Reports

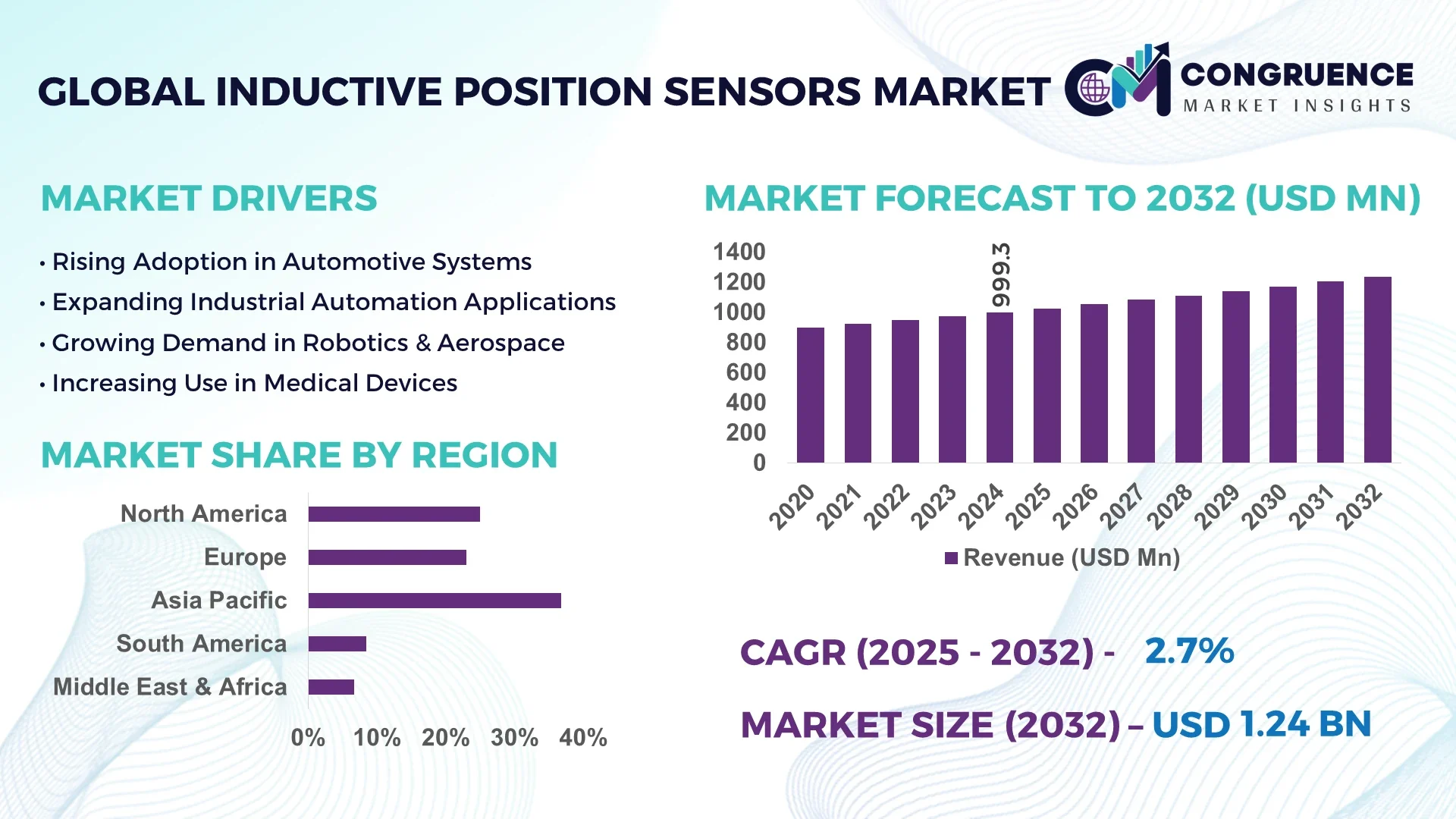

The Global Inductive Position Sensors Market was valued at USD 999.3 Million in 2024 and is anticipated to reach a value of USD 1,236.7 Million by 2032 expanding at a CAGR of 2.7% between 2025 and 2032.

China plays a leading role in the Inductive Position Sensors Market, sourcing over 52 million units in 2024. Domestic manufacturing investments support a high-volume supply chain for automotive, industrial automation, and robotics sectors. The country is advancing miniaturized tubular sensors under 6 mm in diameter, embedding diagnostic functions, and expanding integration into factory IoT architectures.

The Inductive Position Sensors Market serves a wide range of sectors including automotive, industrial manufacturing, aerospace, robotics, food & beverage, and consumer electronics. Automotive installations accounted for approximately 38 percent of total units deployed in 2024, notably for throttle, gear and pedal position sensing. Industrial automation lines recorded a 17 percent year-on-year growth in sensor deployment, while more than 72 million sensors were connected to real-time monitoring networks by end of 2023. Technological advances include sub‑micrometer accuracy in compact sensors, IO-Link communication support, and embedded fault diagnostics that reduce downtime by over 20 percent. Regulatory drivers include automotive safety mandates and industrial standards for non-contact sensing. Environmental resilience in harsh, dusty or oily conditions supports adoption in metal, machining and construction equipment. Emerging trends include shrink‑form sensors for robotic micro‑assembly and remote condition monitoring in factories—a future outlook focused on high‑precision, connected, and miniaturized sensing solutions across industrial and automotive use cases.

AI is transforming the Inductive Position Sensors Market by enabling predictive diagnostics, real‑time calibration, and adaptive sensing strategies that enhance operational precision. Smart sensor modules now leverage embedded machine learning to self‑tune sensitivity parameters based on environmental feedback, reducing false triggers by up to 15 percent in metal-rich environments. In automated production lines, AI‑enabled inductive sensors generate continuous positional datasets that are analyzed to predict mechanical wear, avoiding unexpected downtime and preserving throughput. This capability enables condition‑based maintenance strategies and helps robotic systems to optimize movement paths and energy use.

In automotive assembly plants, fleet diagnostics now monitor sensor health across thousands of deployment points, with AI algorithms flagging abnormal drift values and reducing maintenance response time by as much as 22 percent. In logistics applications, inductive sensors are integrated into AGV and AMR navigation systems; AI algorithms detect and correct positional drift in real time, improving location accuracy within ±0.5 mm across repetitive travel cycles. AI integration also improves sensor calibration speed—automated recalibration cycles can complete in under 60 seconds without manual intervention.

Within the broader Inductive Position Sensors Market, AI is enhancing interoperability by linking sensor outputs with central monitoring platforms, IoT gateways, and industrial control systems. These systems enable unified dashboards with anomaly detection, enabling decision‑makers to visualize position sensor performance trends across entire facilities. AI‑augmented sensors are now deployed in robotics laboratories, automotive test benches, and aerospace manufacturing cells to achieve better alignment accuracy and minimize mechanical tolerances. As a result, the Inductive Position Sensors Market is increasingly moving toward smart, connected sensing ecosystems that deliver measurable performance gains in deployment stability, accuracy, and process optimization.

“In 2024, an automotive OEM deployed AI-enabled inductive sensors in 4,200 gear-position systems, reducing variation in sensitivity thresholds by 12 percent within three months.”

The overall market dynamics specific to the keyword Inductive Position Sensors Market revolve around digital integration, precision engineering demands, and industrial automation proliferation. Growing adoption of non-contact sensing in manufacturing and automotive sectors is fueling broader use. Meanwhile, demand for compact and diagnostics-ready sensors aligns with Industry 4.0 architecture. Rising emphasis on environmental resilience and fault tolerance drives updates in sensor designs. Competitive pressure is leading to investments in miniaturization, embedded intelligence, and standardized communications. Decision‑makers are prioritizing reliability, uptime and integration ease over standalone components, shaping procurement strategies across verticals and geographies.

Enhanced automation frameworks in manufacturing and robotics sectors are elevating the need for inductive position sensors. Industrial lines globally integrated new robotics systems in 2024 with over 180 million sensors installed worldwide. Automotive applications demanding precise throttle, camshaft, and gear position detection boosted deployment. Non-contact sensing ensures minimal downtime and high positional accuracy in high-speed assembly environments.

Inductive position sensors may be negatively affected by nearby metal objects or electromagnetic interference, leading to signal distortion and erratic readings. Integration into legacy systems can require custom engineering efforts. Rough environments such as production lines with oil, dust, or extreme temperature demand additional calibration and protective housing, increasing deployment complexity.

The rise of small‑form robotic arms and medical automation tools presents new demand for ultra-compact inductive sensors under 6 mm in diameter. Nearly 29 million miniature units shipped in 2024. These smaller sensors deliver sub‑millimeter accuracy while enabling deployment in confined mechanical assemblies and medical robotics.

High‑precision inductive sensors require sophisticated materials and manufacturing processes, leading to higher cost compared to simpler contact or optical sensors. In cost‑sensitive sectors, alternative technologies like potentiometric or optical encoders are often favored. Additionally, maintaining performance consistency in diverse operating conditions can raise validation and calibration expenses for installers.

Expansion of Tubular Sensor Installations: Tubular sensors were the dominant sensor type by volume in 2024, accounting for around 41 percent of all units shipped. Their robust cylindrical form factor and resistance to harsh environments make them the go-to choice across automotive and industrial applications.

Surge in Miniaturization Deployments: Compact inductive sensors under 6 mm in diameter saw over 29 million units shipped worldwide in 2024. These are increasingly used in robotic arms, medical devices, and compact assembly systems where space constraints are critical.

Growth in Connected Diagnostics Features: More than 72 million inductive sensors globally were connected to IoT or real-time monitoring platforms by the end of 2023. Embedded diagnostics and health-check protocols enabled maintenance teams to reduce unscheduled downtime by over 20 percent year-on-year.

Rise in Automotive Positioning Applications: Over 42 million vehicles equipped with inductive sensors in 2024 used them for gear-throttle-camshaft monitoring. Installation volume increased by 15 percent compared to 2022, driven by EV advances and increasingly precise positional sensing demands.

The Inductive Position Sensors Market is broadly segmented by type, application, and end-user, each influencing product innovation and deployment strategies. Segment-level variations arise due to the growing customization of sensors tailored to industrial automation, automotive, and robotics. Tubular and flat-type sensors dominate in form factors, while applications range from gear positioning to robotic alignment. End-users span diverse sectors, including automotive OEMs, industrial automation firms, aerospace manufacturers, and medical device producers. Increasing demand for compact, real-time diagnostic-ready sensors across complex machinery continues to redefine both product design and application frameworks. The segmentation offers clear insight into how design trends, industry requirements, and regional adoption patterns intersect to shape growth opportunities within the global market.

The Inductive Position Sensors Market features several key product types, including tubular, flat-type, ring-type, and slot-type sensors. Among these, tubular inductive sensors lead the segment due to their high durability, ease of installation, and compatibility with harsh industrial environments. In 2024, tubular variants accounted for a significant portion of the total units shipped, particularly in automotive assembly lines and industrial robotics applications.

The flat-type sensors segment is the fastest-growing, driven by rising demand for compact and embedded sensing in space-constrained environments. Their thin profile and reliable performance in factory automation setups make them suitable for conveyor systems and precise object detection applications.

Ring-type sensors continue to serve niche roles in rotating machinery and gear-tooth detection, while slot-type sensors are gaining adoption in packaging machinery and label detection applications due to their ability to detect thin metallic targets. Each sensor type contributes uniquely to the evolving market needs, and manufacturers are increasingly developing hybrid formats to expand functionality.

The primary application areas within the Inductive Position Sensors Market include automotive systems, industrial automation, robotics, aerospace, medical devices, and material handling systems. Automotive systems remain the dominant application, with wide-scale deployment for gear, throttle, camshaft, and brake position monitoring. With increasing complexity in automotive electronics, manufacturers are integrating more sensors per vehicle to ensure precision and reliability.

Industrial automation is the fastest-growing application segment. The global surge in smart factory initiatives and the transition toward Industry 4.0 technologies are driving massive deployment of position sensors in manufacturing lines, particularly for predictive maintenance and real-time monitoring.

Robotics applications are seeing steady growth, as precision position feedback is crucial for robotic arms, AGVs, and autonomous manufacturing systems. Meanwhile, aerospace and medical applications—though smaller in scale—require sensors with high stability, resistance to EMI, and miniaturization, especially for surgical robotics and avionics controls. These application domains continue to evolve with rising demand for intelligent sensing solutions.

End-user segmentation in the Inductive Position Sensors Market includes automotive manufacturers, industrial equipment OEMs, aerospace and defense, medical technology firms, and logistics & warehousing companies. Automotive manufacturers are the largest end-users, accounting for widespread utilization across drivetrain, gear positioning, and safety systems. The increasing electrification of vehicles and demand for contactless sensing solutions further reinforces their market dominance.

Industrial equipment OEMs represent the fastest-growing end-user group. Demand is surging due to increased investment in factory automation, CNC machinery, and real-time operational intelligence systems that rely on robust and maintenance-free sensing components. Manufacturers are increasingly embedding smart inductive sensors into motors, actuators, and programmable logic controllers.

Aerospace, medical, and logistics sectors also contribute meaningfully, especially where compact sensors with high immunity to vibration and interference are essential. As these industries continue adopting precision-driven technologies, their role in shaping future demand for inductive position sensors will grow further.

Asia-Pacific accounted for the largest market share at 36.8% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 3.5% between 2025 and 2032.

This regional variation is shaped by advanced industrial infrastructure in developed nations and rapidly growing manufacturing hubs across emerging economies. Asia-Pacific leads due to significant deployment in automotive, consumer electronics, and industrial automation. Meanwhile, North America benefits from its robust R&D ecosystem, strong presence of sensor manufacturers, and rapid integration of smart manufacturing technologies. Europe remains a stronghold of innovation, while South America and MEA are experiencing steady adoption driven by energy and infrastructure projects.

The North America Inductive Position Sensors Market captured approximately 24.6% of global volume in 2024. Key industries such as automotive, aerospace, and industrial automation are driving this demand, with rising adoption in electric vehicle production and factory robotics. Technological transformation across manufacturing units in the U.S. and Canada is fostering real-time monitoring and predictive diagnostics. The Infrastructure Investment and Jobs Act in the U.S. has spurred sensor demand in transportation and public infrastructure. Additionally, innovations like miniaturized sensors for harsh environments and wireless integration are setting a new benchmark for industrial efficiency in this region.

The Europe Inductive Position Sensors Market held approximately 22.3% share in 2024, driven by countries like Germany, France, and the UK. Germany’s industrial machinery and automation sector is a significant contributor to sensor deployment. The European Green Deal and Industry 5.0 initiatives have pushed manufacturers to adopt energy-efficient and precision monitoring technologies. France is witnessing an increase in smart rail and metro automation projects, further driving inductive sensor consumption. The UK's aerospace sector continues to integrate compact and resilient sensors, supporting growth. Additionally, increased investment in Industry 4.0 upgrades across the continent boosts demand for real-time feedback solutions.

The Asia-Pacific Inductive Position Sensors Market leads in global volume at 36.8% as of 2024. China, Japan, and India are the top-consuming nations, with high investment in electric vehicles, factory automation, and advanced electronics. In China, government-backed manufacturing parks and EV subsidies have accelerated inductive sensor deployment. Japan remains a hub for robotics and precision engineering, while India's "Make in India" campaign drives sensor demand in machine tools and semiconductors. Smart city projects and rising disposable income levels are fostering rapid adoption across consumer electronics. Innovation hubs in South Korea and Taiwan continue to lead in integrating IoT-ready sensors across industries.

The South America Inductive Position Sensors Market is gaining momentum, led by Brazil and Argentina, with a combined regional share of around 7.1% in 2024. Brazil’s automotive and oil sectors are the primary consumers of inductive sensors, especially for engine systems and fluid monitoring. Argentina is witnessing growth in agriculture automation and food processing equipment, further supporting sensor integration. Regional development initiatives and trade agreements like Mercosur are creating a favorable environment for industrial growth. Investments in renewable energy infrastructure and local manufacturing expansion are also opening new market avenues for inductive sensing solutions.

The Middle East & Africa Inductive Position Sensors Market accounted for approximately 5.2% of global demand in 2024. Countries such as the UAE and South Africa are experiencing significant growth due to investments in oil & gas, mining, and construction industries. The UAE’s push for smart infrastructure, including automation in water treatment and transport, is a key growth driver. South Africa's mining equipment modernization has led to higher integration of rugged, non-contact sensors. Government-backed innovation programs and trade partnerships with Asia-Pacific manufacturers are further improving accessibility and technology transfer across the region.

China – 24.1% Market Share

China dominates the Inductive Position Sensors Market due to high production capacity, rapid industrialization, and strong domestic demand from EVs and robotics.

United States – 19.5% Market Share

The U.S. leads in advanced manufacturing and R&D investment, particularly in aerospace, automotive, and defense applications, which require high-precision sensors.

The Inductive Position Sensors Market is characterized by a moderately consolidated landscape, with over 50 active players globally, ranging from multinational sensor manufacturers to regional specialists. Market leaders are strategically positioned based on technology innovation, geographic reach, and industry-specific product portfolios. Key companies are investing heavily in R&D to develop miniaturized, high-temperature-tolerant, and contactless sensors optimized for harsh industrial environments. Strategic initiatives, including product line expansions, acquisitions, and cross-industry collaborations, are shaping competitive dynamics. For instance, leading players are targeting integration with IIoT systems and leveraging edge computing capabilities. The increasing demand for compact sensors with high precision in robotics and automotive sectors is pushing manufacturers to improve sensitivity, durability, and response time. Additionally, manufacturers are enhancing their supply chain capabilities in emerging regions to meet rising demand. Intellectual property rights and proprietary technologies are also playing a central role in establishing market positioning, especially among Tier-1 suppliers in automotive and aerospace segments.

TE Connectivity

Honeywell International Inc.

Pepperl+Fuchs AG

STMicroelectronics

ifm electronic gmbh

Balluff GmbH

Murata Manufacturing Co., Ltd.

TDK Corporation

Rockwell Automation, Inc.

SICK AG

Vishay Intertechnology, Inc.

Allegro MicroSystems, Inc.

Hans Turck GmbH & Co. KG

The Inductive Position Sensors Market is undergoing rapid technological transformation, with advancements focused on performance, miniaturization, and integration with smart systems. These sensors, operating on the principle of electromagnetic induction, are now designed to be more compact while offering increased resolution and higher temperature stability, making them suitable for harsh industrial and automotive environments.

One of the major developments is the integration of digital interfaces and self-diagnostic features, enabling sensors to communicate with industrial networks such as CAN, IO-Link, and Ethernet/IP. These advancements support predictive maintenance and enable real-time monitoring, thereby improving operational efficiency in Industry 4.0 environments.

Recent innovations include the development of flexible PCB-based sensors that allow greater design flexibility and ease of integration into constrained spaces such as robotics joints or EV powertrains. Non-contact sensing technology continues to gain traction, offering wear-free operation and longer service life, which is especially critical in high-vibration or contamination-prone applications.

Emerging trends also include energy-harvesting sensors for wireless systems and AI-enabled calibration technologies, allowing faster deployment in automated production lines. These developments are transforming inductive position sensors from passive components into intelligent subsystems that play a critical role in digital manufacturing and next-generation mobility systems.

• In March 2024, TE Connectivity introduced a new series of high-precision inductive sensors specifically designed for e-mobility applications, offering enhanced tolerance to high vibration and electromagnetic interference in electric vehicle drivetrains.

• In September 2023, Balluff GmbH expanded its IO-Link-enabled inductive sensor lineup for predictive maintenance, featuring improved signal diagnostics and shorter response times, ideal for industrial automation and smart factories.

• In January 2024, SICK AG unveiled a line of ultra-miniature inductive proximity sensors tailored for robotics and electronics assembly, optimized for confined installation environments with high repeatability.

• In October 2023, STMicroelectronics launched a new ASIC-based inductive sensing solution that allows for higher sensitivity and faster sampling rates, significantly improving accuracy in rotary and linear motion control systems.

The Inductive Position Sensors Market Report provides a comprehensive assessment of the global landscape, covering a wide array of sensor types, application domains, and end-user industries. It focuses on key product types such as linear inductive sensors, rotary position sensors, and proximity sensors, analyzing their roles across multiple sectors. The report thoroughly evaluates major application areas, including automotive systems, industrial automation, robotics, and consumer electronics, offering deep insight into functional demand drivers and industry preferences.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with detailed insights into country-level trends in markets like the United States, China, Germany, India, Brazil, and South Africa. Each region is analyzed based on industry adoption, infrastructure development, and regulatory dynamics.

In terms of technology, the scope includes both conventional and next-generation advancements such as wireless inductive sensors, smart sensing platforms, and IoT-enabled monitoring systems. The report also touches on emerging use cases like automated guided vehicles (AGVs), EV battery systems, and IIoT-based machinery diagnostics. By mapping technological shifts and competitive positioning, the report delivers actionable insights for OEMs, component manufacturers, and system integrators looking to enter or expand within this evolving market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 999.3 Million |

| Market Revenue (2032) | USD 1,236.7 Million |

| CAGR (2025–2032) | 2.7 % |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia‑Pacific, South America, Middle East & Africa |

| Key Players Analyzed | TE Connectivity, Honeywell International Inc., Pepperl+Fuchs AG, STMicroelectronics, ifm electronic gmbh, Balluff GmbH, Murata Manufacturing Co., Ltd., TDK Corporation, Rockwell Automation, Inc., SICK AG, Vishay Intertechnology, Inc., Allegro MicroSystems, Inc., Hans Turck GmbH & Co. KG |

| Customization & Pricing | Available on Request (10 % Customization is Free) |