve stability on uneven surfaces, inclines, and debris. Recent research into hierarchical perception and reflexive evasion algorithms is further enhancing responsiveness and safety in dynamic environments.

Battery and power management systems are key innovation vectors, with emerging modular battery architectures extending continuous operation to 4–6 hours and support for autonomous charging and swappable modules. These advancements reduce downtime and increase utilization rates in round-the-clock operations.

Modularity and payload flexibility are becoming standard, allowing operators to quickly switch between inspection sensors, manipulators, and specialized instruments without extensive field recalibration. Software platforms are evolving in parallel, enabling fleet orchestration, diagnostics, and remote monitoring through private 5G/LTE networks and cloud-connected dashboards.

Industrial ecosystems are also integrating safety and compliance features such as redundant control loops, certified emergency stop systems, and compliance with industrial communication protocols. The convergence of robotics with digital twin environments allows virtual simulation of missions, predictive maintenance planning, and scenario validation before physical deployment, accelerating enterprise adoption.

Together, these technologies are transitioning quadruped robots from experimental assets into operational cornerstones for asset-intensive industries such as energy, mining, chemicals, and manufacturing—where mobility, perception, and autonomy are pivotal to enhancing safety, productivity, and reliability.

• In January 2026, Boston Dynamics unveiled the new production version of its Atlas humanoid robot at CES Las Vegas 2026, marking a strategic expansion from quadruped robotics into broader industrial automation with multi-task capabilities, autonomous navigation, and integration with enterprise systems, with fleets already committed for deployment. Source: www.bostondynamics.com

• In May 2025, Boston Dynamics expanded its Spot developer ecosystem by publicly releasing the Spot Software Development Kit (SDK) to enable developers to build custom payloads and applications, increasing flexibility and accelerating industry-specific deployments across construction, energy, public safety, and mining sectors. Source: www.bostondynamics.com

• In May 2025, ANYbotics hosted the ANYmal Research Meetup at ICRA 2025, where it launched the ANYmal Research Manipulation Payload, a new mobile manipulation system featuring advanced torque-controlled arms and onboard AI for complex task handling, enhancing research and industrial robotics capabilities. Source: www.anybotics.com

• In May 2025, LG Innotek and Boston Dynamics entered a collaboration to develop next-generation robot vision sensing systems that will enhance perception and environmental awareness for robots like Atlas, integrating high-performance RGB and 3D sensing in low-visibility conditions. Source: www.lginnotek.com

The Industrial Quadruped Robots Market Report encompasses an extensive analysis of the robotic technologies that support autonomous legged mobility across asset-intensive industrial sectors. This includes segmentation by robot type (e.g., inspection, logistics, hybrid, surveillance), applications (site inspection, mapping, material handling, security), and end-user industries such as energy, chemicals, mining, manufacturing, and critical infrastructure. Geographic dimensions cover all major regions—North America, Europe, Asia-Pacific, South America, and Middle East & Africa—providing volume-based comparisons of deployment levels, adoption trends, regulatory influences, and operational practices tailored to local industrial frameworks.

Technological scopes explore autonomy systems, perception architectures, battery and power management, mobility mechanisms, and communication networks (including private 5G integration), detailing how these elements influence operational reliability and decision-maker confidence. The report treats software ecosystems—such as fleet management, SLAM navigation, and edge AI control—as central to assessing long-term scalability. It also evaluates emerging subsegments like modular payloads, autonomous docking and charging, and integrated safety systems, offering insight into niche opportunities and innovation pathways.

Industrial contexts such as digital twin integration, predictive maintenance workflows, and ESG-aligned inspection use cases are examined to illuminate cross-segment value creation. The analysis further highlights competitive positioning, patent landscapes, strategic partnerships, and industry standards that shape procurement decisions. With an emphasis on operational metrics, deployment criteria, and regional infrastructure readiness, the report equips business professionals with a granular understanding of current capabilities, future avenues for expansion, and comparative frameworks for strategic investments in industrial quadruped robot solutions.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 2,201.0 Million |

| Market Revenue (2033) | USD 9,980.6 Million |

| CAGR (2026–2033) | 20.8% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Boston Dynamics, Unitree Robotics, Ghost Robotics, ANYbotics, Deep Robotics, Agility Robotics, Clearpath Robotics, Diligent Robotics, Festo, Bionic Robotics, Agility Robotics, Adept MobileRobots, PAL Robotics, Kawasaki Heavy Industries, Honda Motor Co, SEER Robotics, Nex Robotics |

| Customization & Pricing | Available on Request (10% Customization Free) |