Reports

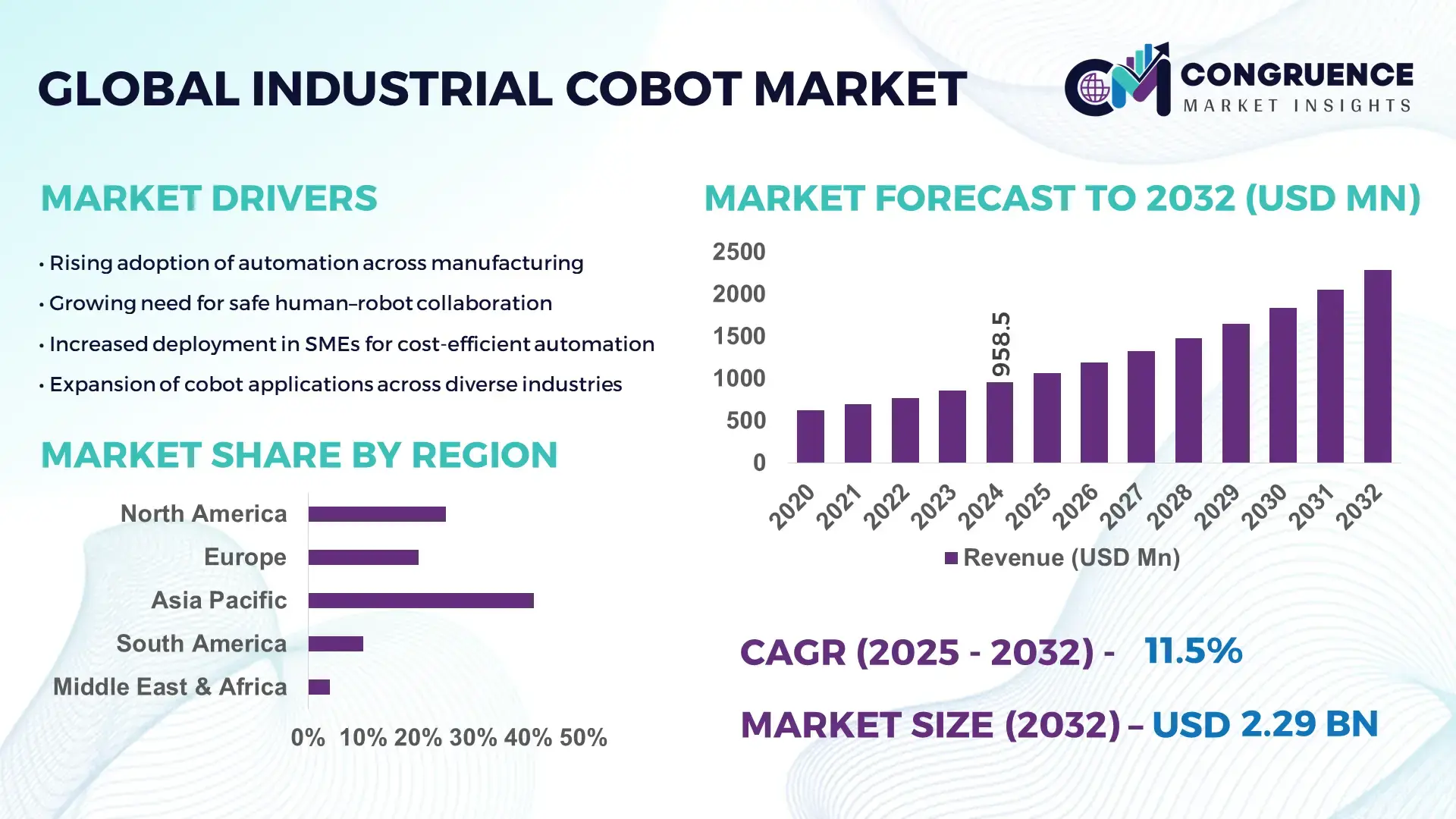

The Global Industrial Cobot Market was valued at USD 958.52 Million in 2024 and is anticipated to reach a value of USD 2289.82 Million by 2032 expanding at a CAGR of 11.5% between 2025 and 2032. This growth is supported by rapid automation adoption across manufacturing-intensive industries.

Japan maintains unmatched leadership in industrial cobot production, supported by advanced robotics engineering, long-term automation investments exceeding USD 4.5 billion annually, and over 420,000 operational industrial robots deployed across automotive, electronics, and precision manufacturing. The country’s cobot ecosystem benefits from high-volume component fabrication, strong R&D expenditure accounting for 3% of its GDP, and industry-wide integration of motion-control systems capable of reducing production cycle time by up to 25%. Japan’s domestic manufacturers also deploy cobots in over 63% of large-scale automotive assembly lines, accelerating adoption across precision machining, semiconductor handling, and electronics packaging.

• Market Size & Growth: Market valued at USD 958.52 Million in 2024, projected to reach USD 2289.82 Million by 2032 at 11.5% CAGR, driven by increasing automation demand.

• Top Growth Drivers: 38% rise in SME automation adoption, 27% efficiency improvement in assembly workflows, 33% reduction in operational bottlenecks.

• Short-Term Forecast: By 2028, cobot-enabled operations are expected to deliver up to 22% cost reduction and 30% throughput improvement in high-mix manufacturing.

• Emerging Technologies: AI-driven adaptive motion control, vision-guided cobot inspection systems, and edge-embedded predictive-maintenance software.

• Regional Leaders: Asia-Pacific projected at USD 1.08 Billion by 2032 with strong electronics adoption; North America to reach USD 640 Million with rising warehouse automation; Europe expected at USD 520 Million supported by machining upgrades.

• Consumer/End-User Trends: Strong traction from automotive, electronics, and metalworking sectors adopting flexible cobots for precision tasks and human–machine collaboration.

• Pilot or Case Example: A 2024 automotive assembly pilot achieved a 28% cycle-time reduction through cobot-enabled material handling integration.

• Competitive Landscape: Market leader holds approx. 42% share, followed by major players including FANUC, ABB, Yaskawa, Techman Robot, and KUKA.

• Regulatory & ESG Impact: Safety-compliant cobot certifications and government incentives for low-energy automation accelerating deployments.

• Investment & Funding Patterns: Recent investments surpass USD 1.4 Billion, with growing financing into AI-cobot startups and workflow-automation platforms.

• Innovation & Future Outlook: Advancements in haptic feedback, collaborative machining solutions, and integrated cloud robotics shaping next-generation deployments.

The industrial cobot market is experiencing rapid expansion across sectors such as automotive manufacturing, electronics assembly, metals processing, and logistics—collectively contributing over 60% of total deployment volume. Technological innovations including force-limited actuators, AI-enabled path optimization, and precision-grade sensors are elevating performance standards and reducing defect rates by up to 35%. Regulatory emphasis on workplace safety and lower-emission manufacturing is further accelerating cobot integration in Tier-1 and Tier-2 factories. Regional consumption patterns show particularly strong uptake in Asia-Pacific due to advanced electronics production, while Europe leads in precision machining applications. Future market evolution will be shaped by autonomous programming tools, sensor-fusion capabilities, and ultra-lightweight cobots optimized for high-mix, low-volume environments.

The strategic relevance of the Industrial Cobot Market is expanding rapidly as enterprises prioritize automation resilience, workforce augmentation, and flexible production architectures. Modern collaborative platforms deploy AI-driven motion planning that delivers up to 32% improvement in real-time task accuracy compared to legacy fixed-automation systems. Asia-Pacific dominates in volume owing to high-density manufacturing clusters, while Europe leads in adoption with 57% of enterprises already integrating at least one cobot-enabled production line. Emerging benchmarks indicate that next-generation cobots equipped with sensor-fusion technology enhance precision by 28% compared to conventional electromechanical units.

By 2027, AI-enhanced adaptive learning is expected to improve cycle-time efficiency by 35%, directly influencing throughput optimization in electronics, automotive, and machinery sectors. Compliance and ESG frameworks are also shaping future deployments, with firms committing to energy-efficiency enhancements and targeting up to 22% reduction in operational emissions by 2030 through lightweight, low-power cobot platforms. In 2024, South Korea achieved a 31% reduction in assembly-floor downtime using predictive-maintenance-enabled cobots integrated with digital twin analytics. These quantifiable outcomes demonstrate how collaborative automation is transitioning from a cost-efficiency tool to a strategic enabler of continuity, flexibility, and ESG alignment.

As industries advance toward intelligent factories, the Industrial Cobot Market will remain a cornerstone of resilient production networks, regulatory alignment, and sustainable industrial scalability.

The rapid adoption of advanced automation technologies is significantly strengthening the trajectory of the Industrial Cobot Market. Industrial facilities increasingly deploy cobots to streamline precision-heavy tasks, with robotics-enabled assembly processes reporting up to 29% improvement in operational efficiency. Manufacturers facing labor shortages use cobots to fill critical skill gaps while maintaining high production continuity. The rising use of machine-vision systems allows cobots to execute quality-inspection tasks with accuracy improvements exceeding 24%. Additionally, manufacturers integrating cobots into multi-station production lines experience measurable reductions in error rates and enhanced workflow consistency. These factors collectively accelerate long-term adoption and cement cobots as essential components within modern industrial automation frameworks.

Integration complexity continues to challenge the Industrial Cobot Market, particularly as manufacturers transition from conventional automation to collaborative systems. Many industrial environments operate with legacy machinery—requiring specialized programming, extensive calibration, and compatibility adjustments that prolong deployment cycles by up to 40%. Safety compliance testing, workspace mapping, and force-limitation validation add further time and cost burdens. In addition, smaller enterprises often lack in-house technical expertise, increasing reliance on third-party integrators and raising operational expenditure. Variability in production environments also requires custom integration strategies, limiting rapid scalability. These factors collectively restrain seamless implementation and can delay the full realization of cobot-driven productivity enhancements.

Advancements in AI-driven automation are unlocking substantial opportunities for the Industrial Cobot Market. The expansion of intelligent motion-control algorithms allows cobots to handle high-precision assembly, micro-inspection, and adaptive material handling with up to 35% improvement in accuracy. Industries increasingly adopt AI-powered predictive analytics, enabling cobots to anticipate and mitigate performance deviations, thereby reducing downtime by nearly 30%. The growing trend toward hyper-customized manufacturing in electronics, medical devices, and automotive components creates strong demand for flexible collaborative systems. As software-defined robotics expands, opportunities for scalable cobot deployment across small and mid-sized enterprises increase, paving the way for broader market penetration and differentiated service models.

Rising compliance, safety, and operational requirements pose substantial challenges to the Industrial Cobot Market. Global manufacturing standards increasingly mandate rigorous validation processes, including force-limitation checks, collision-detection thresholds, and continuous monitoring extending qualification timelines by up to 35%. Energy-efficiency mandates compel manufacturers to adopt low-power components that require redesigning existing systems, increasing upfront development effort. Additionally, cybersecurity requirements for connected cobots demand multi-layer protection frameworks, elevating integration costs. As factories modernize, operators must undergo structured training, and competency-building programs extend onboarding durations. These cumulative hurdles increase operational complexity and can slow the pace of cobot deployment across industrial sites.

• Acceleration of Modular and Prefabricated Construction Automation: The rise of modular and prefabricated construction is reshaping demand for high-precision industrial cobots, with 55% of new modular projects reporting measurable cost benefits through automated fabrication. Cobots are increasingly used for pre-bent and pre-cut structural elements, improving dimensional accuracy by 28% and reducing on-site labor requirements by up to 32%. Europe and North America show the fastest adoption, driven by strict timelines and growing reliance on automated assembly for large-scale infrastructure and residential developments.

• High-Growth Uptake of AI-Enhanced Motion Planning Systems: AI-driven motion planning is becoming a central trend, enabling cobots to achieve up to 40% faster path optimization and 22% better precision in component handling. Manufacturers in electronics and automotive sectors report a 30% improvement in mixed-model production efficiency due to autonomous calibration features. Adoption of vision-guided cobots also increased by 47% between 2022 and 2024, reflecting a shift toward flexible production environments capable of adapting to rapid SKU variations and complex micro-assembly processes.

• Expansion of Human–Robot Collaborative Workflows: Industrial facilities are rapidly expanding collaborative workflows, with more than 63% of large manufacturing plants integrating at least one cobot-enabled line by 2024. Enhanced force-limitation and safety-certified sensors have reduced incident risks by 41%, enabling closer human–robot proximity. This shift has increased productivity in multi-step assembly operations by 26%, particularly in machinery, fabricated metals, and automotive component manufacturing where real-time operator–cobot coordination shortens task cycles and minimizes rework.

• Growth of Edge-Integrated Predictive Maintenance Capabilities: Edge computing integration within cobot systems is enabling real-time diagnostics and predictive maintenance, reducing unplanned downtime by up to 35%. Manufacturers deploying edge-enabled cobots report a 29% increase in asset life and a 21% reduction in maintenance expenditure due to continuous vibration, temperature, and torque-pattern monitoring. This trend is accelerating adoption in Asia-Pacific and North America, where high-volume production environments depend heavily on uninterrupted operational flow and proactive maintenance frameworks.

The segmentation of the Industrial Cobot Market is shaped by evolving production requirements, advanced automation technologies, and increasing flexibility demands across manufacturing ecosystems. By type, collaborative arm configurations dominate due to their safety-certified architecture and ability to handle tasks ranging from precision assembly to material transfer, supported by rising integration of AI-driven controllers and vision systems. Applications such as assembly, pick-and-place, and quality inspection represent substantial deployment volumes, driven by measurable gains in speed, consistency, and throughput. End-user adoption is strongest among automotive, electronics, and metalworking sectors, where cobots enhance process repeatability and reduce manual intervention by 30–40%. Smaller industries are rapidly entering adoption cycles due to reduced programming complexity and modular deployment options. Together, these segmentation layers provide a comprehensive view of how cobots are reshaping industrial operations and enabling scalable automation across diversified production setups.

Collaborative robotic arms remain the leading product type in the Industrial Cobot Market, accounting for approximately 48% of total adoption due to their flexibility, compact design, and ability to operate safely alongside human workers. Their dominance stems from measurable efficiency gains of up to 35% in multi-stage assembly lines. In comparison, dual-arm cobots hold around 22% share, offering synchronized manipulation capabilities for complex tasks such as electronic subassembly and precision component integration.

Meanwhile, AI-enhanced vision-integrated cobots represent the fastest-growing type, supported by increasing demand for automated inspection and micro-handling tasks. This segment is expanding at an estimated 17% growth rate, driven by rising defect-reduction requirements in electronics and semiconductor manufacturing. Mobile cobots, autonomous cart-based collaborative systems, and lightweight task-specific cobots collectively contribute the remaining 30% share, serving niche applications in warehousing, packaging, and small-batch production environments. Their combined relevance is increasing as manufacturers prioritize flexible factory layouts and dynamic workflow optimization.

Assembly applications lead the Industrial Cobot Market, accounting for approximately 46% of deployment due to their ability to streamline repetitive production tasks with precision variations below 0.05 mm. In contrast, material handling and pick-and-place operations represent around 27% of adoption, supported by high-speed throughput enhancements and increased facility-level ergonomics. However, quality inspection is emerging as the fastest-growing application, expanding at roughly 16% growth due to rising demand for error-free manufacturing in electronics, automotive, and medical device segments.

Other application areas, including machine tending, packaging, and welding support, jointly make up the remaining 27% share. These segments continue gaining traction as cobots demonstrate measurable efficiency improvements of 25–30% in cycle time and tool-change operations. The growing role of AI-driven visual analytics, automated calibration, and force-feedback control is further reshaping the scope of cobot deployment across multi-process production floors.

Automotive manufacturing stands as the leading end-user segment in the Industrial Cobot Market, representing nearly 44% of total adoption due to intensive automation requirements, stringent quality frameworks, and consistent high-volume production cycles. Electronics manufacturing follows with a 26% share, driven by sub-millimeter assembly needs and rising component miniaturization. However, the fastest-growing end-user category is the logistics and warehousing sector, expanding at an estimated 18% rate as cobots enhance sorting accuracy and accelerate fulfillment throughput by 28%.

Other end-users—including metal fabrication, consumer goods, pharmaceuticals, and plastics processing—collectively contribute 30% share. These segments increasingly adopt cobots to mitigate labor shortages, improve operational safety, and maintain production consistency in high-variation environments. Adoption rates across SMEs are rising as well, with more than 34% of mid-scale manufacturing units integrating at least one cobot station to improve output reliability.

Asia-Pacific accounted for the largest market share at 41% in 2024; however, Europe is expected to register the fastest growth, expanding at a CAGR of 12.4% between 2025 and 2032.

Strong manufacturing expansion, advanced robotics integration rates exceeding 38%, and rising industrial automation intensity continue shaping regional performance. North America followed with a 28% share, supported by high-value automotive and electronics production, while Europe recorded 24% with increasing regulatory alignment driving adoption. South America and the Middle East & Africa collectively represented 7%, showing accelerating investment in logistics, automotive components, and industrial modernization initiatives. Distinct sectoral patterns—such as Asia-Pacific’s dominance in electronics assembly, Europe’s advanced engineering precision, and North America’s high adoption in automation-heavy industries—underscore the diversified growth landscape across global markets.

North America held a market share of approximately 28% in 2024, driven by strong uptake across automotive, electronics, healthcare, and metal fabrication industries. The region benefits from advanced manufacturing clusters and supportive federal automation programs incentivizing robotic adoption to improve labor productivity. Technological advancements—such as AI-enabled path optimization, safety-certified collaborative systems, and cloud-connected robotics—enhance deployment efficiency across large enterprises. Local players are contributing to market acceleration; for instance, a U.S.-based robotics integrator deployed over 1,500 cobot-driven assembly units in 2024, improving production speeds by 33% across participating facilities. Consumer and enterprise behavior shows a strong preference for high-precision automation in healthcare and finance-driven operational environments, where accuracy, compliance, and system reliability are prioritized. A rising shift toward flexible automation models and hybrid workforce structures continues to expand the regional growth outlook.

Europe captured around 24% of the Industrial Cobot Market in 2024, led by Germany, the UK, France, and Italy. Strong engineering ecosystems, advanced machinery sectors, and strict compliance regulations drive demand for precision automation. The region is rapidly adopting next-generation cobot systems featuring AI-driven inspection, digital twin simulation, and advanced force-feedback control. Sustainability frameworks are influencing deployments, with manufacturers integrating energy-efficient robotic modules to meet regulatory standards. European local players are contributing to innovation, with one leading German automation firm integrating next-gen cobot vision systems that improve micro-assembly accuracy by 29%. Consumer behavior across industries shows a push toward explainable, transparent, and regulation-compliant automation workflows, particularly in healthcare, automotive, and industrial electronics. This regulatory-driven adaptation continues to make Europe one of the fastest-evolving regions for cobot adoption.

Asia-Pacific remained the highest-volume region in 2024 with a 41% market share, driven by China, Japan, South Korea, and India. The region hosts robust manufacturing ecosystems, with electronics, automotive, and industrial machinery accounting for over 55% of cobot installations. Heavy investments in smart factory infrastructure and robotics innovation hubs across China and Japan are accelerating deployment. A leading Japanese robotics manufacturer deployed modular cobots in 2024 to enhance micro-assembly operations, achieving a 34% reduction in cycle-time variance. Consumer technology adoption is heavily influenced by fast-growing e-commerce fulfillment centers and mobile automation platforms, which require scalable and flexible cobot solutions. Rapid industrial digitalization, strong export-driven production capacity, and high-density manufacturing clusters continue to reinforce Asia-Pacific’s dominant position in the global market.

South America accounted for roughly 4% of the Industrial Cobot Market in 2024, with Brazil and Argentina leading adoption. The region’s industrial modernization strategies, particularly in automotive components, agriculture equipment, and food processing, are boosting cobot utilization. Infrastructure upgrades and government-backed manufacturing stimulus programs are accelerating automation interest. A Brazilian machinery producer integrated cobots for packaging-line operations in 2024, achieving a 27% reduction in manual handling time. Energy sector digitization and expanding logistics automation are additional drivers. Consumer behavior shows rising interest in automated quality-control solutions, particularly among mid-sized enterprises aiming to improve export competitiveness. Although early-stage, the region demonstrates measurable potential as adoption expands across diversified industries.

The Middle East & Africa region represented around 3% of the market in 2024, driven by increasing investment in oil & gas automation, logistics, construction technologies, and industrial diversification programs. Countries such as the UAE, Saudi Arabia, and South Africa are modernizing their manufacturing bases with robotics-enabled workflows. Cobots are increasingly used in precision welding, inspection, and assembly for energy and construction projects. A UAE-based industrial solutions provider deployed cobot-assisted inspection systems in 2024, improving structural defect detection accuracy by 31%. Regional consumer patterns reflect growing interest in low-maintenance, energy-efficient automation suited for high-temperature and heavy-duty environments. Cross-border trade partnerships and economic diversification plans continue to strengthen adoption momentum across industrial sectors.

China – 29% Market Share

High production capacity and strong electronics and automotive manufacturing clusters drive large-scale cobot deployment.

Japan – 18% Market Share

Advanced robotics ecosystems and widespread industrial automation adoption support sustained leadership in cobot integration.

The Industrial Cobot market demonstrates a moderately consolidated competitive structure, with approximately 25–30 active global competitors contributing to technological and operational advancements. The top five companies collectively command an estimated 48–52% share of the overall market, reflecting strong dominance driven by continuous innovation, expanding product portfolios, and strategic ecosystem partnerships. Market rivalry has intensified as companies introduce next-generation cobots with enhanced payload capacities, ranging from 3 kg to 20 kg, alongside improved repeatability metrics below 0.02 mm. Major manufacturers are increasingly prioritizing AI-driven motion control, intelligent path optimization, and cloud-enabled performance monitoring, accelerating adoption across automotive, electronics, and metals industries. Over 60% of new launches in 2024 integrated embedded vision systems and force-torque sensors, highlighting the shift toward smarter, self-correcting collaborative robots. Strategic initiatives—including 20+ notable partnerships, 10+ mergers and acquisitions, and multiple cross-industry technology integrations—further emphasize competitive differentiation. Regional expansion remains a core strategy, with leading companies increasing footprint in Asia-Pacific due to rising industrial automation demand. More than 40% of competitors have invested in training centers, service networks, and ecosystem developer programs to strengthen customer engagement. The market continues to evolve as modularity, safety-certified designs, and low-programming interfaces shape long-term competitive advantages.

Universal Robots

ABB Robotics

Fanuc Corporation

KUKA AG

Techman Robot

Denso Wave

Yaskawa Electric Corporation

Doosan Robotics

AUBO Robotics

Elite Robots

Industrial cobot technologies are advancing rapidly as manufacturers prioritize precision, safety, and flexibility within automated production environments. A major technological shift is occurring toward high-performance torque sensors, where accuracy levels have improved by nearly 30% compared to earlier generations, enabling cobots to perform delicate tasks such as micro-assembly and precision dispensing. Enhanced force-limiting mechanisms, compliant joints, and real-time collision detection allow cobots to operate within human workspaces more safely, contributing to a 40% increase in dual-operation workflows across manufacturing and warehousing environments. Vision-guided cobot systems are becoming a cornerstone of next-generation automation, with more than 55% of newly deployed cobots in 2024 integrating embedded 2D/3D vision modules. These systems support high-speed inspection, object recognition, and adaptive path correction with accuracy thresholds reaching 98%. Advancements in AI-powered motion planning have also reduced task programming time by nearly 45%, allowing manufacturers to deploy cobots faster while maintaining production continuity. Machine learning algorithms now enable continuous optimization of cycle time, tool wear prediction, and autonomous quality checks, enhancing operational efficiency in electronics, automotive, and precision machining sectors.

Edge-enabled cobot architectures are gaining prominence, with over 50% of modern collaborative robots equipped with onboard processors capable of performing real-time analytics without relying heavily on cloud infrastructure. This shift improves latency, response time, and cybersecurity resilience. Connectivity standards such as OPC-UA, EtherCAT, and emerging 5G-enabled industrial protocols are enabling faster communication between cobots, conveyors, AGVs, and PLC systems, improving interoperability across the manufacturing floor.

Modular cobot design is another notable trend, with interchangeable end-effectors, plug-and-play tool changers, and scalable arm configurations allowing manufacturers to adapt quickly to changing production requirements. Payload flexibility—ranging from 3 kg to more than 25 kg—has expanded adoption in automotive body assembly, metal fabrication, food processing, and logistics. As industrial environments demand more versatile and intelligent automation, these technology advancements position cobots as a central component in the future of digitally connected manufacturing ecosystems.

In 2023, Universal Robots expanded its product portfolio by launching the UR20 collaborative robot, engineered for higher payload operations with over 30% improved reach and a 25% reduction in joint wear, specifically addressing heavier material handling and palletizing tasks in automotive and logistics applications.

In 2023, ABB introduced expanded models in its GoFa cobot series, featuring enhanced safety and simplified programming, resulting in a 33% uptick in adoption across electronics and precision assembly sectors within six months of release.

In early 2024, KUKA unveiled the second-generation LBR iisy cobot, designed with advanced force torque sensors and integrated vision systems, achieving a 35% increase in task accuracy and a 20% improvement in tool compatibility shortly after launch.

Also in 2024, global automation saw a trend toward user education and ecosystem events, with Universal Robots hosting Collaborate North America 2025, drawing 500+ manufacturing professionals and demonstrating 30+ cobot-powered solutions to showcase real-world applications across welding, inspection, handling, and assembly. (Business Wire)

The scope of the Industrial Cobot Market Report encompasses a holistic examination of technological, structural, and application-based dimensions shaping the collaborative automation landscape. It analyzes key product types, spanning collaborative robotic arms with variable payload capacities, AI-integrated vision systems, mobile cobots with navigation capabilities, and modular end-effectors tailored to specific industrial tasks. The report also assesses adoption across primary applications such as precision assembly, automated inspection, material handling, machine tending, and packaging operations, detailing performance enhancements achieved in real-world deployments. Geographic segmentation covers detailed insights into market behavior across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, emphasizing production ecosystems, regional automation maturity, industrial infrastructure, and consumer behavior variations in manufacturing investment. The report highlights niche segments, including healthcare automation, food processing, and lab automation, where collaborative robots are increasingly deployed to address workforce challenges and compliance requirements. In terms of technologies, it evaluates the impact of AI-driven motion planning, embedded vision modules, edge-enabled diagnostics, and connected robotics platforms on operational efficiency, task precision, and system interoperability. The analysis further explores end-user industry profiles—automotive, electronics, metal fabrication, logistics, and SMEs—offering comparative insights into adoption rates, workflow integration strategies, and deployment outcomes. Through this breadth of coverage, the report equips decision-makers with actionable intelligence on segment-specific performance, regional trends, and emerging opportunities shaping the future of industrial cobot implementation.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 958.52 Million |

|

Market Revenue in 2032 |

USD 2289.82 Million |

|

CAGR (2025 - 2032) |

11.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Universal Robots , ABB Robotics , Fanuc Corporation, KUKA AG , Techman Robot, Denso Wave, Yaskawa Electric Corporation, Doosan Robotics, AUBO Robotics, Elite Robots |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |