Reports

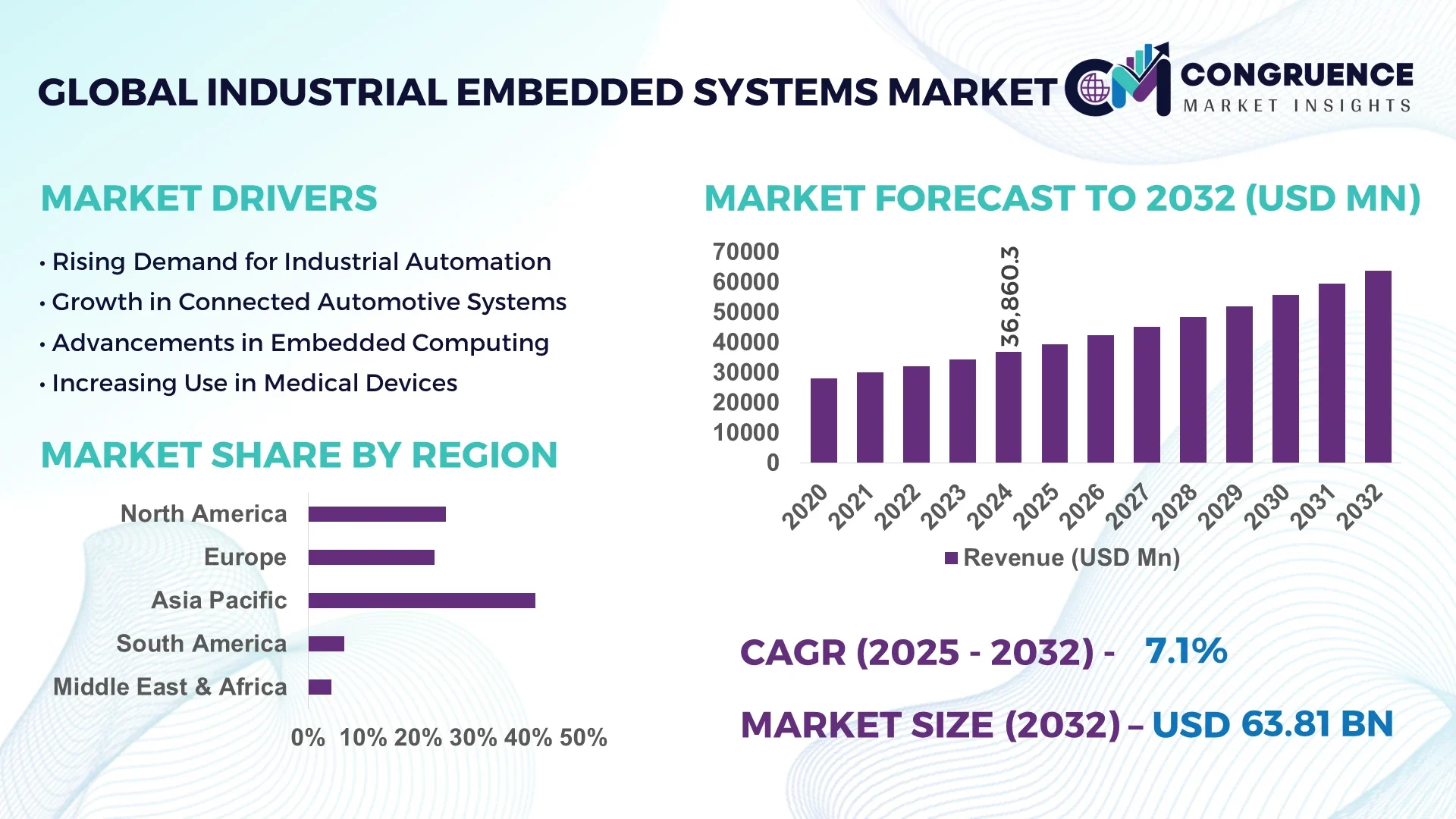

The Global Industrial Embedded Systems Market was valued at USD 36,860.3 Million in 2024 and is anticipated to reach a value of USD 63,807.9 Million by 2032, expanding at a CAGR of 7.1% between 2025 and 2032.

China plays a pivotal role in the Industrial Embedded Systems market. The country continues to lead with massive investments in automation, AI-integrated manufacturing, and high-precision embedded controller fabrication. China’s industrial parks in provinces like Guangdong and Jiangsu have seen a surge in embedded solution deployments across automotive, energy, and electronics sectors, backed by advanced infrastructure and R&D ecosystems.

The Industrial Embedded Systems market is characterized by high adoption across critical industries including automotive, industrial automation, telecommunications, aerospace, and energy management. Automotive applications involve embedded solutions for ADAS, EV power management, and infotainment systems. The automation sector sees strong usage in PLCs, SCADA systems, and smart factory devices. Innovation is prominent with advancements in System-on-Chip (SoC) architectures, low-latency microcontrollers, and AI-integrated embedded platforms. Government policies promoting green technologies and digital transformation are accelerating embedded adoption in industrial and utility sectors. North America and Asia-Pacific remain key growth regions, with increasing IIoT deployments and demand for intelligent edge devices. Additionally, trends like real-time analytics, low-power designs, and RISC-V architecture expansion are expected to reshape the market landscape through 2032.

Artificial Intelligence is radically transforming the Industrial Embedded Systems Market by infusing intelligence into core control and processing units used in industrial applications. With AI, embedded systems are evolving beyond static control modules to become adaptive, self-learning units capable of real-time decision-making and predictive functionality. These AI-powered embedded platforms enhance industrial automation, enabling factories to shift towards smart manufacturing ecosystems that prioritize efficiency, autonomy, and safety.

One of the significant applications is in predictive maintenance, where AI algorithms process real-time sensor data to anticipate machine failures before they happen, minimizing downtime and reducing repair costs. In automated quality control, vision-based AI embedded systems inspect product defects with far greater speed and accuracy than traditional human inspection. In power and utilities, embedded AI improves grid responsiveness and supports renewable energy integration by forecasting load demands and managing energy distribution dynamically.

AI is also driving the development of edge AI embedded devices, allowing industrial systems to process data locally rather than relying on cloud resources. This leads to reduced latency, faster response times, and enhanced cybersecurity. The AI transformation also facilitates collaborative robotics (cobots) that interact with humans safely in manufacturing environments, powered by real-time data processing on embedded AI modules. As industrial environments demand greater operational intelligence, AI is poised to remain a cornerstone of growth in the Industrial Embedded Systems Market through the next decade.

“In January 2024, Siemens introduced its next-generation SIMATIC S7-1500 TM NPU module with integrated AI capability, enabling machine learning inference directly on the PLC level. This AI-enhanced embedded system reduced production line inspection time by 35% and improved fault detection accuracy by over 40% in test deployments across automotive assembly lines.”

Industrial automation is one of the most critical growth drivers for the Industrial Embedded Systems market. Modern manufacturing plants are rapidly incorporating programmable logic controllers (PLCs), smart sensors, and real-time control systems—all of which are underpinned by embedded technology. According to recent industrial reports, over 60% of manufacturing facilities globally adopted some form of automation in 2024, and this figure continues to rise. Embedded systems enable continuous machine-to-machine communication and adaptive control, supporting efficient, safe, and high-speed production. With the global trend of labor shortage in industrial sectors, automation backed by embedded platforms is increasingly viewed as a viable and sustainable solution to enhance output quality and reduce human error.

One of the primary restraints in the Industrial Embedded Systems market is the complexity associated with hardware-software integration. Industrial embedded systems must operate under harsh environmental conditions and meet real-time performance requirements, making system design highly complex. Developing application-specific embedded solutions demands specialized engineering expertise, custom firmware development, and rigorous testing to ensure compatibility with legacy industrial infrastructure. Moreover, as embedded systems evolve to include AI and ML capabilities, the software stack becomes more layered and harder to manage. This complexity can slow down product development cycles and increase production costs for OEMs, deterring smaller enterprises from rapid adoption.

The rising adoption of Edge AI presents a significant opportunity in the Industrial Embedded Systems market. As industries aim to minimize latency and enhance real-time responsiveness, there's growing interest in deploying AI directly on embedded edge devices. These systems allow immediate decision-making without depending on cloud processing, which is vital for time-sensitive operations in manufacturing, energy grid management, and transportation. In 2024, more than 45% of new industrial embedded deployments were reported to support some level of edge AI functionality. This trend opens avenues for embedded solution providers to develop compact, power-efficient platforms with onboard neural processing units (NPUs), catering to use cases like visual inspection, predictive maintenance, and robotics automation.

Cybersecurity remains a growing challenge in the Industrial Embedded Systems market, particularly as IIoT connectivity expands across critical infrastructure. Embedded systems are increasingly exposed to cyber threats due to their networked nature and often outdated firmware. In 2024, several high-profile breaches highlighted the vulnerability of industrial control systems running on insecure embedded firmware. Additionally, embedded systems typically have limited computing resources, making it difficult to implement conventional cybersecurity measures. As cyber-attacks become more sophisticated, manufacturers are under pressure to incorporate security-by-design principles, frequent firmware updates, and encrypted communication protocols—often requiring additional investment and development time, thereby complicating deployment strategies.

Rise in Modular and Prefabricated Construction: The adoption of modular construction techniques is significantly impacting the Industrial Embedded Systems market. Automated production of prefabricated components such as pre-bent beams and pre-cut panels demands precise control systems and real-time data processing. Embedded systems facilitate this precision by powering robotic arms, CNC machinery, and automated quality assurance mechanisms. In 2024, over 35% of new industrial building projects in North America and Europe incorporated prefabricated elements, driving strong demand for embedded solutions capable of withstanding continuous operation in off-site factory environments.

Integration of Real-Time Operating Systems (RTOS): Industrial equipment increasingly requires faster processing with low-latency task execution, fueling the implementation of RTOS in embedded platforms. These systems enable seamless multitasking, time-critical process control, and synchronized equipment coordination. By mid-2024, approximately 48% of newly developed embedded industrial controllers were running RTOS-based environments, especially in sectors such as automotive manufacturing, oil & gas automation, and heavy machinery control. This shift is accelerating software standardization and enhancing compatibility across cross-vendor industrial ecosystems.

Expansion of Embedded Systems in Renewable Energy Infrastructure: The global push for decarbonization has led to a surge in renewable energy projects, with embedded systems playing a central role in optimizing solar tracking systems, wind turbine controllers, and energy storage management. In 2024, installations of smart embedded inverters and energy management modules rose by 27%, particularly in Asia-Pacific and Latin America. These embedded solutions ensure efficient power generation and grid connectivity through real-time data analytics, fault detection, and predictive control mechanisms.

Increased Adoption of Embedded Vision Systems in Quality Control: Industrial manufacturing lines are rapidly adopting embedded vision systems to automate quality control and reduce human error. These systems integrate cameras with on-board AI processors capable of inspecting products at high speeds and with extreme accuracy. As of Q4 2024, usage of embedded vision systems rose by 31% across electronics and precision tools manufacturing sectors. This trend enhances efficiency in detecting defects, classifying products, and ensuring consistent output—key drivers for competitive industrial operations worldwide.

The Industrial Embedded Systems market is distinctly segmented by type, application, and end-user, each contributing uniquely to overall market performance and growth. Product types range from hardware platforms to software-based embedded solutions, with advancements in real-time processing and compact system designs expanding adoption across industries. Applications span factory automation, industrial robotics, power distribution systems, and monitoring solutions. The market is further driven by end-user demand in industries such as automotive, energy, manufacturing, and telecommunications. The diversification of use cases, combined with increasing demands for industrial digitization and real-time data processing, is fueling the evolution of each segment. Notably, embedded systems integrated with edge AI capabilities are transforming industrial operations by providing localized intelligence. Meanwhile, demand for resilient systems suitable for extreme environments, especially in energy and aerospace sectors, continues to influence product development strategies. Overall, each segment plays a pivotal role in shaping market direction and delivering value to industry stakeholders.

The Industrial Embedded Systems market includes various product types such as microcontrollers, microprocessors, field-programmable gate arrays (FPGAs), digital signal processors (DSPs), and embedded software solutions. Among these, microcontrollers currently lead the segment due to their compact size, cost-effectiveness, and versatility in handling real-time tasks in automation systems, sensor integration, and actuator control. Their widespread deployment in programmable logic controllers (PLCs) and robotic arms makes them the preferred choice for most manufacturing environments. FPGAs represent the fastest-growing type, driven by their reconfigurability and capacity to handle high-speed data processing in real-time industrial applications. Their use in sectors like aerospace, smart grid automation, and predictive maintenance systems is expanding, due to increasing demand for customizable and energy-efficient solutions. Other product types such as DSPs are predominantly used in audio, imaging, and control-intensive processes. Embedded software is also gaining relevance with the growth of IoT-driven architectures, supporting scalability, remote updates, and cloud integration for industrial-grade applications.

Key application areas of Industrial Embedded Systems include industrial automation, robotics, energy management systems, process control, and safety & surveillance. Industrial automation stands as the dominant application area, underpinned by the proliferation of smart factories and Industry 4.0 integration. Embedded systems play a central role in enabling machine-to-machine communication, sensor coordination, and adaptive control in automated workflows. Robotics is witnessing the fastest growth in application, fueled by increasing investment in collaborative robots (cobots) and autonomous material handling units. This surge is evident in sectors like logistics, pharmaceuticals, and precision manufacturing, where embedded processors support machine learning algorithms and motion control functionalities. Other applications such as energy management systems and industrial safety monitoring are gaining traction due to increased emphasis on energy efficiency and workplace safety. The growing deployment of embedded systems in these domains underscores their flexibility and critical importance across diverse operational environments.

The end-user landscape of the Industrial Embedded Systems market encompasses manufacturing, automotive, energy & utilities, aerospace & defense, and telecommunications. Manufacturing leads the market due to the widespread integration of embedded platforms in assembly lines, CNC machines, and smart control panels. Their ability to reduce downtime, enhance operational visibility, and support predictive analytics has made them indispensable to modern manufacturing ecosystems. The automotive sector is currently the fastest-growing end-user, driven by the shift toward electric vehicles (EVs), advanced driver assistance systems (ADAS), and real-time vehicular diagnostics. Embedded solutions are increasingly deployed for real-time sensor fusion, powertrain control, and in-vehicle infotainment systems. Other significant contributors include energy & utilities, where embedded systems are essential in smart metering and grid automation, and aerospace & defense, where system reliability and ruggedization are paramount. Telecommunications also benefits from embedded platforms in network infrastructure, enabling high-speed data routing and real-time communication protocols.

Asia-Pacific accounted for the largest market share at 41.3% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 8.2% between 2025 and 2032.

Asia-Pacific’s lead in the Industrial Embedded Systems market stems from its dominant electronics and manufacturing hubs across China, Japan, South Korea, and India. Rising investments in smart factories and increasing demand for automated systems have significantly boosted market adoption. Meanwhile, North America's push toward industrial automation, coupled with increasing adoption of AI-integrated embedded solutions in industries like automotive and aerospace, is expected to fuel its accelerated growth. Europe remains a mature yet innovation-centric region due to sustainability-driven digital initiatives. South America and the Middle East & Africa are gradually expanding their embedded infrastructure, propelled by energy diversification and industrial digitization. Each region contributes uniquely, with technological trends, governmental reforms, and industry-specific needs guiding the market trajectory.

"Digital Transformation and Defense Modernization Fuel Embedded Systems Demand in North America"

North America held approximately 26.7% of the global Industrial Embedded Systems market in 2024, driven by strong investments in digital infrastructure and defense modernization. The U.S. remains the dominant player, with high embedded system integration across sectors such as automotive, aerospace, and industrial robotics. Canada is also investing in next-gen smart grids and advanced manufacturing. Government-backed initiatives like the CHIPS Act have further encouraged domestic semiconductor production, strengthening the embedded supply chain. Adoption of industrial IoT (IIoT) technologies and machine learning capabilities continues to transform legacy manufacturing processes. Real-time analytics, edge computing, and automation systems are becoming standard in operational environments, reinforcing North America’s strategic importance in this domain.

"Automation, Sustainability, and Smart Infrastructure Accelerate Embedded System Deployment Across Europe"

Europe captured around 21.4% of the Industrial Embedded Systems market share in 2024, driven by technological advancements in Germany, the UK, and France. Germany, known for its high-tech manufacturing ecosystem, remains a central hub for embedded controller applications in automotive and industrial robotics. France and the UK are pushing digitalization in public infrastructure and energy grids. Sustainability-focused regulations from entities like the European Commission are accelerating the use of energy-efficient embedded solutions. Additionally, the rise of electric vehicle production and Industry 5.0 initiatives are driving embedded integration. Embedded solutions are also gaining traction in smart cities and environmental monitoring across the EU, further reinforcing market penetration.

"Asia-Pacific’s Manufacturing Backbone and IoT Ecosystems Dominate the Global Embedded Systems Market"

Asia-Pacific recorded the highest volume in the Industrial Embedded Systems market, holding a substantial 41.3% share in 2024. China leads the region, with its expansive manufacturing infrastructure and major advancements in automation and robotics. Japan and South Korea are key contributors through innovation in high-performance embedded processors used in electronics and automotive sectors. India is experiencing rapid growth, driven by digital transformation in energy, telecom, and industrial automation. Widespread deployment of smart sensors, real-time monitoring systems, and AI-integrated hardware across manufacturing hubs has driven adoption. Major innovation centers in Shenzhen, Tokyo, and Bengaluru continue to fuel regional expansion, reinforcing Asia-Pacific’s lead in this evolving market.

"Infrastructure Modernization and Industrial Upscaling Promote Embedded Systems Adoption in South America"

South America accounted for approximately 5.2% of the Industrial Embedded Systems market in 2024, with Brazil leading the regional charge. The country is focusing on industrial upscaling through automation in automotive production and smart utility grids. Argentina is also experiencing steady growth, particularly in energy management and telecommunications. Embedded solutions are increasingly used in process control systems, smart metering, and industrial automation. Government-backed programs aimed at improving digital infrastructure and import incentives on electronics are encouraging broader adoption. As energy sector reforms and construction projects expand, demand for embedded control systems in power generation and distribution is rising steadily across key economies.

"Oil Sector Digitalization and Infrastructure Expansion Propel MEA Embedded Systems Market"

The Middle East & Africa region held around 5.4% of the Industrial Embedded Systems market share in 2024, driven by demand in oil & gas, construction, and infrastructure. The UAE and Saudi Arabia are spearheading embedded technology implementation in smart cities and oilfield automation. South Africa is focusing on industrial digitalization for its manufacturing and utility sectors. Countries across the GCC are embracing IoT-integrated embedded devices to enhance operational efficiency in critical energy operations. Additionally, strategic trade partnerships and local assembly incentives are supporting market development. Embedded control systems are increasingly used in HVAC systems, building automation, and security surveillance, reflecting growing technological modernization across the region.

China

Market Share: 28.6%

China leads the Industrial Embedded Systems market due to its unmatched electronics manufacturing capacity and robust automation demand in smart factories.

United States

Market Share: 21.1%

The U.S. dominates through strong innovation in defense systems, industrial IoT adoption, and local semiconductor production supported by government initiatives.

The Industrial Embedded Systems market is marked by intense competition, with over 200 active global and regional players competing for technological leadership and market share. The competitive landscape is shaped by rapid innovation cycles, with companies heavily investing in advanced product development, particularly in areas such as AI-enabled embedded platforms, real-time control systems, and edge computing integration. Industry leaders are engaging in strategic collaborations with software developers and hardware manufacturers to accelerate innovation. For example, cross-industry partnerships have been formed to co-develop embedded platforms optimized for industrial automation and Industry 4.0 frameworks.

Mergers and acquisitions remain prevalent, particularly among firms seeking to expand their embedded solution portfolios or gain access to high-growth end-user markets such as automotive, energy, and smart manufacturing. There is also a notable trend of companies establishing local manufacturing and R&D hubs in emerging economies to enhance cost efficiency and reduce supply chain vulnerabilities. Competitive differentiation is increasingly driven by the ability to deliver customizable, energy-efficient, and interoperable embedded solutions aligned with industry-specific requirements. Companies that offer secure, scalable, and modular systems are gaining prominence across both mature and developing industrial sectors.

Intel Corporation

Advantech Co., Ltd.

Renesas Electronics Corporation

STMicroelectronics N.V.

Siemens AG

Arm Ltd.

NXP Semiconductors

Texas Instruments Incorporated

Kontron AG

Microchip Technology Inc.

The Industrial Embedded Systems market is undergoing rapid transformation driven by innovations in microcontroller architectures, integrated software frameworks, and edge AI technologies. One of the most significant advancements is the integration of AI and machine learning capabilities directly into embedded devices. These intelligent systems can now perform real-time analytics on-site, reducing latency and improving decision-making speed for applications in robotics, automation, and predictive maintenance.

Another major development is the adoption of 5G-enabled embedded systems, which support ultra-reliable low-latency communication (URLLC) for mission-critical industrial applications. This technology has allowed for seamless connectivity among machines, sensors, and control units across smart factories, significantly improving efficiency and throughput. Additionally, system-on-chip (SoC) designs with built-in security features, such as hardware-based encryption modules and secure boot capabilities, are being widely implemented to combat growing cybersecurity threats in industrial environments.

The emergence of Time-Sensitive Networking (TSN) in embedded Ethernet modules ensures deterministic communication, a key requirement for synchronized manufacturing systems and automated assembly lines. Modular embedded systems with customizable I/O and ruggedized enclosures are also gaining popularity, especially in sectors like oil & gas, mining, and defense. These systems are designed for high-reliability operations in extreme environments. Collectively, these technologies are driving the shift toward autonomous, connected, and highly adaptive industrial systems.

• In March 2024, Siemens unveiled its new SIMATIC IPC BX39A embedded industrial PC, designed for edge computing in harsh factory settings. The system boasts an ultra-compact design, high shock resistance, and an extended temperature range of -25°C to 60°C, making it ideal for real-time automation environments.

• In January 2024, STMicroelectronics launched the STM32H7R/S microcontrollers featuring 600 MHz Cortex-M7 cores. These new MCUs are engineered for high-performance industrial control applications, offering advanced peripherals and real-time performance for motor drives and industrial power conversion.

• In October 2023, Advantech introduced the UNO-238 V2 edge gateway series equipped with 12th Gen Intel Core processors. These devices support AI and deep learning model inference at the edge, enabling smart energy management and equipment diagnostics in industrial applications.

• In June 2023, NXP Semiconductors released its i.MX 93 applications processors built on an energy-efficient NPU (Neural Processing Unit). These processors support next-generation HMI (Human-Machine Interface) and vision processing applications in manufacturing, helping reduce energy consumption and improve edge intelligence.

The Industrial Embedded Systems Market Report provides an in-depth analysis of a diverse and highly specialized sector that spans multiple technologies, end-use industries, and global regions. This report captures the extensive scope of embedded solutions used in industrial automation, robotics, process control, smart energy, and transportation systems. It evaluates a wide array of embedded hardware components such as microcontrollers, microprocessors, field-programmable gate arrays (FPGAs), and application-specific integrated circuits (ASICs), along with software platforms that support real-time operating systems and edge intelligence frameworks. Geographically, the report covers six major regions—North America, Europe, Asia-Pacific, South America, the Middle East, and Africa—with detailed insights into key markets like the United States, Germany, China, India, Brazil, and the UAE. It highlights both established and emerging markets, offering a granular view of local demand trends, infrastructure developments, and industrial digitization initiatives.

From an application perspective, the report addresses critical sectors such as manufacturing, automotive, oil & gas, aerospace, energy and utilities, and building automation. It also touches on newer fields like industrial IoT and autonomous systems, where embedded platforms are becoming vital for decentralized decision-making and data processing. The scope further includes an analysis of market participants, innovation trends, competitive dynamics, and opportunities arising from sustainability-focused manufacturing and digital transformation initiatives. This comprehensive coverage ensures stakeholders have a strategic understanding of where and how embedded technologies are shaping industrial growth globally.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 36,860.3 Million |

|

Market Revenue in 2032 |

USD 63,807.9 Million |

|

CAGR (2025 - 2032) |

7.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Intel Corporation, Advantech Co., Ltd., Renesas Electronics Corporation, STMicroelectronics N.V., Siemens AG, Arm Ltd., NXP Semiconductors, Texas Instruments Incorporated, Kontron AG, Microchip Technology Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |