Reports

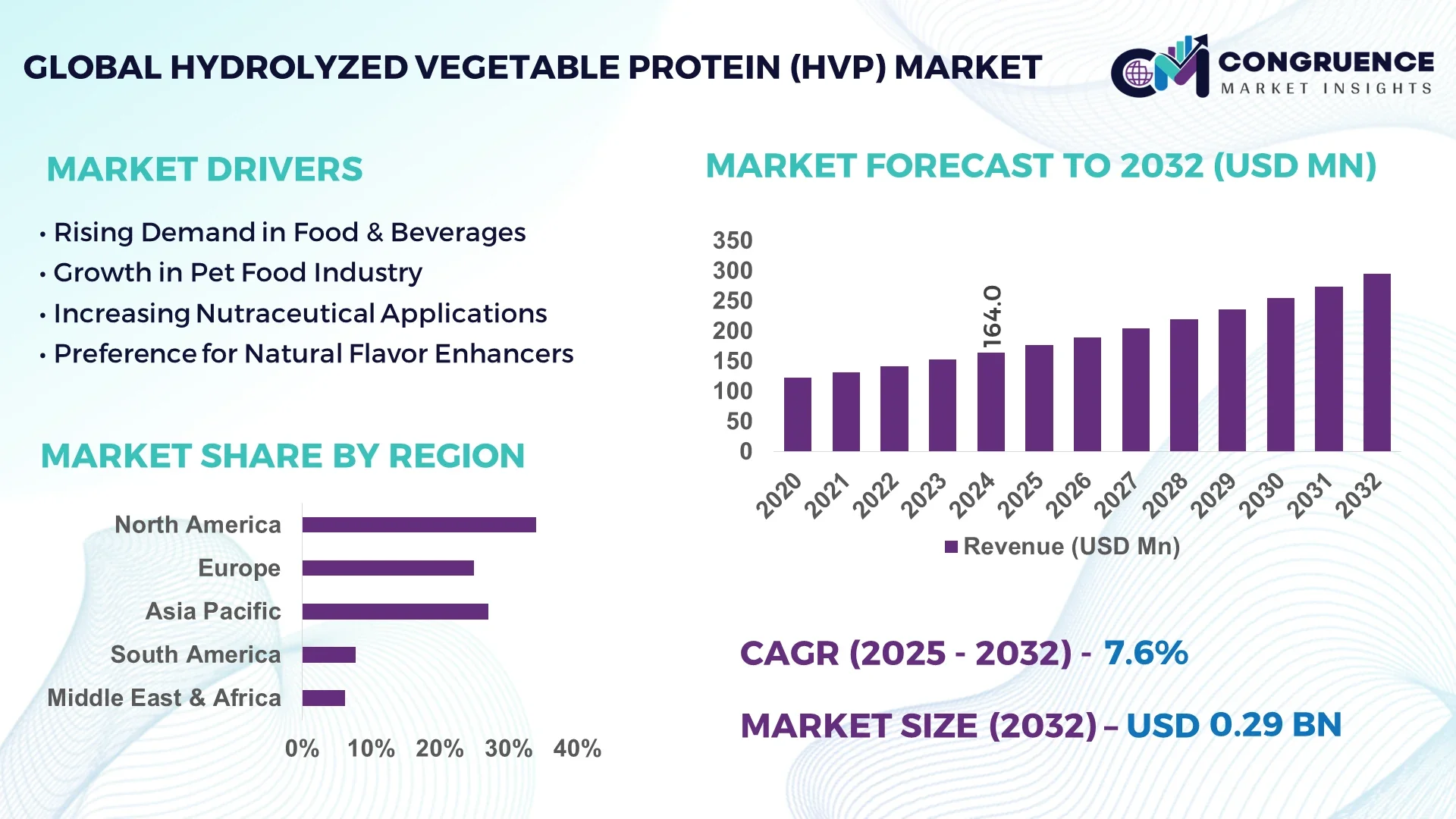

The Global Hydrolyzed Vegetable Protein (HVP) Market was valued at USD 164.0 Million in 2024 and is anticipated to reach a value of USD 294.7 Million by 2032 expanding at a CAGR of 7.6% between 2025 and 2032.

In the United States—the country that dominates the Hydrolyzed Vegetable Protein (HVP) Market—industry players operate some of the largest production facilities worldwide, with several plants boasting annual capacities upward of 15,000 metric tons. Significant investments have been directed toward upgrading enzymatic hydrolysis lines and integrating high-throughput mixers to meet industrial demand for savory enhancers in snack foods, sauces, soups, and pet nutrition. Technological advances include continuous tubular reactors and real-time viscosity controls that improve batch uniformity.

The Hydrolyzed Vegetable Protein (HVP) Market spans multiple industry sectors—chief among them are food & beverage (including savory seasonings, soups, snacks), pet food, and nutritional supplements—with food & beverage constituting the largest segment by volume. Recently, technological and product innovations have included enzyme-specific formulations reducing processing times by up to 20%, extended-shelf-life liquid HVP products, and ultra-filtration techniques to remove off-flavors while enhancing umami potency. Regulatory drivers such as stricter labeling and clean-label trends have prompted manufacturers to shift toward non-chemical acid hydrolysis and invest in enzyme-based production. Environmental factors—including efforts to reduce effluent acidity—are encouraging adoption of closed-loop water reuse systems. Regionally, Asia Pacific continues to exhibit strong consumption growth due to increasing packaged food demand and convenience eating, while North America leads in industrial processing innovation and higher-protein applications. Emerging trends include co-developed HVP blends tailored for low-sodium formulations, spray-dried powdered concentrates, and collaborations between ingredient firms and foodservice outlets for customized flavor systems. Together, these shifts point to a future outlook centered on cleaner processing, customized solutions, and multifunctional ingredients to meet evolving consumer and industrial requirements.

Artificial intelligence (AI) is significantly reshaping the Hydrolyzed Vegetable Protein (HVP) Market by enhancing process control and operational performance. Decision-makers in the Hydrolyzed Vegetable Protein (HVP) Market are leveraging AI-powered predictive maintenance systems to monitor enzyme reactor health, reducing unscheduled downtime by approximately 30%. AI-driven process optimization tools adjust hydrolysis parameters in real time—such as temperature, pH, and mixing speed—resulting in consistent product quality and a 15% improvement in batch yield. Smart sensor arrays and machine-learning models detect deviations in viscosity and nitrogen levels early, allowing production teams to intervene swiftly, thus maintaining high standards in savory and peptide content for downstream applications. Supply chain management within the Hydrolyzed Vegetable Protein (HVP) Market is also being streamlined through AI-based forecasting platforms that better align raw material purchases, reducing inventory holding periods by up to 10%. Furthermore, AI-driven quality assurance systems use hyperspectral imaging to detect particulate impurities or color inconsistencies in HVP, accelerating inspection throughput by 40%, enabling faster release to food processors. These AI applications benefit decision-makers by reducing production risk, improving throughput, and enabling more reliable delivery of high-purity HVP necessary for premium food formulations.

“In 2024, an AI-guided enzymatic hydrolysis control system implemented in a North American HVP facility monitored pH and temperature every 30 seconds, reducing batch variation by 12% and increasing enzyme utilization efficiency by 8%.”

The Hydrolyzed Vegetable Protein (HVP) Market Dynamics reflect a confluence of shifting consumer preferences, industrial processing advancements, and evolving regulatory landscapes. Companies are responding to demand for cleaner, label-friendly ingredients by adopting enzymatic hydrolysis technologies. Simultaneously, investments in automation and smart data analytics are enabling tighter control of process parameters and faster time-to-market. Raw material supply volatility—particularly fluctuations in soybean meal and corn protein prices—continues to influence cost optimization strategies. Decision-makers are increasingly pursuing strategic partnerships with enzyme providers to co-develop tailored HVP variants with specific flavor profiles. Sustainability expectations, including water recycling and lower chemical inputs, are shaping facility upgrades and operational planning. More broadly, the interplay of innovation, supply considerations, and regulatory compliance is driving a dynamic environment where agile adaptation is critical for success.

Growing demand for clean-label ingredients is driving the Hydrolyzed Vegetable Protein (HVP) Market, as food manufacturers seek alternatives to chemically hydrolyzed counterparts. Enzyme-based hydrolysis systems have responded by enabling production of HVP with fewer additives and reduced processing footprints. For example, several manufacturers have reported that switching to enzymatic systems cut chemical usage—including hydrochloric acid—by over 40%, and reduced wastewater acidity by 25%. These operational improvements have boosted production flexibility while aligning with consumer preferences and regulatory trends favoring minimally processed label claims.

The Hydrolyzed Vegetable Protein (HVP) Market faces constraints due to inherent volatility in the prices of base materials such as soy or corn proteins. For instance, a 15% spike in soybean meal prices in early 2025 led several HVP producers to delay capacity expansion plans or renegotiate supply contracts. This pricing unpredictability strains margin management and complicates long-term procurement strategies. Operators must frequently adjust procurement schedules, hedge against commodity swings, or secure long-term supplier agreements to stabilize input costs—yet these tactics may limit flexibility and hinder rapid response to evolving consumer demand.

One emerging opportunity in the Hydrolyzed Vegetable Protein (HVP) Market lies in developing specialty plant-protein blends that deliver enhanced flavor while supporting formulation for plant-based meat analogues and high-protein snacks. Recent pilot projects combining HVP with pea and rice proteins have demonstrated 20% improvement in flavor intensity and texture when used in meat substitute applications. Ingredient firms that can co-develop these blends with food manufacturers stand to capture new application-driven demand, particularly as the plant-based sector expands and seeks savory, protein-rich ingredients that enhance mouthfeel and umami complexity in value-added foods.

Producers in the Hydrolyzed Vegetable Protein (HVP) Market are grappling with rising compliance costs associated with stricter food safety, labeling, and environmental regulations. For example, implementing additional wastewater treatment systems to meet new effluent standards increased operational costs by an estimated 10% at several HVP plants. Frequent updates to food labeling rules—requiring detailed disclosure of allergens and processing aids—have prompted retraining of quality and regulatory teams, and necessitated label redesigns and reformulation efforts. These added complexities increase overhead and slow new product introductions, requiring companies to allocate more resources to compliance rather than innovation.

Automated Enzymatic Reactor Deployments Accelerate: Leading HVP production sites in Europe and North America have reported a 25% reduction in cycle times thanks to fully automated enzymatic reactors. These systems integrate precise dosing, real-time monitoring, and feedback loops, resulting in quicker batch turnovers and lower labor intensity in high-volume operations.

Spray-Dried Liquid HVP Concentrate Innovations Expand: Spray-dried HVP concentrates, developed for industrial convenience, now account for 40% of new product launches, offering extended shelf-life and simplified transport. Users benefit from a 30% decrease in handling time compared to liquid HVP drums.

Regional Custom Flavor Systems Gain Traction: Ingredient suppliers in Asia Pacific and Latin America increasingly offer region-specific HVP flavor systems tailored to local taste profiles. Adoption rates have grown substantially, with pilot programs in Southeast Asia showing a 35% higher acceptance in localized snack products.

Closed-Loop Water Reuse Implementation: Environmental initiatives are prompting HVP manufacturers to install closed-loop water recycling systems. In recent projects, plants reduced freshwater withdrawals by 50% and cut wastewater discharge volumes by 45%, enhancing sustainability with minimal impact on production outputs.

The Hydrolyzed Vegetable Protein (HVP) Market is segmented by type, application, and end-user industries, each contributing uniquely to overall growth and market positioning. Segmentation analysis reveals that specific product types dominate due to their flavor intensity and compatibility with diverse formulations, while others occupy niche roles catering to specialized industries. Applications extend widely across food and beverage, pet nutrition, dietary supplements, and emerging industrial uses, each reflecting evolving consumer preferences and industry innovation. End-users such as large-scale food manufacturers, specialty ingredient providers, and nutraceutical companies form the backbone of market demand, with each group influencing production priorities and technological advancements. Understanding these segments allows stakeholders to identify where opportunities are concentrated and where evolving consumption patterns are likely to reshape future strategies.

The Hydrolyzed Vegetable Protein (HVP) Market by type encompasses acid-hydrolyzed, enzyme-hydrolyzed, and mixed-method products. Among these, acid-hydrolyzed protein currently leads the segment due to its long-established industrial usage, high efficiency in flavor release, and scalability in mass production. Its stability and consistent performance across soups, sauces, and snack seasonings secure its leadership position. Enzyme-hydrolyzed protein, however, represents the fastest-growing type, driven by clean-label demands, lower chemical dependency, and improved nutritional profiles. Recent advancements in enzymatic hydrolysis technology have improved production yields, reduced off-flavors, and supported broader adoption in premium food formulations and dietary supplements. Mixed-method products, which combine both acid and enzymatic processes, serve niche requirements where manufacturers seek to balance cost efficiency with enhanced taste attributes. Although smaller in scale, these products play an important role in bridging traditional processing with newer, more sustainable methods. Together, these categories demonstrate how technological evolution and consumer-driven trends are reshaping the type-based outlook of the market.

Applications of Hydrolyzed Vegetable Protein (HVP) span food and beverages, pet food, nutritional supplements, and industrial uses. Food and beverages remain the leading application, as HVP is widely incorporated into soups, instant noodles, sauces, and snacks to enhance savory flavor profiles. Its long-standing role in flavor enhancement ensures continued high-volume demand. Pet food represents the fastest-growing application, fueled by rising consumer focus on animal nutrition, protein enrichment, and palatability improvements. Pet food formulations increasingly integrate HVP for its digestibility and ability to enhance taste acceptance among animals. Nutritional supplements also contribute meaningfully, particularly in protein powders and sports nutrition products where flavor masking and digestibility improvements are critical. Industrial applications, such as flavor intermediates and specialty fermentation feedstocks, remain relatively small but showcase niche potential. Each application area demonstrates distinct demand drivers, with food and beverages providing stability and scale, while emerging applications in pet food and supplements highlight new areas of dynamic expansion.

End-users in the Hydrolyzed Vegetable Protein (HVP) Market include food and beverage manufacturers, pet food producers, nutraceutical companies, and specialty ingredient suppliers. Food and beverage manufacturers dominate as the primary end-user group, accounting for the largest share due to their extensive use of HVP in processed and convenience foods. Their investments in R&D and continuous product innovation reinforce their leading role. Pet food producers are the fastest-growing end-user segment, benefiting from consumer willingness to spend more on premium formulations that incorporate high-quality protein sources like HVP. Nutraceutical companies also play a significant role, particularly in functional food and supplement sectors, where HVP supports flavor masking and improved digestibility in protein-rich formulations. Specialty ingredient suppliers contribute strategically by developing tailored HVP blends for regional cuisines and emerging product lines. Collectively, these end-user segments illustrate a diversified demand base where large-scale manufacturers ensure market stability, and specialized industries drive innovation and new growth opportunities.

North America accounted for the largest market share at 34% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.1% between 2025 and 2032.

The Hydrolyzed Vegetable Protein (HVP) Market demonstrates varied regional strengths, with established economies leveraging advanced processing technologies while emerging markets focus on rising consumption and evolving dietary preferences. Growth dynamics are influenced by food industry expansion, regulatory standards, and technological modernization across regions. While North America leads in terms of share due to its robust industrial base and demand for savory flavorings, Asia-Pacific is anticipated to drive the next wave of expansion, supported by rising packaged food demand and investments in advanced manufacturing infrastructure.

North America held approximately 34% of the Hydrolyzed Vegetable Protein (HVP) Market share in 2024, making it the leading regional market. The United States and Canada drive demand through strong food processing industries, including snack manufacturing, ready-to-eat meals, and pet food. Regulatory frameworks such as stricter food safety labeling requirements are reshaping product formulations to ensure compliance with clean-label trends. Technological advancements in enzymatic hydrolysis and AI-based process optimization are enabling manufacturers to achieve consistent flavor quality while reducing operational costs. Digitalization within production plants, particularly predictive maintenance and sensor integration, is further improving efficiency. North America’s market strength lies in its established processing ecosystem, combined with continuous investment in technology upgrades and sustainability initiatives.

Europe accounted for around 28% of the Hydrolyzed Vegetable Protein (HVP) Market share in 2024, supported by high demand in Germany, the UK, and France. The region’s stringent regulatory landscape, guided by the European Food Safety Authority (EFSA), continues to influence production practices and encourage sustainable sourcing of raw materials. Key industries driving demand include processed food, bakery, and plant-based alternatives. Sustainability initiatives such as carbon reduction commitments have accelerated the adoption of energy-efficient enzymatic hydrolysis technologies. European manufacturers are also investing in clean-label product portfolios, meeting growing consumer expectations for natural and minimally processed ingredients. Technology adoption, particularly automation and data-driven quality control, is enabling more precise production while enhancing product safety. Europe’s focus on sustainability and consumer trust underpins its strong position in the global HVP market.

Asia-Pacific ranked as the second-largest region by volume in 2024, holding nearly 24% of the Hydrolyzed Vegetable Protein (HVP) Market and projected to rise significantly through 2032. China, India, and Japan are the top consuming countries, supported by increasing urbanization and demand for packaged foods. Infrastructure improvements in food processing and advanced manufacturing hubs across China and Southeast Asia are expanding production capacities. India’s growing middle-class population is fueling the shift toward savory snacks and convenience meals incorporating HVP. Technological innovation hubs in Japan and South Korea are pioneering advanced enzymatic methods, improving flavor concentration and reducing processing cycles. The region’s rapid adoption of automation in food manufacturing, combined with favorable economic growth, positions Asia-Pacific as the fastest-growing market for HVP globally.

South America represented close to 8% of the Hydrolyzed Vegetable Protein (HVP) Market share in 2024, with Brazil and Argentina leading the region’s demand. Brazil’s strong agricultural base supports cost-effective sourcing of soy and corn proteins used in HVP production, while Argentina contributes with robust food export industries. Growth is driven by increased demand in local food and beverage industries, particularly in processed snacks and flavoring for sauces. Infrastructure development in food processing plants is enhancing efficiency and export capacity. Governments in the region have introduced incentives for industrial modernization and trade policies to support regional competitiveness in the global ingredient supply chain. South America is positioning itself as a competitive player, supported by raw material availability and growing demand from both domestic and export-oriented industries.

The Middle East & Africa accounted for around 6% of the Hydrolyzed Vegetable Protein (HVP) Market share in 2024, with the United Arab Emirates, Saudi Arabia, and South Africa emerging as leading growth contributors. Rising demand from the foodservice and packaged food sectors is a key driver, as regional diets increasingly incorporate processed and convenience food products. Government-led food security programs are fostering investments in local food processing facilities to reduce import dependence. Technological modernization, including automation and digital monitoring systems in new plants, is improving product quality and output efficiency. Trade partnerships with global food ingredient suppliers are further enabling market integration. Local regulations are focusing on ensuring safety standards while encouraging foreign direct investment in food processing infrastructure. This combination of food security priorities and modernization trends underpins steady regional progress in the HVP market.

United States – 22% Market Share

Dominance supported by extensive production capacity, advanced food processing infrastructure, and widespread use of HVP in packaged food and pet nutrition industries.

China – 18% Market Share

Leadership driven by high domestic consumption of savory and packaged foods, combined with large-scale investments in food manufacturing and processing capabilities.

The Hydrolyzed Vegetable Protein (HVP) Market is characterized by a moderately fragmented competitive landscape, with over 40 active global and regional competitors vying for market share. The competitive environment is defined by product differentiation strategies, expansion into high-growth regions, and a rising focus on clean-label and sustainable production practices. Leading players have strategically positioned themselves by expanding production capacities, diversifying raw material sources such as soy, wheat, and corn, and engaging in partnerships with food manufacturers to strengthen distribution networks. Innovation trends, such as enzymatic hydrolysis methods for improved flavor profiles and allergen-free solutions, are driving product development and intensifying competition. Mergers and acquisitions have also reshaped the market, as companies consolidate to strengthen their R&D and broaden product portfolios. Furthermore, advancements in flavor masking technologies, coupled with digital platforms for supply chain transparency, are being leveraged by major players to secure a competitive edge. This competitive intensity is expected to accelerate, with firms increasingly focusing on sustainable production methods and compliance with stringent global food safety standards.

Kerry Group plc

Tate & Lyle plc

Ajinomoto Co., Inc.

Griffith Foods Inc.

Givaudan SA

Koninklijke DSM N.V.

Cargill, Incorporated

Sensient Technologies Corporation

Symrise AG

AngelYeast Co., Ltd.

Technological innovation is a defining factor in the Hydrolyzed Vegetable Protein (HVP) Market, enabling manufacturers to deliver high-quality, sustainable, and cost-efficient products. The transition from traditional acid hydrolysis to enzymatic hydrolysis has significantly improved the nutritional and sensory profile of HVP, producing cleaner flavors with fewer by-products. Enzymatic processes also allow for allergen reduction, making products safer for sensitive populations.

Automation and digital transformation are streamlining production processes, reducing downtime, and improving consistency in product quality. Artificial intelligence (AI) and machine learning are increasingly applied for flavor optimization, predictive maintenance, and supply chain management. Furthermore, extrusion technologies and bioprocessing methods are being developed to enhance yield efficiency while maintaining flavor integrity.

Sustainability-driven technologies, such as the integration of renewable energy in manufacturing and the use of plant-based raw material blends, are gaining prominence. Novel encapsulation techniques are also being used to stabilize HVP in various applications, extending its shelf life and maintaining flavor intensity. The adoption of blockchain for traceability ensures product authenticity and compliance with global food safety regulations. Collectively, these technological advancements are reshaping the HVP market, offering companies new pathways for innovation and differentiation in a highly competitive industry.

• In March 2023, Ajinomoto Co., Inc. expanded its flavor solutions portfolio by launching a new line of enzymatically hydrolyzed vegetable protein products, designed to deliver enhanced umami taste while reducing sodium content in packaged foods.

• In July 2023, Kerry Group plc invested in a state-of-the-art facility in the United States dedicated to sustainable HVP production, integrating renewable energy sources to reduce operational carbon emissions by 30%.

• In February 2024, Symrise AG introduced a next-generation HVP flavor enhancer targeted at plant-based meat alternatives, offering improved heat stability and a cleaner label profile for global food producers.

• In May 2024, Cargill, Incorporated announced a strategic partnership with a major Asian food manufacturer to expand HVP distribution across China and India, supporting the region’s growing demand for processed food and instant meals.

The scope of the Hydrolyzed Vegetable Protein (HVP) Market Report encompasses an in-depth analysis of the global market across diverse segments, regions, and applications. It covers key product types such as acid-hydrolyzed, enzymatic-hydrolyzed, and other niche variants derived from different raw materials, including soy, wheat, and maize. The report examines applications across food and beverage industries, with particular emphasis on savory snacks, soups, sauces, seasonings, and plant-based meat alternatives. It also extends to end-use industries such as foodservice, packaged food, and industrial-scale production.

Geographically, the report spans major regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting unique regional demand patterns, infrastructure development, and evolving consumer preferences. The scope also considers emerging markets and the role of local producers in shaping regional competitiveness.

Technological insights are an integral part of the report, addressing innovations in enzymatic hydrolysis, sustainable production, digital manufacturing, and flavor encapsulation. The analysis also evaluates how regulatory frameworks and sustainability initiatives are shaping industry strategies and investment patterns. By providing comprehensive coverage of market dynamics, competitive landscape, technological advancements, and emerging opportunities, this report delivers actionable intelligence for decision-makers, investors, and stakeholders seeking to navigate the evolving Hydrolyzed Vegetable Protein (HVP) Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 164.0 Million |

| Market Revenue (2032) | USD 294.7 Million |

| CAGR (2025–2032) | 7.6% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Kerry Group plc, Tate & Lyle plc, Ajinomoto Co., Inc., Griffith Foods Inc., Givaudan SA, Koninklijke DSM N.V., Cargill,Incorporated, Sensient Technologies Corporation, Symrise AG, AngelYeast Co., Ltd. |

| Customization & Pricing | Available on Request (10% Customization is Free) |