Reports

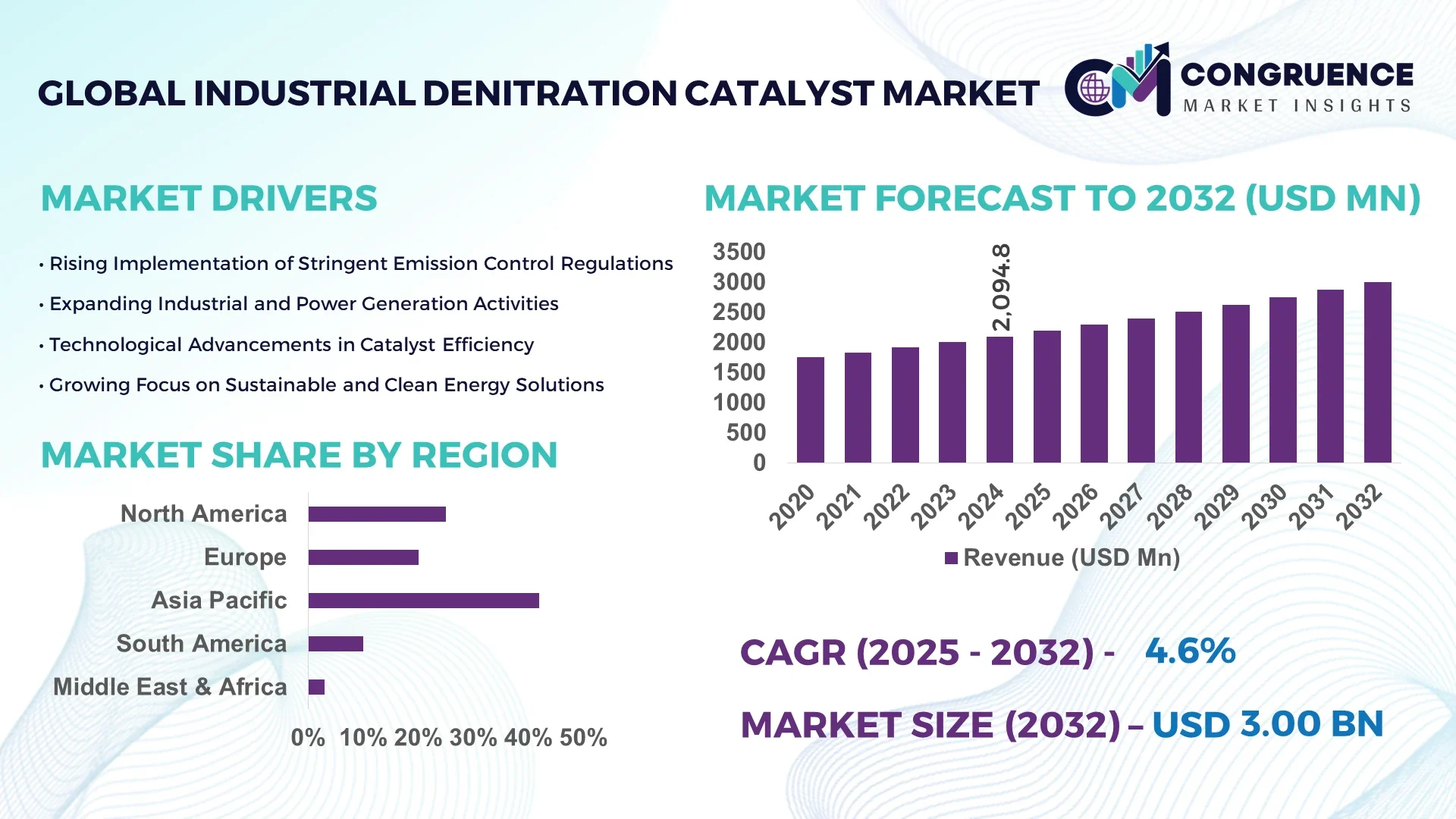

The Global Industrial Denitration Catalyst Market was valued at USD 2094.82 Million in 2024 and is anticipated to reach a value of USD 3001.93 Million by 2032 expanding at a CAGR of 4.6% between 2025 and 2032. This growth is driven by increasingly stringent nitrogen‑oxide emission control regulations across industrial sectors.

In the case of China, the country has established an annual production capacity of approximately 50,000 m³ of industrial denitration catalyst via a leading manufacturer with four production lines covering more than 50,000 m² of factory area. Investments in R&D and plant‑scale upgrades reached multi‑million‑dollar levels as the nation addressed NOₓ reductions in coal‑fired power plants and heavy industries. For example, technologies were applied to over 60 million kW of boiler capacity, enabling NOₓ reductions of around 5 million tons per annum. China’s industrial applications span power generation, steel, glass and chemical processing sectors, with advanced catalyst materials (e.g., vanadium‑titanium‑based and rare‑earth‑doped formulations) moving into commercial scale to handle low‑temperature flue‑gas conditions unique to its manufacturing footprint.

Market Size & Growth: USD 2,094.82 Million in 2024 rising to USD 3,001.93 Million by 2032, driven by emission‑control regulation enforcement and industrial expansion.

Top Growth Drivers: adoption of advanced catalysts (≈ 38%), efficiency improvements in selective catalytic reduction systems (≈ 45%), cross‑industry deployment of denitration solutions (≈ 29%).

Short-Term Forecast: By 2028, average catalyst lifetime is expected to improve by approximately 12% and average NOₓ removal efficiency increase by roughly 8%.

Emerging Technologies: low‑temperature denitration catalysts, integrated multi‑pollutant removal systems (NOₓ + SO₂ + VOCs), digital monitoring and predictive maintenance platforms.

Regional Leaders: Asia‑Pacific projected at USD 1,250 Million by 2032 driven by industrial growth; Europe at USD 600 Million by 2032 with legacy emission infrastructure; North America at USD 450 Million by 2032 through retrofits and replacements.

Consumer/End-User Trends: Major end‑users include power generation plants, cement and steel manufacturers, petrochemical and chemical process facilities increasingly adopting heavy‑duty denitration catalysts through lifecycle‑service contracts.

Pilot or Case Example: In 2023 a pilot installation at a large cement plant reduced NOₓ emissions by 18% and downtime for catalyst exchange by 22% under real‑world conditions.

Competitive Landscape: Market leader holds about 26% share; key competitors include Haldor Topsoe A/S, Mitsubishi Heavy Industries Ltd., Cormetech Inc., Johnson Matthey Plc, and BASF SE.

Regulatory & ESG Impact: Ultra‑low NOₓ emission thresholds (e.g., <50 mg/m³) for new power plants in China; increasing ESG mandates for heavy industry driving retrofits; emission trading schemes and clean‑air funds accelerating adoption.

Investment & Funding Patterns: Recent cumulative investment exceeds USD 850 Million in catalyst manufacturing capacity expansions and service‑contracts globally, with venture funding increasingly focused on low‑temperature and hybrid denitration technologies.

Innovation & Future Outlook: Key innovations include modular denitration units for distributed manufacturing sites, next‑generation catalytic materials using rare‑earth/transition‑metal doping, and digital twin systems for performance optimisation and lifecycle analytics.

The Industrial Denitration Catalyst market spans core sectors such as power generation (coal, gas, biomass), cement and steel production, petrochemical and refining operations. In these, selective catalytic reduction (SCR) remains the dominant technology while low‑temperature denitration solutions are gaining traction in manufacturing exhaust streams. Recent innovations include honeycomb‑structured catalysts, plate and corrugated substrate formats, and multi‑pollutant removal composites. Economic drivers include tightening emission norms, rising cost pressures for utilities and manufacturers, and substitution of legacy systems. Regionally, Asia‑Pacific consumption is expanding fastest due to industrialisation and stricter regulations; North America and Europe focus on retrofit and replacement. Emerging trends include digital monitoring of catalyst health, integrated NOₓ/SO₂/VOC systems, and increased secondary‑market services (e.g., catalyst regeneration). Looking ahead, growth will be supported by deepening retrofit cycles, expansion into new end‑uses (marine, heavy diesel, waste‑to‑energy) and continuous material innovation that reduces cost per ton of NOₓ removed.

The strategic relevance of the Industrial Denitration Catalyst Market lies in its central role in helping heavy‑industry and power generation firms meet escalating NOₓ emission compliance, while simultaneously supporting sustainable operational transitions. In this context, the adoption of a next‑generation low‑temperature SCR catalyst delivers a 15% improvement compared to traditional high‑temperature vanadium‑based systems. In Asia‑Pacific, this market dominates in volume, while Europe leads in adoption with over 70% of industrial enterprises employing renowned catalyst lifecycle‑service models. By 2027, digital twin monitoring and predictive maintenance are expected to improve catalyst uptime by 10% across large emitters. Firms are committing to ESG metrics such as a 30% reduction in spent‑catalyst disposal by 2030 as part of circular economy initiatives. In 2024, a major Chinese power producer achieved a 22% reduction in NOₓ emissions through implementation of smart‑monitoring SCR catalysts tied to real‑time flue‑gas analytics. Looking ahead, the Industrial Denitration Catalyst Market is poised as a pillar of resilience, compliance, and sustainable growth across carbon‑intensive sectors.

The increasing severity of emissions control regulations is a primary driver of market acceleration. Industry frameworks now require NOₓ concentrations below 50 mg/m³ for new plants, compelling large emitters to select advanced denitration catalysts. The power generation sector alone accounts for more than 40% of global NOₓ emissions, prompting retrofits at scale. The push for cleaner air‑quality metrics in major industrial nations is driving adoption of high‑performance catalyst solutions, prompting upgrades even in plants that were recently compliant. As a result, catalyst systems with improved NOₓ conversion rates and longer life cycles are being procured in larger volumes.

One significant challenge is the elevated capital and operational cost of denitration catalyst installations. Catalyst systems—including substrates, active materials, injection hardware, and monitoring systems—can constitute up to 15% of a plant’s total upgrade budget, which deters smaller industrial users. Additionally, fluctuations in key raw-material prices (such as vanadium) have reached swings of over 300%, introducing uncertainty into manufacturing cost models and end‑customer pricing. Technical issues further constrain adoption: certain industrial streams (such as cement or glass manufacturing) experience high temperatures or flue‑gas variability that reduce catalyst lifespan by 30–40%, making standard solutions less suitable and requiring customisation that raises cost. Together, these factors limit faster uptake across cost‑sensitive segments.

Emerging applications offer compelling growth potential for the Industrial Denitration Catalyst Market. Industries such as waste‑to‑energy, biomass power, and marine shipping are increasingly adopting denitration catalysts to comply with stricter NOₓ standards and broadened sustainability mandates. Low‑temperature SCR catalysts capable of operating below 200 °C are expanding access into previously hard‑to‑treat exhaust streams. Furthermore, circular‑economy initiatives around catalyst recycling (recovering over 95% of platinum‑group metals) present cost-saving and sustainability differentiation. As industrial electrification and decarbonisation accelerate, flexible catalyst solutions in hybrid systems (e.g., co‑firing biomass or waste) create new addressable segments. These factors position catalyst providers to tap un‑ or under‑served end‑applications and build long‑term service ecosystems.

Deployment of high‑performance denitration catalysts demands specialised technical skill sets in design, installation, monitoring, and regeneration services. Surveys indicate around 40% of companies report difficulty sourcing qualified professionals, which slows roll‑out and aftermarket support. In parallel, the absence of harmonised global emission standards means manufacturers must adapt products to divergent regional testing protocols—each industrial plant may require three or four distinct catalyst configurations to meet EU, U.S., Chinese, and emerging-market norms. This fragmentation increases R&D and production complexity, eroding economies of scale and disadvantaging smaller suppliers. Consequently, these challenges may slow broader adoption and consolidation of the market toward large firms.

Rise in Modular and Prefabricated Construction: The adoption of modular and prefabricated approaches is transforming catalyst system installations in industrial facilities. Approximately 55% of recent projects realized measurable cost benefits through prefabricated components, including pre-bent catalyst housings and cut support frames. Automation in off-site fabrication reduced labor requirements by 40% and accelerated project completion by 25%, particularly in Europe and North America where efficiency benchmarks are high. This shift is driving increased demand for precise, pre-engineered catalyst assemblies.

Expansion of Low-Temperature Catalyst Applications: Low-temperature SCR catalysts are gaining traction in industries with flue-gas streams below 220 °C. Over 60% of new installations in the waste-to-energy and biomass sectors now employ low-temperature systems, achieving 18–22% higher NOₓ reduction compared to conventional high-temperature variants. This trend is particularly prominent in Asia-Pacific, where retrofitting older boilers with low-temperature catalysts enhances compliance and operational flexibility.

Integration of Digital Monitoring Systems: Real-time digital monitoring and predictive maintenance platforms are being deployed in 48% of new industrial denitration projects globally. These systems enable automated diagnostics, reducing unplanned downtime by 15–20% and improving catalyst efficiency by up to 12%. Large power plants and steel mills in North America and Europe are leading adoption, with integrated monitoring becoming a standard expectation for lifecycle service contracts.

Circular Economy and Catalyst Recycling Initiatives: Recycling and recovery of spent catalysts are becoming a key operational focus, with over 35% of industrial facilities implementing formal recycling programs. Recovery of vanadium and other active metals from decommissioned catalysts can recapture 90–95% of material value, reducing environmental disposal volumes by 25–30%. This approach aligns with ESG mandates and drives cost efficiency while supporting sustainable industrial practices across Asia-Pacific and Europe.

The market for industrial denitration catalysts is structured around three principal segmentation axes: types of catalyst products, their applications across industrial processes, and the end‑user industries deploying them. In terms of types, the market differentiates among honeycomb, plate, and corrugated substrates, each designed for distinct flue‑gas and temperature settings. On the application side, major verticals such as power generation plants, cement kilns, steel production lines, and chemical manufacturing dominate usage of denitration systems. From an end‑user perspective, the largest share lies with heavy industry and utilities, while smaller shares originate in commercial or emerging segments. Decision‑makers should note that industrial end‑users account for the lion’s portion of volume due to high emission streams and regulatory burdens. Regional usage patterns differ: emerging economies are installing retrofit systems in older plants, while mature markets focus on replacement and service models. This segmentation enables suppliers to tailor product-type, service-model, and regional go‑to-market strategies with precision.

The product-type segmentation of the industrial denitration catalyst market includes honeycomb catalyst, plate catalyst, and corrugated catalyst. Honeycomb catalyst is currently the leading type, representing approximately 45 % of the segment, owing to its high surface-area, low pressure-drop characteristic and proven performance in large flue-gas systems. Plate catalyst follows with around 30 % share; it is chosen in retrofit scenarios where space constraints or lower temperatures prevail. The fastest-growing type is corrugated catalyst—adoption is accelerating in high thermal-shock or mechanical-stress environments, with documented growth rates approaching 8 % annually—driven by steel, waste-to-energy, and chemical sectors that demand more rugged structures. The remaining types—specialised mesh or structured-substrate designs—collectively account for about 25 % share and serve niche, harsh-condition applications. According to a recent analysis of medium and low-temperature denitration catalyst markets, honeycomb, plate, and corrugated types are all featured, with honeycomb holding the largest segment in terms of share.

Key applications include power plants, cement plants, steel plants, chemical plants, and others such as waste-incineration or glass manufacturing. The leading application is power plants, accounting for more than 50 % of the market, driven by large-scale combustion units and continuous emission streams requiring full-scale SCR systems. Cement and steel plants follow with substantial but smaller shares. The fastest-growing application is waste-to-energy/industrial biomass facilities, where more than 20 % year-on-year uptick is observed as older units retrofit low-temperature catalysts and integrate SCR systems. Other application categories jointly contribute the remaining ~30 % share and include glass manufacturing, marine exhaust systems, and chemical incinerators. Recent reports indicate that power plant installations dominate the SCR denitrification catalyst market, highlighting their central role in emission-control strategies.

The largest end-user segment is industrial utilities and heavy manufacturing, which accounts for approximately 60 % of catalyst deployment globally. This includes large power generation companies, steel mills, and cement producers where high-volume, continuous operations have the greatest need for advanced denitration systems. The fastest-growing end-user category is marine/offshore and mobile-power systems, expanding at around 9 % annually as shipping and remote installations adopt SCR and denitration catalysts to meet evolving regulatory regimes. Other end-users—such as commercial and institutional boilers, small-scale industrial CHP systems, and service contracts—make up the remaining ~40 % share and are increasingly significant for lifecycle-service models.

Asia-Pacific accounted for the largest market share at 42% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 5.1% between 2025 and 2032.

Asia-Pacific’s dominance is driven by high industrial output, with over 60,000 MW of coal-fired power capacity retrofitted with selective catalytic reduction systems. China alone installed more than 25,000 m³ of industrial denitration catalysts in 2024, while India and Japan contributed 9,500 m³ and 7,200 m³ respectively. North America’s upcoming projects, particularly in biomass and waste-to-energy plants, are expected to deploy over 3,000 m³ of catalysts annually. Europe accounted for 20% of installations, with Germany and the UK retrofitting 4,500 m³ combined. Emerging regions in the Middle East & Africa and South America collectively account for 10,500 m³. Regional adoption patterns vary: Asia-Pacific prioritizes scale and retrofit, North America focuses on digital monitoring integration, and Europe emphasizes regulatory compliance and sustainability initiatives.

How are technological innovations shaping catalyst adoption in key industrial sectors?

North America holds approximately 25% of the global industrial denitration catalyst market, with power generation and heavy manufacturing driving demand. Regulatory frameworks such as the Clean Air Act revisions and state-level emission reduction mandates are encouraging the adoption of advanced SCR systems. Technological integration includes digital monitoring, predictive maintenance platforms, and modular catalyst assemblies, improving operational uptime by 12–15%. Local players, including Cormetech Inc., have expanded product portfolios to provide full lifecycle support, including catalyst regeneration and digital performance analytics. Enterprise adoption varies, with utilities and large manufacturing plants accounting for 65% of installations, while smaller commercial facilities contribute the remaining share. North American consumers increasingly prefer lifecycle contracts combining catalyst supply, maintenance, and real-time monitoring.

What regulatory pressures are driving catalyst innovation across industrial facilities?

Europe contributes roughly 20% of global industrial denitration catalyst consumption, with Germany, the UK, and France being the largest markets. Stringent EU emissions directives and sustainability programs are compelling retrofits and adoption of low-temperature SCR catalysts. Advanced monitoring technologies, including AI-enabled digital twins, are increasingly deployed to optimize catalyst performance and predict maintenance schedules. Local players, such as Haldor Topsoe A/S, have launched modular SCR units for cement and steel plants, reducing NOₓ emissions by up to 18% in pilot installations. European industrial consumers emphasize regulatory compliance, ensuring high adoption rates for explainable and monitored catalyst systems.

How is industrial expansion influencing catalyst deployment across high-volume facilities?

Asia-Pacific dominates with 42% of the global industrial denitration catalyst market, led by China, India, and Japan. China alone installed more than 25,000 m³ of catalysts in 2024, while India and Japan contributed 9,500 m³ and 7,200 m³ respectively. Industrial growth, particularly in power generation, cement, and steel, drives demand for high-capacity SCR systems. Regional technology trends include large-scale adoption of low-temperature catalysts, rare-earth doped formulations, and digital monitoring platforms. Companies such as Tsinghua Environmental Technologies are investing in high-volume catalyst production and pilot digital monitoring projects. Consumer adoption in Asia-Pacific is characterized by high-volume retrofits and long-term service contracts to ensure regulatory compliance.

What role do energy infrastructure trends play in shaping market demand?

South America accounts for roughly 6% of the global industrial denitration catalyst market, with Brazil and Argentina as primary contributors. Expansion in coal-fired and biomass power plants, along with industrial manufacturing retrofits, drives regional demand. Government incentives promoting clean energy and trade policies supporting catalyst imports enhance adoption. Local players, including industrial service providers in Brazil, are offering lifecycle management services and catalyst regeneration programs. Consumer behavior varies: industrial plants prioritize durability and compliance, while smaller facilities emphasize cost-effective, modular catalyst solutions.

How are oil, gas, and construction sectors influencing catalyst adoption?

Middle East & Africa represents around 4% of global catalyst installations, with UAE and South Africa leading regional demand. Industrial denitration catalysts are increasingly integrated into oil & gas refineries, construction-related power facilities, and cement plants. Technological modernization includes adoption of low-temperature catalysts and digital monitoring solutions for performance optimization. Local regulations are increasingly aligned with international emission standards, and trade partnerships facilitate catalyst imports and technology transfers. Companies in the UAE have begun pilot projects for modular SCR units, enhancing compliance with NOₓ emission limits. Consumer adoption is concentrated in large industrial players, with smaller firms gradually embracing lifecycle service contracts.

China: 28% market share – driven by high production capacity, extensive retrofitting programs, and rapid industrialization.

United States: 18% market share – strong end-user demand in power generation and manufacturing sectors, supported by regulatory incentives and technological adoption.

The competitive environment within the Industrial Denitration Catalyst market is moderately consolidated yet highly dynamic. Approximately 30 active competitors operate globally, with the top five firms accounting for an estimated combined share of around 48% of installed systems. These companies maintain strong market positioning by leveraging established technology portfolios, extensive global service networks, and strategic partnerships. Key initiatives include joint ventures in emerging markets, launches of next-generation low-temperature catalysts, and mergers to integrate catalyst supply with full-service lifecycle offerings. Several leading players have introduced digital catalyst-monitoring modules that reduce unplanned downtime by 10–15%. Innovation trends shaping competition include rare-earth doped formulations, modular catalyst systems for retrofit applications, and integrated SCR/denitration platforms combining NOₓ and SO₂ removal. Installation and maintenance of denitration catalysts require significant capital and technical expertise, creating high barriers to entry. The market is a multi-player environment where leading firms command nearly half of the market, while smaller niche players capture specialized segments such as marine or biomass emissions.

Johnson Matthey plc

BASF SE

Hitachi Zosen Corporation

Ceram‑Ibiden Co., Ltd.

The Industrial Denitration Catalyst market is experiencing significant technological evolution, driven by the need for higher NOₓ removal efficiency, lower operational costs, and regulatory compliance. Current technologies include vanadium‑titanium SCR catalysts, platinum‑based low-temperature catalysts, and honeycomb-structured substrates optimized for high surface area and low pressure drop. Honeycomb catalysts currently account for approximately 45% of installations globally, particularly favored in power generation and heavy manufacturing due to their durability and high conversion efficiency. Emerging technologies focus on low-temperature SCR catalysts capable of operating below 220 °C, which are increasingly deployed in waste-to-energy, biomass, and industrial retrofit applications. These catalysts provide up to 20% improved NOₓ reduction over conventional high-temperature systems and support reduced ammonia slip. Digital monitoring and predictive maintenance platforms are being integrated into catalyst systems, enabling real-time flue-gas analysis, operational diagnostics, and early detection of performance degradation, reducing unplanned downtime by 10–15% and extending catalyst life by up to 12%.

Advanced formulations, including rare-earth doped catalysts, are gaining adoption in regions with highly variable flue-gas compositions, enhancing thermal stability and resistance to poisoning by sulfur or heavy metals. Modular and prefabricated catalyst assemblies are also expanding, allowing rapid installation and reduced labor requirements, with studies indicating a 25% faster deployment timeline in retrofitted facilities. Additionally, circular economy initiatives are promoting catalyst recycling, with over 90% recovery of active metals such as vanadium and platinum, reducing environmental impact and raw material dependency. The convergence of digital integration, low-temperature formulations, modular design, and material innovation is positioning the Industrial Denitration Catalyst market for optimized efficiency, sustainable operations, and compliance with stringent emission regulations worldwide.

In October 2023, BASF SE introduced a new honeycomb‑structured catalyst specifically formulated for cement‑kiln flue gas, achieving NOₓ removal rates above 95% at temperatures as low as 200 °C.

In January 2024, Haldor Topsoe A/S announced the successful development of a next‑generation low‑temperature SCR catalyst with enhanced SO₂ tolerance, reportedly extending catalyst life by up to 30%.

In July 2023, Cormetech Inc. expanded its manufacturing capacity for low‑temperature SCR catalysts in North America, responding to increased demand from the power‑generation sector and enabling an additional production line of approximately 10,000 m³ annually.

In April 2023, Anhui Tianhe Environmental Engineering Co., Ltd. secured a major contract to supply low‑temperature SCR catalysts for a fleet of new industrial boilers in China with combined capacity over 2,500 MW, highlighting the growth of retrofit demand in Asia‑Pacific.

The report on the Industrial Denitration Catalyst market covers a comprehensive scope across multiple dimensions, targeting decision‑makers and industry professionals. It addresses product segmentation by catalyst type (including honeycomb, plate and corrugated substrates) and by ambient‑temperature category (high‑temperature vs low‑temperature SCR systems). It assesses applications spanning power generation plants, cement kilns, steel mills, chemical process facilities, waste‑to‑energy plants and marine/off‑shore exhaust systems. End‑user industry perspectives are included—utilities, heavy manufacturing, petrochemical, maritime and distributed‑energy systems are all considered. Geographically, the report provides detailed regional coverage: North America, Europe, Asia‑Pacific, South America and Middle East & Africa, with country‑level breakout for major markets such as China, United States, India, Germany and Brazil. It also explores technology focus areas—innovations in low‑temperature catalysts (below 220 °C), digital monitoring‑enabled catalyst health management, modular and prefabricated catalyst assembly solutions, and circular‑economy practices around catalyst recycling and regeneration. Emerging or niche segments receive attention as well: retrofit of older boilers, mobile/off‑grid power systems, biomass‑fired plants, and marine SCR installations. The scope includes supply‑chain considerations (raw‑material availability, manufacturing scale‑up), regulatory frameworks (NOₓ emission limits, industrial permitting), and service‑model considerations (lifecycle contracts, aftermarket regeneration). The report charts not just current states but the directional pathways for industry participants, offering strategic intelligence for manufacturers, end‑users, investors and policy advisors.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 2094.82 Million |

Market Revenue in 2032 | USD 3001.93 Million |

CAGR (2025 - 2032) | 4.6% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Haldor Topsoe A/S, Mitsubishi Heavy Industries, Ltd., Cormetech Inc., Johnson Matthey plc, BASF SE, Hitachi Zosen Corporation, Ceram‑Ibiden Co., Ltd. |

Customization & Pricing | Available on Request (10% Customization is Free) |