Reports

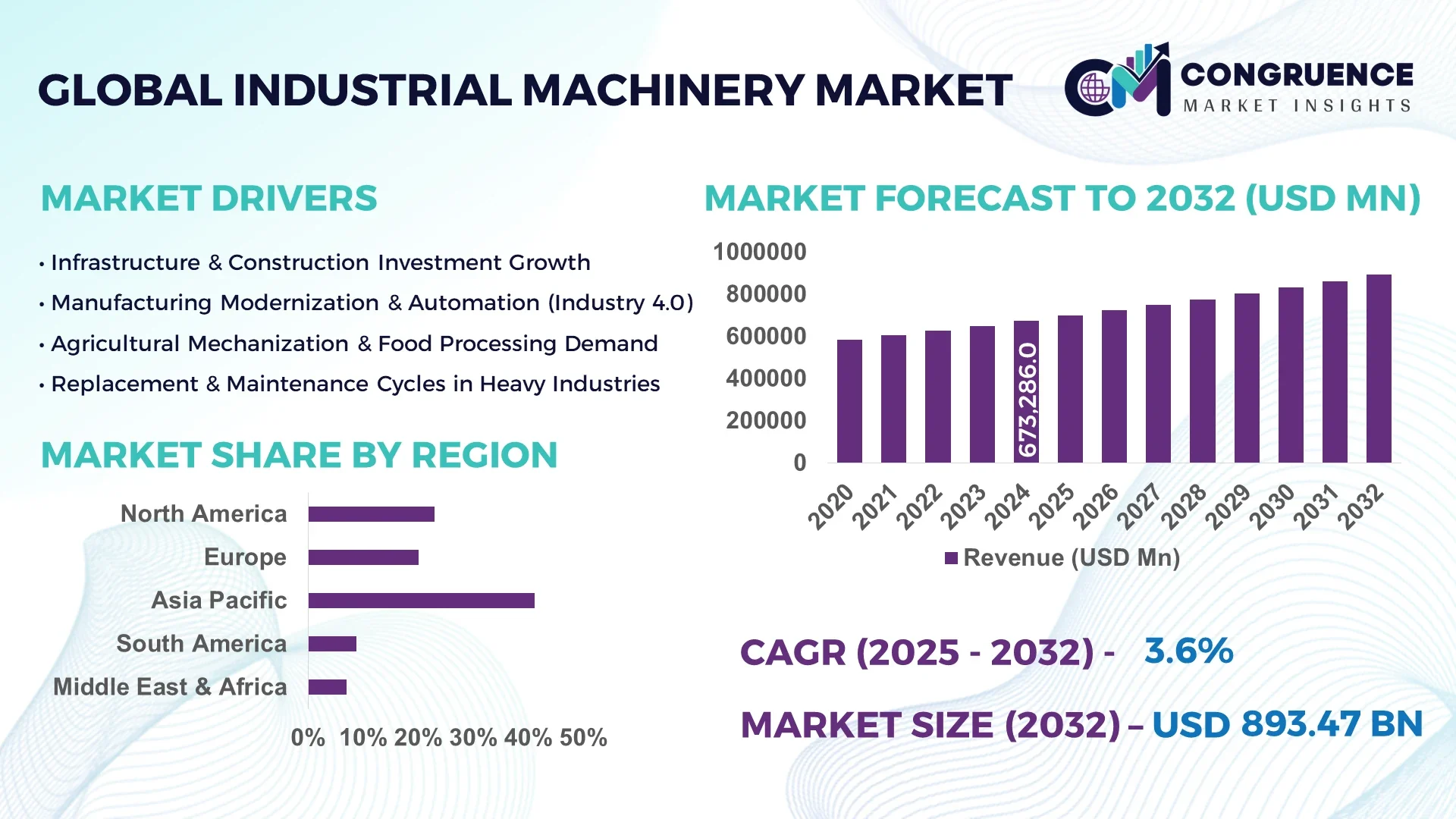

The Global Industrial Machinery Market was valued at USD 673,286.04 Million in 2024 and is anticipated to reach a value of USD 893,465.22 Million by 2032 expanding at a CAGR of 3.6% between 2025 and 2032.

Germany stands as the dominant country in this sector, driven by its robust manufacturing infrastructure, consistent investments in precision engineering, and a high volume of automation-enabled machinery production. Germany’s industrial ecosystem thrives on advanced robotics applications, additive manufacturing capabilities, and exports of high-performance systems for automotive and aerospace segments.

The Industrial Machinery Market encompasses a wide range of sectors including construction, agriculture, mining, oil & gas, packaging, and heavy electrical machinery. A key contributor is the rise in demand for automated and energy-efficient machinery systems in both developed and emerging economies. Technological innovations such as robotic welding systems, CNC-controlled machining centers, and IoT-integrated monitoring systems are reshaping production facilities and driving productivity. Regulatory shifts around emission control and energy consumption are accelerating the shift toward cleaner, smarter machinery. Asia-Pacific shows strong consumption growth, led by increased infrastructure spending and industrialization. North America and Europe continue to innovate through R&D, particularly in sustainable manufacturing technologies. Looking forward, the integration of smart controls, remote diagnostics, and predictive maintenance will play a pivotal role in shaping the market’s trajectory.

Artificial Intelligence is revolutionizing the Industrial Machinery Market by unlocking significant advancements in operational intelligence, predictive maintenance, and smart automation. Through real-time data analytics, AI enables manufacturers to optimize machine performance, reduce unplanned downtime, and lower maintenance costs. In high-volume production environments, AI-powered systems continuously learn from machine behavior, enabling condition-based maintenance strategies that enhance overall equipment effectiveness (OEE). These systems not only predict potential failures but also recommend corrective actions, improving both machinery life cycle and output quality.

Advanced robotics, powered by AI algorithms, are now handling tasks that require high precision, consistency, and speed. These smart machines are extensively used in assembly lines, welding stations, and packaging units where human error can be costly. Moreover, AI-driven vision systems are enabling automated quality control with remarkable accuracy, reducing waste and enhancing compliance with industrial standards. Integration with ERP and MES platforms also ensures seamless decision-making and supply chain coordination. In the Industrial Machinery Market, AI’s impact extends across asset management, real-time diagnostics, production forecasting, and workflow optimization—making it indispensable for future-ready manufacturing operations.

"In 2024, a major industrial machinery manufacturer deployed an AI-powered predictive maintenance system across 1,200 CNC machines, resulting in a 28% reduction in machine downtime and a 15% increase in throughput within six months."

The Industrial Machinery Market is undergoing a significant transformation, driven by digital innovation, automation, and increasing global demand for precision-engineered equipment. As industries prioritize efficiency, safety, and sustainability, the demand for smart, integrated machinery solutions has accelerated. Major sectors including automotive, aerospace, construction, and energy are leveraging advanced machinery to enhance productivity and reduce operational downtime. Regional shifts in production hubs, particularly in Asia-Pacific, are influencing global supply chains. Moreover, the trend toward modular, flexible manufacturing lines is fostering the adoption of multi-functional machinery. Digital twins, remote diagnostics, and predictive analytics are further contributing to a dynamic and competitive market environment, compelling manufacturers to innovate continuously.

Automation is a major driver propelling growth in the Industrial Machinery Market, particularly in high-precision and large-scale manufacturing sectors. Companies are increasingly adopting robotics and AI-powered systems to streamline production, reduce human error, and maintain consistent quality across operations. For example, industrial robots used in metal fabrication, automotive assembly, and electronics manufacturing have witnessed significant upticks, with global robotic installations exceeding 550,000 units in 2024 alone. This shift toward automated machinery reduces reliance on manual labor, increases throughput, and optimizes resource utilization. Additionally, integration of real-time data analytics and programmable logic controllers (PLCs) ensures greater control over complex industrial operations, further accelerating market adoption.

One of the key restraints in the Industrial Machinery Market is the substantial upfront investment required for advanced machinery and the ongoing maintenance costs associated with its operation. High-precision CNC machines, robotic systems, and automated packaging equipment demand significant financial commitment from manufacturers, especially small and mid-sized enterprises (SMEs). Furthermore, specialized training and skilled personnel are often required for equipment operation and troubleshooting, adding to operational expenses. The cost of regular upgrades and compliance with evolving safety and environmental standards compounds the financial burden. These challenges can delay equipment modernization and reduce adoption rates in cost-sensitive markets, particularly in developing regions.

The rapid expansion of Industry 4.0 and the emergence of smart factories present significant growth opportunities in the Industrial Machinery Market. Smart manufacturing environments utilize interconnected machinery, IoT sensors, and AI-based systems to create highly responsive and adaptive production lines. This digital ecosystem enhances real-time decision-making, improves asset management, and enables mass customization. Global investments in smart factory infrastructure are on the rise, with countries such as China, the U.S., and South Korea leading the charge in automation and digital twin technologies. The need for intelligent machinery capable of communicating across systems and adjusting parameters autonomously is opening new demand verticals in diverse industrial domains.

A persistent challenge in the Industrial Machinery Market is the integration of modern technologies with existing legacy systems. Many industries operate on outdated equipment that lacks compatibility with advanced digital platforms such as cloud computing, AI, or industrial IoT. Retrofitting legacy machinery for data communication, predictive analytics, or remote monitoring requires complex and costly customizations. This compatibility gap can result in inefficiencies, increased downtime, and limited scalability. Additionally, cybersecurity risks associated with connecting older equipment to digital networks create concerns around data protection and operational continuity. Overcoming these integration hurdles remains critical for organizations aiming to fully capitalize on smart manufacturing advancements.

• Rise in Modular and Prefabricated Construction: The adoption of modular and prefabricated construction methods is reshaping demand dynamics in the Industrial Machinery Market. Automated cutting, bending, and welding machines are being widely used to prepare components off-site, particularly in North America and Europe where construction timelines are compressed, and labor costs are high. In 2024, over 18% of mid-rise residential buildings in the U.S. incorporated prefabricated modules, driving significant demand for CNC cutting and robotic assembly systems. This trend is pushing manufacturers to offer machinery that ensures dimensional precision and supports standardized output formats for large-scale deployments.

• Growth of Predictive Maintenance and Remote Diagnostics: Industrial machinery providers are increasingly integrating AI and IoT-enabled sensors to offer predictive maintenance and remote diagnostics features. In 2024, over 37% of newly installed heavy machinery came equipped with real-time monitoring systems that collect operational data and provide failure forecasts. These systems allow operators to minimize unplanned downtime and reduce repair costs. Demand for embedded telemetry units and cloud-based analytics platforms is rising rapidly across Asia-Pacific, particularly in industrial parks and large manufacturing hubs.

• Surge in Electric and Hybrid Machinery Demand: Driven by environmental compliance regulations and sustainability goals, the market is witnessing a surge in demand for electric and hybrid industrial machinery. This shift is prominent in sectors such as construction and logistics, where zero-emission equipment is becoming mandatory in certain jurisdictions. In 2024, electric-powered hydraulic lifts and compact loaders accounted for nearly 22% of all new purchases in urban construction zones. Manufacturers are redesigning traditional diesel-based systems to accommodate electric drivetrains without compromising performance or durability.

• Adoption of Human-Robot Collaboration (Cobots): The integration of collaborative robots, or cobots, is transforming production environments by enabling safe and flexible human-machine interaction. These systems are widely used in light assembly, packaging, and quality control applications, especially in electronics and food processing industries. As of mid-2024, cobots accounted for 11% of all industrial robot installations globally. Their affordability, ease of programming, and enhanced safety features make them ideal for small and mid-sized enterprises seeking automation without full-scale robotics deployment.

The Industrial Machinery Market is segmented by type, application, and end-user, reflecting its expansive and multifaceted nature. Product type segmentation includes various machinery systems such as machining centers, material handling equipment, packaging systems, and construction machinery, each serving distinct industrial functions. Application-based segmentation highlights the deployment of machinery across sectors like automotive, aerospace, agriculture, mining, and energy, with each demanding varying degrees of automation and specialization. End-user segmentation shows how different business verticals—from large industrial manufacturers to mid-sized OEMs—utilize machinery to enhance operational efficiency, safety, and output. Emerging trends such as smart manufacturing, sustainability mandates, and the shift toward modular systems are reshaping how stakeholders across segments select and invest in machinery.

The Industrial Machinery Market comprises several key product types, including material handling equipment, construction machinery, packaging machinery, machine tools, and robotic systems. Among these, construction machinery leads the segment due to ongoing infrastructure development and increasing demand for earthmoving and lifting equipment. Urbanization and smart city initiatives have made heavy-duty cranes, excavators, and loaders integral to major construction projects. The fastest-growing type is robotic systems, which are increasingly used in precision manufacturing, especially in automotive and electronics industries. Their ability to perform repetitive tasks with high accuracy and reduced labor intervention has driven rapid adoption. Machine tools remain a critical category, offering high versatility in metalworking and fabrication processes. Packaging machinery continues to gain ground in the food and beverage sector, driven by product diversity and regulatory packaging standards. Meanwhile, material handling systems like conveyors and palletizers play a crucial supporting role in warehouse automation and logistics efficiency.

Industrial machinery serves a broad range of applications, with the automotive sector accounting for the largest share. This is driven by the need for precision assembly, welding, and quality control systems in vehicle manufacturing. In 2024, the sector witnessed increased integration of robotic assembly lines and automated painting systems. The fastest-growing application is within renewable energy manufacturing, particularly for solar panel and wind turbine production. The global push toward cleaner energy sources has resulted in higher demand for machinery that supports component fabrication and installation. Aerospace applications remain essential, with high-precision machinery used in parts manufacturing and testing. The food processing sector also shows steady demand for automated slicing, packaging, and sanitation machinery, addressing the need for hygiene and speed. Mining and agriculture applications rely on durable, high-capacity machines designed for extreme environments and heavy loads, forming a stable yet niche part of the application spectrum.

Large manufacturing enterprises dominate the end-user landscape of the Industrial Machinery Market due to their extensive capital resources and need for complex machinery systems. These companies invest in customized, high-capacity equipment to drive continuous production with minimal downtime. In 2024, large enterprises accounted for over 55% of total machinery deployments across sectors. The fastest-growing end-user group is small and mid-sized enterprises (SMEs), spurred by the availability of modular and affordable machinery solutions, as well as government incentives for manufacturing modernization. SMEs increasingly adopt compact, digitally connected systems that require minimal floor space and support plug-and-play integration. Public infrastructure agencies also represent a critical end-user, particularly for large-scale civil engineering and road-building projects. Additionally, contract manufacturers and third-party logistics (3PL) firms are investing in material handling and packaging machinery to enhance service delivery and reduce labor dependency, contributing further to the diversified market landscape.

Asia-Pacific accounted for the largest market share at 41.2% in 2024 however, Region Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 4.7% between 2025 and 2032.

Asia-Pacific’s dominance is underpinned by high machinery consumption in rapidly industrializing nations such as China, India, and South Korea. Countries in this region are investing heavily in smart manufacturing, large-scale construction, and export-driven industrial production. Meanwhile, Middle East & Africa are witnessing robust development in construction, logistics, and energy projects—driven by diversification agendas and increased FDI inflows.

The Industrial Machinery Market continues to evolve in line with technological upgrades, automation trends, and sector-specific demand. Equipment such as CNC machines, robotic arms, precision tools, and heavy construction machinery remain vital across verticals including automotive, electronics, aerospace, agriculture, and oil & gas. Environmental regulations are influencing machine design, with rising interest in energy-efficient motors and smart control systems. North America and Europe focus on high-end automation and predictive maintenance solutions, while Asia-Pacific drives volume-based manufacturing. The global outlook is shaped by sustainability requirements, labor shortages, digitization, and smart factory investments, positioning industrial machinery at the core of modern manufacturing ecosystems.

Digital Retrofitting and Smart Factory Transition Define Regional Machinery Demand

In 2024, the North American region held a 24.6% share of the global Industrial Machinery Market, with robust demand fueled by industries such as aerospace, defense, oil & gas, and automotive manufacturing. The U.S. remains the central hub, with Canada showing notable growth in mining and energy-focused machinery adoption. Government incentives supporting domestic manufacturing and automation adoption under acts like the CHIPS and Science Act have led to increased capital spending on advanced equipment. The trend toward retrofitting existing plants with IoT-enabled machinery and predictive maintenance capabilities continues to dominate investments. Digital twin technology and 3D printing integration in industrial processes are gaining traction, making factories more responsive and resource-efficient.

Industrial Automation and Green Manufacturing Fuel Regional Machinery Growth

Europe accounted for 20.8% of the global Industrial Machinery Market in 2024, with Germany, the UK, and France being the primary contributors. Germany leads in precision engineering and industrial robotics, while the UK shows strength in food processing and pharmaceutical machinery. The European Green Deal and eco-design directives are reshaping the machinery ecosystem, encouraging development of energy-efficient systems and emissions-reducing equipment. Regulatory frameworks from agencies like the European Chemicals Agency (ECHA) have promoted safer and compliant machinery usage. Emerging technologies like AI-driven machine learning, modular automation, and cloud-based controls are widely adopted across the region, further strengthening Europe’s competitive edge in advanced manufacturing.

Infrastructure Expansion and Smart Production Drive Machinery Demand Surge

The Asia-Pacific region topped global charts in 2024 with a 41.2% volume share in the Industrial Machinery Market. China, India, and Japan emerged as the leading consumers, supported by large-scale infrastructure projects, expansive manufacturing zones, and export-focused production hubs. China dominates with mass adoption of CNC machines, robotics, and automation systems across automotive and electronics sectors. India is seeing rising investment in agricultural and textile machinery. Japan continues to push innovation in robotic manufacturing and precision machinery. Across the region, industrial corridors, smart city plans, and the proliferation of industrial parks are pushing machinery demand. Innovation hubs in Shenzhen, Tokyo, and Bangalore are fostering next-gen machinery solutions integrating AI, 5G, and IoT.

Energy Projects and Industrial Revamp Ignite Machinery Sector Advancement

South America captured a 6.5% share of the Industrial Machinery Market in 2024, with Brazil and Argentina being the key contributors. Brazil’s robust oil & gas industry and infrastructure growth drive consistent demand for heavy machinery, pumps, compressors, and construction equipment. Argentina is experiencing renewed machinery imports in the agricultural and food processing sectors following favorable trade revisions. Public-private investment in renewable energy projects is boosting machinery for wind turbine and solar panel manufacturing. Trade policies under Mercosur and government incentives for local machinery production are improving domestic manufacturing capabilities. Growing digital adoption in machinery design and diagnostics is also evident across urban industrial hubs.

Oil Diversification and Mega Projects Accelerate Smart Machinery Adoption

In 2024, the Middle East & Africa region accounted for 6.9% of the global Industrial Machinery Market, with UAE, Saudi Arabia, and South Africa leading demand. The construction of megaprojects such as NEOM and Smart City initiatives are fueling rapid adoption of automated and energy-efficient machinery. Regional demand is primarily driven by oil & gas exploration, real estate, and logistics expansion. Technological modernization is accelerating through initiatives that support local manufacturing clusters and free zones equipped with Industry 4.0 infrastructure. Local regulations promoting industrial diversification, combined with strategic trade agreements and tax benefits, are attracting global machinery manufacturers to set up operations in the region.

China – 28.9% market share

High production capacity and advanced manufacturing infrastructure across multiple sectors.

Germany – 13.6% market share

Strong end-user demand and leadership in automation and precision industrial technologies.

The Industrial Machinery Market is highly competitive, characterized by the presence of over 150 globally active manufacturers, each focusing on diverse machinery categories such as automation systems, material handling equipment, precision tools, and construction machinery. Market participants range from well-established multinational corporations to specialized regional manufacturers, each leveraging advanced technologies to strengthen their market positioning. Key players are increasingly investing in R&D to develop energy-efficient, AI-integrated, and IoT-enabled machinery to align with Industry 4.0 trends.

Strategic initiatives such as cross-border partnerships, joint ventures, and mergers are prevalent across the industry. In 2024, several machinery firms announced collaborations to integrate smart manufacturing solutions into their product lines, aiming to enhance real-time diagnostics, modular functionality, and predictive maintenance capabilities. Additionally, new product launches featuring digital twin compatibility and automated calibration systems gained traction in major manufacturing hubs. The competitive landscape is also shaped by the push for localization in emerging markets and growing demand for machinery that meets stringent environmental standards, influencing product innovation and market share dynamics.

Caterpillar Inc.

Komatsu Ltd.

Siemens AG

Mitsubishi Heavy Industries Ltd.

Doosan Corporation

ABB Ltd.

Hitachi Construction Machinery Co., Ltd.

CNH Industrial N.V.

Bosch Rexroth AG

FANUC Corporation

Deere & Company

Atlas Copco AB

Technological innovation continues to reshape the Industrial Machinery Market, with advancements focused on automation, digitalization, energy efficiency, and sustainability. The integration of Industrial Internet of Things (IIoT) is significantly influencing machinery design and performance, allowing for real-time monitoring, remote diagnostics, and advanced predictive maintenance. IIoT-enabled systems are particularly prevalent in sectors such as automotive and aerospace manufacturing, where precision and uptime are critical. In 2024, more than 60% of newly manufactured industrial machines included some form of embedded sensor or telemetry system.

Artificial Intelligence (AI) and Machine Learning (ML) algorithms are increasingly used to optimize production workflows, perform real-time error detection, and enhance quality assurance processes. These technologies are also enabling adaptive control systems that automatically adjust to variable workloads, minimizing energy usage and maximizing output consistency. Additionally, the rise of digital twin technology is enabling virtual simulations for performance testing, process optimization, and maintenance planning without physical downtime.

Electric and hybrid machinery systems are gaining traction, particularly in urban construction and logistics operations, where environmental regulations are stringent. Robotics integration, especially in packaging, welding, and assembly, is accelerating, with cobots contributing to flexible and safe human-machine collaboration. Additive manufacturing, including industrial-scale 3D printing, is emerging as a valuable technology in prototyping and short-run production. Collectively, these innovations are setting new standards for productivity, sustainability, and cost-efficiency across the Industrial Machinery Market.

• In March 2023, Bosch Rexroth launched the CytroMotion hydraulic compact drive, combining motor, pump, and controller into one unit. It enables energy-efficient linear motion for applications in small industrial presses and testing systems, reducing energy consumption by up to 80% compared to conventional hydraulics.

• In August 2023, Komatsu unveiled its PC210LCE electric hydraulic excavator powered by lithium-ion batteries. Designed for mid-range construction tasks, the machine supports zero-emission operation and features a digital interface for load monitoring and performance analytics.

• In February 2024, Siemens introduced the Sitrans SAM IQ application that uses AI and sensor data for real-time predictive maintenance in industrial flow measurement. The software improves maintenance planning and reduces system downtime by 30% in water and chemical processing environments.

• In June 2024, FANUC expanded its collaborative robot line with the CRX-25iA, featuring a 25 kg payload and 1,889 mm reach. The cobot offers intuitive programming via tablet interface and is aimed at handling heavy materials in manufacturing environments with limited human supervision.

The Industrial Machinery Market Report provides a comprehensive analysis of the global machinery industry, covering a wide array of equipment categories, applications, and technological domains. The scope spans critical machinery types such as construction equipment, manufacturing systems, packaging machines, machine tools, and automated handling units. It includes advanced robotic systems, AI-enabled process machinery, and energy-efficient electric or hybrid-powered units.

Geographically, the report encompasses North America, Europe, Asia-Pacific, South America, and Middle East & Africa, offering regional insights into market demand, regulatory environments, and infrastructure developments. It evaluates machinery applications across key sectors including automotive, aerospace, energy, agriculture, construction, logistics, and food processing. Special attention is given to rapidly emerging sectors such as renewable energy component manufacturing and precision engineering for medical devices.

The report also covers advancements in automation, predictive maintenance, remote diagnostics, and cloud-integrated control systems. Emphasis is placed on Industry 4.0 technologies such as digital twins, industrial AI, and IIoT, along with sustainability-driven innovations including low-emission machines and recyclable material components. Furthermore, the report outlines end-user perspectives from SMEs to large enterprises and public sector projects. This detailed scope ensures that decision-makers receive a well-rounded view of current capabilities, market dynamics, and future potential within the Industrial Machinery Market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 673286.04 Million |

|

Market Revenue in 2032 |

USD 893465.22 Million |

|

CAGR (2025 - 2032) |

3.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Caterpillar Inc., Komatsu Ltd., Siemens AG, Mitsubishi Heavy Industries Ltd., Doosan Corporation, ABB Ltd., Hitachi Construction Machinery Co., Ltd., CNH Industrial N.V., Bosch Rexroth AG, FANUC Corporation, Deere & Company, Atlas Copco AB |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |