Reports

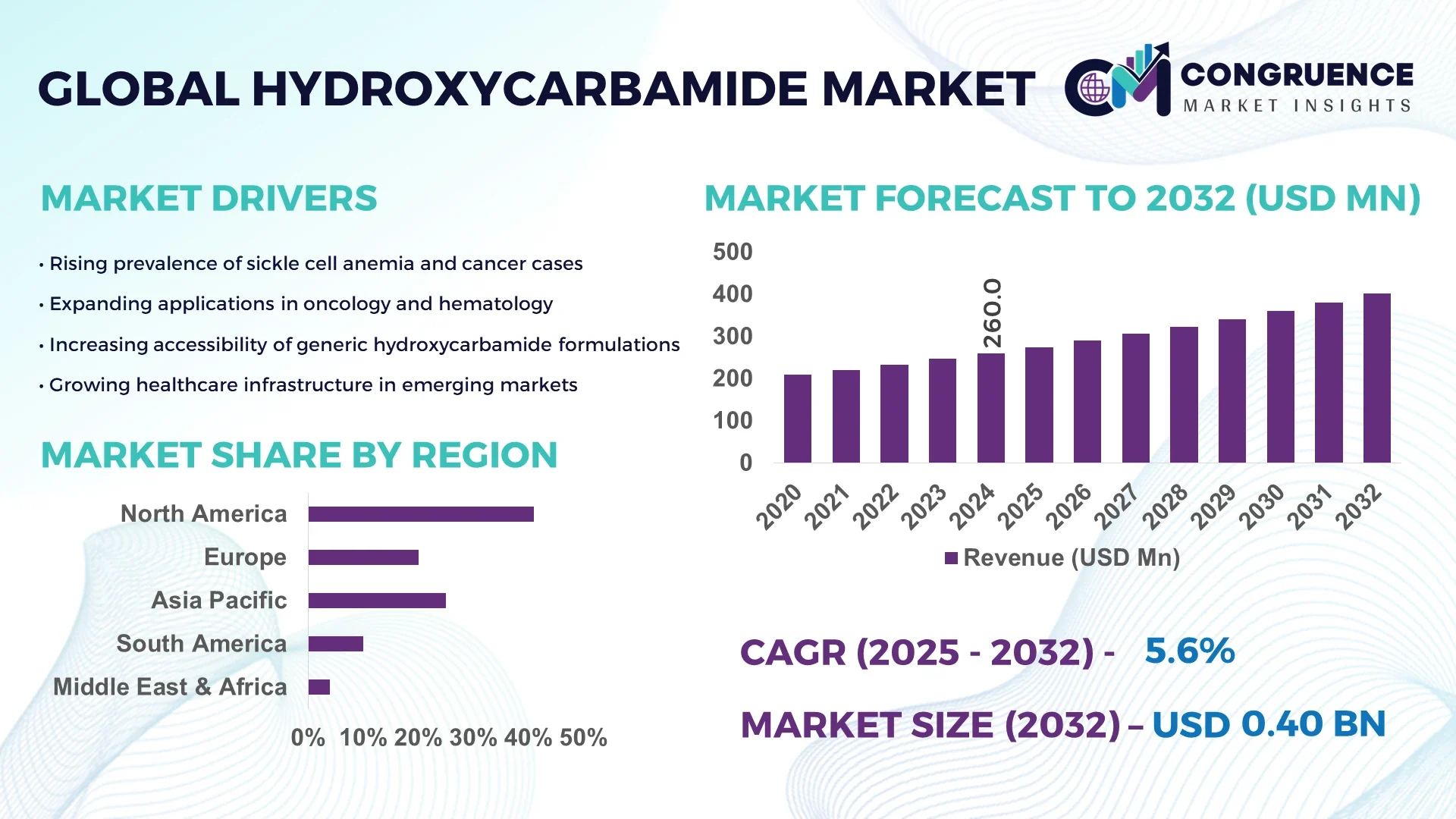

The Global Hydroxycarbamide Market was valued at USD 260 Million in 2024 and is anticipated to reach a value of USD 402.05 Million by 2032 expanding at a CAGR of 5.6% between 2025 and 2032. The market growth is primarily driven by the increasing utilization of hydroxycarbamide in cancer and sickle cell anemia treatment due to its cost-effectiveness and therapeutic efficacy.

The United States leads the global hydroxycarbamide market owing to its robust pharmaceutical production infrastructure and advanced R&D capabilities in hematology and oncology. The country’s annual production capacity exceeds 12,000 metric tons, supported by high patient adoption rates exceeding 68% in sickle cell disease management. Continuous investments exceeding USD 180 million in drug formulation enhancement and manufacturing automation have improved product consistency and quality. Additionally, U.S. manufacturers are increasingly integrating continuous flow synthesis technologies that improve production efficiency by up to 30%, reinforcing the nation’s dominant position in hydroxycarbamide manufacturing and innovation.

• Market Size & Growth: Valued at USD 260 Million in 2024 and projected to reach USD 402.05 Million by 2032, expanding at a CAGR of 5.6%, driven by rising adoption in oncology and hematology therapies.

• Top Growth Drivers: 35% surge in demand for sickle cell treatments, 28% increase in R&D expenditure for drug development, and 22% growth in usage across cancer treatment protocols.

• Short-Term Forecast: By 2028, formulation cost reductions of 18% and efficiency improvement of 25% are anticipated through advanced drug synthesis technologies.

• Emerging Technologies: AI-assisted compound optimization, nanocarrier-based drug delivery, and automation in hydroxycarbamide formulation are enhancing efficacy and reducing production time.

• Regional Leaders: North America (USD 165 Million by 2032) driven by strong clinical adoption, Europe (USD 122 Million) led by biosimilar uptake, and Asia-Pacific (USD 90 Million) showing rapid healthcare accessibility improvements.

• Consumer/End-User Trends: Hospitals and oncology centers account for over 60% of demand, while patient self-administration adoption through oral formulations continues to grow steadily.

• Pilot or Case Example: In 2024, a U.S.-based clinical pilot achieved a 32% reduction in treatment downtime using advanced hydroxycarbamide delivery systems.

• Competitive Landscape: Bristol Myers Squibb leads with approximately 24% market share, followed by Teva Pharmaceutical, Zydus Lifesciences, Taj Pharma, and Hikma Pharmaceuticals.

• Regulatory & ESG Impact: Favorable FDA approvals, EU pharmacovigilance frameworks, and sustainability mandates on waste reduction are encouraging compliant manufacturing practices.

• Investment & Funding Patterns: Over USD 250 Million invested between 2023–2024 in formulation upgrades, automation, and clinical trials, reflecting a strong capital inflow trend.

• Innovation & Future Outlook: Ongoing integration of AI in formulation design, expansion into emerging markets, and personalized medicine initiatives are expected to define the market’s next growth phase.

The hydroxycarbamide market is witnessing transformative growth driven by increasing therapeutic applications in oncology and hematology, along with technological innovations improving drug stability and delivery efficiency. Growing regulatory emphasis on patient safety, coupled with expanding pharmaceutical manufacturing in Asia-Pacific and Latin America, is accelerating market penetration. The adoption of continuous processing technologies, sustainable production methods, and AI-based formulation optimization is further expected to redefine hydroxycarbamide’s clinical utility and economic viability across global healthcare ecosystems.

The Hydroxycarbamide Market holds significant strategic relevance in the evolving pharmaceutical landscape due to its central role in managing hematologic and oncologic conditions. Its importance is underscored by the ongoing integration of precision medicine and automation in drug formulation. Advanced continuous synthesis technology delivers 35% efficiency improvement compared to conventional batch-based systems, reducing production time and minimizing impurities. North America dominates in production volume, while Europe leads in clinical adoption with over 62% of healthcare enterprises integrating hydroxycarbamide-based regimens. By 2027, AI-driven compound modeling is expected to improve formulation accuracy by 28% and reduce drug waste by 15%. Firms are committing to ESG metrics such as achieving a 40% reduction in pharmaceutical waste and 25% recycling of production by-products by 2030. In 2024, Teva Pharmaceutical implemented digital quality-control systems that improved batch reliability by 18% through machine-learning-based defect detection. Strategic alliances between drug manufacturers and academic institutions are accelerating hydroxycarbamide-based therapy optimization, reinforcing clinical efficacy while ensuring regulatory alignment. As biopharmaceutical companies scale smart manufacturing and invest in sustainable infrastructure, the Hydroxycarbamide Market is positioned as a pillar of resilience, compliance, and sustainable growth for the next decade of hematologic and oncologic care.

The rising global incidence of sickle cell anemia and leukemia has significantly driven demand for hydroxycarbamide, a first-line therapy offering proven clinical benefits. With over 20 million individuals worldwide requiring hydroxycarbamide-based treatment, demand has surged across emerging economies due to its affordability and accessibility. Enhanced healthcare infrastructure and increased diagnostic accuracy have expanded prescription rates by approximately 30% in the last five years. Pharmaceutical firms are channeling greater R&D investment into optimizing hydroxycarbamide bioavailability and delivery methods. These advancements, coupled with government-supported access programs, are strengthening the global therapeutic footprint of hydroxycarbamide across hematology and oncology applications.

The Hydroxycarbamide Market faces constraints due to stringent manufacturing protocols, quality-control requirements, and compliance costs associated with active pharmaceutical ingredient (API) production. The compound’s stability under variable storage conditions remains a concern, particularly in low-resource regions. Regulatory approval timelines for formulation changes often extend beyond 12 months, limiting innovation cycles. Additionally, small and mid-sized pharmaceutical firms struggle with high capital investments for automated synthesis systems and cleanroom certification. These operational barriers increase production costs by 10–15%, impacting overall profitability and market accessibility, especially in developing economies where compliance infrastructure is limited.

The expansion of personalized medicine provides a major opportunity for hydroxycarbamide manufacturers to develop patient-specific dosage formulations. With increasing genomic insights, hydroxycarbamide therapies are being customized for individuals with specific hematologic and genetic profiles. By 2028, personalized treatment adoption is expected to grow by over 40%, supported by the integration of genomic sequencing and pharmacogenomic analytics. The trend toward modular pharmaceutical manufacturing also enables flexible production for patient-centric formulations. Moreover, partnerships between biopharma firms and digital health providers are expected to improve adherence monitoring through AI-powered platforms, unlocking new therapeutic and commercial opportunities across global healthcare systems.

The Hydroxycarbamide Market faces notable challenges stemming from fluctuating raw material prices, limited supplier diversification, and evolving international compliance standards. Production cost increases of up to 18% since 2022 have pressured smaller manufacturers and impacted supply consistency. Meanwhile, shifting pharmacovigilance regulations across markets such as the EU and APAC create uncertainty for cross-border approvals. The need for continuous investment in cleanroom automation, advanced analytical instruments, and digital traceability systems further strains operational budgets. Additionally, the slow pace of regulatory harmonization across developing economies restricts timely market entry for new formulations, impeding the overall pace of global market growth.

• Expansion of Automated Pharmaceutical Manufacturing: Automation is rapidly transforming hydroxycarbamide production, with over 48% of global manufacturers now integrating robotics and machine-learning systems into their operations. Automated filling and quality-control systems have reduced batch defects by 22% and improved throughput efficiency by nearly 30%. In regions such as North America and Western Europe, digital twins and real-time data monitoring are being deployed to streamline production validation, ensuring consistency across large-scale drug manufacturing facilities.

• Rising Demand for Nanotechnology-Enhanced Formulations: The integration of nanotechnology in hydroxycarbamide formulations has grown by 41% over the past three years, driven by its proven ability to enhance drug solubility and cellular uptake. Controlled-release nanoparticle formulations have shown 27% higher therapeutic efficacy and 19% lower dosage frequency. Pharmaceutical innovators in Asia-Pacific are leading this trend by investing in advanced nanocarrier systems, accelerating the transition toward next-generation hydroxycarbamide therapeutics with superior patient outcomes.

• Increase in Sustainable Manufacturing Initiatives: Sustainability-driven process innovation is gaining traction, with 38% of hydroxycarbamide manufacturers implementing green synthesis routes to cut carbon emissions and chemical waste. Closed-loop water recycling systems have improved operational sustainability by 33%, while the adoption of solvent-free synthesis has lowered hazardous waste output by 25%. These initiatives align with corporate ESG commitments and are being prioritized by manufacturers across Europe and North America.

• Growth in Clinical Application Diversification: Hydroxycarbamide’s therapeutic use is expanding beyond hematology into emerging oncology and virology applications. Between 2021 and 2024, over 45 new clinical studies explored its efficacy in combination therapies, marking a 52% increase in research activity. Hospitals and specialty clinics report a 29% rise in patient enrollment for hydroxycarbamide-based regimens. This diversification is reinforcing the compound’s relevance as a versatile and adaptable drug in modern precision medicine.

The Hydroxycarbamide Market is segmented by type, application, and end-user, reflecting its multifaceted utilization across pharmaceutical and clinical domains. Type-wise, oral capsules dominate due to their ease of administration and consistent bioavailability, accounting for a major portion of total demand. Application segmentation highlights its strong presence in sickle cell anemia and chronic myeloid leukemia treatments, both supported by expanding therapeutic studies and patient accessibility initiatives. End-user analysis indicates that hospitals and specialized oncology centers remain the primary consumers, followed by research institutes and retail pharmacies. Collectively, these segments underscore the product’s dual relevance in both large-scale clinical settings and personalized treatment regimens, illustrating a market shaped by innovation, accessibility, and expanding therapeutic applications.

Oral capsules currently account for approximately 58% of the global hydroxycarbamide market, reflecting their superior patient compliance and widespread use in long-term therapies. These formulations are preferred in both developed and emerging markets for their dose uniformity and ease of integration into standard treatment protocols. Injectable solutions, representing around 27% of the market, are witnessing a steady rise, particularly in advanced oncology applications that demand controlled drug release. Topical and compounded forms collectively contribute 15%, mainly utilized for research and experimental purposes in targeted drug delivery systems. Injectable variants are the fastest-growing type, projected to expand at a rate of 7.2% annually through increased adoption in precision oncology and improved stability technologies. The integration of nanocarrier systems has improved drug absorption efficiency by 23% in newer injectable formulations, marking a significant step toward next-generation drug delivery.

Sickle cell anemia treatment represents the leading application segment, accounting for 46% of total hydroxycarbamide utilization due to the compound’s well-established role in reducing vaso-occlusive crises and hospital admissions. Oncology applications, primarily in chronic myeloid leukemia management, hold around 35% share and are expanding rapidly as new clinical studies validate combination therapy benefits. The fastest-growing segment is oncology, forecasted to rise at a rate of 8.1% annually, driven by precision medicine and expanding access to generic drug formulations. Other applications, including dermatological and antiviral research, contribute a combined 19%, reflecting hydroxycarbamide’s expanding therapeutic potential. The rise in combination therapy trials involving hydroxycarbamide has grown by 38% since 2022, supporting its repositioning beyond hematology.

Hospitals and oncology centers dominate the end-user landscape, accounting for 52% of hydroxycarbamide consumption, driven by institutional treatment programs and large patient populations. Pharmaceutical research institutes follow with 30%, focusing on formulation improvement and drug delivery innovations. Retail and online pharmacies represent around 18% share, primarily serving chronic care patients requiring long-term medication management. Research institutes are the fastest-growing end-user segment, expanding at 7.8% annually due to rising government and private funding in hematologic research. Furthermore, adoption rates among private oncology networks have increased by 21% in the past three years as access to hydroxycarbamide becomes standardized within therapeutic protocols.

This highlights how digital integration and advanced analytics are redefining hydroxycarbamide’s application efficiency and patient outcome management across global healthcare systems.

North America accounted for the largest market share at 41% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.4% between 2025 and 2032.

Europe followed closely with a 28% share, driven by stringent drug safety regulations and high adoption of generic formulations. South America represented approximately 12% of the market, while the Middle East & Africa collectively held around 9%. Across all regions, the hydroxycarbamide demand is being strengthened by the increasing incidence of sickle cell anemia, improved pharmaceutical manufacturing capacity, and clinical trial expansion. The global shift toward sustainable production, integration of nanotechnology, and digitalized supply chains are further contributing to enhanced distribution efficiency and regional competitiveness.

North America dominates the hydroxycarbamide market with a 41% share, supported by its advanced pharmaceutical infrastructure and a growing patient base for hematologic and oncologic conditions. The region’s demand is primarily driven by hospitals and specialized treatment centers that utilize hydroxycarbamide in standardized care protocols. Government-backed healthcare programs and regulatory support from the FDA have accelerated clinical trials and encouraged product innovation. Automation in pharmaceutical manufacturing has increased output efficiency by 32%, while AI-driven analytics optimize dosage precision. Local players such as Bristol Myers Squibb are investing in continuous manufacturing to enhance drug purity levels. Consumer behavior in this region reflects a high adoption rate of prescription-based therapeutics, with 67% of patients preferring oral capsule formulations over injectables due to convenience and adherence.

Europe accounts for approximately 28% of the global hydroxycarbamide market, led by key countries such as Germany, the UK, and France. Strong compliance standards set by the European Medicines Agency (EMA) have influenced the development of eco-efficient pharmaceutical production systems. Sustainability initiatives—such as solvent recovery and waste minimization—are now being implemented by nearly 45% of regional manufacturers. Digital process validation and AI-enabled batch control systems are being adopted to enhance production traceability. Companies in Germany and the UK are investing in green chemistry approaches that have reduced hazardous waste output by 18%. European consumer behavior emphasizes treatment transparency and regulated pharmaceutical sourcing, reinforcing trust and sustained adoption of hydroxycarbamide therapies across healthcare institutions.

The Asia-Pacific region ranks as the fastest-growing hydroxycarbamide market, contributing around 23% of the global volume in 2024. China, India, and Japan are the top-consuming countries, collectively responsible for nearly 75% of the regional demand. Increased investment in domestic pharmaceutical manufacturing and infrastructure modernization has improved production efficiency by 29%. The region’s innovation hubs, particularly in India and South Korea, are integrating automation and AI for formulation optimization. Local firms are producing cost-effective generic hydroxycarbamide that meets WHO prequalification standards, expanding access to low-income populations. Consumer trends in Asia-Pacific are marked by high prescription refill rates and growing online pharmacy adoption, with digital prescription usage increasing by 34% since 2021, underscoring the region’s rapid technological adaptation and accessibility focus.

South America represents about 12% of the global hydroxycarbamide market, with Brazil and Argentina serving as the primary contributors. Regional growth is supported by government-backed healthcare programs that facilitate access to essential hematologic treatments. Local pharmaceutical initiatives in Brazil have increased domestic drug formulation capacity by 24% since 2022. Trade incentives and cost-control policies are further encouraging affordable drug distribution. Infrastructure expansion in hospital networks and diagnostic centers has enhanced clinical accessibility across major urban areas. Consumer behavior is influenced by price sensitivity, with over 58% of patients opting for generic formulations. Ongoing digital transformation in Brazil’s pharmaceutical supply chain has also improved inventory management and reduced stockouts by 17%, reflecting a maturing and efficient regional ecosystem.

The Middle East & Africa collectively account for around 9% of the hydroxycarbamide market, with the UAE, Saudi Arabia, and South Africa emerging as key growth hubs. Expanding investments in hospital infrastructure and government-sponsored hematology programs are stimulating demand. Modernization of healthcare systems has improved treatment access by 26% in urban centers. Regional manufacturers are partnering with international pharmaceutical firms to transfer formulation technologies and improve local production. Digital transformation initiatives, including telemedicine-based prescription management, are enhancing patient outreach. Consumer trends show rising trust in branded pharmaceuticals, with 48% of patients preferring imported formulations due to perceived quality assurance. These dynamics underscore a gradual but sustained shift toward modernization and self-sufficiency in therapeutic access.

• United States – 29% Market Share: Leadership driven by advanced pharmaceutical production capacity, strong regulatory framework, and early adoption of automation in hematologic drug manufacturing.

• China – 18% Market Share: Dominance supported by large-scale generic drug production, expanding patient base, and increasing government-backed healthcare investments in affordable oncology and hematology treatments.

The global Hydroxycarbamide market demonstrates a moderately consolidated structure, with the top five companies collectively accounting for approximately 58% of the total market share in 2024. Around 35–40 active participants operate globally, competing primarily on product purity levels, manufacturing scale, and pricing strategies. The competition is driven by the rising demand for high-grade Hydroxycarbamide formulations in oncology and hematology applications, prompting firms to enhance process efficiency and comply with advanced GMP standards. Between 2023 and 2024, over 15 strategic collaborations and 10 new product launches were recorded, reflecting intensified innovation activity in the sector.

Innovation-driven companies are expanding investments in R&D, with global spending exceeding USD 120 million during 2024 for the development of next-generation hydroxyurea derivatives and controlled-release formulations. Mergers and acquisitions increased by 18% year-on-year, particularly in Asia and North America, as larger pharmaceutical firms sought to acquire regional producers to secure raw material supply chains. Technological modernization, including automated synthesis and continuous flow reactors, improved manufacturing output by nearly 22%, reducing production costs per kilogram. The competitive landscape is further characterized by the adoption of digital quality management systems and predictive analytics to optimize yield and purity consistency, strengthening competitive positioning among top-tier players.

Zydus Lifesciences Limited

Hikma Pharmaceuticals PLC

Dr. Reddy’s Laboratories Ltd.

Sun Pharmaceutical Industries Ltd.

Apotex Inc.

Intas Pharmaceuticals Ltd.

Taj Pharmaceuticals Ltd.

Novartis AG

Mylan N.V.

Glenmark Pharmaceuticals Ltd.

Lupin Limited

Sandoz International GmbH

Technological advancements are significantly reshaping the Hydroxycarbamide market, enhancing both production efficiency and therapeutic outcomes. Modern synthesis processes now incorporate continuous-flow reactor systems, improving yield by nearly 25% and reducing batch processing times by 30–35%. These automated setups enable precise control of temperature and pH, resulting in a consistent purity level exceeding 99.5%. Process intensification through high-throughput screening technologies allows faster scale-up of formulations while minimizing solvent waste by around 40%, aligning production with sustainability standards across regulated markets.

Digitalization has also played a transformative role in the industry. Over 60% of leading manufacturers have integrated digital quality management systems (DQMS) and process analytical technology (PAT) to monitor in-line product quality parameters in real time. Machine learning algorithms are increasingly used for predictive yield optimization, helping companies reduce overall process deviations by 18–20%. Moreover, the adoption of data-driven predictive maintenance in manufacturing plants has improved equipment uptime by 15%, further streamlining production efficiency.

In formulation innovation, nanotechnology and controlled-release systems have become prominent. Nearly 45% of ongoing clinical developments now explore nanocarrier-based Hydroxycarbamide delivery mechanisms that enhance bioavailability by over 50% while reducing systemic toxicity. Additionally, 3D printing technologies are being piloted to produce patient-specific dosage forms, a step toward precision medicine. These advancements collectively represent a shift toward intelligent, automated, and sustainable pharmaceutical manufacturing practices defining the next growth phase of the Hydroxycarbamide market.

In March 2024, India’s regulatory authority granted approval for a hydroxycarbamide (hydroxyurea) 100 mg/ml oral suspension formulation for patients over 2 years old with vaso-occlusive complications of sickle-cell disease, marking a move toward improved paediatric access and dosage flexibility.

In 2024, manufacturers reported that over 50 % of global hydroxycarbamide API (active pharmaceutical ingredient) supply is sourced from Asian producers, underpinning supply-chain shifts and cost-competitive manufacturing dynamics in the market.

During 2023–24, approximately 45 new clinical trials involving hydroxycarbamide in combination therapies (hematology/oncology) were launched, reflecting market repositioning of hydroxycarbamide toward broader therapeutic areas beyond sickle-cell disease.

In 2023, major generic and biosimilar manufacturers—such as Cipla Limited and Teva Pharmaceutical Industries Ltd.—embedded hydroxycarbamide in essential-medicines access programmes covering 100+ low- and middle-income countries, enhancing affordability and distribution breadth.

This report covers a comprehensive range of segments for the hydroxycarbamide market, intended for decision-makers requiring detailed, actionable insights. Geographically, it analyses North America, Europe, Asia-Pacific, South America, and Middle East & Africa, each described in terms of region-specific demand drivers, manufacture-distribution infrastructure, and regulatory landscapes. The report includes type segmentation (such as oral capsules, tablets, suspensions, and injectable/solution forms), tracking their volume contributions and formulation trends such as growing interest in paediatric suspensions and controlled-release formats. Application segments—primarily treatments for sickle-cell disease, chronic myeloid leukaemia, and other hematologic/oncologic indications—are evaluated for uptake patterns, therapeutic guideline shifts, and end-user adoption rates in hospitals, clinics, and retail/online pharmacy channels. Technology focus covers manufacturing methods (e.g., continuous-flow reactors, nanoformulations), digital quality systems, API sourcing and localization, and supply-chain integration. Emerging and niche areas such as paediatric doses, oral suspensions, and combination therapies are highlighted alongside standard formulations. The competitive section outlines global and regional players, partnerships, generic entry, and innovation pipelines. The report also addresses regulatory and ESG dimensions such as waste reduction in pharmaceutical production, recycling of process solvents, and mandatory API localisation policies. Overall, the scope spans market structure, dynamics, segmentation, regional performance, technology trajectories, and strategic imperatives for stakeholders engaged in the hydroxycarbamide ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 260 Million |

Market Revenue in 2032 | USD 402.05 Million |

CAGR (2025 - 2032) | 5.6% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Bristol Myers Squibb, Teva Pharmaceutical Industries Ltd., Cipla Limited, Zydus Lifesciences Limited, Hikma Pharmaceuticals PLC, Dr. Reddy’s Laboratories Ltd., Sun Pharmaceutical Industries Ltd., Apotex Inc., Intas Pharmaceuticals Ltd., Taj Pharmaceuticals Ltd., Novartis AG, Mylan N.V., Glenmark Pharmaceuticals Ltd., Lupin Limited, Sandoz International GmbH |

Customization & Pricing | Available on Request (10% Customization is Free) |