Reports

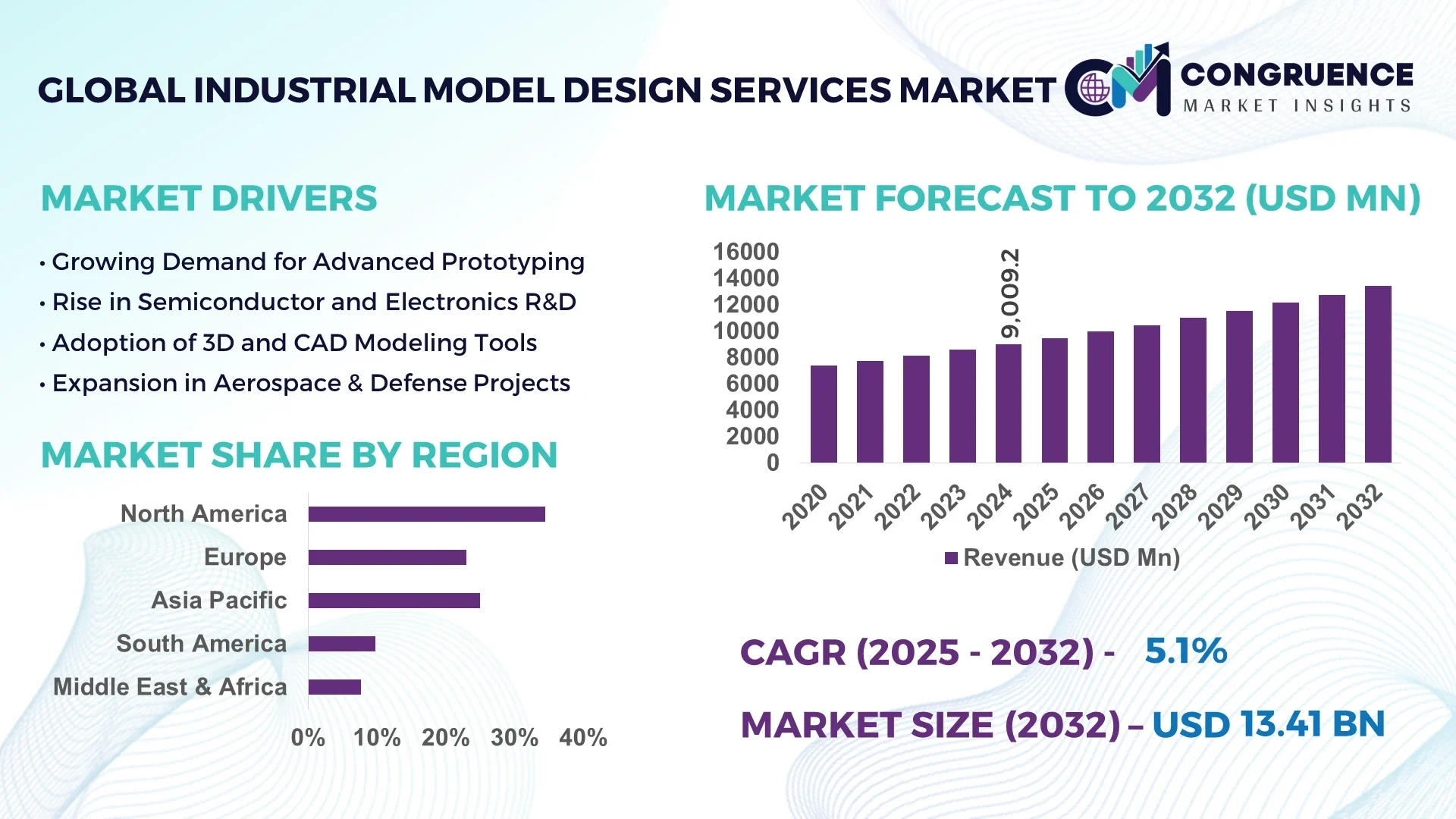

The Global Industrial Model Design Services Market was valued at USD 9009.17 Million in 2024 and is anticipated to reach a value of USD 13412.4 Million by 2032 expanding at a CAGR of 5.1% between 2025 and 2032.

Germany remains a pivotal hub for the Industrial Model Design Services Market, boasting advanced manufacturing infrastructure, high R&D investment in mechanical prototyping, and strong integration of smart modeling systems across industrial automation, transportation, and energy sectors.

The Industrial Model Design Services Market is experiencing substantial growth, driven by rising demand from sectors like automotive, aerospace, energy, heavy engineering, and smart manufacturing. The adoption of 3D visualization, digital twin technology, and precision engineering tools is accelerating innovation in industrial model prototyping. Regulatory shifts encouraging low-waste design methods and eco-efficient industrial solutions are fueling further innovation. With an increasing emphasis on real-time collaboration tools, design validation accuracy, and simulation-based performance testing, businesses are leaning toward external design service providers for faster turnaround and scalability. Regional consumption is particularly robust in East Asia and Western Europe, supported by manufacturing digitization and supportive industrial policies. Moreover, the expanding use of virtual reality (VR) and augmented reality (AR) in design walkthroughs is emerging as a key trend. Going forward, increased investments in smart factories and intelligent model customization are set to redefine the future outlook of the Industrial Model Design Services Market globally.

Artificial Intelligence is playing a transformative role in redefining operational efficiencies and design precision in the Industrial Model Design Services Market. By integrating AI-driven software into the design process, service providers are achieving enhanced accuracy, reduced prototyping time, and optimized resource allocation. AI-powered generative design algorithms enable engineers to produce highly optimized industrial models that meet structural and functional criteria while reducing material usage. These advanced design simulations help eliminate traditional trial-and-error iterations, saving both time and operational costs.

Furthermore, machine learning is increasingly used to analyze historical design data, enabling predictive modeling and automated error detection in CAD files. This reduces design revisions and minimizes production delays. In the Industrial Model Design Services Market, AI also aids in real-time collaboration by synchronizing multi-disciplinary inputs from geographically dispersed teams, ensuring uniformity in project execution. As industrial clients demand faster go-to-market timelines, AI enhances scalability by auto-adjusting designs based on customized project specifications.

AI applications are also advancing robotics integration within model testing processes, streamlining stress testing and performance evaluation without extensive human intervention. These changes have improved productivity by nearly 30% in some large-scale industrial model design projects. With smart algorithms learning from every design cycle, the Industrial Model Design Services Market is entering a new phase of intelligent design automation—maximizing quality while minimizing overheads.

“In March 2024, a leading German design engineering firm integrated an AI-based parametric modeling engine that reduced design cycle times by 42%, significantly accelerating model prototyping for industrial robotics and turbine components.”

The Industrial Model Design Services Market is undergoing a dynamic transformation, shaped by technological innovations, shifting industrial standards, and evolving consumer expectations across various sectors. Increased demand for rapid industrial prototyping, enhanced product visualization, and streamlined engineering workflows is significantly influencing the growth trajectory. Market players are leveraging advanced simulation tools, AI-based design optimization, and digital twin technology to deliver high-precision outputs for applications in aerospace, automotive, heavy machinery, and energy. Industry 4.0 adoption is intensifying the need for integrated design services, while regional diversification in manufacturing hubs is broadening the client base. Additionally, customized design solutions and flexible prototyping models are helping service providers gain competitive advantages. Regulatory focus on sustainable manufacturing, reduced design-to-production timelines, and higher production efficiency is further accelerating market development.

Growing investment in smart manufacturing is significantly fueling the Industrial Model Design Services Market. As industries transition toward automation and digital transformation, there is an increased demand for advanced industrial models that align with sensor-based machinery, robotics, and IoT-integrated environments. In 2024, over 40% of Tier 1 manufacturers globally initiated smart factory upgrades, many of which required high-fidelity design services for machinery, layouts, and workflows. Digital twins and AI-assisted simulations are being deployed at scale to reduce downtime and predict machine behaviors. These advancements directly contribute to higher demand for external model design experts who can deliver precise and modular solutions tailored to evolving smart infrastructure.

One of the key restraints impacting the Industrial Model Design Services Market is the high cost associated with integrating and maintaining advanced design tools and technologies. Many mid-sized design firms struggle with the financial burden of licensing premium CAD/CAM software, deploying AI modules, and training personnel in emerging technologies. Additionally, adopting digital twin platforms or real-time rendering engines often demands substantial upfront investments, which can limit accessibility for smaller players. This cost barrier is particularly significant in developing economies where budgets for engineering services remain tight. As a result, potential clients may delay or limit the scope of outsourcing, slowing overall market expansion.

The increasing industrialization in emerging economies such as India, Brazil, and Vietnam is creating new opportunities for the Industrial Model Design Services Market. As manufacturers in these regions adopt automation and expand production capabilities, there is a growing requirement for custom-designed equipment, layout modeling, and virtual testing. Government incentives aimed at boosting local manufacturing further support this trend. For example, India’s “Make in India” initiative has spurred the creation of thousands of new industrial units that rely heavily on design services for machinery and infrastructure development. This demand offers service providers the opportunity to expand operations and build long-term client relationships in high-growth regions.

A critical challenge facing the Industrial Model Design Services Market is the shortage of skilled professionals proficient in digital design, simulation, and AI-driven modeling tools. As the market shifts toward intelligent design frameworks and high-precision outputs, the talent gap in using advanced design platforms like SolidWorks, CATIA, and generative design engines becomes a bottleneck. In many regions, vocational and engineering education systems lag behind industry needs, limiting the availability of ready-to-deploy talent. Consequently, firms must invest heavily in training, recruitment, and retention strategies to meet project demands, which adds pressure on margins and extends project timelines.

Rise in Modular and Prefabricated Construction Modular and prefabricated construction is rapidly influencing demand in the Industrial Model Design Services market. Across North America and Western Europe, prefabrication methods now account for over 20% of all new industrial construction. Designers are increasingly required to create ultra-precise digital models that ensure compatibility with pre-manufactured elements. Automated fabrication systems demand exact model specifications, increasing reliance on model design firms equipped with 3D visualization and parametric modeling capabilities. The shift has also reduced on-site labor by up to 30%, boosting project efficiency and contractor adoption of external design services.

Integration of Digital Twin Technology in Engineering Models Digital twin adoption has grown significantly within industrial modeling, especially in sectors like energy and heavy machinery. In 2024, over 35% of European-based model design projects integrated real-time digital twins for continuous asset monitoring and simulation-based optimization. This approach allows clients to run failure scenario testing, monitor performance degradation, and perform predictive maintenance directly from the initial model. Industrial model design firms are now tailoring services to include embedded sensors and IoT features within their blueprints to meet this advanced requirement.

Customization-Driven Demand in Heavy Equipment Design There is a rising need for customized industrial model solutions, particularly in the heavy equipment and process manufacturing sectors. Over 60% of design requests in 2024 required high-complexity customizations involving load simulations, material optimization, or ergonomic compliance. This trend has fueled investment in AI-integrated modeling platforms that can automatically generate bespoke layouts based on client-supplied variables. As a result, design services now deliver personalized models faster while meeting higher standards of mechanical integrity and safety compliance.

Increased Use of Cloud-Based Collaboration Tools The shift to remote and hybrid work models has driven the Industrial Model Design Services market toward cloud-based platforms. Over 50% of collaborative design projects in 2024 used cloud-based CAD and PLM systems to facilitate real-time coordination across geographically distributed teams. This has significantly improved feedback loops, reduced communication gaps, and cut design cycle times by as much as 25%. Service providers are increasingly offering integrated cloud access as a core part of their design packages to remain competitive and agile in global project execution.

The Industrial Model Design Services market is segmented into three primary categories: by type, by application, and by end-user. These segments reflect the diverse range of service offerings, usage demands, and customer profiles across industries. In terms of type, the market includes 3D modeling, virtual prototyping, simulation modeling, CAD-based design, and physical model production. Applications range from equipment layout planning and factory infrastructure to robotics integration and structural testing. Key end-users span automotive manufacturers, aerospace companies, energy plants, heavy engineering firms, and construction contractors. Each segment presents unique drivers—such as speed, precision, or customization—that shape design expectations and service delivery. This segmentation enables stakeholders to identify specific areas of investment and operational focus aligned with evolving market requirements.

Among the various types, 3D modeling dominates the Industrial Model Design Services market due to its widespread use in machinery design, layout planning, and visualization. It enables real-time rendering and modifications, which supports iterative development processes for complex projects. The fastest-growing type is simulation modeling, driven by the rise in predictive engineering and demand for real-world scenario testing without physical prototypes. Simulation-based services are particularly gaining traction in aerospace and automotive segments for stress analysis and material performance forecasting. CAD-based design remains a fundamental component, especially in legacy industrial systems requiring standardized documentation. Meanwhile, virtual prototyping is gaining popularity in early-stage concept development phases, helping companies evaluate feasibility before committing to large-scale manufacturing. Physical model production, though less prevalent, retains niche importance in academic, architectural, and high-detail presentations, where tactile representations are necessary for stakeholder approvals or exhibitions.

Equipment layout design leads all application segments in the Industrial Model Design Services market, as manufacturers continually upgrade or reconfigure production lines for efficiency. Clients prioritize space optimization, utility integration, and operational flow accuracy—needs best addressed through detailed model designs. The fastest-growing application is robotic integration modeling, as industries automate assembly, inspection, and packaging processes. Growth in robotics usage demands precise, sensor-compatible model planning that synchronizes with movement patterns and safety zones. Structural analysis modeling is also expanding, particularly in construction and civil engineering sectors, where digital models simulate building performance under various conditions. Additionally, process flow simulation is growing steadily among chemical and food processing industries seeking to optimize throughput and reduce waste. All these applications point to a future where industrial design is increasingly data-driven and functionality-focused.

Automotive manufacturers represent the leading end-user segment in the Industrial Model Design Services market, consistently demanding high-detail modeling for assembly lines, testing facilities, and advanced machinery. Their focus on continuous innovation, lean manufacturing, and safety compliance sustains high-volume design needs. The fastest-growing end-user is the energy and utilities sector, especially renewable energy companies requiring complex modeling for turbines, solar installations, and smart grids. Their projects often need structural modeling integrated with environmental simulation and maintenance planning tools. Aerospace and defense also remain critical, demanding ultra-high precision in component prototyping and stress simulation. Meanwhile, heavy engineering firms and construction contractors leverage design services for machinery setup, site planning, and structural safety validation. These varied end-users collectively drive the market toward higher accuracy, speed, and customization in industrial modeling solutions.

North America accounted for the largest market share at 34.5% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2025 and 2032.

The Industrial Model Design Services Market is expanding across all major regions due to the rising complexity of industrial infrastructure, increasing demand for digital design workflows, and global adoption of automation. North America's dominance is fueled by mature industrial bases and high investment in digital transformation. Meanwhile, Asia-Pacific’s acceleration is attributed to its large-scale manufacturing growth and significant government-backed industrial modernization programs. Europe remains a robust player, influenced by sustainability mandates and advanced simulation technologies, while South America and the Middle East & Africa are catching up, driven by energy and infrastructure initiatives. As regional manufacturing policies evolve and smart technologies spread, region-specific demand for tailored industrial model design solutions is growing rapidly.

Digitalization and Advanced Prototyping Driving Strong Demand

In this region, the Industrial Model Design Services Market accounted for 34.5% of global share in 2024, with substantial demand led by the automotive, aerospace, and energy sectors. U.S. and Canadian companies are increasingly adopting digital twin systems and simulation-based design services for machinery upgrades and smart factory setups. A key contributing factor is regulatory support for energy-efficient infrastructure, such as the Infrastructure Investment and Jobs Act in the U.S. which encourages tech-led industrial development. Significant strides in cloud-based collaboration tools and AI-powered modeling are further enhancing the productivity and precision of industrial design services, creating robust opportunities for design providers.

Eco-Compliance and Simulation Technologies Reshaping Market Dynamics

The Industrial Model Design Services Market in this region held approximately 27.8% of global share in 2024, driven by strong demand from Germany, France, and the United Kingdom. The European Commission’s focus on carbon-neutral manufacturing is compelling industries to redesign processes using sustainable digital models. Countries such as Germany lead in precision manufacturing, leveraging simulation modeling for engineering excellence. UK-based firms are investing in AI-powered design software to improve production agility. High compliance standards under initiatives like Fit for 55 and the Digital Europe Programme are encouraging deeper integration of design services into industrial development, especially in advanced machinery and green energy segments.

Manufacturing Expansion and Smart Technology Integration Boost Growth

This region ranked as the fastest-growing in the Industrial Model Design Services Market in 2024, driven by high industrial output in China, India, and Japan. China remains the leading consumer, owing to its vast manufacturing base and smart factory upgrades. India is emerging as a strategic hub, supported by infrastructure modernization and the Make in India initiative. Japan’s focus on robotics and precision engineering further elevates demand for advanced model design services. Smart city projects and investments in digital infrastructure are pushing rapid innovation, particularly in 3D simulation, virtual prototyping, and IoT-integrated design processes that align with evolving industrial expectations.

Infrastructure and Energy Sectors Fueling Demand Surge

In this region, the Industrial Model Design Services Market is steadily gaining traction, led by Brazil and Argentina, which together accounted for over 9.3% of regional demand in 2024. These countries are experiencing rapid infrastructure growth, with large-scale industrial zones and renewable energy projects driving the need for advanced design services. Brazil’s growing wind and solar energy projects require precision layout and system modeling, while Argentina’s industrial recovery is increasing demand for machinery and structural design. Recent trade reforms and incentives for industrial automation have supported the adoption of digital engineering and 3D visualization tools among local firms and contractors.

Oil & Gas Modernization and Smart Infrastructure Shaping Market Trends

Demand for Industrial Model Design Services in this region is being shaped by industrial diversification in UAE and South Africa. The region accounted for 6.5% of global demand in 2024, fueled by infrastructure upgrades and oil & gas facility modernization. The UAE’s Vision 2030 is accelerating digitalization in industrial planning, boosting adoption of high-precision design solutions. South Africa is witnessing growth in utility and energy-related industrial zones, where customized design models are critical. Regional trade pacts and public-private partnerships are enhancing the accessibility of advanced technologies such as CAD/CAM and simulation modeling across key sectors like construction, petrochemicals, and mining.

United States – 28.2% market share

High production capacity, advanced digital engineering capabilities, and heavy investment in smart manufacturing solutions drive its leading position in the Industrial Model Design Services Market.

China – 22.6% market share

Dominance stems from massive manufacturing activity, rapid infrastructure expansion, and widespread adoption of automation in industrial operations, boosting consistent demand for industrial model design solutions.

The Industrial Model Design Services market is marked by a moderately fragmented but highly competitive landscape, comprising over 120 active firms globally. These include established engineering consultancies, specialized design service providers, and new entrants leveraging digital technologies. Market leaders are focusing on expanding service capabilities through strategic partnerships, such as collaborations with AI software developers and industrial hardware manufacturers. Several companies have launched integrated platforms combining CAD, simulation, and virtual prototyping features to offer end-to-end model design solutions.

Notable competitive trends include the rapid adoption of AI-enhanced modeling tools, cloud-based collaborative design environments, and increased focus on sustainability-driven solutions. Firms are investing in regional expansion strategies to tap into high-growth areas like Southeast Asia and Eastern Europe. Mergers and acquisitions have also intensified, particularly among mid-tier players aiming to broaden service portfolios and strengthen global delivery networks. Additionally, top-tier companies are introducing modular design services for smart factories and renewable energy infrastructure, responding to sector-specific demand shifts. Innovation in digital twin technology and real-time simulation services continues to be a key differentiator, pushing competitors to invest in R&D and staff training to stay ahead.

Altair Engineering Inc.

Autodesk Inc.

Dassault Systèmes SE

PTC Inc.

AVEVA Group plc

Bentley Systems, Incorporated

Intergraph Corporation

HCL Technologies Ltd.

Foster + Partners

Tata Elxsi Ltd.

Arup Group

WSP Global Inc.

Jacobs Engineering Group Inc.

Buro Happold

ZWSOFT Co., Ltd.

The Industrial Model Design Services market is increasingly shaped by the rapid integration of digital technologies that enhance speed, precision, and customization in industrial design workflows. A key technological enabler is digital twin technology, which allows real-time synchronization between physical industrial systems and their virtual counterparts. This facilitates predictive maintenance, operational testing, and performance optimization directly from the design phase. As of 2024, over 35% of industrial design projects in developed markets incorporate digital twin capabilities.

AI-powered generative design is another transformative innovation gaining traction. These tools can generate multiple high-performance design variants based on specific engineering constraints, significantly reducing development cycles. In parallel, cloud-based CAD and PLM systems are enabling real-time collaboration among geographically distributed design teams, resulting in up to 25% reduction in design timelines for large-scale industrial modeling projects.

3D printing and rapid prototyping technologies are further enhancing the ability to create functional prototypes with intricate geometries. These systems are increasingly used in sectors like aerospace and heavy machinery to validate concepts prior to full-scale production. Additionally, immersive technologies such as augmented reality (AR) and virtual reality (VR) are being deployed for design validation, walk-through simulations, and client presentations. These tools are improving stakeholder engagement and reducing costly post-production changes. Overall, the convergence of AI, simulation, cloud, and immersive technologies is driving a new era of high-efficiency, smart industrial design services.

• In February 2024, Dassault Systèmes partnered with a global aerospace manufacturer to implement AI-based generative design tools that cut prototype design cycles by 40%, accelerating jet engine model development timelines significantly.

• In October 2023, Tata Elxsi launched an advanced simulation suite for industrial robotics modeling, enabling end-users to validate robotic path planning and mechanical interactions in virtual environments before deployment.

• In May 2024, Autodesk expanded its Fusion platform with a cloud-integrated PLM module, allowing engineering teams to collaborate on industrial model designs across continents with seamless version control and access to real-time feedback.

• In July 2023, Arup Group introduced a new structural modeling framework using immersive VR walkthroughs for industrial plant design, enhancing client decision-making accuracy and reducing design revisions by 22% during early project phases.

The Industrial Model Design Services Market Report provides a comprehensive evaluation of the industry’s global footprint, covering a broad spectrum of technologies, end-user industries, and service applications. The report analyzes design service types such as 3D modeling, CAD-based drafting, simulation modeling, virtual prototyping, and digital twin development. These offerings cater to industries including automotive, aerospace, energy, heavy machinery, construction, and smart infrastructure.

Geographically, the study spans major markets including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. It provides a comparative analysis of regional service adoption patterns, technological maturity, and industrial investment trends. Emphasis is placed on high-growth countries like the United States, China, Germany, and India, which are driving demand through manufacturing innovation and digital transformation.

The report further investigates critical application areas like robotic integration design, structural simulation, equipment layout planning, and process flow optimization. It also includes insights into market dynamics driven by automation, sustainability goals, and AI adoption. Additionally, the scope includes evaluation of niche segments such as immersive model validation, cloud collaboration tools, and sustainability-compliant industrial designs. This coverage equips business leaders with data-driven insights necessary for strategic planning, investment assessment, and competitive benchmarking within the evolving industrial model design landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 9009.17 Million |

|

Market Revenue in 2032 |

USD 13412.4 Million |

|

CAGR (2025 - 2032) |

5.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Veeco Instruments Inc., AIXTRON SE, Tokyo Electron Limited, AMEC (Advanced Micro-Fabrication Equipment Inc.), Riber S.A., NuFlare Technology Inc., Taiyo Nippon Sanso Corporation, II-VI Incorporated, LayTec AG, IntelliEPI (Intelligent Epitaxy Technology Inc.), IQE plc, GlobalWafers Co., Ltd., Sumitomo Electric Industries, Ltd., Siltronic AG |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |