Reports

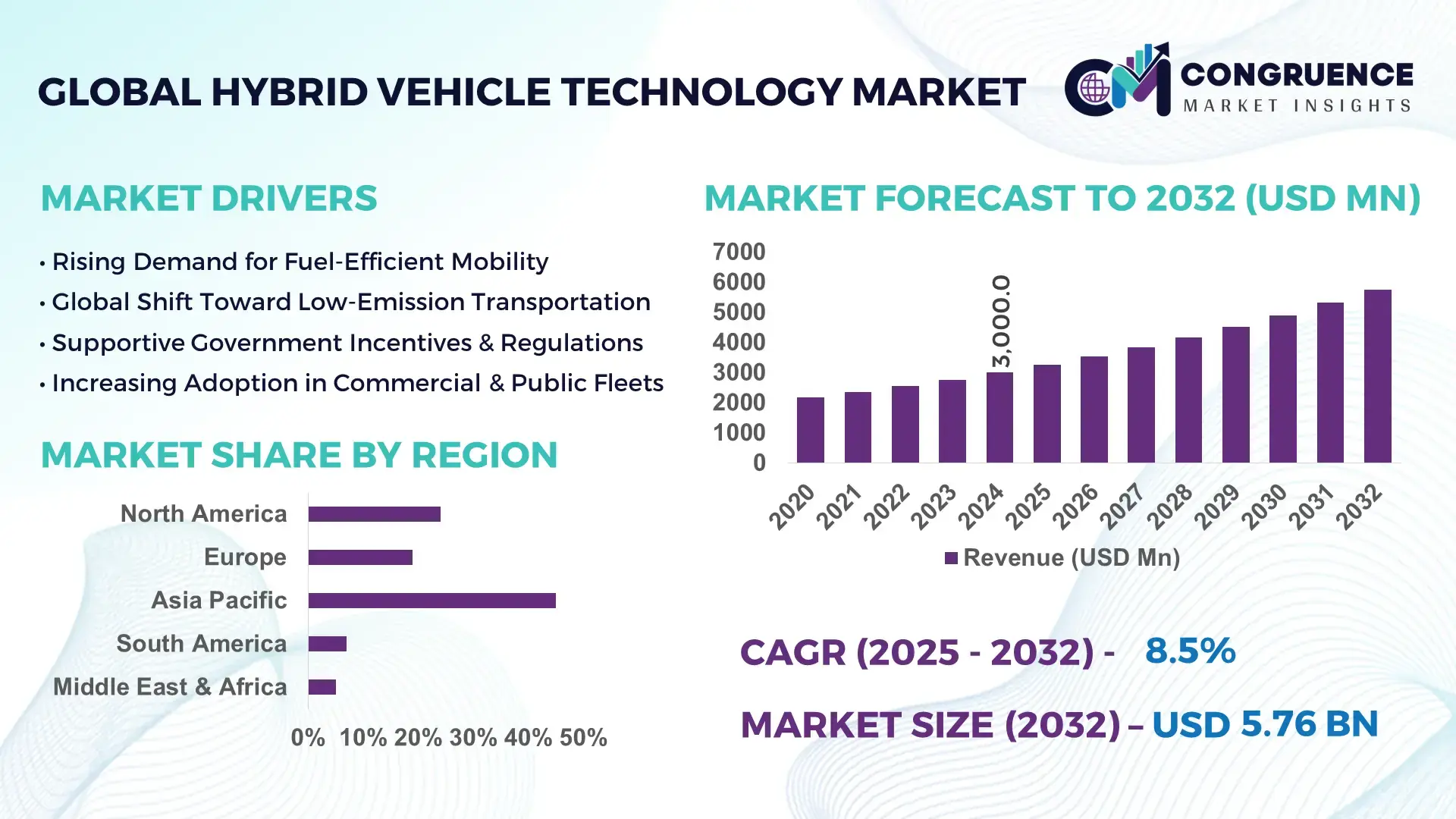

The Global Hybrid Vehicle Technology Market was valued at USD 3,000 Million in 2024 and is anticipated to reach a value of USD 5,761.8 Million by 2032, expanding at a CAGR of 8.5% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is underpinned by rising regulatory pressure to reduce emissions and increasing demand for fuel‑efficient transport solutions.

In China, which leads the hybrid‑vehicle technology market, automakers like BYD, Geely, and SAIC have built substantial production capacity: China produced over 12.8 million new‑energy vehicles in 2024, of which roughly 40% were plug-in hybrids. The country is aggressively investing in hybrid powertrain R&D, including advanced regenerative braking and energy‑efficient battery systems. China is also scaling fleet applications: public transport and delivery vehicles increasingly use hybrid drivetrains, reducing operational costs while meeting urban emission targets.

Market Size & Growth: The market is projected to grow from USD 3,000 Million in 2024 to USD 5,761.8 Million by 2032 at a CAGR of 8.5%, driven by tighter emissions regulation and cost‑effective electrification.

Top Growth Drivers: Penetration of hybrid adoption (~ 40%), improvement in fuel efficiency (~ 30%), and government incentives (~ 25%).

Short-Term Forecast: By 2028, hybrid powertrain system costs are expected to decline by ~ 15% due to scale economies and modular architectures.

Emerging Technologies: Mild‑hybrid systems, regenerative braking enhancements, and next‑generation battery-pack integration.

Regional Leaders: Asia-Pacific (~ USD 2,200 M by 2032), North America (~ USD 1,500 M), Europe (~ USD 1,000 M) — with Asia-Pacific driven by fleet electrification, North America by consumer hybrids, and Europe by regulation-led adoption.

Consumer/End-User Trends: Increasing use of hybrids in commercial fleets and ride‑hailing services for lower running costs and emissions.

Pilot or Case Example: In 2025, a major European logistics firm piloted hybrid delivery vans and reduced fuel consumption by ~ 18% per vehicle.

Competitive Landscape: Market leader estimated at ~ 30% share, with major competitors including Toyota, General Motors, Ford, and Honda.

Regulatory & ESG Impact: Stricter CO₂ emission standards, tax credits, and low-emission zones are boosting hybrid adoption globally.

Investment & Funding Patterns: Several OEMs have announced over USD 2 billion in hybrid‑powertrain R&D since 2023, along with strategic partnerships with battery suppliers.

Innovation & Future Outlook: Focus is shifting toward plug-in hybrids with 100+ km electric range, multi-mode hybrid systems, and software-driven energy management.

The hybrid vehicle technology space is evolving rapidly, with innovations and investments aligning to make it a sustainable, efficient, and regulation‑friendly powertrain choice for the next decade.

The market is also seeing notable growth across passenger cars, commercial fleets, and public transit, driven by technological advances, favorable regulation, and shifting consumer preferences toward lower emissions and lower total cost of ownership.

The hybrid vehicle technology market sits at a strategic inflection point, offering a bridge between traditional internal combustion engines and fully electric vehicles (EVs). For many automakers, hybrids deliver ~ 25% better fuel efficiency compared to conventional ICE-only vehicles while avoiding some of the infrastructure challenges that pure EVs face. When benchmarked against older powertrains, the latest multi-mode hybrid systems deliver up to 20% better energy recovery during braking compared to first-generation mild-hybrids — a significant boost in operational efficiency.

Regionally, Asia-Pacific dominates in volume, driven by mass production and fleet electrification, while Europe leads in adoption, with over 40% of new light commercial vehicle manufacturers incorporating hybrid technologies by 2025. In the near term, by 2027, the integration of AI-powered energy management systems is projected to reduce hybrid system energy losses by 10–12%, further enhancing efficiency.

From an ESG standpoint, firms are committing to tangible goals: many automakers aim for a 30% reduction in well-to-wheel CO₂ emissions by 2030 via hybrid technology, and by 2026, several OEMs intend to recycle at least 50% of battery materials from hybrid battery packs. In a micro-scenario, in 2025, a major Chinese OEM achieved a 15% reduction in fuel consumption across its hybrid fleet by deploying predictive driving algorithms.

Looking forward, hybrid vehicle technology represents a resilient and compliant platform. It aligns with sustainability goals, enables incremental electrification, and de-risks transitions — positioning it as a cornerstone of both current automotive portfolios and future mobility strategies.

The Hybrid Vehicle Technology Market is driven by a complex interplay of regulatory pressures, consumer demand for fuel efficiency, and technological innovation. As governments worldwide tighten emissions standards, automakers are increasingly turning to hybrid solutions to meet compliance while maintaining range and performance. At the same time, consumers — especially in cost-conscious and fleet sectors — view hybrids as a pragmatic alternative to full EVs, offering lower running costs without requiring full charging infrastructure. On the technology side, advances in battery energy density, power electronics, and control algorithms are enabling more efficient, compact, and cost-effective hybrid powertrains. The market is further shaped by macroeconomic factors: rising fuel prices, geopolitical concerns around raw material supply, and capital investment cycles for R&D and manufacturing capacity all influence adoption. Collectively, these forces make the hybrid vehicle technology market a strategically critical segment as the automotive industry transitions to greener mobility.

Regulatory pressure is one of the most powerful drivers in the hybrid vehicle technology market. Many regions have instituted stricter CO₂ emissions targets that make hybrid powertrains highly attractive for automakers: hybrids can significantly reduce tailpipe emissions without requiring the full infrastructure shift needed for battery-electric vehicles. Countries in Europe and Asia are mandating tighter fuel efficiency regulations, pushing OEMs to adopt hybrid systems in both passenger and commercial vehicles. Hybrid vehicles enable compliance by combining internal combustion engines with electric motors and regenerative braking, which together reduce greenhouse gas emissions and improve fuel efficiency. Financial incentives such as tax credits and low-emission zones also encourage adoption, accelerating technology uptake.

High upfront costs remain a significant restraint on the widespread adoption of hybrid vehicle technology. Although hybrids reduce fuel consumption, their initial manufacturing cost is higher than conventional ICE vehicles due to the need for additional components like electric motors, power electronics, and batteries. These incremental costs translate into higher sale prices, which can be a barrier for cost-sensitive consumers, especially in emerging markets. While long-term fuel savings can offset costs, not all buyers have the time horizon or usage pattern to realize these benefits. Financing models and residual value uncertainties further restrict adoption, particularly where subsidies are weak.

Fleet electrification presents a major growth opportunity for hybrid vehicle technology. Logistics companies, delivery services, and public transport operators benefit from hybrids as they combine electric efficiency with combustion engine range, reducing both fuel costs and emissions without sacrificing operational flexibility. Low-emission zones and government incentives encourage adoption of hybrid buses and vans. Predictive route optimization and telematics maximize electric motor usage, enabling measurable ROI and positioning hybrids as an ideal solution for urban fleet operations.

Battery supply risk represents a key challenge for hybrid vehicle technology. Hybrids rely on lithium-ion batteries and other critical materials such as nickel and cobalt. Fluctuations in raw material prices, geopolitical constraints, and limited refining capacity can increase production costs or create bottlenecks. Inadequate recycling infrastructure raises long-term sustainability concerns. Manufacturers may need to invest heavily in securing stable battery supply chains or alternative chemistries, which can increase costs and create planning uncertainties for scaling hybrid production.

Modular Powertrain Architectures: There is a rising shift toward modular hybrid platforms. These architectures allow automakers to mix and match electric motors, engines, and power electronics, reducing development time by 20–25% and cutting tooling costs by ~18%.

Advanced Regenerative Braking Systems: Regenerative braking is becoming more efficient: newer hybrid models recapture up to 70% more kinetic energy compared to earlier-generation hybrids, translating into measurable fuel savings during urban driving cycles.

Integration of Predictive AI Energy Management: OEMs are deploying AI-driven control systems that predict driver behavior and route profiles, improving battery-electric motor utilization by as much as 12% in real-world driving.

Fleet Electrification Adoption: Hybrid vehicles are seeing increasing use in urban logistics and public transport – hybrid vans and buses now account for roughly 35% of new fleet orders in key city markets, driven by urban emissions regulation and total cost of ownership benefits.

The Hybrid Vehicle Technology Market is systematically segmented based on type, application, and end-user to provide detailed insights for strategic decision-making. By type, the market comprises mild hybrids, full hybrids, and plug-in hybrids, each offering unique performance and energy efficiency benefits tailored to diverse vehicle categories. By application, hybrids are deployed across passenger vehicles, commercial fleets, and public transport systems, with specific designs optimizing fuel efficiency and emission reduction per sector. End-user segmentation spans individual consumers, corporate fleets, and government/public transport entities, each with distinct adoption patterns and operational requirements. Consumer preferences, regulatory mandates, and infrastructure readiness collectively influence these segments, driving tailored product development and deployment strategies. Insights into usage intensity, urban versus rural adoption, and fleet operational optimization further shape market planning and investment.

The full hybrid segment currently leads the market, accounting for approximately 45% of adoption, primarily due to its ability to deliver significant fuel efficiency without extensive charging infrastructure. Plug-in hybrids are the fastest-growing segment, driven by expanding electric range capabilities, favorable incentives, and integration into urban fleet operations; adoption in this segment is expected to rise sharply over the next decade. Mild hybrids contribute a combined share of roughly 30%, primarily appealing to cost-sensitive markets where partial electrification can reduce emissions. Recent technological advancements in battery efficiency, regenerative braking, and power electronics are further enhancing type-specific performance.

Passenger vehicles dominate hybrid technology adoption, holding around 50% of the application market, due to broad consumer acceptance, urban commuting needs, and corporate fleet acquisitions for company cars. The fastest-growing application area is commercial fleets, supported by low-emission zone compliance, cost-reduction mandates, and the integration of hybrid vans and trucks into logistics operations. Other applications, such as public transport and government vehicles, contribute a combined 25% share, with adoption focused on emission control and fuel efficiency. In 2024, over 38% of enterprises globally reported piloting hybrid vehicles for last-mile delivery solutions, demonstrating practical operational adoption. Additionally, in the US, 42% of municipal transportation authorities integrated hybrid buses into urban fleets, reducing operational fuel use by nearly 18%.

Individual consumers currently represent the largest end-user segment, accounting for approximately 48% of adoption, influenced by rising environmental awareness, fuel efficiency, and government incentives. The fastest-growing end-user segment is corporate fleets, fueled by operational cost savings, compliance with regional emission regulations, and the ability to reduce total carbon footprint; adoption rates in urban logistics companies have increased by 22% in 2024. Other end-users, including public transport authorities and government fleets, contribute a combined 30% share, leveraging hybrid technologies for energy efficiency and emission reduction. Notably, over 60% of Gen Z consumers prefer vehicles with hybrid technology, reflecting generational environmental preferences.

Asia-Pacific accounted for the largest market share at 45% in 2024; however, Region North America is expected to register the fastest growth, expanding at a CAGR of 9.2% between 2025 and 2032.

In 2024, Asia-Pacific recorded over 1.35 million hybrid vehicles produced, with China leading at 12.8 million new-energy vehicle output, followed by Japan with 1.2 million hybrid units. North America reached 850,000 units, driven by fleet electrification and corporate adoption, while Europe reported 700,000 units. South America produced roughly 120,000 units, and Middle East & Africa combined contributed around 80,000 units, reflecting early-stage market development. Infrastructure investments, regulatory incentives, and digital adoption patterns in each region are shaping both consumer demand and OEM strategies, emphasizing the strategic relevance of hybrids for sustainable mobility.

North America accounted for approximately 28% of the global hybrid vehicle technology market in 2024. Key industries driving demand include logistics, healthcare, and finance, where corporate fleets increasingly integrate hybrids for cost efficiency. Government support, such as tax credits and emissions-based incentives, has accelerated adoption, while regulatory changes in California and Canada promote low-emission vehicles. Technological advancements include AI-driven energy management systems and predictive telematics, improving fleet efficiency. Local players, such as Ford, have implemented hybrid powertrains across their F-series trucks, achieving a 15% reduction in fuel consumption. Consumer behavior reflects higher enterprise adoption, especially in urban centers, with over 40% of corporate fleets now integrating hybrid vehicles for operational efficiency.

Europe accounted for around 25% of the global hybrid vehicle technology market in 2024. Key markets include Germany, the UK, and France, which are focusing on emission reduction and fleet electrification. Regulatory bodies have established stringent CO₂ limits, low-emission zones, and incentives that drive hybrid uptake. Emerging technologies like multi-mode hybrid systems and advanced regenerative braking are widely adopted. Local players, such as Volkswagen, have launched hybrid versions of their Passat and Golf series, increasing urban fleet integration. Consumer behavior is influenced heavily by regulatory pressure, with over 35% of European companies upgrading corporate vehicles to hybrids to meet compliance and ESG targets.

Asia-Pacific represented the largest share at 45% of the global market in 2024, with China, Japan, and India as top consumers. China alone produced 12.8 million new-energy vehicles, including 5 million hybrids, while Japan contributed 1.2 million units. Manufacturing infrastructure is rapidly expanding, with significant investments in battery production and R&D centers. Regional tech trends include modular hybrid platforms and advanced energy management systems. Local players, like BYD, have rolled out plug-in hybrid buses across urban fleets, achieving 18% fuel savings per route. Consumer adoption is driven by urban commuting, fleet electrification, and government incentives, making Asia-Pacific a hub for both production and technology development in hybrid vehicles.

South America held approximately 7% of the global hybrid vehicle technology market in 2024, with Brazil and Argentina as key contributors. Infrastructure improvements in urban areas and growing energy diversification are encouraging hybrid adoption. Government incentives, including tax benefits and fleet subsidies, support local uptake. Local players, such as Volkswagen Brazil, are introducing hybrid delivery vans and passenger vehicles to urban fleets. Consumer behavior varies, with adoption largely tied to cost efficiency, urban commuting needs, and regional media campaigns promoting sustainable vehicles. Brazil alone recorded 70,000 hybrid units in 2024, reflecting early-stage but growing market interest.

Middle East & Africa contributed roughly 5% of the global hybrid vehicle technology market in 2024. Key growth countries include the UAE and South Africa, driven by urbanization, logistics, and construction sector demand. Technological modernization includes hybridized buses and fleet vehicles for government and commercial use. Local regulations and trade partnerships encourage cleaner transportation and fleet upgrades. Companies like Nissan South Africa have piloted hybrid taxis, achieving 12% fuel cost reductions. Consumer behavior indicates early adoption, primarily in corporate fleets and government contracts, with gradual uptake in individual consumer vehicles due to infrastructure limitations.

China – 28% Market Share: High production capacity and aggressive investment in hybrid technology have driven extensive fleet and passenger vehicle adoption.

United States – 20% Market Share: Strong corporate fleet integration, regulatory incentives, and technology-driven efficiency improvements underpin market dominance.

The Hybrid Vehicle Technology Market is moderately consolidated, with dozens of active global competitors and the top 5 companies—such as Toyota, Ford, General Motors, Honda, and Stellantis—accounting for an estimated combined share of around 60–65% of the market. These players are engaged in intense strategic initiatives: Toyota continues to refine its Hybrid Synergy Drive and expand HEV/PHEV model lines, while Ford has launched a next‑generation hybrid powertrain with improved motor efficiency for its F‑150 PowerBoost system. General Motors is leveraging its Ultium component expertise to scale hybrid drivetrains, and Honda is investing in next‑generation battery systems for better hybrid range. Stellantis, meanwhile, has committed to offering 30 hybrid models in Europe by 2024, including new eDCT transmissions and multi-energy platforms. Innovation trends are strong: AI-enabled energy management systems, modular powertrain architectures, and advanced battery-management strategies are all shaping competition. Several firms are also forming partnerships—such as powertrain JVs—to reduce development risk and cost. Overall, the competitive landscape is marked by a mix of legacy automakers, technology collaborations, and increasing R&D intensity in electrified hybrid systems.

Honda Motor Co., Ltd.

Stellantis N.V.

BMW Group

Hyundai Motor Group

Nissan Motor Co., Ltd.

Hybrid vehicle technology is increasingly being shaped by advanced control systems and next‑generation drivetrain architectures. One key trend is the integration of AI-driven energy management: modern hybrid powertrains use machine‑learning algorithms to dynamically allocate power between the internal combustion engine and electric motor, optimizing performance and fuel efficiency in real time. Complementing this, battery management systems (BMS) are becoming more sophisticated, with predictive diagnostics that enhance battery longevity and safety by monitoring state-of-charge, temperature, and health.

On the architecture side, OEMs are exploring multi-mode hybrid systems (series-parallel or P2/P3 layouts) that offer greater flexibility and better packaging. These architectures enable more efficient regenerative braking and seamless transitions between power sources. In mild hybrid (48V) systems, cost-effective torque assist and start/stop functionality are being widely adopted, delivering fuel‑economy improvements of 10–15% without major platform redesigns.

Another emerging technology is deep reinforcement‑learning (DRL) control for PHEVs: these AI techniques optimize clutch engagement and power-split decisions to improve energy efficiency under diverse driving conditions. Furthermore, there is growing interest in modular hybrid platforms that allow automakers to reuse standardized electric motors, power electronics, and transmission modules across multiple models—reducing costs and accelerating deployment.

Finally, hybrid transmission innovation plays a central role: advanced eDCT (electrified dual-clutch transmission) systems, compact power-split gearsets, and optimized thermal management are boosting hybrid powertrain performance, lowering system weight, and improving overall drivability. This continuous innovation underscores hybrids’ strategic importance as a bridge technology between internal combustion and full electrification.

In July 2024, Stellantis announced it would roll out 30 hybrid models in Europe that year, with six additional hybrid launches planned through 2026. The company highlighted its eDCT dual‑clutch transmission hybrid powertrain, delivering up to 20% fuel-economy gains in deceleration to improve efficiency. Source: www.stellantis.com

In the first half of 2024, Stellantis reported a 53% year-over-year increase in EU30 hybrid vehicle sales, driven in part by its hybrid eDCT technology and multi-energy manufacturing approach. Source: www.stellantis.com

In December 2024, Toyota Kirloskar Motor (India) launched the All‑New Camry Hybrid with its 5th-generation hybrid technology, powered by a 2.5 L Dynamic Force engine and a Li‑ion battery. The vehicle delivers a claimed efficiency of 25.49 km/l and is priced at INR 48 lakh. Source: www.toyotabharat.com

In May 2024, Ford upgraded its F‑150 Hybrid, removing the RWD (rear-wheel drive) option and improving its driveline, while reiterating plans to double production of its hybrid F‑150 in 2024 amid rising demand. Source: www.ford.com

This Hybrid Vehicle Technology Market Report covers a comprehensive spectrum of market dimensions tailored for strategic decision-makers. It examines product types (mild hybrids, full hybrids, and plug-in hybrids) and analyzes each in terms of performance characteristics, deployment contexts, and technology evolution. The report breaks down applications across passenger vehicles, commercial fleets, and public transport, giving insight into which sectors are investing most heavily in hybrid solutions. It also profiles end-users, from individual consumers and corporate fleets to government transit systems, illustrating the adoption dynamics and operational drivers in each category.

Geographically, the report spans all major regions—North America, Europe, Asia-Pacific, South America, and Middle East & Africa—offering a detailed look at production hubs, regulatory environments, infrastructure readiness, and innovation clusters. On the technology front, it delves into emerging trends such as AI-based energy management, modular hybrid platforms, deep reinforcement-learning for PHEVs, and advanced hybrid transmissions. Strategic initiatives like joint ventures, R&D investments, and manufacturing expansions are examined, along with insights into component supply chains such as battery, motor, and power-electronics production. Finally, the report includes a competitive analysis of major OEMs and their hybrid strategies, enabling stakeholders to benchmark innovation, partnerships, and market positioning as they navigate the evolving hybrid landscape.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 3,000 Million |

| Market Revenue (2032) | USD 5,761.8 Million |

| CAGR (2025–2032) | 8.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Toyota Motor Corporation, Ford Motor Company, General Motors, Honda Motor Co., Ltd., Stellantis N.V., BMW Group, Hyundai Motor Group, Nissan Motor Co., Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |