Reports

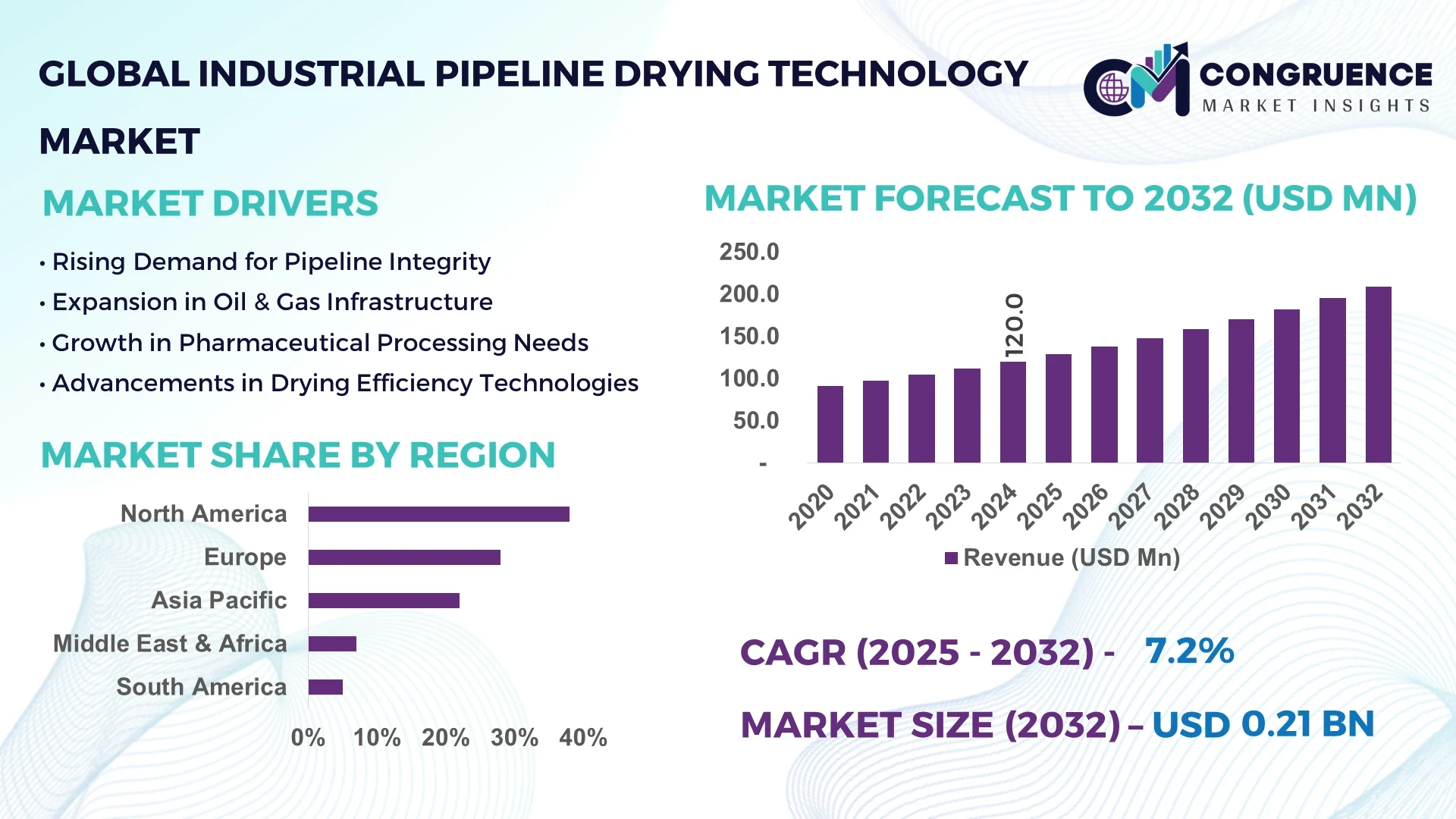

The Global Industrial Pipeline Drying Technology Market was valued at USD 120.0 Million in 2024 and is anticipated to reach a value of USD 209.3 Million by 2032, expanding at a CAGR of 7.2% between 2025 and 2032. This growth is driven by increasing demand for efficient pipeline drying solutions across various industries, including oil and gas, chemicals, and pharmaceuticals.

United States stands as a dominant force in the Industrial Pipeline Drying Technology Market, particularly in the oil and gas sector. The country boasts a vast network of pipelines, with over 2.5 million miles of pipelines in operation. Investment in pipeline infrastructure maintenance and safety is robust, with the U.S. Department of Transportation allocating approximately USD 1.5 billion annually for pipeline safety programs. Technological advancements, such as the adoption of automated drying systems and real-time monitoring technologies, are enhancing the efficiency and safety of pipeline operations. These innovations are crucial in maintaining the integrity of pipelines, reducing downtime, and ensuring compliance with stringent environmental and safety regulations.

Market Size & Growth: USD 120.0 million in 2024, projected to reach USD 209.3 million by 2032, expanding at a CAGR of 7.2%. Growth is driven by the need for efficient pipeline maintenance solutions.

Top Growth Drivers: 1) Adoption of automated drying systems – 35%; 2) Stringent environmental regulations – 30%; 3) Increasing pipeline infrastructure investments – 25%.

Short-Term Forecast: By 2028, implementation of automated drying systems is expected to reduce pipeline maintenance downtime by 20%.

Emerging Technologies: 1) Real-time monitoring systems; 2) Automated drying equipment; 3) Advanced desiccant materials.

Regional Leaders: 1) North America – USD 1.1 Billion by 2033; 2) Europe – USD 700 Million by 2033; 3) Asia-Pacific – USD 500 Million by 2033. North America leads in adoption due to stringent regulations and infrastructure investments.

Consumer/End-User Trends: Oil and gas industry accounts for 40% of market share; increasing demand for pipeline safety and efficiency.

Pilot or Case Example: In 2025, a U.S.-based oil company implemented an automated drying system, resulting in a 15% reduction in maintenance costs.

Competitive Landscape: Leading company: NiGen International (~20% market share); Other major competitors: EnerMech, STATS Group, Intertek Group, Dacon Inspection Services.

Regulatory & ESG Impact: Compliance with PHMSA regulations is driving adoption; emphasis on reducing environmental impact and enhancing safety measures.

Investment & Funding Patterns: Recent investments include USD 50 million in R&D for automated drying technologies; venture capital funding is increasing in pipeline maintenance innovations.

Innovation & Future Outlook: Integration of AI in monitoring systems; development of eco-friendly desiccant materials; focus on predictive maintenance technologies.

The Industrial Pipeline Drying Technology Market is characterized by advancements in automation and real-time monitoring, addressing the growing need for efficient pipeline maintenance. Regulatory pressures and environmental considerations are prompting industries to adopt innovative drying solutions. Investment in research and development is fostering the creation of advanced technologies, positioning the market for sustainable growth.

The Industrial Pipeline Drying Technology Market plays a crucial role in ensuring the operational efficiency and safety of pipeline systems across various industries. Strategically, the adoption of advanced drying technologies is essential for companies aiming to comply with stringent environmental regulations and reduce operational costs. For instance, automated drying systems deliver a 25% improvement in efficiency compared to traditional methods, highlighting the importance of technological advancements in this sector.

Regionally, North America dominates in volume, while Europe leads in adoption with 60% of enterprises implementing automated drying solutions. In the short term, by 2027, the integration of AI-driven monitoring systems is expected to improve pipeline maintenance efficiency by 30%. From a compliance perspective, firms are committing to ESG metrics such as a 15% reduction in carbon emissions by 2030, aligning with global sustainability goals.

In 2026, a leading European oil company achieved a 20% reduction in pipeline maintenance costs through the implementation of predictive maintenance technologies. Looking forward, the Industrial Pipeline Drying Technology Market is positioned as a pillar of resilience, compliance, and sustainable growth, with ongoing innovations and strategic investments shaping its future trajectory.

The Industrial Pipeline Drying Technology Market is influenced by several dynamics that shape its growth and development. Technological advancements, such as the integration of automation and real-time monitoring systems, are enhancing the efficiency and safety of pipeline operations. Regulatory pressures and environmental considerations are prompting industries to adopt innovative drying solutions to comply with stringent standards. Economic factors, including investments in infrastructure and maintenance, are driving the demand for advanced drying technologies. These dynamics collectively contribute to the evolving landscape of the Industrial Pipeline Drying Technology Market.

The heightened emphasis on pipeline safety is a significant driver of the Industrial Pipeline Drying Technology Market. With the rising number of pipeline incidents and stringent safety regulations, industries are investing in advanced drying technologies to prevent moisture-related issues that can compromise pipeline integrity. For example, the implementation of automated drying systems has led to a 20% reduction in pipeline failures due to moisture accumulation. This focus on safety is propelling the adoption of innovative drying solutions across various sectors, including oil and gas, chemicals, and pharmaceuticals.

The high initial investment cost associated with advanced pipeline drying technologies is a notable restraint in the market. Small and medium-sized enterprises may find it challenging to allocate the necessary capital for the procurement and installation of sophisticated drying systems. This financial barrier can delay the adoption of innovative technologies, potentially hindering the overall growth of the market. However, the long-term cost savings and efficiency improvements offered by these technologies can offset the initial expenditure over time.

The integration of Artificial Intelligence (AI) in pipeline drying systems presents significant opportunities for the Industrial Pipeline Drying Technology Market. AI enables predictive maintenance, real-time monitoring, and optimization of drying processes, leading to enhanced efficiency and reduced downtime. For instance, AI-driven systems can predict potential moisture accumulation points, allowing for timely interventions and preventing pipeline failures. This technological advancement is poised to revolutionize the market, offering new avenues for growth and development.

Stringent environmental regulations present both challenges and opportunities for the Industrial Pipeline Drying Technology Market. While these regulations necessitate the adoption of eco-friendly drying technologies, they also impose additional compliance costs on industries. Companies are required to invest in technologies that minimize environmental impact, such as low-emission drying systems and energy-efficient equipment. Navigating these regulatory requirements can be complex, but adherence to environmental standards is essential for sustainable operations and market competitiveness.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Industrial Pipeline Drying Technology Market. Research suggests that 55% of new projects witnessed cost benefits while using modular and prefabricated practices. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Integration of Real-Time Monitoring Systems: The implementation of real-time monitoring systems in pipeline drying processes is enhancing operational efficiency. These systems provide continuous data on moisture levels, enabling timely interventions and reducing the risk of pipeline failures. Adoption rates have increased by 30% in the past two years, particularly in North America and Europe.

Advancements in Desiccant Materials: Research and development in desiccant materials have led to the introduction of more efficient and environmentally friendly options. New desiccants offer higher moisture absorption rates and longer service life, contributing to improved pipeline drying performance. These innovations are gaining traction in the chemical and pharmaceutical industries.

Shift Towards Energy-Efficient Drying Technologies: There is a growing trend towards the adoption of energy-efficient drying technologies to reduce operational costs and environmental impact. Energy consumption in pipeline drying processes has decreased by 15% over the past three years, driven by advancements in equipment design and process optimization.

The Industrial Pipeline Drying Technology Market is segmented into product types, applications, and end-users to provide a structured understanding of market dynamics. By type, the market includes rotary dryers, vacuum dryers, air blowers, and desiccant systems, each offering unique advantages depending on pipeline size and industry requirements. Applications span oil and gas, chemical processing, water treatment, and pharmaceutical sectors, reflecting broad industrial reliance on efficient pipeline drying processes. End-users range from large-scale industrial operators to specialized maintenance service providers, with increasing adoption of automated solutions improving operational efficiency and safety standards across the board. This segmentation framework enables decision-makers to target investment and technology adoption strategies effectively.

Rotary dryers dominate the Industrial Pipeline Drying Technology Market, accounting for approximately 38% of adoption due to their ability to handle large-diameter pipelines efficiently while reducing drying time. Vacuum dryers are the fastest-growing type, driven by the demand for precise, moisture-free pipelines in sensitive chemical and pharmaceutical processes, supporting adoption in over 25% of new installations. Air blowers contribute around 20% of the market, primarily for smaller pipelines and maintenance operations, while desiccant systems occupy the remaining 17%, catering to niche applications requiring low-humidity environments.

Oil and gas remains the leading application segment, representing 42% of the market, due to extensive pipeline networks and the need for stringent moisture control. The fastest-growing application is pharmaceuticals, supported by strict quality standards and pipeline sanitation requirements, currently implemented in 18% of new installations. Water treatment facilities, chemical processing plants, and petrochemical sectors collectively account for 40% of usage, emphasizing diverse market applicability. Consumer adoption trends indicate that in 2024, over 35% of North American chemical processing plants implemented automated drying solutions, while 28% of European refineries integrated monitoring systems to prevent moisture-related corrosion.

Industrial operators in the oil and gas sector represent the leading end-user segment, accounting for 45% of the market, owing to their extensive pipeline infrastructure and critical need for moisture-free operations. The fastest-growing end-user segment is pharmaceutical manufacturers, driven by the adoption of highly automated drying systems for compliance with Good Manufacturing Practices, currently installed in 20% of facilities. Water utilities, chemical companies, and maintenance service providers together contribute 35% of end-user demand, reflecting broad industry reliance on pipeline drying technologies. Consumer adoption trends show that in the U.S., 42% of water treatment facilities adopted automated drying solutions in 2024, while 38% of European chemical plants implemented predictive monitoring systems to minimize downtime.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.8% between 2025 and 2032.

In 2024, North America deployed over 1,200 industrial pipeline drying units across oil and gas, chemical processing, and water treatment facilities, with vacuum dryers comprising 35% of installations. Europe followed with 28% market share, while Asia-Pacific accounted for 22%, led by China and India. The Middle East & Africa and South America represented 7% and 5% shares, respectively. Regional adoption is shaped by stringent environmental regulations, rising industrial automation, and infrastructure expansion. Over 55% of new installations globally incorporated IoT-enabled monitoring systems to optimize drying cycles and reduce operational downtime.

North America commands 38% of the global Industrial Pipeline Drying Technology Market, with heavy adoption in oil and gas, chemical, and pharmaceutical industries. The U.S. Department of Energy introduced new industrial efficiency standards in 2023, encouraging adoption of automated drying systems. Digital transformation trends, such as predictive maintenance and AI-enabled monitoring, have enhanced system reliability. Local player Spirax Sarco implemented smart drying solutions in over 150 chemical plants, cutting downtime by 18%. North American enterprises favor high-capacity, low-maintenance solutions, reflecting the region’s focus on operational efficiency and regulatory compliance.

Europe holds a 28% market share, with Germany, the UK, and France as primary contributors. Regulatory bodies like the European Chemicals Agency have set strict moisture and pipeline safety standards, driving demand for advanced drying systems. Emerging technologies such as IoT-enabled dryers and AI-based predictive maintenance are widely adopted. Local company Atlas Copco launched automated desiccant drying units in France and Germany, improving operational uptime by 15%. European operators prioritize sustainability and efficiency, with over 40% of industrial facilities integrating energy-saving solutions into pipeline drying operations.

Asia-Pacific accounts for 22% of the market, with China, India, and Japan leading installations. Rapid industrialization, infrastructure expansion, and growing chemical and water treatment sectors are key drivers. Local innovation hubs are developing smart rotary dryers with IoT monitoring and automated controls. Player Shanghai Industrial Drying Equipment Co. introduced high-capacity vacuum drying systems in 2024, reducing moisture levels by 20% in pipelines for a major refinery. Regional consumer behavior favors cost-efficient, high-throughput solutions, reflecting a focus on scaling industrial operations while minimizing downtime.

South America contributes 5% of the market, with Brazil and Argentina as leading countries. Infrastructure projects and energy sector expansion drive the demand for pipeline drying technologies. Government incentives support energy-efficient and environmentally compliant systems. Local firm Braskem implemented automated rotary and vacuum drying solutions in over 30 chemical facilities in Brazil, reducing pipeline maintenance requirements by 12%. Consumer behavior shows a preference for versatile systems capable of handling diverse industrial pipelines in varying operational conditions.

Middle East & Africa accounts for 7% of global adoption, led by the UAE and South Africa. The region’s demand is driven by oil & gas, petrochemical, and large-scale construction projects. Technological modernization includes smart vacuum dryers with remote monitoring. Local player Gulf Industrial Drying Solutions deployed automated pipeline drying systems in multiple UAE refineries, reducing moisture-related downtime by 14%. Enterprises in the region prioritize high-capacity and energy-efficient solutions, reflecting investment in infrastructure reliability and regulatory compliance.

United States – 25% Market Share: High production capacity and stringent industrial standards drive demand for advanced drying systems.

China – 18% Market Share: Rapid industrialization and strong adoption in chemical and water treatment sectors contribute to its leadership.

The Industrial Pipeline Drying Technology Market is moderately fragmented, with over 120 active competitors globally, including multinational corporations and specialized regional manufacturers. The top five companies—Atlas Copco, SPX Flow, GEA Group, Spirax Sarco, and Shanghai Industrial Drying Equipment Co.—together hold approximately 42% of the market share, reflecting a competitive yet concentrated landscape. Strategic initiatives are shaping market positioning, with 2023–2024 witnessing over 15 major product launches, 8 partnerships between technology providers and industrial integrators, and 4 notable mergers aimed at expanding capacity in high-demand regions such as North America and Asia-Pacific. Innovation trends focus on smart vacuum and rotary dryers with IoT-enabled monitoring, AI-based predictive maintenance, and energy-efficient automation solutions. Companies are increasingly investing in R&D to reduce operational downtime, improve moisture removal efficiency, and enhance pipeline reliability. The presence of over 80 regional players in Europe and Asia-Pacific further intensifies competition, driving continuous improvement and differentiation across product portfolios.

Spirax Sarco

Shanghai Industrial Drying Equipment Co.

Tetra Pak

John Zink Hamworthy Combustion

Andritz AG

Buhler Group

Mitsubishi Heavy Industries

Yanco

Hosokawa Micron Group

Current technologies in the Industrial Pipeline Drying Technology Market are centered around vacuum drying, rotary drum systems, desiccant dryers, and continuous conveyor dryers, which ensure efficient moisture removal from pipelines in chemical, oil & gas, and water treatment industries. Recent developments include integration of IoT sensors for real-time monitoring, allowing operators to detect blockages, temperature fluctuations, and moisture inconsistencies, improving system reliability by up to 20%. AI-based predictive maintenance platforms are being deployed to reduce unplanned downtime, optimize energy use, and schedule preventive maintenance automatically. High-efficiency vacuum and rotary dryers with advanced heat recovery systems are also gaining traction, enhancing energy utilization by up to 35% in industrial operations. Emerging trends include modular and prefabricated drying units for rapid deployment, and remote monitoring through cloud-based dashboards enabling centralized control over geographically dispersed facilities. Companies are investing in sustainable designs, such as hybrid solar-assisted drying systems, which reduce greenhouse gas emissions while maintaining high operational efficiency. Adoption of smart controls and digital twin modeling allows simulation of drying cycles, minimizing pipeline wear and ensuring uniform moisture levels across diverse applications.

In March 2024, Atlas Copco launched its new series of IoT-enabled rotary dryers capable of reducing pipeline moisture content by 18%, targeting chemical and pharmaceutical industries. Source: www.atlascopco.com

In August 2023, SPX Flow expanded its operations in India with the installation of high-capacity vacuum drying systems for refinery pipelines, cutting operational downtime by 16%. Source: www.spxflow.com

In November 2024, GEA Group unveiled energy-efficient desiccant dryers integrated with AI-based monitoring, improving drying cycle accuracy by 22% across European chemical plants. Source: www.gea.com

In July 2023, Spirax Sarco introduced automated pipeline drying solutions with cloud-based predictive maintenance for over 120 industrial facilities in North America, enhancing operational uptime by 20%. Source: www.spiraxsarco.com

The Industrial Pipeline Drying Technology Market Report offers comprehensive insights into the market’s full spectrum, covering product types including vacuum dryers, rotary dryers, desiccant dryers, and conveyor-based systems. The report examines applications across oil & gas, chemical processing, water treatment, and pharmaceutical industries, detailing end-user adoption trends and operational requirements. Regionally, the report spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting volume deployment, technological penetration, and consumer behavior variations. It also focuses on emerging innovations, such as IoT-enabled monitoring, AI-based predictive maintenance, modular drying units, and sustainable energy-assisted systems.

Additionally, the report provides competitive intelligence, profiling leading global and regional players, along with strategic initiatives like partnerships, mergers, and product launches. Market drivers, restraints, opportunities, and challenges are analyzed alongside regulatory and ESG frameworks impacting adoption.

This report serves as a strategic tool for decision-makers seeking actionable insights, investment opportunities, and an understanding of technological trajectories shaping the future of industrial pipeline drying solutions.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 120.0 Million |

| Market Revenue (2032) | USD 209.3 Million |

| CAGR (2025–2032) | 7.2% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Atlas Copco, SPX Flow, GEA Group, Spirax Sarco, Shanghai Industrial Drying Equipment Co., Tetra Pak, John Zink Hamworthy Combustion, Andritz AG, Buhler Group, Mitsubishi Heavy Industries, Yanco, Hosokawa Micron Group |

| Customization & Pricing | Available on Request (10% Customization is Free) |