Reports

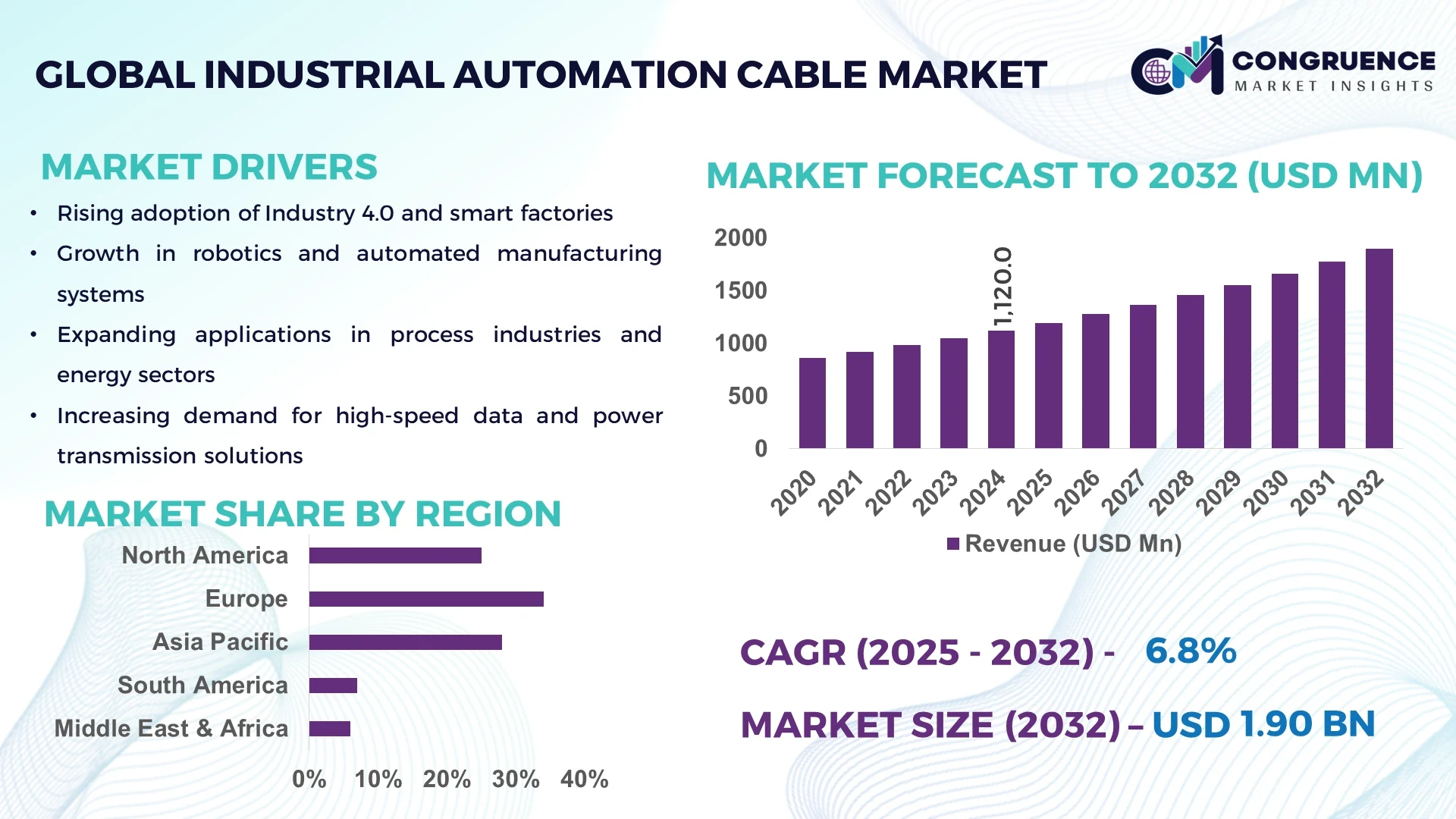

The Global Industrial Automation Cable Market was valued at USD 1,120.0 Million in 2024 and is anticipated to reach a value of USD 1,895.8 Million by 2032 expanding at a CAGR of 6.8% between 2025 and 2032. Growth is fueled by rising demand for high-performance cabling solutions in industrial automation systems.

Germany plays a dominant role in the Industrial Automation Cable Market with its advanced manufacturing ecosystem, supported by over 6,000 automation-focused enterprises. Investments exceeding USD 12 billion in Industry 4.0 initiatives have enhanced production capacity across sectors such as automotive, chemical, and heavy machinery. The country’s adoption rate of smart factories reached 45% in 2024, with robotics-driven automation contributing significantly to demand for durable cables.

Market Size & Growth: Valued at USD 1,120.0 Million in 2024, projected to reach USD 1,895.8 Million by 2032 at a CAGR of 6.8%, driven by rising factory digitalization.

Top Growth Drivers: Automation adoption (48%), efficiency improvements (36%), and predictive maintenance integration (29%).

Short-Term Forecast: By 2028, operational downtime in automated plants is projected to reduce by 22% with improved cabling reliability.

Emerging Technologies: Smart cables with IoT sensors, fiber-reinforced insulation, and flexible hybrid cables.

Regional Leaders: Asia-Pacific (USD 720.0 Million by 2032) led by manufacturing hubs, Europe (USD 540.0 Million) with Industry 4.0 adoption, and North America (USD 460.0 Million) with advanced robotics integration.

Consumer/End-User Trends: Automotive and electronics sectors dominate, with 62% adoption across production lines.

Pilot or Case Example: In 2024, a Japanese automotive plant achieved 18% higher assembly efficiency using fiber-enhanced automation cables.

Competitive Landscape: Market leader holds ~14% share, followed by 4 major players including cable specialists and industrial automation providers.

Regulatory & ESG Impact: Regulations on energy efficiency and 20% recycling targets by 2030 are boosting eco-friendly cabling demand.

Investment & Funding Patterns: Over USD 2.3 billion invested globally in automation cable R&D during 2023–2024.

Innovation & Future Outlook: Rising integration of data-transmission and power cables will shape next-generation industrial automation infrastructure.

The Industrial Automation Cable Market is evolving with strong adoption in automotive, aerospace, and electronics industries, where high-speed, durable, and sustainable solutions are critical. Innovations in smart cable monitoring, eco-friendly materials, and regional consumption shifts toward Asia-Pacific are reinforcing future growth prospects.

The Industrial Automation Cable Market holds strategic importance as industries worldwide pursue automation, digitalization, and energy efficiency. Reliable cabling forms the backbone of robotics, process control, and smart manufacturing. Advanced hybrid cables deliver 28% higher data transfer efficiency compared to conventional copper wiring, setting new performance benchmarks.

Asia-Pacific dominates in production volume due to strong manufacturing bases, while Europe leads adoption with 52% of enterprises integrating Industry 4.0-ready cabling systems. By 2027, IoT-enabled cables are expected to reduce maintenance costs in automated plants by 25%, accelerating operational efficiency.

Compliance and sustainability are key pillars: firms are committing to a 30% reduction in non-recyclable cable waste by 2030, aligning with global ESG mandates. In 2024, a US-based electronics manufacturer achieved a 22% downtime reduction through AI-driven smart cable diagnostics, underlining the impact of digital transformation. Looking ahead, the Industrial Automation Cable Market is set to become a critical enabler of global smart industry ecosystems, fostering resilience, sustainability, and competitive advantage across multiple manufacturing domains.

The Industrial Automation Cable Market is influenced by rapid industrial digitalization, rising demand for connected infrastructure, and robust adoption of Industry 4.0 solutions. Increased investment in robotics, predictive maintenance, and smart manufacturing is driving steady growth. Demand for hybrid and high-flexibility cables is surging as industries focus on minimizing downtime and enhancing performance. The sector is further shaped by government-backed smart factory initiatives, stricter environmental regulations, and shifting consumer demand for energy-efficient and sustainable products.

The acceleration of digital transformation across manufacturing and process industries is creating heightened demand for reliable, high-capacity cabling systems. Over 50% of factories globally have integrated robotics and automated control systems that require advanced connectivity. Industrial Ethernet and fiber optic cables are seeing wider adoption to support low-latency communication, enabling seamless IoT integration. Automation cables are now critical in minimizing downtime, with predictive maintenance supported by real-time monitoring reducing failures by up to 30%. As factories expand digital adoption, the cabling infrastructure market is seeing a consistent push toward smarter, stronger, and faster solutions.

One of the key restraints for the Industrial Automation Cable Market is the volatility of raw material costs, especially copper and aluminum, which account for a significant share of production expenses. Prices of copper fluctuated by more than 18% during 2023–2024, impacting manufacturing margins and project costs. Furthermore, sourcing high-quality insulation materials, such as fluoropolymers, has become cost-intensive due to rising demand across industries. These factors create financial uncertainty for manufacturers, delaying large-scale procurement and limiting expansion in cost-sensitive regions. As cable producers seek alternatives such as composites and recycled materials, supply-side constraints remain a barrier to stable growth.

The rise of Industry 4.0 presents significant opportunities for advanced automation cable solutions. Smart factories rely heavily on cables that support real-time communication, predictive maintenance, and seamless robotics integration. Approximately 42% of enterprises are planning to deploy IoT-enabled cabling systems by 2026 to enhance operational reliability. This presents new prospects for hybrid cables capable of transmitting both power and data, reducing infrastructure costs and simplifying designs. Moreover, advancements in eco-friendly materials and recyclable cabling provide additional growth opportunities, especially as firms face stricter environmental compliance standards. The shift toward intelligent and sustainable infrastructure is expanding market potential across automotive, aerospace, and electronics industries.

As industrial automation systems become increasingly interconnected, the security of data transmitted through cabling networks is emerging as a critical challenge. With over 65% of factories deploying IoT-enabled systems, concerns about data interception and unauthorized access are on the rise. Industrial Ethernet cables are central to transmitting sensitive operational information, making them potential targets for cyber threats. Furthermore, the integration of smart sensors within cables raises additional vulnerabilities in data communication lines. Addressing these concerns requires significant investment in encryption, shielding, and security-focused designs, adding to production costs and complexity. This creates challenges for manufacturers seeking to balance security, performance, and cost efficiency.

Rising Demand for High-Flex Cables in Robotics: In 2024, demand for flexible cables used in robotic arms grew by 31%, with more than 58,000 robotic systems globally relying on specialized cabling for repetitive motion. These cables enhance durability and efficiency, reducing replacement cycles by 18%.

Shift Toward Hybrid Power-Data Cables: Over 40% of new industrial automation projects in 2024 adopted hybrid cabling, reducing system complexity by 22%. This trend is most visible in automotive and electronics assembly lines, where integration of power and data pathways accelerates production efficiency.

Adoption of Fiber-Optic Cabling for Smart Factories: Fiber-optic installations in automated facilities increased by 27% in 2024, particularly in Asia-Pacific. These solutions support high-speed data transfers, enabling real-time monitoring and predictive analytics in production environments with minimal latency.

Eco-Friendly Materials in Cable Manufacturing: With sustainability targets becoming stricter, 33% of industrial cable manufacturers introduced recyclable or bio-based insulation materials in 2024. This shift is reducing plastic waste and aligning with ESG commitments, enhancing brand positioning for eco-conscious buyers.

The Industrial Automation Cable Market is segmented by type, application, and end-user, reflecting diverse industrial needs and technological adoption patterns. By type, demand spans from flexible power cables to advanced fiber-optic and hybrid variants, with each category tailored for specific industrial environments. Applications range from robotics and factory automation to energy systems and process industries, with high-performance connectivity increasingly required for digital transformation. End-users include manufacturing, automotive, aerospace, healthcare, energy, and logistics, each driving demand through unique operational requirements. Adoption trends highlight a strong shift toward high-speed data cables, eco-friendly insulation, and smart manufacturing compatibility, showcasing both maturity and growth potential across multiple verticals.

In 2024, flexible power and control cables dominated the market, accounting for approximately 38% of total adoption. Their prevalence is tied to their versatility in machinery, assembly lines, and conveyor systems, where durability and safety are essential. Fiber-optic cables, currently holding around 22% of adoption, are the fastest-growing type, supported by a CAGR of 9.1% as industries accelerate data-driven operations and high-speed connectivity needs. Hybrid cables, combining power and data transmission, represented about 15% of the market, with increasing uptake in robotics and automation-intensive applications. Remaining types, including coaxial and specialty cables, together contributed 25%, serving niche uses in defense, mining, and harsh environments.

Robotics and factory automation led the application segment in 2024, representing 36% of total adoption. This leadership is driven by the critical need for reliable cabling to support robotic arms, conveyors, and assembly systems. Process industries, including oil, gas, and chemicals, followed with 28% adoption, while energy and utilities accounted for 18%. Transportation and logistics made up 12%, while other applications represented the remaining 6%. While factory automation dominates, the fastest-growing application is energy and utilities, expanding at a CAGR of 8.7%, as renewable energy projects and smart grids demand resilient, high-performance cabling.

In 2024, more than 42% of enterprises globally reported integrating automation cabling solutions into manufacturing execution systems to streamline real-time monitoring. Additionally, over 55% of logistics companies enhanced warehouse efficiency by deploying advanced cabling in automated storage and retrieval systems.

Manufacturing was the leading end-user in 2024, accounting for 40% of global adoption, due to its reliance on automated production lines, robotics, and connected factory infrastructure. Automotive followed with 22%, supported by demand for electric vehicle assembly and advanced production plants. Healthcare held 14%, while aerospace and defense collectively contributed 11%. Other industries, including logistics, energy, and retail, made up the remaining 13%. Healthcare is the fastest-growing end-user, projected to expand at a CAGR of 9.4%, driven by digital hospital infrastructure, surgical robotics, and connected medical equipment.

In 2024, nearly 46% of manufacturers in advanced economies reported implementing predictive maintenance systems requiring industrial-grade cabling for real-time machine health monitoring. Similarly, 39% of healthcare providers invested in automation-compatible cables to support robotic-assisted surgeries and AI-enabled diagnostic equipment.

Europe accounted for the largest market share at 34% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.5% between 2025 and 2032.

Europe’s dominance stems from Germany, which alone represented 14% of the global market due to its advanced industrial base and widespread Industry 4.0 adoption. The region benefits from strong regulations, sustainable manufacturing practices, and heavy automation investments exceeding USD 18 billion in 2024. In contrast, Asia-Pacific, led by China, India, and Japan, is witnessing rapid infrastructure expansion and automation adoption. By 2032, the region is expected to capture 31% of global demand, supported by a large-scale shift to smart factories and robotics-driven manufacturing.

North America held a 28% share of the global Industrial Automation Cable Market in 2024, with the United States leading adoption across manufacturing, automotive, and healthcare sectors. Strong demand is driven by automotive assembly plants, aerospace facilities, and food processing industries. Regulatory changes such as stricter energy efficiency mandates and the expansion of the National Institute of Standards and Technology (NIST) frameworks are enhancing demand for advanced cabling solutions. Technological trends such as smart factory rollouts and IoT-enabled predictive maintenance are widespread. Local player General Cable invested heavily in high-flex and hybrid cabling solutions in 2024 to meet industrial robotics requirements. Consumer behavior reflects higher enterprise adoption in healthcare and finance, where 56% of facilities have integrated high-performance cabling systems to support digital operations.

Europe commanded the largest market share at 34% in 2024, led by Germany, the UK, and France. Germany alone accounted for 14% of the global share, supported by its strong automotive, machinery, and chemical industries. The European Union’s push for sustainability, coupled with initiatives such as the European Green Deal and stricter REACH compliance, has encouraged the adoption of eco-friendly automation cables. Emerging technologies such as fiber-optic and hybrid cables are increasingly used in advanced manufacturing facilities. Local player Leoni AG expanded its production of automation-ready fiber cables in 2024 to support robotics and energy-efficient infrastructure. Consumer behavior is shaped by regulatory pressure, with 62% of enterprises prioritizing sustainability and explainable digital transformation in procurement decisions.

Asia-Pacific ranked second by volume in 2024 and is expected to be the fastest-growing market, projected to account for 31% of demand by 2032. China, Japan, and India are the largest consumers, with China alone responsible for over 12% of the global market volume. Growth is fueled by manufacturing expansion, smart city projects, and government incentives supporting robotics and automation. Technological innovation hubs such as Shenzhen and Bengaluru are spearheading the adoption of IoT-enabled cables. Local player LS Cable & System in South Korea launched flexible automation cables tailored for electronics assembly lines in 2024, strengthening regional competitiveness. Consumer behavior reflects strong demand from e-commerce, mobile-driven AI applications, and high-speed electronics production, which are pushing cable manufacturers to increase output capacity.

South America represented 8% of the global Industrial Automation Cable Market in 2024, with Brazil and Argentina accounting for the majority of demand. Infrastructure upgrades, renewable energy investments, and automotive assembly operations are major contributors. Government incentives, including tax breaks for local manufacturing in Brazil, have encouraged the deployment of automation cabling in industrial plants. Demand for durable and flexible cables is also rising in mining operations and food processing facilities. Local cabling firms in Brazil are increasingly collaborating with multinational automation players to supply high-flex power and data cables. Consumer behavior in this region reflects demand for localized solutions, including Spanish- and Portuguese-language interfaces in automation systems, as enterprises prioritize media and language localization in digital transformation.

The Middle East & Africa accounted for 6% of global market demand in 2024, led by the UAE, Saudi Arabia, and South Africa. Oil & gas, construction, and mining industries are the largest consumers of industrial automation cables. The UAE’s Vision 2030 and Saudi Arabia’s diversification initiatives are accelerating modernization and investment in smart manufacturing. Technological advancements such as IoT-enabled plant monitoring and high-performance fiber cabling are being adopted to enhance production efficiency. Local companies in the UAE have begun manufacturing high-durability cables for oilfield automation to reduce import dependency. Consumer behavior shows growing demand for energy-efficient, long-lasting cables, particularly in large infrastructure projects and smart city initiatives, where reliability and sustainability are critical.

Germany – 14% Market Share: Germany leads due to its advanced automotive and machinery industries, extensive Industry 4.0 adoption, and strong automation ecosystem.

China – 12% Market Share: China ranks second, driven by large-scale electronics and manufacturing capacity, along with rapid automation in industrial hubs.

The Industrial Automation Cable Market is characterized by a semi-consolidated competitive environment, with a large number of active competitors—over 70 globally—balanced by strong influence from the leading firms. The top 5 companies together account for about 55–60% of overall production volume and specialty product penetration, leaving the remainder to mid-sized and regional players. Strategic initiatives are prominent: several firms launched high-flex and hybrid cables in 2023–2024 tailored to robotics and smart factory applications, while others expanded manufacturing capacity or invested in enhanced automated testing and quality control systems. Key players are pushing innovation in fiber-optic data transmission cables, flame-retardant and wash-down rated insulation, and long-life designs suited for high-vibration or harsh environments. Partnerships and mergers are also shaping the landscape; for example, acquisition of TPC Wire & Cable by larger interconnect firms, and expanded production in Asia by European manufacturers. Competition is driven by performance reliability, custom engineering, stringent regulatory compliance, and regional proximity to high-demand industrial hubs. The market pressure is high to lower lead times, improve durability (e.g., offering cables rated for thousands of bend cycles), and provide better warranties and service support.

LAPP Group

HELUKABEL GmbH

Sumitomo Electric Industries Ltd.

General Cable

Southwire Company LLC

KEI Industries Ltd.

LS Cable & System Ltd.

Technological innovation is playing a central role in transforming the Industrial Automation Cable Market. One major trend is the rise of hybrid cables, which combine both power and data lines to reduce installation complexity; these are increasingly used in robotics, automated welding stations, and packaging systems. Fiber optic cable technologies are moving beyond telecommunication, being adapted for industrial floor networks to support real-time data, video and control signaling in tightly constrained spaces. Enhanced insulation materials—such as fluoropolymer coatings, cross-linked polyethylene (XLPE), and thermoplastic elastomers—are being used to improve chemical resistance, thermal endurance, and flexibility under cyclic mechanical stress. Automated cable assembly lines are introducing high-precision cutting, over-molding, and abrasion-resistant sheathing capabilities to meet specifications for harsh environments. Monitoring technologies embedded within cable systems—e.g. fiber-optic sensing for temperature or strain—are enabling predictive maintenance and early fault detection. Also, standards such as Single Pair Ethernet (SPE), EtherCAT, PROFINET, and Industrial Ethernet are increasingly important, pushing cable designs toward higher data rates, better signal integrity, and lower latency. As digitalization and automation intensify, technologies that enable quicker deployment, longer cable life, and tighter tolerances are becoming major differentiators among suppliers.

In April 2024, Amphenol TPC Wire & Cable expanded its Custom Cable Assembly & Solution Center by 60%, adding climate-controlled assembly space and automated testing equipment to reduce lead times and improve production capacity. Source: www.amphenol.com

In 2023, Belden introduced new Ethernet cables with real-time monitoring capabilities, aimed at smart factory and industrial automation network environments.

In early 2024, LS Cable & System secured major supply contracts in the automotive sector in China for high-flex and flame-resistant industrial automation cables.

In 2023, BizLink released an Ethernet-APL cable that also meets Single Pair Ethernet standards for process automation, enhancing connectivity options in industrial automation installations. Source: www.bizlinktech.com

This report’s scope covers in depth product types such as power cables, control & instrumentation cables, sensor bus cables, fiber-optic industrial cables, hybrid power-data solutions, and specialty/environments-specific variants (e.g., high-temperature, abrasion-resistant, chemical/wash-down rated). Application sectors span traditional factory automation, robotics, automotive manufacturing, electronics/semiconductors, process industries (oil & gas, chemical, food & beverage), power & utilities, and renewable energy systems. End-users include manufacturing plants, automotive OEMs, electronics assembly lines, energy and utilities companies, and infrastructure players. Geographic coverage includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa with attention to regional technology adoption rates, regulatory frameworks (e.g. EU RoHS, Green Deal standards), and industrial policies. The report also examines innovation trends (hybrid cables, IoT-embedded monitoring, SPE), manufacturing capacity expansions, sustainability in materials and production, and the evolving competitive landscape including product launches, mergers, and strategic partnerships. It is designed to guide decision-makers in procurement, investment, and product development priorities.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 1,120.0 Million |

| Market Revenue (2032) | USD 1,895.8 Million |

| CAGR (2025–2032) | 6.8% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Prysmian Group, Belden Inc., Nexans, LAPP Group HELUKABEL GmbH, Sumitomo Electric Industries Ltd., General Cable, Southwire Company LLC, KEI Industries Ltd., LS Cable & System Ltd. |

| Customization & Pricing | Available on Request (10% Customization is Free) |