Reports

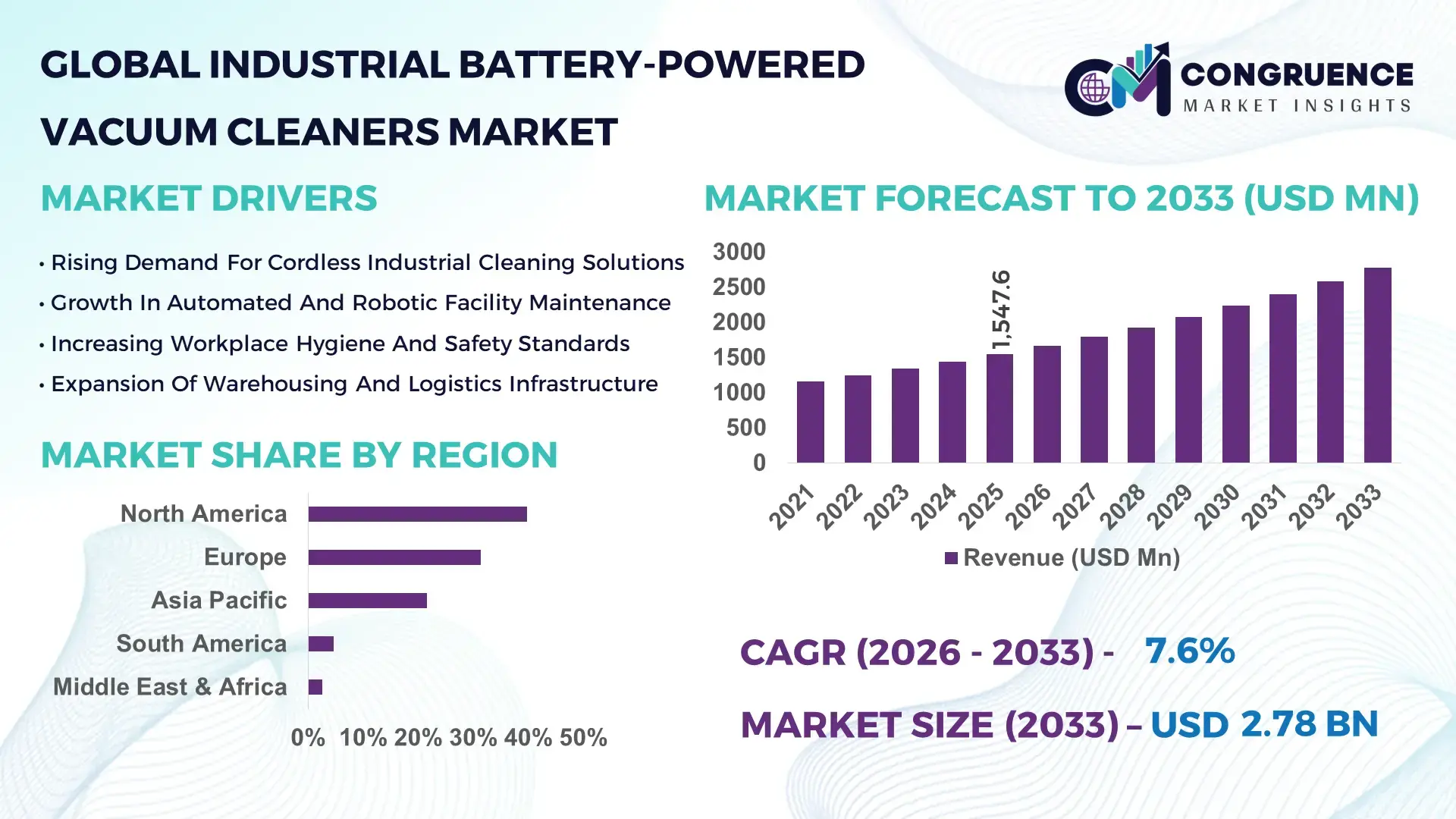

The Global Industrial Battery-Powered Vacuum Cleaners Market was valued at USD 1,547.6 Million in 2025 and is anticipated to reach a value of USD 2,780.7 Million by 2033 expanding at a CAGR of 7.6% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is driven by increasing adoption of cordless, energy-efficient cleaning solutions across manufacturing, logistics, and commercial facilities.

The United States leads the Industrial Battery-Powered Vacuum Cleaners market through advanced production capacity, strong industrial demand, and continuous investment in lithium-ion powered cleaning equipment. In 2024, U.S. manufacturers produced over 1.8 million industrial cordless vacuum units, supported by more than USD 420 million in annual investments toward battery-powered industrial cleaning technologies. Warehouse and logistics facilities accounted for nearly 34% of industrial deployments, while manufacturing plants represented 29% of installations. Over 52% of newly purchased industrial vacuum systems in the country now feature lithium-ion battery packs with run times exceeding 60 minutes, and more than 18,000 large facilities adopted cordless cleaning fleets for safety and productivity improvements.

Market Size & Growth: Valued at USD 1,547.6 million in 2025, projected to reach USD 2,780.7 million by 2033 at 7.6% CAGR, driven by shift to cordless industrial cleaning solutions.

Top Growth Drivers: Lithium-ion adoption (48%), warehouse automation growth (36%), workplace safety regulations (27%).

Short-Term Forecast: By 2028, battery-powered cleaning fleets are expected to cut facility cleaning time by 22%.

Emerging Technologies: High-density lithium-ion packs, brushless DC motors, smart fleet monitoring systems.

Regional Leaders: North America projected at USD 1.1 billion by 2033 with logistics adoption; Europe at USD 820 million driven by sustainability mandates; Asia Pacific at USD 690 million supported by manufacturing expansion.

Consumer/End-User Trends: Growing demand from warehouses, food processing, and electronics plants, with cordless units used in 44% of large facilities.

Pilot or Case Example: In 2024, a logistics center reduced cleaning labor hours by 31% using battery-powered industrial vacuums.

Competitive Landscape: Kärcher leads with about 18% share, followed by Nilfisk, Tennant, Hako, and Dyson Professional.

Regulatory & ESG Impact: Emission-reduction mandates and workplace safety rules accelerating cordless equipment adoption.

Investment & Funding Patterns: Over USD 620 million invested globally in battery-powered industrial cleaning technologies from 2022–2024.

Innovation & Future Outlook: Integration of IoT sensors, predictive maintenance, and modular battery systems shaping next-generation equipment.

Industrial manufacturing accounts for nearly 39% of equipment demand, followed by logistics and warehousing at 32% and food processing at 17%. Innovations in fast-charging battery packs and brushless motors are reducing downtime by up to 28%. Environmental regulations and noise-reduction mandates support adoption, while Asia-Pacific’s industrial expansion and Europe’s sustainability standards continue to shape regional demand patterns.

The Industrial Battery-Powered Vacuum Cleaners Market is strategically positioned at the intersection of workplace automation, energy efficiency, and sustainability mandates. Industrial facilities are shifting from corded or fuel-powered cleaning equipment to battery-powered solutions that offer greater mobility, lower emissions, and reduced maintenance requirements. Modern lithium-ion battery systems deliver up to 35% longer operating cycles compared to traditional lead-acid batteries, improving productivity across large facilities.

From a regional perspective, Asia-Pacific dominates in volume due to large-scale manufacturing and warehouse infrastructure, while Europe leads in adoption with over 58% of industrial facilities transitioning to low-emission cleaning equipment. By 2028, smart battery management systems are expected to improve equipment uptime by 25%, reducing unplanned maintenance and operational interruptions.

Sustainability commitments are shaping procurement strategies. Many industrial operators are targeting 30% reductions in carbon emissions from facility maintenance equipment by 2030. Battery-powered vacuum fleets contribute significantly to these goals by eliminating fuel-based emissions and reducing noise levels by up to 40%. In 2024, a major European distribution center achieved a 27% reduction in energy consumption after replacing corded vacuums with lithium-ion powered units integrated with automated cleaning schedules.

Future pathways emphasize integration with automated guided vehicles, predictive maintenance platforms, and centralized fleet management systems. By 2027, connected cleaning systems are expected to reduce facility cleaning costs by 18%. These developments position the Industrial Battery-Powered Vacuum Cleaners Market as a pillar of operational resilience, regulatory compliance, and sustainable industrial growth.

The Industrial Battery-Powered Vacuum Cleaners market is influenced by rapid electrification of industrial equipment, stricter workplace safety regulations, and the shift toward automated facility management. Lithium-ion battery technology has improved energy density by more than 30% over the past five years, enabling longer operating times and faster charging cycles. Demand is rising across warehouses, manufacturing plants, and food processing facilities where cordless mobility enhances cleaning efficiency. Noise reduction requirements and emission standards are accelerating the transition away from corded or fuel-powered machines. At the same time, advancements in brushless motor technology and modular battery systems are improving durability, reducing maintenance intervals, and enabling fleet-wide performance monitoring.

The rapid growth of automated warehouses and distribution centers is significantly increasing demand for Industrial Battery-Powered Vacuum Cleaners. Automated logistics hubs operate up to 20 hours per day, requiring flexible, cordless cleaning equipment that can function without cable restrictions. In 2024, over 46% of newly built warehouses adopted battery-powered cleaning equipment as standard infrastructure. Lithium-ion powered vacuums improved cleaning productivity by 24% and reduced equipment downtime by nearly 18% compared to corded units. These performance benefits are driving adoption across e-commerce fulfillment centers and automated storage facilities.

Despite operational benefits, high initial equipment and battery costs remain a key restraint. Industrial lithium-ion vacuum systems typically cost 20–35% more than equivalent corded units. Battery replacement cycles and charging infrastructure investments further increase total ownership costs. In price-sensitive markets, nearly 27% of facilities continue using corded or refurbished equipment due to lower capital expenditure. These financial constraints slow adoption, particularly among small and medium-scale industrial operators.

Sustainability initiatives across industrial facilities present strong growth opportunities. More than 52% of large manufacturing plants have set emission-reduction targets for maintenance equipment. Battery-powered vacuum cleaners reduce noise by up to 40% and eliminate exhaust emissions, making them suitable for food processing and pharmaceutical environments. In 2024, facilities that adopted cordless cleaning fleets reported 22% reductions in energy consumption. Increasing regulatory focus on workplace air quality and carbon reduction is expected to expand adoption across multiple industries.

Battery lifecycle management and charging logistics remain operational challenges. Industrial facilities using multiple battery-powered units must invest in charging stations and battery rotation systems. In high-usage environments, battery degradation can reduce runtime by up to 15% after two years of continuous operation. Additionally, inadequate charging infrastructure can lead to equipment downtime during peak shifts. These challenges require strategic fleet planning and advanced battery management solutions.

Shift Toward High-Capacity Lithium-Ion Systems: Over 63% of new industrial cordless vacuum launches in 2024 used high-capacity lithium-ion battery packs, extending runtime by 28% and reducing charging frequency by 19%.

Adoption of Brushless Motor Technology: Brushless DC motors were integrated into 57% of newly deployed industrial battery vacuums, improving energy efficiency by 23% and extending motor lifespan by 35%.

Growth of Smart Fleet Monitoring: Around 41% of large industrial facilities adopted IoT-enabled vacuum fleets in 2024, enabling predictive maintenance and reducing unexpected equipment failures by 26%.

Noise-Reduction and Indoor Air Quality Compliance: Nearly 48% of food processing and pharmaceutical facilities adopted low-noise battery vacuums, cutting operational noise levels by 32% and improving compliance with indoor air quality standards.

The Industrial Battery-Powered Vacuum Cleaners market is segmented by equipment type, application, and end-user industries. Segmentation reflects differences in cleaning intensity, facility size, and mobility requirements. Equipment types range from compact portable units to heavy-duty ride-on systems. Applications include manufacturing, logistics, food processing, and commercial facilities, each with distinct operational needs. End-user insights show that industrial and warehouse operators prioritize runtime, durability, and energy efficiency, while food and pharmaceutical sectors emphasize hygiene compliance and low-noise performance.

Walk-behind industrial battery-powered vacuum cleaners account for approximately 46% of adoption, as they offer a balance of maneuverability and cleaning power suitable for warehouses and factory floors. Ride-on vacuum systems hold about 28%, preferred in large facilities exceeding 50,000 square meters. However, robotic battery-powered vacuum cleaners are the fastest-growing segment, expected to expand at over 12% CAGR, driven by automation trends and labor cost pressures. Portable handheld and specialty units collectively represent 26%, serving maintenance, tight-space cleaning, and niche industrial tasks.

In 2024, a national logistics modernization program deployed over 8,000 walk-behind battery vacuum units across automated warehouses, improving cleaning cycle efficiency by 25%.

Manufacturing facilities lead with a 39% share due to continuous production environments requiring frequent cleaning. Logistics and warehousing follow with 32%, driven by high-traffic fulfillment centers. Food processing is the fastest-growing application, expanding above 10% CAGR due to hygiene regulations and noise control requirements. Pharmaceuticals, electronics, and commercial facilities collectively represent 29% of applications. In 2025, nearly 44% of large industrial sites reported shifting from corded to battery-powered cleaning systems.

In 2024, over 2,300 food processing plants adopted battery-powered industrial vacuum systems, reducing cleaning downtime by 21%.

Industrial manufacturing remains the leading end-user at 41% of adoption, reflecting high demand for heavy-duty cleaning equipment. Warehousing and logistics operators are the fastest-growing end-user segment, expanding at over 11% CAGR as e-commerce infrastructure expands. Food and beverage, pharmaceuticals, and electronics manufacturers collectively represent 37% of end-user demand. In 2025, more than 38% of industrial facilities reported piloting connected battery-powered cleaning equipment for predictive maintenance.

In 2024, a national warehouse automation initiative equipped over 1,200 logistics centers with battery-powered cleaning fleets, improving operational efficiency by 23%.

North America accounted for the largest market share at 39.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.2% between 2026 and 2033.

North America recorded more than 620,000 industrial battery-powered vacuum units in active operation across manufacturing plants, logistics hubs, and commercial facilities in 2025. Europe followed with a 31.4% share, supported by sustainability mandates and electrification targets across industrial cleaning fleets. Asia-Pacific accounted for approximately 21.6% of global installations, with China, Japan, and India together deploying over 480,000 cordless industrial vacuum systems. South America represented 4.6% of total demand, driven by warehouse modernization in Brazil and Argentina. Middle East & Africa held 2.6%, with adoption concentrated in oil, construction, and large commercial infrastructure projects across UAE and South Africa.

How are automation and safety mandates transforming cordless industrial cleaning adoption?

North America held approximately 39.8% of the global Industrial Battery-Powered Vacuum Cleaners market in 2025, reflecting high adoption across manufacturing, logistics, food processing, and commercial facilities. Over 58% of large warehouses and distribution centers deployed cordless cleaning fleets to support automated operations. Workplace safety regulations and emission-reduction standards accelerated the shift from corded systems, with nearly 47% of newly purchased industrial vacuums powered by lithium-ion batteries. Technological trends include IoT-enabled fleet monitoring, fast-charging battery packs, and brushless motor systems. A regional manufacturer introduced smart battery-powered vacuums with predictive maintenance alerts, reducing service interruptions by 21%. Consumer behavior shows strong preference for low-noise, high-mobility equipment, especially in healthcare, retail, and food production facilities.

Why are sustainability directives driving electrified cleaning equipment across industrial facilities?

Europe accounted for approximately 31.4% of the Industrial Battery-Powered Vacuum Cleaners market in 2025, with Germany, the UK, and France contributing nearly 62% of regional installations. Environmental regulations targeting workplace emissions and noise levels accelerated adoption of cordless cleaning equipment. Over 54% of newly deployed industrial vacuum units in Western Europe used lithium-ion battery technology. Regulatory frameworks focused on energy efficiency and lifecycle sustainability influenced procurement decisions. A European manufacturer launched eco-designed battery-powered vacuum systems with recyclable components, reducing material waste by 18%. Regional consumer behavior reflects strong preference for energy-efficient and regulation-compliant cleaning solutions across manufacturing and commercial sectors.

What is enabling large-scale cordless cleaning adoption across manufacturing and logistics hubs?

Asia-Pacific ranked second by volume in 2025, accounting for more than 480,000 deployed industrial battery-powered vacuum units. China, India, and Japan represented nearly 74% of regional demand, supported by expanding manufacturing capacity and warehouse infrastructure. Industrial clusters in China and Southeast Asia increasingly integrate cordless cleaning fleets into automated production lines. Technological trends include high-density lithium-ion battery production and compact motor designs. A regional equipment manufacturer launched battery-powered industrial vacuums optimized for e-commerce fulfillment centers, achieving over 120,000 unit shipments within one year. Consumer behavior in the region is driven by cost efficiency, mobility, and rapid adoption in logistics and electronics manufacturing.

How is warehouse modernization increasing cordless cleaning equipment demand?

South America represented about 4.6% of the global Industrial Battery-Powered Vacuum Cleaners market in 2025, with Brazil and Argentina accounting for nearly 68% of regional demand. Growth is supported by logistics infrastructure upgrades and expansion of large retail distribution centers. Industrial electrification policies reduced import duties on battery-powered equipment by up to 12% in select markets. A regional distributor partnered with an equipment manufacturer to supply cordless vacuum fleets to over 400 logistics facilities. Consumer behavior reflects demand for durable, cost-efficient equipment suited for multilingual and multi-shift operations.

How are infrastructure and industrial projects boosting cordless equipment deployment?

The Middle East & Africa region accounted for approximately 2.6% of global installations in 2025, led by UAE and South Africa. Demand is driven by oil and gas facilities, construction projects, and large commercial complexes. Over 36% of newly built industrial facilities in the Gulf region adopted battery-powered cleaning equipment to meet noise and emission standards. Technological modernization includes integration of high-temperature-resistant battery systems. A regional facility management company deployed over 3,200 cordless industrial vacuum units across infrastructure projects, improving cleaning productivity by 19%. Consumer behavior varies, with premium adoption in Gulf commercial centers and cost-focused purchases in emerging African markets.

United States Industrial Battery-Powered Vacuum Cleaners Market – 36.9%: High industrial automation levels and strong adoption across warehouses and manufacturing plants.

Germany Industrial Battery-Powered Vacuum Cleaners Market – 15.2%: Advanced industrial infrastructure and strict energy-efficiency and workplace safety regulations.

The Industrial Battery-Powered Vacuum Cleaners market is moderately consolidated, with approximately 50 active global and regional manufacturers competing across industrial, commercial, and logistics segments. The top five companies collectively hold about 61% of total market presence, supported by strong product portfolios, extensive distribution networks, and advanced battery technologies. Competition is driven by innovations in lithium-ion battery performance, brushless motor efficiency, and smart fleet management systems. Product refresh cycles average 18–30 months, reflecting rapid advancements in battery density and charging speeds. Strategic partnerships between equipment manufacturers and industrial facility operators increased by nearly 24% between 2023 and 2025. Several competitors are investing in autonomous cleaning systems and modular battery platforms to differentiate their offerings. The competitive environment is increasingly shaped by energy efficiency metrics, runtime improvements, and total cost of ownership reductions, reinforcing technology-driven competition.

Kärcher

Nilfisk Group

Tennant Company

Hako Group

Dyson Professional

Makita Corporation

Numatic International

IPC Group

Comac SpA

Pacvac

Minuteman International

Factory Cat

Technological progress in the Industrial Battery-Powered Vacuum Cleaners market is centered on lithium-ion battery advancements, high-efficiency brushless motors, and intelligent fleet management systems. Modern lithium-ion battery packs offer energy densities exceeding 240 Wh/kg, extending operating times by up to 30% compared to earlier battery generations. Fast-charging systems can restore 80% capacity within 45 minutes, reducing equipment downtime. Brushless DC motors improve energy efficiency by 20–25% while extending motor lifespan beyond 5,000 operating hours.

Smart fleet management platforms are increasingly integrated, enabling real-time monitoring of battery health, usage patterns, and maintenance needs. Facilities using connected cleaning fleets reported up to 26% reductions in unexpected equipment failures. Autonomous navigation technologies are also emerging, allowing robotic battery-powered vacuum systems to operate in warehouses and large industrial spaces with minimal human intervention. Advanced filtration systems, including HEPA and multi-stage cyclonic filtration, capture up to 99.97% of fine particles, meeting stringent indoor air quality standards. These technologies collectively enhance productivity, reduce operational costs, and support sustainability objectives across industrial cleaning operations.

In March 2025, Kärcher launched a new lithium-ion powered industrial vacuum platform featuring interchangeable battery modules and brushless motors, extending continuous runtime to over 90 minutes and improving cleaning efficiency in large logistics facilities. Source: www.kaercher.com

In November 2024, Nilfisk introduced an upgraded cordless industrial vacuum series with high-density battery packs, reducing charging time by 30% and increasing airflow performance for heavy-duty manufacturing environments. Source: www.nilfisk.com

In June 2024, Tennant Company unveiled a battery-powered industrial cleaning system with smart fleet connectivity, enabling predictive maintenance alerts and reducing unplanned service downtime by 22% in pilot facilities. Source: www.tennantco.com

In February 2024, Hako Group released a new industrial cordless vacuum platform designed for continuous multi-shift operations, incorporating fast-swap lithium-ion batteries and noise-reduction technology to support indoor industrial applications. Source: www.hako.com

The Industrial Battery-Powered Vacuum Cleaners Market Report covers a comprehensive analysis of equipment types, applications, technologies, and end-user industries across global regions. The scope includes walk-behind, ride-on, robotic, and portable battery-powered vacuum systems designed for industrial and commercial cleaning environments. Applications analyzed span manufacturing plants, logistics and warehousing, food processing facilities, pharmaceuticals, electronics, and large commercial complexes.

Technology coverage includes lithium-ion battery systems, brushless motor platforms, smart fleet monitoring, autonomous navigation, and advanced filtration technologies. The report evaluates performance metrics such as runtime, charging cycles, filtration efficiency, and noise levels across different equipment categories. Geographic coverage includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with country-level insights for key industrial markets.

Emerging segments such as robotic industrial vacuum systems, connected fleet solutions, and energy-efficient cleaning platforms are also assessed. The report supports strategic planning by providing insights into equipment adoption patterns, technology transitions, regulatory influences, and industry-specific demand trends relevant to manufacturers, distributors, facility operators, and investors.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1,547.6 Million |

|

Market Revenue in 2033 |

USD 2,780.7 Million |

|

CAGR (2026 - 2033) |

7.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Tiger-Vac, Pullman-Ermator, Goodway Technologies , Kärcher, Nilfisk Group, Tennant Company, Hako Group, Dyson Professional, Makita Corporation, Numatic International, IPC Group, Comac SpA, Pacvac, Minuteman International, Factory Cat |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |