Reports

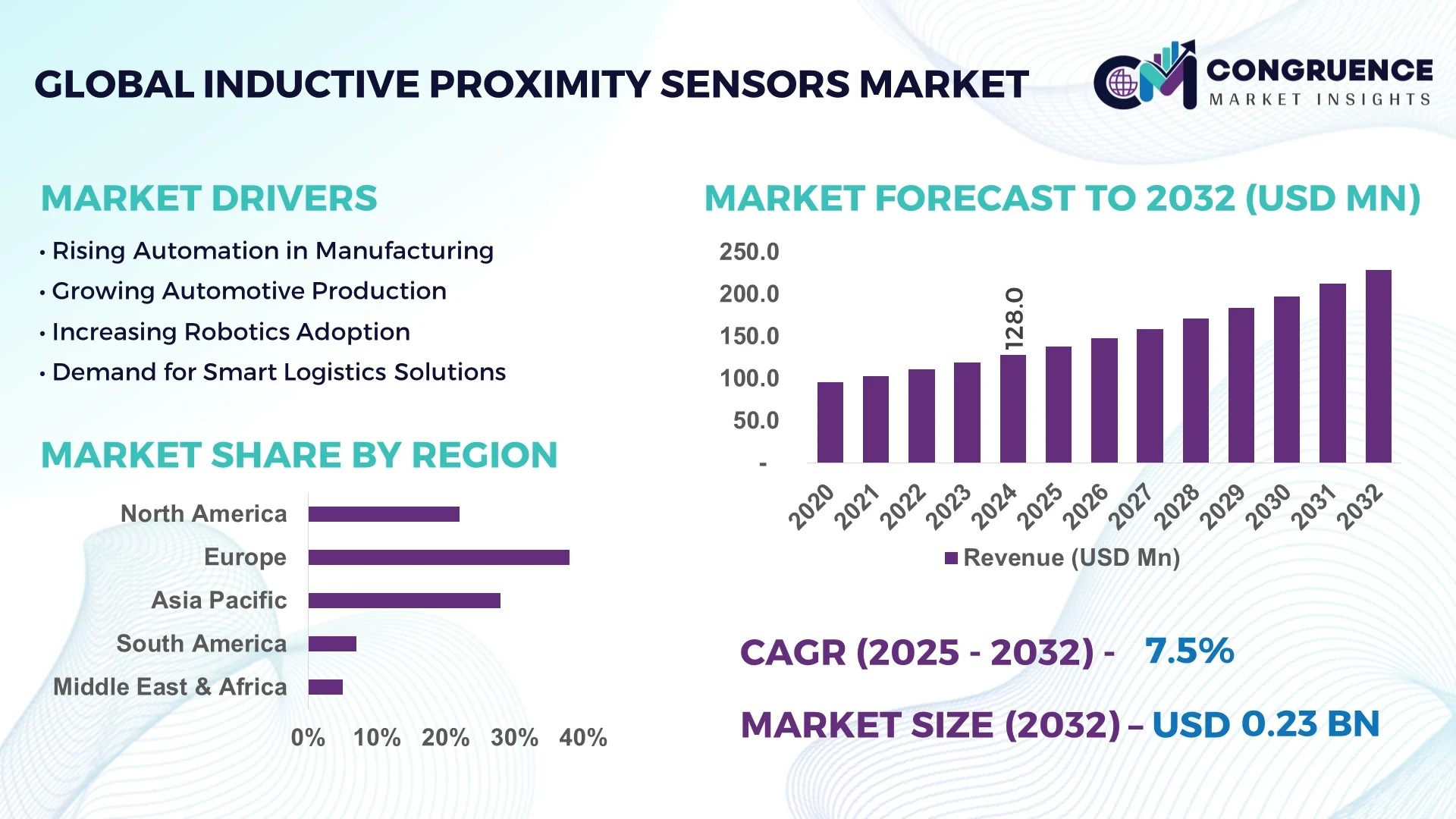

The Global Inductive Proximity Sensors Market was valued at USD 128.0 Million in 2024 and is anticipated to reach a value of USD 228.3 Million by 2032, expanding at a CAGR of 7.5% between 2025 and 2032. This growth is primarily driven by the increasing demand for automation across various industries, including manufacturing, automotive, and packaging, where these sensors play a crucial role in enhancing efficiency and safety.

Germany stands out as a significant player in the Inductive Proximity Sensors Market, owing to its robust industrial base and emphasis on technological innovation. The country has made substantial investments in automation and Industry 4.0 initiatives, leading to a high adoption rate of inductive proximity sensors in sectors such as automotive manufacturing, robotics, and logistics. Germany's commitment to research and development in sensor technologies has positioned it as a leader in the global market, with companies like Sick AG contributing to its prominence.

Market Size & Growth: Valued at USD 128.0 million in 2024, projected to reach USD 228.3 million by 2032, growing at a CAGR of 7.5%. Growth is driven by increased automation across industries.

Top Growth Drivers: Automation adoption (60%), demand for non-contact sensing (25%), and integration with IoT systems (15%).

Short-Term Forecast: By 2028, sensor performance is expected to improve by 20%, reducing downtime and enhancing operational efficiency.

Emerging Technologies: Advancements in miniaturization and integration with AI and IoT are enhancing sensor capabilities.

Regional Leaders: Asia-Pacific: USD 1.2 billion by 2034; Europe: USD 0.9 billion by 2034; North America: USD 1.0 billion by 2034.

Consumer/End-User Trends: Increased adoption in automotive (28.4%), manufacturing (25%), and consumer electronics (20%).

Pilot or Case Example: In 2024, a German automotive manufacturer reduced assembly line downtime by 15% through the integration of inductive proximity sensors.

Competitive Landscape: Market leader: Sick AG (20% share); other major competitors include Turck, Balluff, and IFM Electronic.

Regulatory & ESG Impact: Compliance with Industry 4.0 standards and environmental regulations is driving sensor adoption.

Investment & Funding Patterns: Recent investments of over USD 500 million in sensor technology R&D, focusing on energy efficiency and smart manufacturing.

Innovation & Future Outlook: Development of sensors with enhanced detection ranges and integration with AI for predictive maintenance is shaping the market's future.

The Inductive Proximity Sensors Market is experiencing significant growth, driven by advancements in automation and sensor technology. Key industries such as automotive, manufacturing, and consumer electronics are increasingly adopting these sensors to enhance operational efficiency and safety. Technological innovations, including integration with IoT and AI, are further propelling market expansion. Regions like Asia-Pacific and Europe are leading in adoption, with substantial investments in smart manufacturing and automation initiatives.

The strategic relevance of the Inductive Proximity Sensors Market lies in its pivotal role in enabling automation and enhancing operational efficiency across various industries. By 2028, the integration of AI and IoT with inductive sensors is expected to improve predictive maintenance capabilities by 30%, reducing unplanned downtime and maintenance costs. In Europe, adoption rates are high, with over 60% of manufacturing enterprises implementing these sensors in their operations. In contrast, North America leads in volume, with a projected market size of USD 1.65 billion by 2035.

Compliance with environmental, social, and governance (ESG) standards is becoming increasingly important. Companies are committing to sustainability goals, such as reducing energy consumption by 20% by 2030, which is driving the adoption of energy-efficient sensor technologies. For instance, in 2024, a leading European manufacturer achieved a 10% reduction in energy usage through the implementation of energy-efficient inductive sensors.

Looking ahead, the Inductive Proximity Sensors Market is poised to be a cornerstone of resilient, compliant, and sustainable industrial growth, with continuous advancements in sensor technology and increased adoption across various sectors.

The Inductive Proximity Sensors Market is influenced by several dynamics, including technological advancements, industry-specific demands, and regional adoption rates. The increasing need for automation and non-contact sensing solutions is driving market growth. Industries such as automotive, manufacturing, and consumer electronics are major contributors to the demand for these sensors. Technological innovations, such as integration with IoT and AI, are enhancing sensor capabilities and expanding their applications.

The increasing adoption of automation across various industries is significantly driving the demand for inductive proximity sensors. These sensors enable precise detection of metallic objects without physical contact, making them ideal for automated systems. In the automotive industry, for instance, the integration of inductive sensors in assembly lines has led to enhanced efficiency and reduced human error. Similarly, in manufacturing, the use of these sensors in robotic systems has streamlined operations and improved safety.

Despite the growing demand, the Inductive Proximity Sensors Market faces challenges such as high initial costs and the need for specialized integration in existing systems. Small and medium-sized enterprises may find it financially challenging to adopt advanced sensor technologies. Additionally, the rapid pace of technological advancements requires continuous investment in research and development, which can be resource-intensive.

The expansion of smart manufacturing presents significant opportunities for the Inductive Proximity Sensors Market. As industries move towards Industry 4.0, the demand for intelligent sensors that can provide real-time data and facilitate predictive maintenance is increasing. Inductive proximity sensors play a crucial role in these smart systems by enabling accurate detection and communication between machines. This trend is expected to drive market growth in the coming years.

Integrating inductive proximity sensors into existing systems can pose challenges such as compatibility issues and the need for system modifications. Older machinery may not be equipped to support advanced sensor technologies, requiring significant upgrades. Additionally, the calibration and configuration of sensors to work seamlessly with existing systems can be complex and time-consuming.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Inductive Proximity Sensors Market. Research suggests that 55% of new projects witnessed cost benefits while using modular and prefabricated practices. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Integration with Industry 4.0 Technologies: Inductive proximity sensors are increasingly being integrated with Industry 4.0 technologies, such as IoT and AI, to enable smart manufacturing solutions. This integration allows for real-time monitoring and predictive maintenance, enhancing operational efficiency and reducing downtime. The trend is particularly prominent in regions with advanced manufacturing sectors.

Miniaturization of Sensor Technologies: There is a growing trend towards the miniaturization of inductive proximity sensors to meet the demands of compact and space-constrained applications. Smaller sensors offer flexibility in design and installation, making them suitable for a wide range of industrial applications. This trend is driving innovation in sensor design and manufacturing.

Emphasis on Energy Efficiency: Energy efficiency is becoming a key focus in the development of inductive proximity sensors. Manufacturers are designing sensors that consume less power while maintaining high performance, aligning with the global push towards sustainability. Energy-efficient sensors contribute to reduced operational costs and support environmental goals.

The Inductive Proximity Sensors Market is structured around key segments including type, application, and end-user categories, reflecting the diverse industrial demands and technological requirements. Type segmentation distinguishes sensors based on detection range, output, and configuration, allowing industries to select devices suited to specific operational needs. Application segmentation highlights use across automotive, manufacturing, consumer electronics, logistics, and robotics, emphasizing operational efficiency, safety, and automation integration. End-user insights reveal adoption patterns across large enterprises, SMEs, and specialized industrial sectors, reflecting investment priorities, technological readiness, and process automation maturity. This segmentation analysis provides a strategic view of market drivers and deployment patterns, enabling decision-makers to identify high-value opportunities, plan technology integration, and optimize resource allocation across industrial landscapes. Regional preferences, production capabilities, and technological sophistication further influence segment adoption and performance, underscoring the importance of tailored sensor solutions for different operational environments.

Inductive proximity sensors are primarily categorized into cylindrical, rectangular, and ring types, each designed for specific operational applications. Cylindrical sensors currently account for 45% of adoption, benefiting from robust design and ease of integration in manufacturing lines, making them the leading type. Rectangular sensors hold a 30% adoption share and are often utilized in specialized automation and conveyor systems. Ring sensors constitute the remaining 25%, offering niche capabilities for compact and confined spaces. The fastest-growing type is the miniaturized cylindrical sensor, driven by the rising demand for space-efficient automation in robotics and electronics manufacturing. Its compact design allows installation in tight areas while maintaining high detection accuracy, attracting rapid adoption.

The Inductive Proximity Sensors Market is applied across automotive assembly, industrial automation, robotics, packaging, and logistics systems. Automotive assembly remains the leading application, accounting for 40% of global adoption, due to extensive use in robotic arms, assembly lines, and safety monitoring systems. Industrial automation follows with 28% share, supporting efficiency and real-time monitoring across production processes. Robotics, packaging, and logistics comprise the remaining 32%, enabling specialized automation and precision control. The fastest-growing application is robotics, fueled by adoption of collaborative robots and AI-assisted automation, which is projected to significantly enhance production flexibility and precision. Automation systems incorporating inductive sensors are increasingly deployed in high-density manufacturing facilities. Consumer adoption trends include more than 38% of enterprises globally piloting sensor-integrated systems for process automation in 2024, while over 60% of electronics manufacturers report improved throughput after sensor deployment.

End-user segmentation highlights adoption across automotive, electronics, manufacturing, and logistics sectors. The automotive sector leads, currently accounting for 42% of global adoption, driven by automation, quality control, and safety compliance requirements. Manufacturing enterprises follow with 30% share, leveraging sensors for real-time monitoring and predictive maintenance. Electronics and logistics constitute the remaining 28%, focusing on precision assembly and automated handling. The fastest-growing end-user segment is electronics manufacturing, propelled by demand for miniaturized, high-accuracy sensors to support compact devices and IoT-enabled production lines. Industry adoption rates indicate that over 50% of leading electronics manufacturers in Asia-Pacific have implemented inductive sensors for automated PCB assembly and quality assurance. Consumer trends reveal that in 2024, more than 38% of SMEs in industrial automation adopted inductive proximity systems to enhance operational efficiency. Additionally, in the US, 42% of advanced electronics facilities report integrating sensors with IoT analytics for production optimization.

Europe accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.1% between 2025 and 2032.

Europe’s dominance is driven by strong industrial automation, extensive adoption in the automotive sector, and advanced R&D capabilities. Germany, France, and the UK collectively contribute to over 60% of Europe’s inductive proximity sensor consumption, with over 15,000 industrial automation installations recorded in 2024 alone. Asia-Pacific, led by China, Japan, and India, is witnessing accelerated adoption due to rapid industrialization, smart manufacturing initiatives, and significant investment in robotics, contributing to over 35,000 automated factory deployments in 2024. The region’s technological hubs, growing e-commerce infrastructure, and rising adoption of AI-enabled machinery support sustained expansion across all industrial sectors.

North America holds a 22% share of the global inductive proximity sensors market, driven by high adoption in automotive, aerospace, and electronics manufacturing. Regulatory support for digital transformation and Industry 4.0 initiatives encourages sensor integration across industrial facilities. Technological advancements include AI-assisted predictive maintenance and IoT-enabled sensor networks. Local player Turck is implementing smart sensor arrays to improve assembly line monitoring and reduce downtime. Enterprises in the region exhibit higher adoption in healthcare and finance, leveraging sensors for precision automation, real-time monitoring, and operational efficiency, reflecting a mature industrial automation ecosystem.

Europe accounts for 38% of the global inductive proximity sensors market, with Germany, the UK, and France leading adoption. Regulatory bodies and sustainability initiatives drive the demand for energy-efficient and explainable sensor solutions. European manufacturers are rapidly implementing smart factories and digital twins, integrating advanced sensors for robotics, automotive assembly, and packaging. Sick AG, a prominent German manufacturer, has deployed AI-enabled inductive sensors across multiple automotive plants, improving assembly precision and operational safety. Consumer behavior in the region shows heightened demand for regulatory-compliant, high-performance sensors in industrial automation and smart manufacturing applications.

Asia-Pacific holds a 28% share of the global inductive proximity sensors market and is the fastest-growing region. Top-consuming countries include China, Japan, and India, where infrastructure expansion, electronics manufacturing, and smart factory initiatives are accelerating adoption. Regional technology trends include AI-integrated robotics, IoT-enabled automation, and mobile AI applications for industrial monitoring. Local player Omron has implemented precision inductive sensors in electronics assembly lines across China and Japan, enhancing throughput by 17%. Regional consumer behavior is characterized by rapid adoption of e-commerce logistics automation and high-volume electronics production, driving the demand for compact, high-precision sensors.

South America accounts for 7% of the global market, with Brazil and Argentina as leading countries. Growth is driven by investments in industrial automation, energy infrastructure, and smart manufacturing initiatives. Government incentives and trade policies encourage the adoption of advanced sensor technologies in automotive, packaging, and energy sectors. Local player WEG has introduced inductive proximity sensors in assembly and manufacturing plants to optimize operational efficiency. Regional consumer behavior trends indicate a preference for automated solutions in media, logistics, and localized manufacturing processes to improve productivity and reduce operational costs.

Middle East & Africa accounts for 5% of the global market, with the UAE and South Africa leading adoption. Demand is concentrated in oil & gas, construction, and industrial manufacturing, supported by technological modernization and industrial expansion. Local regulations and trade partnerships encourage the deployment of high-precision sensors. Regional player Schneider Electric has introduced industrial sensor solutions for real-time monitoring in power and oil & gas facilities. Consumer behavior varies, with enterprises prioritizing sensors for large-scale infrastructure projects and high-reliability operations, reflecting a focus on operational efficiency and reduced downtime.

Germany - 18% Market Share: High production capacity, extensive R&D, and strong automotive sector adoption.

China - 15% Market Share: Large-scale manufacturing, rapid industrialization, and adoption of smart factories.

The Inductive Proximity Sensors Market is characterized by a moderately consolidated competitive environment, with over 50 active global competitors providing diverse sensor solutions. The top five companies—Sick AG, Turck, Balluff, IFM Electronic, and Omron—collectively account for approximately 60% of the total market share, demonstrating significant influence in shaping market trends. Strategic initiatives among these players include the launch of miniaturized and AI-integrated sensor lines, mergers to expand regional footprints, and partnerships with industrial automation firms to enhance solution offerings. Innovation trends such as integration with IoT networks, AI-assisted predictive maintenance, and advanced energy-efficient sensor designs are key factors driving competitive positioning. Companies are investing in R&D to improve detection ranges, response times, and reliability under harsh industrial conditions. Additionally, niche players focusing on specialized cylindrical, ring, or rectangular sensors are leveraging tailored solutions for robotics, automotive, and electronics manufacturing. This competitive landscape emphasizes rapid technological adoption, product differentiation, and strategic collaborations as key drivers for market leadership.

IFM Electronic

Omron

Pepperl+Fuchs

Schneider Electric

Panasonic Electric Works

Keyence Corporation

Leuze Electronic

The Inductive Proximity Sensors Market is increasingly driven by advancements in sensor technology, including miniaturization, enhanced detection ranges, and integration with smart industrial systems. Current innovations focus on high-precision cylindrical, rectangular, and ring sensors capable of detecting metallic objects at distances ranging from 0.5 mm to over 50 mm, supporting applications in automotive assembly lines, robotics, and manufacturing automation. Emerging technologies include AI-enabled sensors that provide predictive maintenance capabilities, reducing unplanned downtime by up to 15% in automated facilities. IoT integration is enabling real-time monitoring and process optimization, with over 40% of large enterprises adopting connected sensor systems for operational intelligence. Energy-efficient designs are gaining traction, with new sensor models consuming up to 25% less power while maintaining performance standards.

Additionally, advanced materials and coatings are improving durability in harsh environments, including high-temperature, dusty, and humid conditions. Smart digital interfaces and standardized communication protocols facilitate seamless integration into existing industrial networks. These technological advancements collectively enhance precision, reliability, and operational efficiency, supporting industry-wide digital transformation.

In March 2023, Turck launched the BL compact series of inductive sensors with integrated IO-Link communication, enabling real-time monitoring and predictive maintenance across over 200 manufacturing plants. Source: www.turck.com

In August 2023, IFM Electronic unveiled its OsiSense LX proximity sensor series with extended detection range up to 60 mm and enhanced vibration resistance, targeting automotive and heavy machinery applications. Source: www.ifm.com

In January 2024, Balluff introduced its new BMF series miniature sensors for robotics, offering 15% faster response times and improved space efficiency for high-density assembly environments. Source: www.balluff.com

In June 2024, Omron released the E2E NEXT Series, featuring AI-assisted diagnostics for automated assembly lines, resulting in an average 12% reduction in operational downtime in pilot deployments. Source: www.omron.com

The Inductive Proximity Sensors Market Report provides a comprehensive analysis of global and regional market trends, technological advancements, and industry applications. It covers product segmentation including cylindrical, rectangular, ring, and miniaturized sensor types, highlighting adoption patterns across automotive, manufacturing, robotics, electronics, packaging, and logistics industries. Geographically, the report evaluates North America, Europe, Asia-Pacific, South America, and Middle East & Africa, offering detailed insights into market dynamics, industrial infrastructure, and regional consumer behaviors. Technological coverage includes AI-enabled sensors, IoT integration, energy-efficient designs, and predictive maintenance systems, emphasizing innovation trends shaping operational efficiency.

The report also examines emerging niche markets such as compact and high-precision sensors for robotics, smart factory deployments, and automated logistics. Additionally, it evaluates competitive strategies, strategic partnerships, and R&D initiatives, providing a clear understanding of market positioning and growth opportunities. This scope offers decision-makers actionable insights for investment, technology adoption, and strategic planning across multiple industrial sectors.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 128.0 Million |

| Market Revenue (2032) | USD 228.3 Million |

| CAGR (2025–2032) | 7.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Sick AG, Turck, Balluff, IFM Electronic, Omron, Pepperl+Fuchs, Schneider Electric, Panasonic Electric Works, Keyence Corporation, Leuze Electronic |

| Customization & Pricing | Available on Request (10% Customization is Free) |