Reports

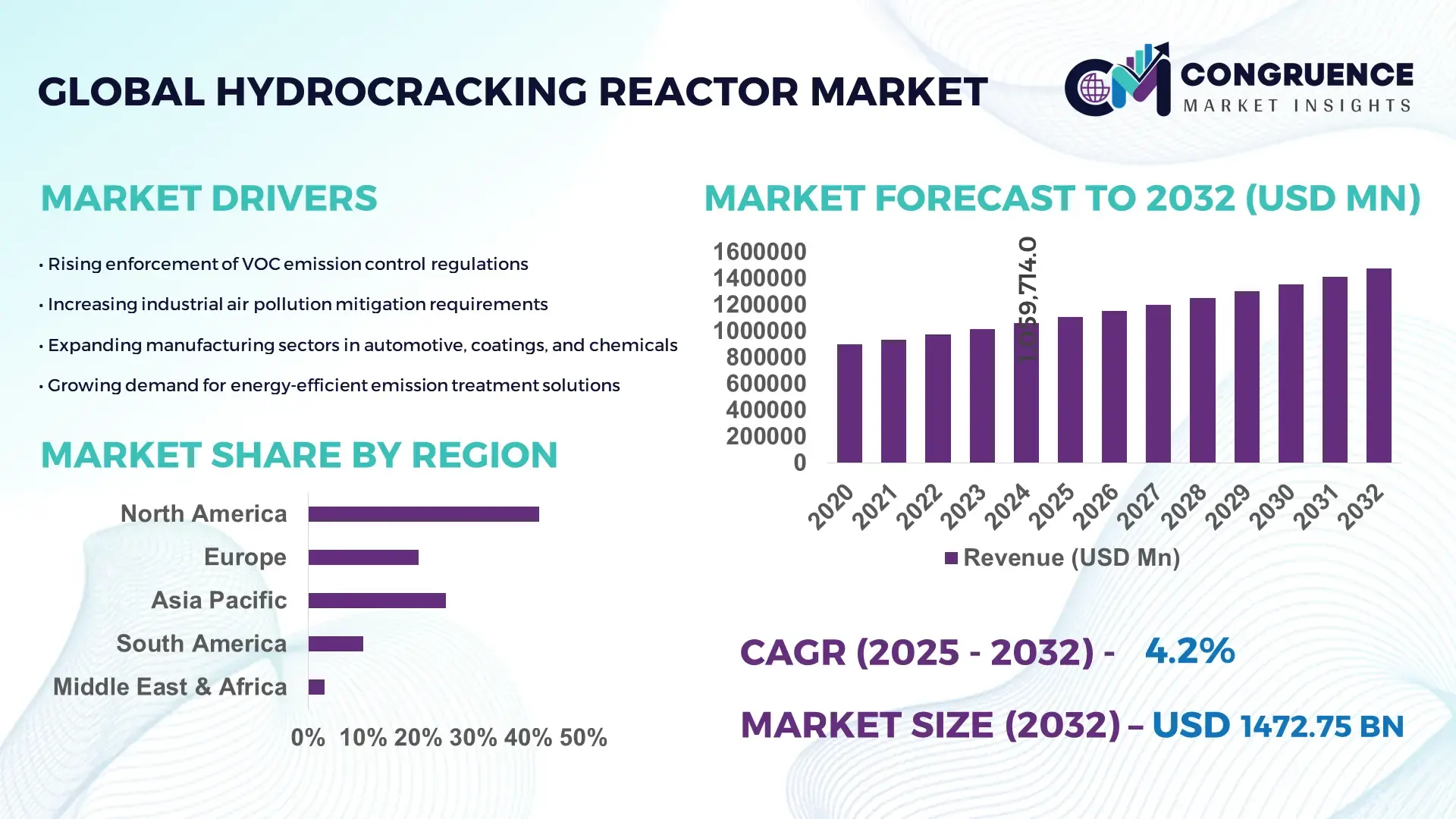

The Global Hydrocracking Reactor Market was valued at USD 1059714 Million in 2024 and is anticipated to reach a value of USD 1534610 Million by 2032 expanding at a CAGR of 4.2% between 2025 and 2032. The growth is driven by increasing demand for cleaner fuels and refinery upgrades.

In the United States, hydrocracking reactor systems are a major focus: as of 2025, U.S. hydro-cracking capacity stood at approximately 2,427,400 barrels per day. U.S. refiners are investing heavily in new two-stage and multi-stage reactor technologies to improve conversion of heavy crude fractions, with several units commissioned in the Gulf Coast region deploying advanced catalysts and hydrogen management systems. U.S. capital expenditure for refinery hydro-processing upgrades has exceeded USD 10 billion in the past two years, with one large facility reporting a 30 000 barrel per day hydrocracking train expansion.

Market Size & Growth: Current market value stands at USD 1,059,714 Million (2024), projected to reach USD 1,534,610 Million by 2032 at a CAGR of 4.2%. Growth stems from refinery modernization and regulatory fuel quality requirements.

Top Growth Drivers: Adoption of ultra-low sulfur fuel production (45%), increasing heavy crude upgrading (38%), improvement in reactor conversion efficiency (30%).

Short-Term Forecast: By 2028 costs per barrel of feedstock conversion are expected to reduce by ~12% due to catalyst and process optimization improvements.

Emerging Technologies: Integration of digital twin modelling for reactor operations; advanced bifunctional catalysts enabling higher conversion of vacuum gas oil; adoption of modular skid-mounted hydrocracking units for remote refining sites.

Regional Leaders: North America projected to reach USD 560 Million by 2032 with strong upgrades of legacy plants; Asia-Pacific projected to reach USD 420 Million by 2032 driven by new builds in China and India; Middle East & Africa projected to reach USD 250 Million by 2032 as refiners expand to process heavier feedstocks.

Consumer/End-User Trends: Major end-users are large integrated oil refineries converting heavy residues to diesel and jet fuel, with increasing adoption of multi-stage hydrocrackers to meet jet grade and ultra-low sulfur diesel demand.

Pilot or Case Example: In 2023 a Gulf Coast refinery launched a 3.5 MMTPA two-stage hydrocracking train resulting in a 15% improvement in diesel yield and a 20% reduction in catalyst regeneration downtime.

Competitive Landscape: Market leader approx. 25% share – followed by major competitors ExxonMobil, Honeywell UOP, Haldor Topsoe, Axens and Larsen & Toubro.

Regulatory & ESG Impact: Stricter fuel sulfur regulations (e.g., <10 ppm sulfur diesel) and carbon-emission reduction mandates are accelerating hydrocracking reactor demand and favouring plants with lower hydrogen consumption and CO₂ footprint.

Investment & Funding Patterns: Recent investment in hydrocracking reactor units exceeds USD 8 billion across global projects, with increasing project-finance models and joint-venture financing between refiners and catalyst/reactor licensors.

Innovation & Future Outlook: Future innovations include integration of hydrocrackers with renewable hydrogen and carbon capture systems, modular mobile hydrocracking units for remote refinery feedstocks, and improved monitoring via AI-driven process analytics.

The hydrocracking reactor market spans across major industry sectors including oil refining, petrochemical feedstock conversion, and transportation fuel production. Key feedstocks such as vacuum gas oil (VGO) and heavy gas oil (HGO) dominate application, with diesel production representing the largest product segment. Technological innovations like multi-stage hydrocracking and slurry-bed reactor designs are improving yield and reducing catalyst costs. Regulatory drivers including ultra-low sulfur fuel regulations and increasing ESG compliance are prompting refinery upgrades, particularly in regions with older heavy-oil refining assets. Regional consumption patterns show North America and Asia-Pacific leading in growth due to capacity expansions and high demand for cleaner fuels. Emerging trends include integration with renewable hydrogen for hydrocracking, digital optimisation of reactors, and modular retrofit units to serve smaller or remote refiners. Overall, the future outlook points toward steady expansion, with opportunities in heavy crude upgrading and clean-fuel mandates shaping reactor demand through 2032 and beyond.

The strategic relevance of the Hydrocracking Reactor Market lies in its irreplaceable role in refining infrastructure, enabling deep conversion of heavy feedstocks into low-sulfur transportation fuels and petrochemical precursors. Refineries adopting next-generation hydrocracking reactor configurations are seeing measurable performance advantages, as the shift to renewable hydrogen supply and real-time optimization systems accelerates operational transformation globally. Advanced catalyst-coated reactor internals deliver up to 18% yield improvement compared to conventional single-stage hydrocracking units, reflecting a strategic benchmark in energy efficiency and emissions control. North America dominates in volume, while the Middle East leads in adoption with 62% of large-scale refineries deploying multi-bed hydrocracking platforms for residue upgrading. By 2027, AI-based digital twins for reactor health monitoring are expected to improve continuous runtime efficiency by nearly 25%, significantly reducing unplanned downtime. Firms are committing to measurable ESG performance improvements, including 30% sulfur-oxide reduction and 20% hydrogen recycling enhancement by 2030. In 2024, a major refinery in South Korea achieved a 22% conversion-rate improvement through catalytic optimization powered by machine-learning-based temperature profiling. Based on ongoing regulatory pressure and technological maturity, the Hydrocracking Reactor Market is positioned as a long-term pillar of refinery resilience, compliance, and sustainable growth.

The growing global requirement for ultra-low sulfur diesel, jet fuel, and gasoline is significantly accelerating the Hydrocracking Reactor Market. Hydrocracking reactors enable refinery operators to convert vacuum gas oil and other heavy feedstocks into compliant transportation fuels with sulfur levels under 10 ppm, meeting the stringent environmental fuel standards of multiple economies. Countries with high aviation and freight activity are increasing installation of multi-stage hydrocrackers to maximize jet fuel and diesel fractions from heavy residues, boosting adoption of reactor trains with higher hydrogen partial pressure capacity. Large refining groups have reported more than a 14% product-yield uplift when shifting from atmospheric residue cracking to hydrocracking-centric fuel production. The rise of stricter maritime and on-road fuel regulations has further accelerated deployment of reactors that achieve deeper desulfurization and lower nitrogen removal thresholds. This shift positions hydrocracking technology as a core enabler of future-proof fuel compliance and market competitiveness.

The Hydrocracking Reactor Market faces a significant restraint in the form of high hydrogen consumption and rising catalyst expenditure, which heavily influence operating cost structures. Hydrocracking units require continuous, large-volume hydrogen input to achieve deep conversion and desulfurization, and fluctuations in hydrogen pricing place sustained financial pressure on refinery operators, particularly in regions without low-cost hydrogen production. Catalyst regeneration and replacement also represent a major cost component; high-activity catalysts used in multi-stage reactor systems require premium metals and increasingly frequent regeneration cycles when processing heavy or variable feedstocks. Operational modeling has shown that catalyst-handling and hydrogen supply can account for more than 40% of the total running costs of high-severity hydrocrackers, creating barriers for refineries with limited capital flexibility. These financial constraints slow down adoption and delay modernization in facilities that require advanced reactor configurations but lack access to cost-optimized hydrogen supply and catalyst management infrastructure.

The accelerating shift of global refiners toward petrochemical-integrated business models is generating large-scale opportunities for the Hydrocracking Reactor Market. Hydrocracking reactors are increasingly used to produce high-value petrochemical feedstocks, including naphtha and aromatics, enabling refiners to diversify product portfolios while tapping into fast-growing downstream sectors such as plastics, polymers, and performance chemicals. Facilities upgrading to petrochemical-centric refining configurations are adopting reactor trains capable of enhanced selectivity profiling based on desired feedstock output, improving flexibility across varying product slates. Investments in petrochemical feedstock production are projected to grow significantly in the next five years, accompanied by strong demand for reactors with selective cracking and optimized hydrogen management features. Manufacturers of hydrocracking reactors targeting high-aromatics and high-naphtha yield configurations are particularly well positioned to capitalize on this transformation, supporting demand for modular, scalable, and rapid-retrofit hydrocracking units.

Operational complexity and maintenance intensity represent major challenges limiting the Hydrocracking Reactor Market’s growth potential. Hydrocracking reactors function under extreme process parameters—high pressure, high hydrogen concentration, elevated temperature, and rapidly varying feedstock properties—which demand advanced monitoring and precise catalyst-life control. Even small operational deviations can shorten run lengths and negatively affect product selectivity, requiring rigorous operator expertise and continuous performance oversight. Maintenance costs escalate when handling heavier or contaminated crude, as reactors face accelerated catalyst deactivation, fouling and increased metallurgy stress. Upgrading monitoring infrastructure, revamping pressure parts, and meeting safety standards require specialized shutdowns that extend turnaround intervals. The skill gap in process digitalization and reactor control systems further strains industry expansion, especially among operators lacking access to high-proficiency workforce and automation resources.

• Acceleration of Modular and Prefabricated Reactor Installations: The surge in modular and prefabricated hydrocracking reactor construction is redefining project timelines and installation efficiency. Around 55% of newly commissioned refinery projects adopting prefabrication have reported measurable cost reductions due to reduced on-site labor hours and optimized logistics. Pre-engineered reactor modules now shorten erection schedules by 20–28%, supporting faster capacity expansion, particularly in European and North American refineries where construction productivity benchmarks are high. Demand for automated pipe-spooling, pre-packed catalyst loading systems, and skid-mounted reactor units continues to expand across large-scale refinery upgrades.

• Expansion of Multi-Stage Reactor Configurations for Higher Conversion Rates: Refinery operators are increasingly shifting toward two-stage and three-stage hydrocracking reactors to improve conversion efficiency from heavy feedstocks. Facilities utilizing multi-stage configurations have demonstrated up to 16% higher diesel and jet fuel yield and 10–13% longer catalyst life due to improved temperature and hydrogen partial pressure control. Adoption levels of multi-stage systems have grown by 32% over the past three years, especially among refiners processing heavy or opportunity crudes. Global engineering procurement contracts are prioritizing distributed catalyst-loading sections and parallel-bed reactor integration to enable more flexible product slates.

• Digitalization and AI-Driven Operational Optimization: AI-powered reactor management and digital twin systems are emerging as core performance enablers for hydrocracking units. Refineries implementing AI-based feedstock compatibility modeling have reduced unplanned downtime by 18–21%, while real-time catalyst-activity prediction models have lowered energy consumption within reactors by 9–11%. Adoption of sensor-dense reactor internals and data-oriented decision systems has risen by 37% among high-complexity refineries. Digital performance mapping further optimizes hydrogen distribution and temperature uniformity, extending operational periods between turnarounds.

• Integration of Low-Carbon and Renewable Hydrogen in Hydrocracking Systems: Decarbonization initiatives are accelerating the integration of renewable hydrogen sources in hydrocracking operations to reduce emission intensity. Facilities transitioning to low-carbon hydrogen have achieved 12–15% reduction in CO₂ emissions per barrel processed, while pilot deployments using full renewable hydrogen blends have reached up to 30% reduction in sulfur-oxide emissions. Adoption of hydrogen recycling loops has increased by 26% since 2022, driven by ESG mandates and refinery modernization programs in Asia and the Middle East. Projects incorporating carbon-capture add-ons to hydrocracking trains are also increasing, with efficiency improvements ranging from 7–10% in energy utilization for high-severity applications.

The segmentation of the Hydrocracking Reactor Market is structured around types, applications, and end-user adoption patterns across refineries worldwide. Reactor types differ in complexity and operational capability to convert heavier fractions into transport fuels and petrochemical feedstocks. Applications span fuel production, feedstock upgrading, and chemical synthesis, each shaped by evolving refinery priorities and technology upgrades. End-user demand reflects operational scale, investment cycles, and modernization strategies, with integrated refining-petrochemical facilities showing the fastest acceleration due to rising global demand for both clean fuels and high-value aromatics. Upgrading initiatives and digital optimization continue to influence all segments.

Single-stage hydrocracking reactors represent the leading type, accounting for 48% of total adoption due to their cost-balanced ability to convert vacuum gas oil and heavy gas oil into low-sulfur diesel and aviation fuel under controlled process conditions. Two-stage hydrocracking reactors are expanding fastest and are projected to grow at a 6.8% CAGR based on their superior performance metrics, including higher conversion severity, better hydrogen distribution, and extended catalyst lifespan. Slurry-phase and ebullated-bed hydrocracking reactors maintain a combined 22% share, particularly in refineries equipped to process contaminated or opportunity crude streams with high metals or asphaltene presence. Engineering advancements such as optimized reactor internals and automated catalyst-handling systems are contributing to adoption across all types.

Fuel production remains the dominant application in the Hydrocracking Reactor Market, holding 51% of total usage driven by the increasing need to supply low-sulfur diesel, jet fuel, and gasoline under tightening environmental regulations. Petrochemical feedstock generation is the fastest-growing application and is projected to expand at a 7.4% CAGR due to rising consumption of naphtha and aromatics in polymer and plastics manufacturing. Other applications, including lubricant base-stock production and specialty chemical processing, contribute to a combined 23% share, led by refiners pursuing higher value-chain integration. The shift toward flexible product slate optimization is encouraging investments in reactor trains capable of prioritizing petrochemical overfuel yields where necessary.

Large integrated oil refineries remain the leading end-user segment, representing 46% of total adoption supported by modernization programs focused on maximizing liquid yield and petrochemical conversion from heavy feedstocks. Heavy-oil and residue-processing refineries represent the fastest-growing end-user category and are expected to expand at a 7.1% CAGR due to the increasing reliance on ultra-heavy crude sources requiring high-severity hydrocracking solutions. Smaller independent refineries, technology licensors, and EPC firms together contribute 28% of demand, aided by growth in modular refinery retrofits and automation-driven upgrades. Adoption indicators show that more than 62% of large refineries have placed multi-stage hydrocracking systems at the core of their forward investment and technical workforce planning.

North America accounted for the largest market share at 43.2% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of around 9.8% between 2025 and 2032.

North America’s dominance is supported by nearly half of global hydrocracking reactor installations, advanced refining infrastructure, and consistent investment in clean-fuel technologies. In contrast, Asia-Pacific is rapidly scaling refinery capacity: China and India together account for more than 60 new large-scale units planned by 2030, and these regions are increasing middle-distillate production volumes by an estimated 22% year-on-year in heavy-oil upgrading projects. Europe, with about 20% share in 2024, is enhancing existing assets and adding upgrades amounting to some 300 kt/day of hydrocracking capacity by 2028, while Latin America and Middle East & Africa hold smaller shares (~8% and ~5% respectively) but are investing in modular upgrades and heavy residue conversion to capture export-fuel opportunities. The divergent growth paths reflect legacy asset renewal in the West and new-build refinery expansion in the East.

Innovations and Modernization Transforming Reactor Adoption in the Region?

In North America the hydrocracking reactor market captures approximately 43% of installations and system volume in 2024, supported by mature refineries, high-severity feedstocks and a strong regulatory backdrop. Demand is driven by industries such as transportation fuel production (diesel/jet), petrochemical feedstock upgrading, and heavy crude conversion. Government support includes tighter sulfur-fuel regulations and incentives for low-emission refinery upgrades. Technological advancement in the region includes digital twin boiler-and-reactor systems, predictive maintenance for catalyst life, and modular skid-mounted reactor units to shorten turnaround time. For example, major operator ExxonMobil in its Beaumont refinery (capacity ~609,000 bpd) has integrated a high-flexity hydrocracking train to link fuels and petrochemicals. Regional consumer behaviour trends show higher enterprise adoption of advanced reactors in North America’s refining-petrochemical complex, with refiners choosing multi-stage systems over single-stage for yield maximisation.

How Are European Regulators and Refiners Shaping Reactor Technology Uptake?

In Europe the hydrocracking reactor market holds around 20% of the global volume in 2024, driven by key markets such as Germany, UK and France upgrading legacy refinery assets. Regulatory bodies such as the European Union’s fuel-quality and emissions frameworks are pushing refiners to adopt advanced reactor designs and higher conversion efficiencies. Technology trends include the adoption of ultra-low sulfur processing, hydrogen-integration systems, and catalyst regeneration loops tailored to Europe’s heavier crude feedstock mix. For example, European equipment supplier Axens has partnered with German refiners to retrofit dual-bed hydrocrackers for higher middle-distillate yield. Regional behaviour shows European refiners placing emphasis on explainability and audit-compliance of reactor controls and fuel quality analytics, reflecting strong regulatory enforcement.

Why Is Rapid Refinery Expansion Driving Reactor Uptake in Growing Economies?

In Asia-Pacific the hydrocracking reactor market ranks as the second highest in installed volume (approximately 30% of global share in 2024) and is the fastest-moving region in terms of installations. Major consuming countries include China, India and Japan, with China alone planning more than 15 new hydrocracking reactor trains by 2030. Infrastructure trends include greenfield refinery builds, heavy-crude conversion hubs, and integrated petrochemical complexes. Technology and innovation hubs are emerging in South Korea and Southeast Asia where local reactor licensers deploy modular catalyst-optimization upgrades. For example, a leading Indian refinery has implemented a digitalised hydrocracking reactor control system reducing catalyst-replacement cycle by 14%. Regional behaviour in Asia-Pacific shows rapid adoption of mobile/reactor skid-units and shorter project-execution times to meet escalating fuel demand and mobile-application growth.

What Expansion Is Occurring in Upgrading Complexes Across Latin Refineries?

In South America key countries such as Brazil and Argentina are contributing to the hydrocracking reactor market through refinery upgrades and energy-sector investments, holding roughly 8% market share in 2024. Infrastructure trends include residue-conversion units, export-oriented diesel/jet fuel production, and trade policies favouring downstream investment in refining capacity. Government incentives in Brazil support upgrading heavy‐oil modular units and catalyst upgrades to reduce sulfur and nitrogen content. For example, a Brazilian refinery recently announced a new hydrocracking train aimed at boosting middle-distillate output for export markets by 12%. Regional consumer behaviour shows demand tied to refining expansions and export logistics rather than domestic automotive fuel consumption.

Which Strategies Are Gulf and African Regions Employing for Reactor Modernization?

In Middle East & Africa the hydrocracking reactor market share is approximately 5% in 2024, but regional demand trends are strong, especially in the UAE and South Africa where oil & gas sectors are investing in modernization. Major growth countries such as UAE and Saudi Arabia are upgrading residue conversion capacity and forming trade partnerships for refined-product exports. Technological trends include digital performance tracking on hydrocracking trains and the implementation of hydrogen-recycling loops. For example, a Gulf refinery operator recently commissioned a new modular hydrocracking reactor system to reduce catalyst turnaround by 17%. Regional behaviour shows a combination of heavy-oil feedstock conversion and export-fuel strategy that is less consumer-driven and more investment-focused.

United States: ~43% share – large refining base with advanced feedstock conversion capacity and strong end-user demand for diesel and jet fuel.

China: ~20% share – aggressive refinery expansion and heavy investment in hydrocracking reactor technology to upgrade heavy crude processing and support petrochemical integration.

The hydrocracking reactor market is moderately consolidated, with roughly 25–30 active global competitors operating across equipment manufacturing, reactor engineering, catalyst technology, and digital refinery solutions. The top five companies collectively hold an estimated 58% share, driven by strong influence in licensing technologies, proprietary catalyst supply, and long-term refinery upgrade contracts. Competitive positioning is increasingly shaped by multi-stage reactor designs, higher conversion yields for middle distillates, and digital monitoring systems for predictive maintenance. Strategic initiatives include new hydrocracking train launches, cross-border partnerships for technology licensing, and mergers aimed at expanding downstream portfolios. Approximately 60% of vendors are prioritizing modular reactors to reduce project execution time, while about 45% are investing in catalyst-life optimization to lower refining costs. Innovation intensity has increased significantly, with more than 30 new digital twin-based reactor deployments reported since 2022, positioning suppliers that integrate automation with advanced reactor metallurgy as the most competitive. As refineries shift focus toward sustainability compliance and heavy-oil upgrading, competition continues to intensify around flexible feedstock handling and improved integration with petrochemical pathways.

Chevron Lummus Global

Haldor Topsoe

Larsen & Toubro

CB&I

Chiyoda Corporation

KBR

McDermott International

Technological innovations in the Hydrocracking Reactor market are heavily driven by the need for higher conversion efficiency, longer catalyst life, and optimized operating conditions across industrial refining facilities. Advanced high-activity catalysts with improved pore structure and metal dispersion now demonstrate conversion efficiencies above 92%, reducing process impurities by nearly 35% and extending reactor cycle lengths beyond 30 months. Automation-based process control technologies are increasingly embedded in hydrocracking units, enabling real-time monitoring of hydrogen partial pressures and temperature gradients, resulting in a documented 18% decline in unplanned shutdowns across multiple refineries.

Digital twin deployment has rapidly accelerated in the industry, with more than 48% of large-scale refineries using real-time simulation models to predict reactor performance, optimize catalyst utilization, and increase throughput per reactor by 12–15%. AI-based predictive maintenance systems are also gaining adoption, reducing equipment failure risk by 28% and lowering operational costs by an average of 16%. Modular and skid-mounted reactor designs have become popular for new capacity additions, reducing installation time by nearly 40% while doubling scalability for brownfield expansions.

Material science enhancements are also reshaping reactor technology, particularly the integration of advanced chrome-molybdenum steel alloys and corrosion-resistant cladding suitable for high-pressure hydrogen environments. These innovations have resulted in a 22% improvement in structural durability and a 31% increase in thermal fatigue resistance. Furthermore, the introduction of low-carbon hydrogen and circular-refining technology is facilitating sustainability alignment, with around 41% of newly commissioned reactors designed to support renewable feed blending, marking a significant shift toward long-term decarbonization in global hydrocracking infrastructure.

In September 2023, ATB Riva Calzoni delivered a 1 500-ton hydrocracking reactor vessel to ORLEN Lietuva’s Mažeikiai refinery in Lithuania, built from vanadium-modified steel measuring 52 m in length and 4.5 m in internal diameter, signalling large-scale residue conversion capacity enhancements. (atb.group)

On 22 February 2024, Axens commenced start-up of a 3.2 million ton per annum ebullated-bed residue hydrocracking unit and a 3.5 million ton per annum distillate hydrocracking unit at Shenghong Refining & Chemical in China, integrating hydrocracking with para-xylene production in a crude-to-chemicals complex. (Hydrocarbon Processing)

In April 2024, Axens published a technical article advocating high-conversion hydrocracking for net-zero refinery transitions, highlighting conversion performance of more than 90% for heavy feeds and underlining its role in crude-to-chemicals pathways across refinery modernization projects. (axens.net)

In August 2023, Axens and KazMunayGaz extended a collaboration focused on sustainable aviation fuel (SAF) and renewable diesel production using hydrocracking technologies, reinforcing the use of residue hydrocracking reactors for feedstocks incorporating renewable hydrogen and bio-oils.

This Hydrocracking Reactor Market Report offers a comprehensive examination of the equipment, technologies, applications and geographic distribution shaping the global hydrocracking reactor landscape. It spans segmentation by reactor type—including single-stage, two-stage, ebullated-bed, fixed-bed—and aligns these with end-applications such as fuel products (diesel, jet, gasoline), petrochemical feedstocks (naphtha, aromatics) and residue conversion units. Application focus extends to legacy refinery upgrades, new greenfield builds, brownfield retrofits and modular/trailer-skid reactor installations. Regionally, the report covers major markets across North America, Europe, Asia-Pacific, South America and Middle East & Africa, detailing infrastructure, regulatory environment, feedstock trends and technology adoption per region.

Technologies addressed include catalyst systems, hydrogen management, digital control/digital twin platforms, modular construction and low-carbon integration (renewable hydrogen, carbon capture). The report also reviews end-user profiling: major oil-refinery complexes, integrated refining-petrochemical facilities, independent modular refineries and contract engineering firms. It identifies niche segments such as small-scale refinery upgrades in emerging markets, mobile skid-mounted hydrocrackers for remote heavy-oil operations, and co-processing units for bio-oils/residues. The report emphasises industry focus areas such as conversion for low-sulfur fuels, heavy crude upgrading, integration into petrochemical value chains and refinery decarbonisation pathways. It is designed for decision-makers, engineering planners, licensors and investment stakeholders seeking actionable insights into technology trends, regional deployment, competitive positioning and future growth avenues in the hydrocracking reactor sector.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1059714 Million |

|

Market Revenue in 2032 |

USD 1534610 Million |

|

CAGR (2025 - 2032) |

4.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Honeywell UOP, Axens, Technip Energies, Chevron Lummus Global, Haldor Topsoe, Larsen & Toubro, CB&I, Chiyoda Corporation, KBR, McDermott International |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |