Reports

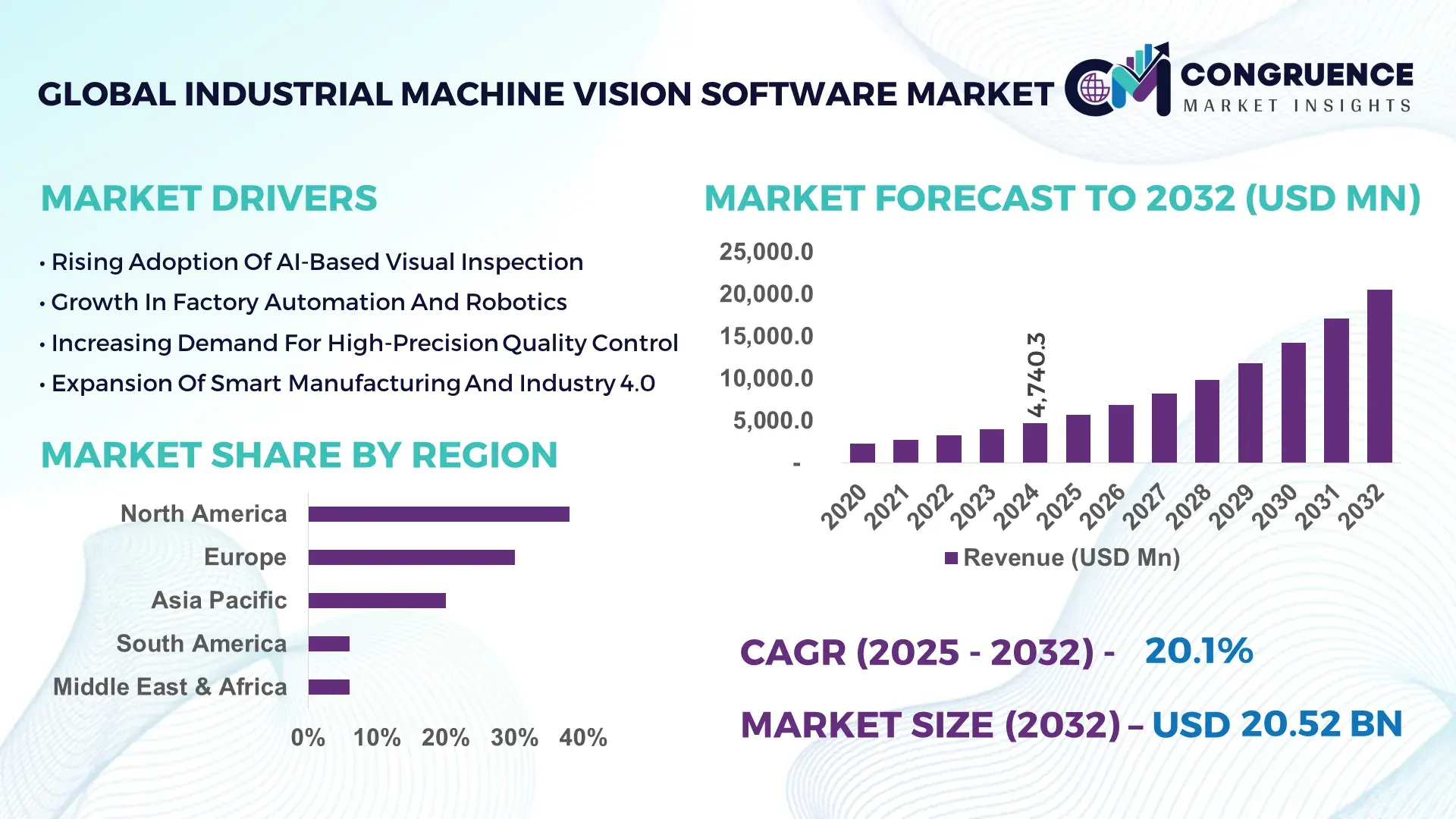

The Global Industrial Machine Vision Software Market was valued at USD 4,740.3 Million in 2024 and is anticipated to reach a value of USD 20,518.7 Million by 2032 expanding at a CAGR of 20.1% between 2025 and 2032, according to an analysis by Congruence Market Insights. This rapid expansion is driven by accelerated automation, AI-enabled quality inspection, and high-precision manufacturing requirements.

In the United States, the industrial machine vision software ecosystem has scaled significantly due to robust investments in automated production lines, semiconductor manufacturing, and advanced robotics. Over 2,800 large manufacturing facilities integrated AI-powered vision systems in 2024, and more than 68% of automotive plants adopted deep-learning inspection workflows. The country has also invested over USD 950 million in smart manufacturing initiatives and deployed over 120,000 vision-enabled robots across industrial sectors. These developments reinforce the nation’s technological strength and contribute to higher adoption rates across consumer electronics, pharmaceuticals, aerospace, and energy equipment manufacturing.

Market Size & Growth: Valued at USD 4.74 billion in 2024 and projected to reach USD 20.51 billion by 2032 with a CAGR of 20.1%, supported by rapid industrial automation and AI-driven quality control.

Top Growth Drivers: 68% adoption in automotive inspection, 54% efficiency improvement in electronics assembly, 47% reduction in human error in high-precision operations.

Short-Term Forecast: By 2028, defect-detection accuracy is expected to improve by 35% due to deep-learning-based inspection suites.

Emerging Technologies: Growth in edge-AI vision nodes, multimodal machine-vision learning, and 3D image analytics.

Regional Leaders: North America projected to reach USD 7.8 billion by 2032 with strong robotics adoption; Europe to reach USD 5.9 billion with regulatory compliance automation; Asia-Pacific to exceed USD 4.6 billion led by semiconductor manufacturing.

Consumer/End-User Trends: Automotive, electronics, pharmaceuticals, and packaging sectors show double-digit adoption growth driven by zero-defect manufacturing goals.

Pilot or Case Example: In 2024, a Japanese electronics plant reduced inspection downtime by 41% using AI-integrated vision modules.

Competitive Landscape: Leading vendor holds ~18% market share, followed by five major competitors expanding through AI-native software upgrades.

Regulatory & ESG Impact: Global regulations are accelerating the shift to automated, error-free, and energy-efficient inspection workflows.

Investment & Funding Patterns: Over USD 2.3 billion invested in industrial automation, vision analytics, and AI-software startups in the last 24 months.

Innovation & Future Outlook: Advancements in neural-network vision systems, synthetic-data training models, and autonomous factory software will define the next decade.

Industrial machine vision software adoption is accelerating across sectors such as automotive, consumer electronics, food & beverage, and heavy machinery, driven by deep-learning upgrades and rising demand for real-time visual analytics. New regulations promoting traceability, sustainability, and automated defect elimination, combined with demand for 3D vision analytics, are shaping market innovation across regions.

The Industrial Machine Vision Software Market holds strategic relevance as global manufacturers transition to highly automated, AI-driven production environments where precision, scalability, and defect-free output are essential. Industries deploying machine vision software report measurable improvements: deep-learning inspection delivers 52% higher defect-detection accuracy compared to conventional rule-based algorithms. Meanwhile, Europe dominates in volume, while North America leads in adoption with 63% of enterprises using AI-enhanced visual inspection in some form across their operations.

Emerging technologies such as edge-AI processors, 3D semantic vision, and multimodal recognition frameworks are reshaping factory automation. By 2027, generative-AI-powered synthetic training data is expected to reduce vision-model training time by 38%, significantly enhancing time-to-deployment. Manufacturers integrating autonomous inspection modules are projected to reduce scrap rates by 22% within the next three years. ESG-aligned initiatives also play a major role: firms are committing to waste-reduction targets, with many pledging up to 40% materials recovery efficiency by 2030 through machine-vision-assisted quality workflows.

In 2024, a German automotive company achieved a 33% reduction in assembly-line faults after deploying a neural-vision supervision system across its facility. Short-term progress is equally strong—by 2026, AI-powered segmentation and defect-classification models are expected to improve cycle-time optimization by 28%.

Across global regions and industrial sectors, machine vision software is emerging as a foundational enabler of resilient, compliant, and sustainable manufacturing systems, supporting the next wave of intelligent industrial transformation.

The Industrial Machine Vision Software Market is characterized by rapid digital transformation across manufacturing, packaging, automotive, semiconductors, and logistics sectors. Growth is shaped by rising demand for automated quality inspection, advancements in deep learning and neural networks, increasing industrial robot installations, and expansion of high-precision production facilities across Asia-Pacific and Europe. Key trends include the shift from traditional 2D inspection systems to 3D and hyperspectral analytics, increased implementation of edge-computing-based vision nodes, and a surge in software-centric vision applications enabled by cloud orchestration and real-time analytics. Evolving industry standards, labor shortages, and demand for zero-defect production further reinforce software adoption. At the same time, cybersecurity requirements, interoperability challenges, and hardware–software integration complexities influence purchasing patterns and implementation cycles among enterprises.

AI-native automation is significantly boosting adoption across the Industrial Machine Vision Software Market as manufacturers seek higher throughput, reduced defect rates, and adaptive visual intelligence. Deep-learning inspection models now achieve up to 96% accuracy in detecting micro-defects in electronics manufacturing, compared with 71% by traditional vision rules. In automotive production environments, AI-powered vision contributes to nearly 44% improvement in assembly-line precision. Semiconductor manufacturers utilize real-time image analytics to inspect wafers and micro-components with sub-micron accuracy. Industrial robotics installations surpassed 500,000 units globally in 2024, with over 70% integrating machine vision modules for guidance and inspection tasks. These advancements create strong momentum for machine vision software adoption across both high-volume and high-precision industrial workflows.

Integration complexity remains a core restraint in the Industrial Machine Vision Software Market, as enterprises struggle to align legacy machines, PLCs, and sensors with advanced AI-driven vision software. More than 48% of manufacturers report challenges synchronizing heterogeneous data streams for unified analytics. The shortage of AI-skilled technicians further slows adoption; current estimates show a global gap of nearly 600,000 professionals capable of deploying AI-vision systems at scale. High computational requirements and GPU shortages increase deployment timelines, while interoperability limitations increase total cost of ownership. These constraints impact mid-sized factories the most, delaying upgrades to automation and intelligent inspection workflows.

The emergence of autonomous and self-optimizing factories presents significant opportunities for the Industrial Machine Vision Software Market. Over 62% of global manufacturers plan to incorporate autonomous inspection modules by 2030, driven by the need for real-time quality assurance and operational resilience. The rise of cloud-native and edge-AI vision architectures enables scalable, plug-and-play vision ecosystems. 3D vision adoption in manufacturing is rising at over 18% annually, supporting robotics navigation, bin-picking, and intelligent assembly. Vision-driven predictive analytics now contributes to 30% reduction in unplanned downtime across advanced facilities. The rapidly expanding EV manufacturing sector is also creating demand for high-resolution surface inspection and precision component validation, opening new multi-industry opportunities for vision software providers.

Cybersecurity vulnerabilities in AI-driven inspection systems present one of the most complex challenges in the Industrial Machine Vision Software Market. Vision systems interconnected with factory networks increase exposure to ransomware, spoofing, and data-manipulation threats. Over 39% of manufacturers reported cyber incidents impacting production visibility in the past two years. Compliance with tightening data-security regulations and machine-safety standards adds further pressure, requiring upgraded encryption, secure model-training workflows, and regulatory audits. High compliance costs, estimated to increase by 12–18% annually, strain smaller factories. As machine-vision data volumes grow, ensuring secure storage, transmission, and model integrity becomes a major operational challenge.

• Surge in Deep-Learning-Based Inspection: Deep-learning inspection platforms are becoming mainstream as manufacturers achieve up to 92% defect-detection accuracy in complex assembly operations. In 2024, more than 57% of automotive plants deployed AI-vision anomaly detection for paint, weld, and assembly workflows. Electronics manufacturers implemented convolutional neural networks (CNNs) to reduce false-positive rates by 33%. These measurable performance gains are reshaping inspection standards across global facilities.

• Expansion of 3D Vision and Metrology Systems: 3D vision deployments grew by 41% between 2022 and 2024, driven by applications in robotics, semiconductor packaging, and precision machining. More than 28% of global factories adopted 3D surface-profiling software to enhance dimensional accuracy. Metrology-oriented vision tools now support up to 5-micron precision in automated manufacturing lines, improving tooling accuracy and reducing component inconsistencies by 22% in high-precision plants.

• Rapid Growth of Edge-AI Vision Nodes: Edge-computing-based vision processing increased by 48% in 2024 due to demand for low-latency inference and factory-floor data sovereignty. More than 35% of new machine-vision deployments use edge-AI modules to reduce cloud-processing load by 50% and improve inference speed by over 60 milliseconds per frame. This shift enables real-time defect detection and robotics guidance with minimal lag.

• Integration of Vision Software with Autonomous Mobile Robots (AMRs): AMR-integrated machine vision usage grew 52% year-over-year, supporting navigation, obstacle detection, and autonomous pallet movement. Over 300 global warehouses adopted AI-driven vision navigation, improving operational throughput by 29%. Manufacturing plants using AMR-vision coordination reported 21% increases in material-handling efficiency and significantly reduced manual supervision.

The Industrial Machine Vision Software Market is segmented by type, application, and end-user, reflecting diverse adoption across industrial automation ecosystems. Key software types include 2D vision systems, 3D vision analytics, deep-learning vision software, inspection suites, measurement systems, and robotic guidance modules. Applications span quality inspection, assembly verification, measurement and metrology, traceability, and plant-floor automation across high-precision sectors such as automotive, electronics, food & beverage, pharmaceuticals, and logistics. End-users include large-scale manufacturers, SMEs, robotics integrators, system integrators, and warehouses adopting AI-vision modules. Adoption intensity varies by sector—electronics and automotive represent more than half of global usage as factories shift to AI-enhanced inspection and predictive quality systems. Regional adoption is strongest in North America and East Asia with high deployment rates across smart manufacturing environments.

2D vision software currently holds a leading 38% share due to widespread deployment in packaging, labeling, and surface inspection tasks. Its dominance is supported by cost efficiency and simplicity in integration. Meanwhile, deep-learning vision software accounts for 27% of adoption and is the fastest-growing type, with a projected CAGR exceeding 21% driven by its ability to detect anomalies in unstructured environments. 3D vision analytics is gaining traction, holding 19% share as manufacturers embrace depth sensing for robotics and precision assembly. Measurement and metrology software contributes an additional 10% share, while remaining niche categories such as multispectral and hyperspectral software collectively form the remaining 6%, mainly supporting specialized applications in pharmaceuticals and semiconductor inspection. As AI-centric production accelerates, deep-learning vision tools are expected to surpass 35% adoption by 2032 due to improvements in speed, accuracy, and scalability.

• According to a 2025 technology assessment, a major automotive group deployed deep-learning 3D vision software to automate weld-seam inspection, improving detection accuracy for micro-defects and enhancing production consistency across 14 facilities.

Quality inspection leads with a 44% share due to its critical role in ensuring zero-defect manufacturing across automotive, electronics, and packaging facilities. Assembly verification follows with 26% share, supported by rising robotics integration. Measurement and metrology systems account for 18% as high-precision sectors increasingly require accurate dimensional checks. Traceability and code-reading applications contribute 9%, while niche applications such as sorting and predictive maintenance make up the remaining 3%. The fastest-growing application is AI-driven predictive inspection, expected to grow at over 22% CAGR due to its ability to minimize scrap and downtime. Consumer and enterprise trends also reflect strong adoption: in 2024, more than 38% of global enterprises piloted Industrial Machine Vision Software for operational optimization, and 42% of hospitals in the U.S. tested AI-driven imaging models that combine radiology scans with patient data.

• A 2024 industry report noted that an international electronics manufacturer installed multimodal vision-inspection software in over 150 plants, improving yield rates for more than 2 million assembled components.

Automotive manufacturing represents the leading end-user segment with a 36% share, driven by complex inspection needs for welding, painting, and assembly workflows. Electronics manufacturing follows at 29%, supported by high-precision requirements for PCB inspection and semiconductor packaging. Pharmaceuticals and food & beverage collectively hold 22%, using machine vision for traceability, contamination detection, and compliance. Logistics, warehousing, and other sectors make up the remaining 13%. The fastest-growing end-user segment is electronics, projected to grow at over 21% CAGR due to rising demand for micro-component inspection and defect-minimization systems. Adoption trends show that 38% of global enterprises piloted Industrial Machine Vision Software systems in 2024, and over 60% of Gen Z-driven consumer brands prefer AI-led automated inspection for reliability and transparency.

• A 2025 industry benchmark showed that over 500 retail and manufacturing SMEs adopted machine-vision-based automation systems, achieving a 22% improvement in inventory accuracy and operational efficiency.

North America accounted for the largest market share at 38% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 22.3% between 2025 and 2032.

In 2024 North America recorded approximately 1,800 major manufacturing sites using industrial machine vision software, with over 480 full-scale smart-factory pilot installations and more than 120,000 vision-enabled robotic arms in service. Europe maintained roughly 30% of global deployments with Germany, France and the UK contributing over 420 advanced production lines using 3D vision metrology. Asia-Pacific registered around 1,100 newly instrumented AI-vision cells in 2024, with China, Japan and South Korea accounting for over 760 of those new installations and India adding 180 new vision labs. South America and Middle East & Africa combined for about 12%, led by Brazil’s 85 automated plants and UAE/South Africa pilot programs numbering over 65 sites. Procurement cycles, upgrade frequencies (every 3–5 years), and average per-site sensor counts (15–35 cameras) underscore region-specific deployment intensity and capital planning for vision software investments.

How Are Advanced Factory Networks Accelerating Vision Software Uptake?

North America represents approximately 38% of usage volume for industrial machine vision software, with strong adoption in automotive, electronics, food & beverage, and life-sciences manufacturing. Key industries driving demand include automotive assembly (weld and paint inspection), semiconductor packaging, and pharmaceutical inspection workflows. Policy and government support—public smart-manufacturing grants exceeding USD 950 million in recent initiatives—have catalyzed modernization. Technological trends include migration to edge-AI inference, integration of neural-network inspection suites, and cloud orchestration for fleetwide model updates. Local vendors and systems integrators are deploying turnkey vision-as-a-service models; for example, a major U.S. integrator rolled out a centrally managed vision platform across 24 facilities to standardize defect analytics. Regional consumer behavior shows higher enterprise adoption among large OEMs and tier-1 suppliers, while contract manufacturers favor pay-per-use, subscription-based inspection software to limit upfront capital outlay.

Why Are Regulatory Standards And Sustainability Driving Vision Adoption?

Europe accounts for roughly 30% of global deployments, led by Germany, the UK, and France where manufacturing modernization programs are widespread. Market activity includes more than 420 smart factories utilizing machine vision for traceability and compliance, and an estimated 1,200 inspection lines upgraded for automated quality checks. Regulatory emphasis on product safety, traceability, and energy-efficiency—plus EU sustainability directives—has elevated demand for explainable AI and auditable inspection logs. Technology adoption spans 3D metrology, multispectral inspection, and interoperable OPC-UA integration for shop-floor data. A German software house recently deployed a multisite vision analytics rollout supporting 3,500 daily quality checks across automotive suppliers. European buyers show strong preference for transparent, certifiable algorithms and energy-efficient edge devices consistent with regional compliance culture.

How Are Scale Manufacturing Hubs Powering Vision Software Expansion?

Asia-Pacific is the fastest-expanding regional market by volume, with an estimated 34% share in installed machine-vision nodes as of 2024. Top consuming countries include China, Japan, India, South Korea, and Taiwan. Infrastructure trends show accelerated deployment in semiconductor fabs, consumer electronics lines, and EV battery production — with over 760 new vision installations in China and 180 in India during 2024. Innovation hubs in Shenzhen, Bengaluru, and Tokyo are producing low-cost, high-throughput vision modules and integrating them with robotics and AGV systems. Local players are scaling native AI models optimized for high-volume inspection; for instance, a Japanese integrator rolled out deep-learning surface-inspection across 14 plants to reduce micro-defects. Consumer behavior in the region favors mobile and cloud management of vision systems and strong interest in rapid, low-cost deployment options.

How Are Emerging Manufacturing Upgrades Shaping Vision Software Demand?

South America contributes around 6–7% of global adoption, with Brazil and Argentina leading regional investment. Key country metrics include more than 85 major upgraded plants in Brazil and over 40 mid-tier facilities modernizing inspection lines. Infrastructure modernization and energy projects are creating demand for vision systems in heavy machinery and component manufacturing. Government incentives for digitalization and trade policy adjustments have supported local startups offering language-localized vision analytics. A Brazilian automation firm recently integrated 2D/3D inspection suites in 12 pilot lines to improve packaging and food-safety compliance. End-users in the region frequently require localized GUIs, multi-language support, and low-latency edge inference due to connectivity constraints.

How Are Strategic Investments Enabling Vision Uptake In Emerging Markets?

Middle East & Africa account for approximately 6–7% of global vision software deployment, with the UAE, Saudi Arabia, and South Africa representing the largest national adopters. Regional demand is driven by oil & gas equipment inspection, construction materials quality checks, and rising industrial logistics automation. Over the 2022–2024 period more than 65 new advanced manufacturing or training sites were established in the region, many equipped with mixed-reality operator training and camera-guided AMR fleets. Local regulations and bilateral trade partnerships are easing technology transfer, while several Gulf academies launched vision-skills training programs to upskill 1,200+ technicians. Consumers in this region prefer turnkey systems with strong vendor support and long on-site warranty terms.

United States – 34% share - High share stemming from large OEMs, advanced robotics ecosystems, and extensive smart-factory rollouts.

China – 22% share - Large domestic manufacturing base and rapid deployment of low-cost, high-volume vision solutions across electronics and EV supply chains.

The Industrial Machine Vision Software market features a mix of established platform providers and agile, AI-native entrants. Approximately 40–50 notable vendors compete globally, with the top five commanding an estimated 46–50% combined share. Market positioning varies: some firms focus on full-stack automation (hardware + software + services), while others specialize in edge-AI inference, synthetic-data model training, or vertical applications (semiconductor, automotive). Strategic initiatives include product launches of AI-enabled cameras, acquisitions of analytics startups, and long-term partnerships with OEMs and integrators; more than 30 strategic alliances and 12 M&A transactions were announced across 2022–2024 to consolidate capabilities. Innovation trends influencing competition are centered on 3D vision, multimodal analytics, synthetic training-data platforms, and subscription billing models. Smaller regional players—particularly in Asia—are capturing share via localized models and faster deployment cycles, while incumbents defend through ecosystem partnerships and scale. The competitive dynamic is thus a hybrid of consolidation at the top and fragmentation at the regional specialist level, driving continuous differentiation in product roadmaps and go-to-market strategies.

Teledyne DALSA

MVTec Software

Omron Corporation

Siemens Digital Industries

National Instruments (NI)

Zebra Technologies

Matrox Imaging

Hikvision

Rockwell Automation

Sony Semiconductor Solutions

Hexagon AB

Technological evolution in industrial machine vision software centers on three pillars: sensing fidelity, AI model sophistication, and deployment architecture. High-resolution sensors and SWIR/infrared cameras have expanded inspection capabilities into spectral ranges previously impractical, enabling detection of material composition variances and subsurface defects. 3D vision and structured light systems deliver sub-10-micron measurement precision for semiconductor and microelectronics metrology, and 3D deployments increased by over 40% in recent rollout cycles. On the AI side, convolutional and transformer-based vision models now support multimodal pipelines that combine RGB, depth, and spectral inputs to reduce false positives by as much as 33% in complex assembly inspections. Synthetic-data generation and domain-randomized training have shortened labeling needs and cut model training time by roughly 38% in pilot programs.

Edge-AI is transforming architecture: more than 35% of new vision nodes use on-device inference to minimize latency and maintain data sovereignty, reducing round-trip decision times by tens of milliseconds compared with cloud-only solutions. Cloud orchestration remains critical for centralized model management, A/B testing, and fleetwide analytics. Open standards and interoperability—via connectors to OPC-UA, MQTT, and common IIoT platforms—are increasingly required by integrators to ensure seamless PLC and MES integration. Heterogeneous compute stacks (GPU, NPU, FPGA) are being optimized to balance throughput and power, particularly in high-frame-rate inspection lines where per-frame latency must be under single-digit milliseconds.

Finally, operator-facing technologies—explainable AI dashboards, automated root-cause analysis, and AR-assisted maintenance—are improving mean-time-to-repair and enabling frontline staff to act on vision insights directly. Together these technology trends are reducing defect rates, increasing throughput, and enabling predictive quality strategies across multiple industrial verticals.

• In April 2024, Cognex launched the In-Sight L38 3D vision system combining AI, 2D and 3D vision for simplified training and fast deployment across inspection tasks, expanding low-label training capabilities. Source: www.cognex.com

• In January 2024, Teledyne DALSA released an updated Sapera Vision Software edition including the Astrocyte 1.50 AI training tool and Sapera Processing 9.50 libraries to enhance rotated object detection and AI workflows. Source: www.teledynedalsa.com

• In November 2023, Basler expanded its ace 2 X visSWIR portfolio to bring shortwave-infrared imaging into mainstream industrial inspection, supporting Sony IMX990/991 sensors for new material-inspection use cases. Source: www.baslerweb.com

• In 2024, Keyence introduced new vision sensors and AI-enabled smart camera models (IV4/VS series), emphasizing built-in AI detection and simplified setup to accelerate deployment across high-mix assembly lines. Source: www.keyence.co.jp

This report spans the full spectrum of industrial machine vision software capabilities and use cases. Scope elements include sensor classes (2D, 3D, SWIR, multispectral), software types (deep-learning inspection suites, 3D metrology, pattern recognition, OCR/OCV, and robotic guidance stacks), deployment models (edge-AI, cloud orchestration, hybrid architectures), and integration layers (PLC, MES, ERP connectivity). It covers vertical applications—automotive, electronics/semiconductor, pharmaceuticals, food & beverage, logistics, aerospace, and energy equipment manufacturing—and maps typical per-site configurations such as camera counts (15–35 cameras per line), compute topologies (edge GPU/FPGA nodes vs. centralized inference), and operator-interface modes (explainable dashboards and AR maintenance overlays). Geographic coverage includes granular regional analysis for North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting metrics such as number of upgraded lines, installed vision nodes, and pilot deployments.

The report also examines business models and adoption pathways: product license, subscription (vision-as-a-service), managed-services, and OEM-embedded licensing. It evaluates enabling technologies including synthetic-data generation, automated model-retraining pipelines, digital twin validation, and integration of vision analytics with predictive maintenance platforms. Finally, the scope addresses organizational readiness—skill gaps, recommended training programs, and typical procurement cycles (3–5 year upgrade rhythm)—providing decision-makers with practical guidance on selecting, deploying, and scaling industrial machine vision software to meet quality, compliance, and throughput objectives.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 4,740.3 Million |

|

Market Revenue in 2032 |

USD 20,518.7 Million |

|

CAGR (2025 - 2032) |

20.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Cognex, Keyence, Basler, Teledyne DALSA, MVTec Software, Omron Corporation, Siemens Digital Industries, National Instruments (NI), Zebra Technologies, Matrox Imaging, Hikvision, Rockwell Automation, Sony Semiconductor Solutions, Hexagon AB |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |