Reports

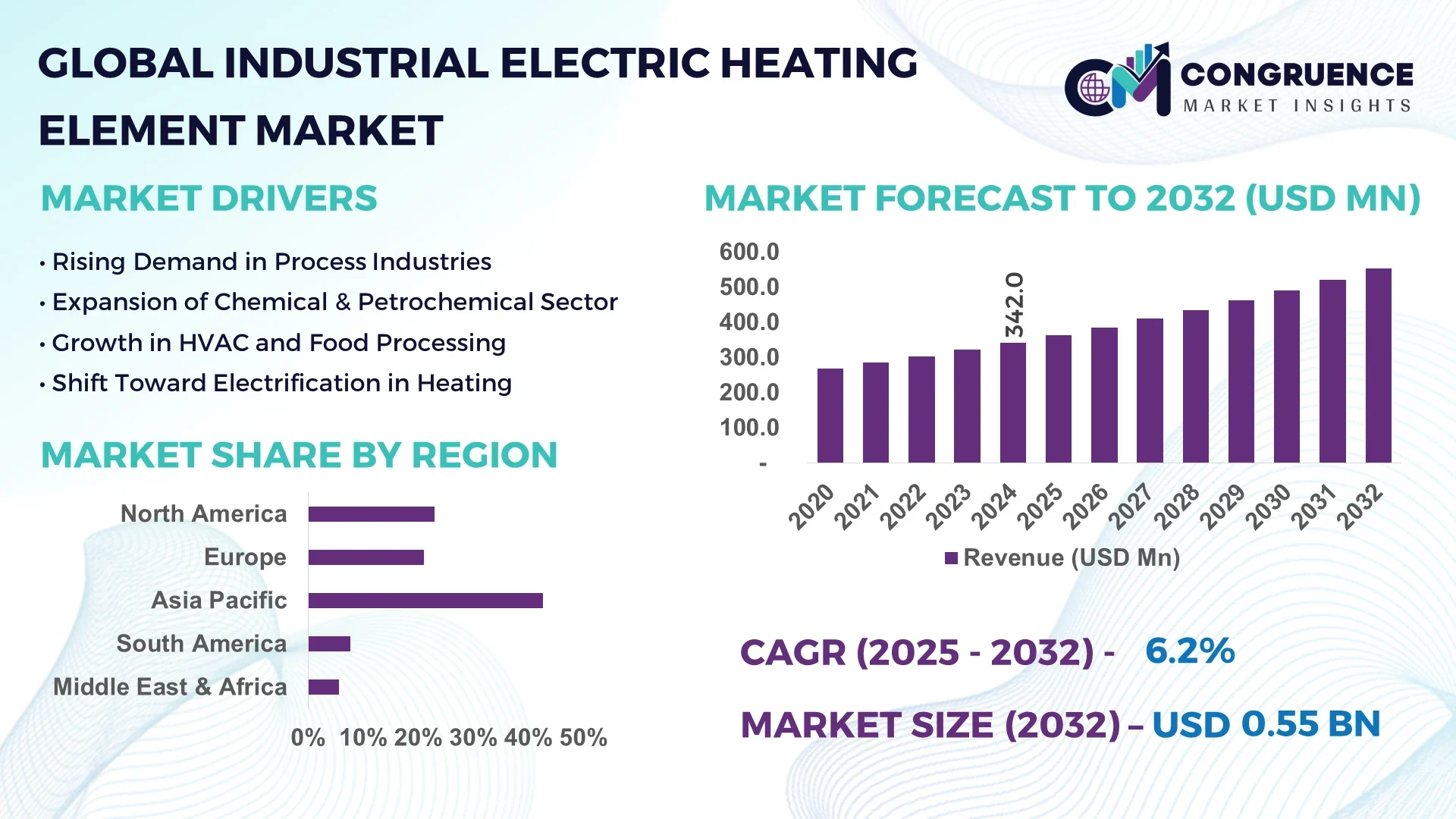

The Global Industrial Electric Heating Element Market was valued at USD 342.0 Million in 2024 and is anticipated to reach a value of USD 552.1 Million by 2032 expanding at a CAGR of 6.17% between 2025 and 2032.

China, the leading country in the Industrial Electric Heating Element Market, continues to expand its production capacity with new high‑throughput manufacturing facilities established in Jiangsu and Zhejiang provinces during 2024. Government-supported investment funds totaling over USD 200 million have been allocated specifically for the development of advanced ceramic and silicon‑based heating elements. Key applications in China include large-scale chemical processing plants, EV battery temperature control, and industrial drying systems. Additionally, technological advancements such as real‑time thermal monitoring and intelligent self‑regulating heating alloys have been successfully implemented in domestic production lines.

The Industrial Electric Heating Element Market serves critical sectors including chemicals, pharmaceuticals, food processing, plastics, oil & gas, and HVAC. Immersion heaters remain the most widely used type, particularly in chemical and plastics where they account for roughly 30% of installations, followed by tubular heaters at around 20%. In pharmaceuticals and food processing, the demand for precision temperature control has driven the adoption of new products featuring integrated PID control and quick‑response ceramic coatings. Regulatory pressures—such as the EU’s Ecodesign Directive and the U.S. Department of Energy’s energy efficiency rules—are pushing manufacturers to improve energy conversion rates and reduce thermal energy loss. Economically, rising electricity tariffs and carbon pricing are incentivizing industrial users to retrofit old heaters with modern electric elements. Geographically, Asia-Pacific continues to show dynamic consumption growth, led by China, India, and Southeast Asia due to rapid industrialization. Emerging market trends include the shift toward self‑regulating PTC (Positive Temperature Coefficient) elements and flexible heater designs for aerospace and electric vehicle applications. Over the next decade, decision-makers can expect continued emphasis on electrification, digital integration, and sustainability-driven innovations to dominate market priorities.

AI is playing an increasingly vital role in the Industrial Electric Heating Element Market by enabling smarter, more adaptive systems that enhance efficiency and performance across industrial operations. In manufacturing plants, AI-driven thermal control systems integrate sensor networks with machine‑learning algorithms to adjust heater activation in real time. For example, in industrial ovens used in metal treatment, AI models have reduced temperature overshoot by up to 15%, minimizing material waste and reducing cycle times by 8%. These improvements translate into tangible gains in energy utilization and throughput.

In equipment maintenance, predictive AI tools analyze sensor data—covering temperature, current draw, and heater lifespan—to forecast wear and schedule maintenance before failures occur. One leading heating system provider reports a 20% drop in unscheduled downtime after deploying AI-based monitoring across its electric heater arrays. Similarly, production automation has seen AI-controlled manufacturing cells calibrate heater power dynamically based on part‑specific requirements, reducing scrap rates by approximately 12% and cutting manual intervention.

Digital twins are another area where AI is reshaping the market. Advanced simulation models now replicate heater behavior under variable loads, enabling engineers to test control strategies virtually. This helps in optimizing element design and accelerating deployment cycles. Furthermore, AI-based energy optimization platforms are increasingly used by industrial facilities to balance heating demand across operations, reducing peak grid consumption by 10–18%.

Overall, the integration of AI into the Industrial Electric Heating Element Market is fostering smarter control, reduced downtime, optimized power usage, and more predictable maintenance. These concrete results are compelling decision‑makers to adopt AI-enabled heating solutions not only for operational benefits but also for aligning with sustainability and digital transformation agendas. The result is a clear shift towards intelligent, data-driven heating systems in industrial environments.

“In 2024, a European plastics manufacturer implemented an AI‑driven heating control system on its immersion heaters, reducing energy consumption by 12% and predictive maintenance alerts increased component lifespan by 18%.”

The Industrial Electric Heating Element Market dynamics revolve around rapid technological upgrade cycles, regulatory shifts towards energy efficiency, and evolving industrial needs. Demand is increasingly driven by the push for electrification and decarbonization, which emphasize transitioning from fossil-fuel-based to electric thermal processes. At the same time, industrial consumers are investing in quality-critical applications—such as pharmaceuticals and microelectronics—that require precise, programmable heating solutions. Operating costs related to electricity prices and thermal losses are influencing procurement decisions, while manufacturers are responding with improved materials (e.g., ceramic composites, nickel‑based alloys) and intelligent control systems. Sustainability mandates and carbon taxes are prompting upgrades to lower‑wattage, self‑regulating heating systems. Regional consumption shows notable divergence: Asia-Pacific remains the fastest‑growing market due to industrial expansion; North America emphasizes retrofit markets and green mandates; Europe leads with smart heating regulations. Competition is rising from gas-based systems and heat pumps, but electric heating holds an edge in fast ramp-up and programmable control. Overall, market dynamics demonstrate a shift toward smarter, cleaner, and more efficient heating solutions.

Pharmaceutical manufacturing increasingly requires tight thermal profiles during synthesis, sterilization, and drying, which has driven demand for precision-controlled Industrial Electric Heating Element Market solutions. Facilities deploying electric heating in reactors and dryers report reduced batch variability by up to 25%. This demand has led manufacturers to develop heaters with integrated PID loops, real‑time temperature feedback, and multi-zone heating control—enhancing process consistency and quality compliance. These systems now support ultra-narrow temperature bands (±0.5 °C) essential for active pharmaceutical ingredients. The result is enhanced production yield, reduced scrap rates, and improved regulatory adherence. As pharmaceutical firms continue to scale air/liquid-based production, their need for advanced electric heating elements firmly positions this driver at the forefront of industry investment in the Industrial Electric Heating Element Market.

Adoption of modern electric heating elements in the Industrial Electric Heating Element Market is hindered by high upfront capital costs. Advanced elements—such as ceramic-based modules with built‑in sensors or PTC self-regulating units—typically cost 40–60% more than traditional resistive heaters. For small‑ and mid‑sized facilities, this premium limits deployment, especially when power costs remain volatile. Additionally, integrating these smart elements requires control system upgrades, wiring changes, and training, further adding to initial expenses. As a result, companies with limited budgets often continue using older technologies, leading to underinvestment in improved operational efficiency. These financial constraints slow down the replacement cycle and hamper overall modernization efforts within the Industrial Electric Heating Element Market.

With industrial electrification and growing renewable energy capacity, there's a significant opportunity for the Industrial Electric Heating Element Market to integrate directly with solar, wind, or grid-flexibility schemes. Electric heating elements can act as dispatchable loads or thermal buffers within power systems—storing energy as heat during off-peak or renewable surplus periods. Pilot projects in Europe have demonstrated cost savings of up to 20% by coordinating electric heater cycles with PV production peaks. Moreover, government incentives—such as dispatchable load tariffs and time-of-use pricing—create incentives for industries to adopt smart electric elements. This synergy opens avenues for cogeneration of heat and grid services, positioning industrial electric heating as both a utility-scale tool and a market differentiator for plant operators.

In many jurisdictions, industrial facilities face escalating compliance costs tied to energy efficiency standards, emissions reporting, and environmental certification schemes. Compliance efforts often mandate periodic validation of heating system performance, traceability of materials, and documented calibration records. These requirements necessitate installation of sensors, logging software, and calibration protocols for electric heating elements—adding to both capital cost and operational overhead. Smaller operators find the burden particularly taxing, as retrofitting existing systems with compliance-grade components can cost 15–20% of the overall plant investment. Regulatory inconsistency across regions further complicates procurement and certification strategies, increasing the complexity for manufacturers and end‑users within the Industrial Electric Heating Element Market.

Modular and Prefabricated Deployment Accelerates Market Penetration: The adoption of modular and prefabricated construction is reshaping demand dynamics in the Industrial Electric Heating Element Market. Pre‑bent and cut elements are prefabricated off‑site using automated machines, reducing labor needs and speeding project timelines. Demand for high‑precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Integration of Smart IoT Sensors for Real-time Thermal Optimization: More than 45% of newly installed electric heating elements in 2024 include embedded IoT sensors capable of wireless telemetry. This connectivity enables operations centers to monitor heating efficiency, detect anomalies, and remotely adjust setpoints—reducing energy waste by 8–12% and proactively flagging wear before failure.

Adoption of Flexible Heaters in EV and Aerospace Manufacturing: Flexible film and silicone electric heaters are seeing double‑digit volume growth in EV battery and aerospace thermal assembly applications. Their ability to conform to curved surfaces, combined with rapid warm-up times under 60 seconds, is driving deployment across vehicle battery conditioning lines and composite material curing processes.

Rise of PTC Self-Regulating Elements in Process Safety: Self‑regulating PTC (Positive Temperature Coefficient) heating elements are gaining traction in safety-critical industrial processes. These elements automatically limit output as temperature rises, eliminating the need for external controls. In 2024, PTC heaters accounted for over 18% of new industrial installations in food and chemical sectors, up from 12% in 2022, reflecting their growing importance in safe, maintenance‑free operations.

The Industrial Electric Heating Element Market is segmented across three primary dimensions: type, application, and end-user. Each segment contributes uniquely to the market's structure and strategic focus, reflecting the diversity of industrial heating requirements across various sectors. Product types range from traditional tubular and immersion heaters to advanced flexible and cartridge heaters. Applications span core industrial processes like heat treatment, drying, distillation, and thermal management across sectors such as chemicals, oil & gas, and food processing. End-user segments encompass industries with varied temperature control needs, including manufacturing, energy, and consumer goods. Notably, customization, energy efficiency, and digital control compatibility are shaping purchasing behaviors across all segments. Segment-wise innovation and operational alignment with smart manufacturing and sustainability goals are major drivers influencing growth trajectories and investment patterns in the Industrial Electric Heating Element Market.

Tubular heaters dominate the Industrial Electric Heating Element Market, widely used for their durability and versatility in applications like chemical processing, ovens, and HVAC systems. Their ability to withstand harsh environments while delivering consistent thermal output makes them the most preferred option across multiple industries. Immersion heaters also command a significant share, primarily used for fluid heating in tanks and vessels within oil & gas and pharmaceutical sectors.

The fastest-growing product type is flexible electric heaters, particularly silicone rubber and polyimide film-based models. Their lightweight design, ability to conform to curved surfaces, and fast heating response make them ideal for EV battery systems, aerospace assemblies, and portable industrial devices. Their integration with sensors and smart controllers is accelerating demand in precision applications.

Cartridge heaters, though more niche, are vital in mold and die applications and compact heating tasks in the plastics industry. Meanwhile, band heaters and strip heaters continue to serve specialized uses such as packaging, extrusion, and food machinery, with steady adoption supported by their compatibility with cylindrical surfaces.

Process heating leads the application segment within the Industrial Electric Heating Element Market due to its critical role in chemical reactions, material synthesis, and thermal conditioning across a variety of industrial plants. Electric heating elements are valued for their clean energy usage and precise temperature control in these operations. Facilities using electric process heating report better temperature uniformity and reduced contamination risks compared to fuel-based alternatives.

The fastest-growing application is thermal management in electric vehicle (EV) manufacturing, driven by the rapid rise in EV adoption worldwide. Battery preheating, cabin comfort systems, and component testing rely on compact, efficient heating elements. Innovations in lightweight, energy-efficient heating technologies are fueling increased deployment in this sector.

Other notable applications include drying and dehumidification in the food and pharmaceutical sectors, where hygiene and exact heat delivery are paramount. Distillation and sterilization processes also utilize electric heating for its rapid response time and ease of integration into automated systems.

The manufacturing sector is the largest end-user of industrial electric heating elements, encompassing sub-industries like automotive, plastics, textiles, and electronics. Manufacturing operations require consistent and programmable heating solutions for welding, molding, drying, and thermal curing. Demand is especially high in regions with stringent emissions norms, where electric heaters provide a cleaner alternative to gas or oil-fired systems.

The fastest-growing end-user segment is the renewable energy and electric vehicle industry, where electric heaters play a critical role in battery systems, power storage, and process equipment that support clean energy transition. These industries prioritize efficiency, precision, and low emissions—all aligning with the core strengths of electric heating technology.

Other contributing sectors include pharmaceuticals, where strict thermal profiles are necessary for product quality, and food processing, which relies on electric heating for pasteurization, drying, and temperature-sensitive cooking processes. Additionally, sectors like semiconductors and aerospace use precision micro-heating systems to support highly specialized production environments.

Asia-Pacific accounted for the largest market share at 42.7% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 6.9% between 2025 and 2032.

The Asia-Pacific region's dominance stems from strong manufacturing infrastructure and demand concentration across China, India, and Southeast Asia. This includes sectors such as automotive, electronics, and chemical processing, all of which utilize industrial electric heating elements extensively. In contrast, North America is witnessing accelerated adoption of smart heating technologies, boosted by energy efficiency mandates and industrial electrification efforts. Across regions, strategic investment in sustainable heating solutions and AI-integrated control systems is influencing procurement decisions and technology upgrades. Each region’s industrial maturity, energy policy, and digital transformation readiness shape its respective growth outlook in the Industrial Electric Heating Element Market.

North America held approximately 22.3% of the global market share in 2024, driven by mature industrial sectors and increasing adoption of energy-efficient heating systems. Key industries such as food processing, pharmaceuticals, and chemicals are central to demand, with industrial facilities prioritizing retrofitting traditional systems with electric alternatives. The U.S. Department of Energy and Environment Canada have both introduced updated thermal efficiency standards for industrial heaters, promoting compliance-driven replacements. Furthermore, federal and state-level green infrastructure incentives are encouraging facilities to shift toward electric thermal systems. Technological developments, particularly the deployment of AI-powered temperature control units and smart sensors, are transforming thermal management in industrial settings. The North American Industrial Electric Heating Element Market is also benefiting from digital manufacturing trends, including predictive maintenance and automation integration across factory floors.

Europe accounted for approximately 25.4% of the global Industrial Electric Heating Element Market in 2024, with strong market activity concentrated in Germany, the United Kingdom, and France. These countries are actively transitioning to clean industrial heating systems in alignment with the European Green Deal and Ecodesign Directive. Regulatory initiatives encourage the use of energy-efficient electric heating components across industrial applications. Germany, in particular, has emerged as a leader in integrating industrial heating with renewable power sources and digital grid frameworks. Advanced ceramic and PTC-based heating elements are gaining traction in food, plastics, and chemical processing. The UK’s aggressive decarbonization goals are further driving adoption of low-emission heating alternatives. Across the continent, the use of IoT-connected heaters with real-time diagnostics and system calibration is contributing to optimized thermal efficiency and reduced operational downtimes.

Asia-Pacific, with a commanding 42.7% share of the global Industrial Electric Heating Element Market in 2024, leads due to high-volume manufacturing and industrial expansion in China, India, and Japan. China remains the top consumer, fueled by its vast electronics and automotive industries, as well as its large-scale chemical and plastics production bases. India is quickly scaling its manufacturing capacity, bolstered by government schemes promoting domestic production and electrification. Regional trends such as automation of thermal processes, rapid infrastructure development, and expansion of industrial parks are driving the surge in demand for efficient electric heating solutions. Innovation hubs in South Korea and Japan are investing in nano-ceramic heating components and flexible thermal devices for advanced sectors like semiconductors and electric vehicles. The Asia-Pacific region is expected to continue dominating volume consumption due to its rapid industrialization and favorable policy landscape supporting low-emission technologies.

In 2024, South America represented approximately 5.2% of the global Industrial Electric Heating Element Market, with Brazil and Argentina emerging as key contributors. Brazil’s industrial sector—particularly in petrochemicals, food processing, and mining—is driving demand for efficient and safe electric heating elements. Infrastructure expansion in the southern regions and increased investment in energy grid modernization have led to higher adoption of electric thermal systems. Argentina is seeing increased use of industrial electric heating in agro-processing and beverage production facilities. Trade policies favoring equipment imports, coupled with financial incentives for sustainable technologies, are shaping procurement trends. Regional challenges such as energy security and cost efficiency are further prompting industries to invest in programmable and automated heating systems that offer energy control, safety, and reliability.

Middle East & Africa accounted for approximately 4.4% of the global Industrial Electric Heating Element Market in 2024. Countries like the UAE and South Africa are at the forefront of growth, supported by large-scale infrastructure projects and industrial diversification efforts. The oil & gas industry remains a significant end-user, especially for immersion and tubular heaters used in pipeline and refinery applications. Simultaneously, the construction boom in Gulf countries is contributing to the use of electric heating systems in HVAC and building material production. Governments across the region are implementing national energy strategies aimed at reducing fossil fuel reliance—this includes integrating electric heating elements into new industrial plants. Technological modernization programs are underway in both public and private sectors, with AI and IoT integration becoming gradually more common. Trade partnerships, especially between Gulf states and Asian suppliers, are improving access to high-performance electric heating components.

China – 31.5% Market Share

High production capacity and robust demand from chemical, electronics, and automotive sectors.

Germany – 14.2% Market Share

Strong end-user demand and regulatory-driven push for sustainable, energy-efficient heating systems.

The Industrial Electric Heating Element Market features a moderately fragmented competitive environment, with over 60 active players globally ranging from multinational corporations to specialized regional firms. Leading companies maintain competitive advantages through extensive product portfolios, global distribution networks, and ongoing innovation in energy-efficient technologies. A significant portion of market players are focusing on strategic collaborations, especially with OEMs and automation firms, to co-develop customized heating elements for evolving industrial applications. Several firms have announced mergers and acquisitions to expand their presence in emerging markets and diversify their product lines, particularly in Asia-Pacific and the Middle East.

Key market participants are heavily investing in research and development, especially in ceramic-based, flexible film, and PTC (Positive Temperature Coefficient) heating technologies. Additionally, manufacturers are focusing on smart electric heating systems with built-in diagnostics, remote control capabilities, and AI-assisted regulation to enhance energy efficiency and safety. Technological differentiation, reliability, and ease of integration are shaping competitive dynamics. Companies that provide tailored solutions for complex industrial heating requirements, such as in chemical, petrochemical, and electronics sectors, are gaining market share. Overall, competition is intensifying with innovation, product differentiation, and geographic expansion as primary strategic levers.

Watlow Electric Manufacturing Company

Chromalox, Inc.

Backer Group

Thermon Group Holdings, Inc.

NIBE Industrier AB

Zoppas Industries S.p.A.

Tutco Heating Solutions Group

Tempco Electric Heater Corporation

Eltherm GmbH

Heatrex, Inc.

Industrial Heater Corporation

Minco Products, Inc.

Omega Engineering, Inc.

The Industrial Electric Heating Element Market is witnessing transformative growth driven by innovations in smart heating technologies, materials engineering, and process automation. Traditional resistance wire-based elements are evolving into high-precision, digitally integrated systems capable of real-time diagnostics, self-regulation, and energy optimization. The introduction of PTC ceramic heating elements is gaining traction across applications requiring stable temperature profiles and safety against overheating, such as in plastics processing and food industries.

Another key advancement is in nano-ceramic and flexible heating films, which offer compact form factors, uniform heat distribution, and fast response times. These are increasingly used in confined or uniquely shaped industrial spaces where conventional heaters are less effective. Additionally, the integration of IoT-enabled controllers allows operators to monitor temperature patterns remotely, enabling predictive maintenance and reducing unplanned downtimes.

Induction and infrared heating are also gaining prominence in applications demanding contactless and precise thermal transfer, especially in semiconductor manufacturing and chemical processing. The use of AI algorithms for process optimization and energy load balancing is being piloted across advanced manufacturing facilities. Furthermore, materials such as Incoloy, stainless steel, and magnesium oxide are being continuously refined for better corrosion resistance and longer service life. These technological advancements are aligning with global energy efficiency mandates and sustainability initiatives, redefining how industries approach process heating.

• In February 2024, Watlow announced the launch of its new ASPYRE® Smart Control Series for electric heaters, offering improved temperature uniformity and real-time performance analytics. The system supports multiple communication protocols for seamless integration into smart factory ecosystems.

• In May 2024, Chromalox expanded its production facility in Ogden, Utah, adding over 60,000 sq. ft. to increase manufacturing capacity for industrial immersion and circulation heaters. The expansion aims to meet rising demand from North American and Latin American markets.

• In August 2023, NIBE Industrier AB acquired 80% of shares in Heatron, Inc., a U.S.-based thermal solution provider, to strengthen its footprint in North American industrial and medical heating markets. The acquisition allows NIBE to offer broader customized heating solutions.

• In November 2023, Zoppas Industries introduced a new range of ultra-thin flexible heating films for industrial automation applications. The solution targets energy savings of up to 18% through faster heat-up times and improved thermal conductivity.

The Industrial Electric Heating Element Market Report offers a comprehensive examination of the market landscape, focusing on product types, applications, technologies, and regional dynamics. It covers key segments including tubular heaters, cartridge heaters, band heaters, flexible heaters, immersion heaters, and strip heaters, providing insights into their usage across various industries such as chemicals, food processing, automotive, electronics, plastics, and pharmaceuticals.

Geographically, the report spans major regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering a detailed assessment of each region’s demand drivers, infrastructure trends, and technological adoption. The report also highlights emerging opportunities in smart and energy-efficient heating solutions, driven by rising automation and environmental regulations.

In addition to established applications like industrial drying and fluid heating, the report includes analysis of emerging niche areas such as electric vehicle battery thermal management and semiconductor fabrication. It also explores how advancements in IoT, AI, and sustainable materials are reshaping market offerings and strategies. Decision-makers gain critical intelligence on market entry barriers, competitive intensity, and innovation trends, helping them to navigate complex procurement environments and long-term investment planning.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 342.0 Million |

| Market Revenue (2032) | USD 552.1 Million |

| CAGR (2025–2032) | 6.17% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape, Technological Insights, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Watlow Electric Manufacturing Company, Chromalox, Inc., Backer Group, Thermon Group Holdings, Inc., NIBE Industrier AB, Zoppas Industries S.p.A., Tutco Heating Solutions Group, Tempco Electric Heater Corporation, Eltherm GmbH, Heatrex, Inc., Industrial Heater Corporation, Minco Products, Inc., Omega Engineering, Inc. |

| Customization & Pricing | Available on Request (10% Customization is Free) |