Reports

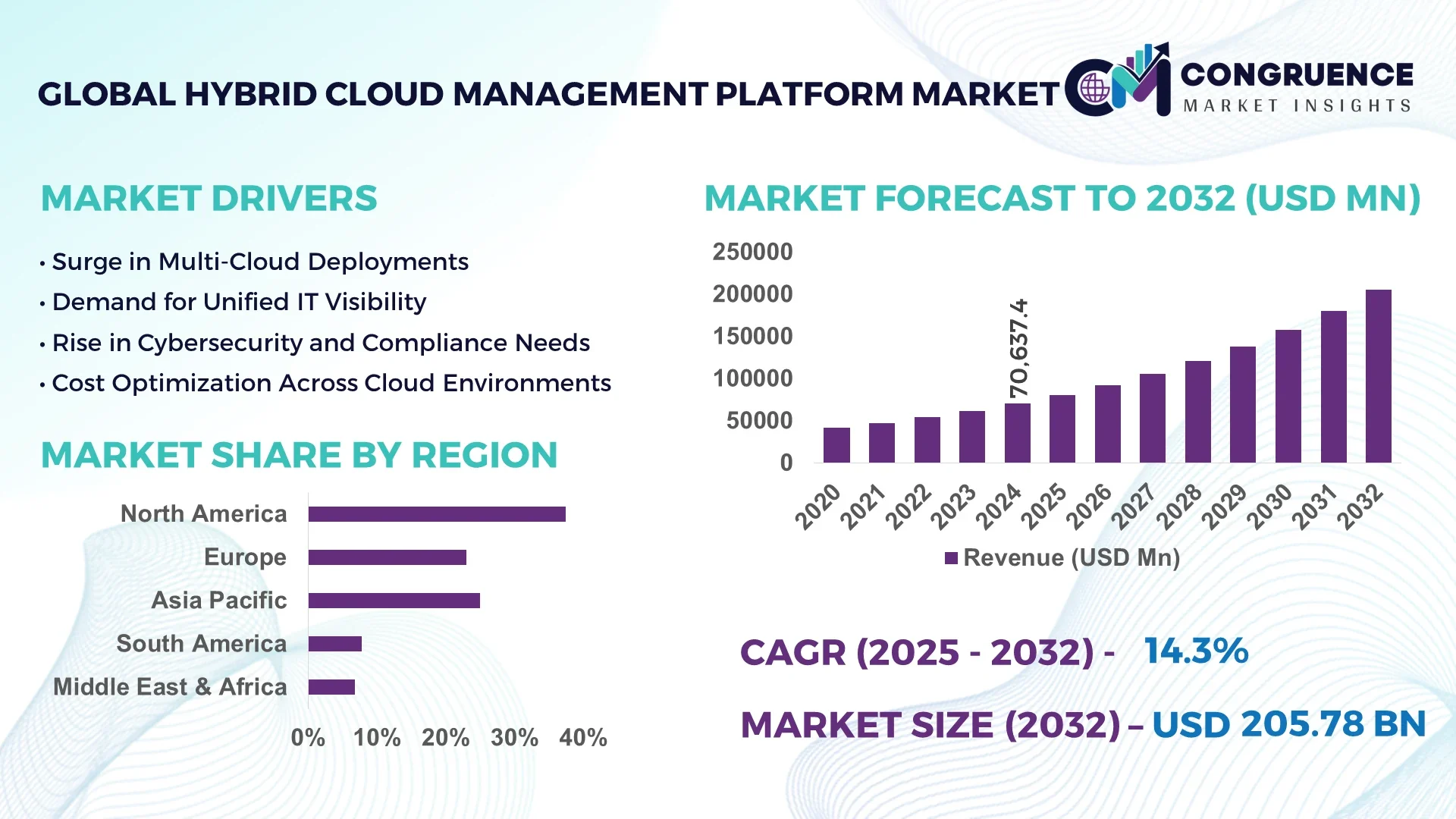

The Global Hybrid Cloud Management Platform Market was valued at USD 70,637.4 Million in 2024 and is anticipated to reach a value of USD 205,780.65 Million by 2032 expanding at a CAGR of 14.3% between 2025 and 2032.

The United States leads the Hybrid Cloud Management Platform market with extensive production capacity in software orchestration tools, substantial investments in multi-cloud security advancements, and high deployment in enterprise digital transformation projects across finance, manufacturing, and healthcare verticals.

The Hybrid Cloud Management Platform market is witnessing accelerated growth driven by the adoption of microservices architecture and container orchestration across critical sectors, including BFSI, retail, and government agencies. Key technological innovations such as AI-powered predictive scaling, unified workload orchestration, and real-time compliance monitoring are reshaping enterprise cloud management practices. Regulatory frameworks emphasizing data sovereignty and low-latency computing are encouraging regional consumption of hybrid models, while environmental priorities are propelling the adoption of energy-efficient data center management within hybrid infrastructures. With a rising demand for business continuity and seamless data governance, the Hybrid Cloud Management Platform market is also seeing increasing interest in edge-cloud integrations and zero-trust security frameworks. As multi-cloud operations become integral to business agility, the market is positioned for continuous evolution with deeper automation, intelligent cost governance, and seamless workload mobility emerging as key growth trends in the coming years.

Artificial Intelligence is reshaping the Hybrid Cloud Management Platform Market by enabling intelligent workload placement, automated security compliance, and predictive performance monitoring across multi-cloud and hybrid environments. AI-powered resource optimization tools help enterprises proactively manage workload spikes while minimizing operational costs and reducing manual intervention, which enhances the reliability of cloud-native applications in mission-critical industries. Advanced ML models embedded within Hybrid Cloud Management Platforms improve anomaly detection, identifying potential security threats and system failures before they impact operations, which significantly enhances system resilience and uptime. AI also facilitates intelligent patch management, workload balancing across on-premises and cloud infrastructures, and advanced predictive analytics, allowing businesses to align their infrastructure with real-time demands efficiently.

The Hybrid Cloud Management Platform Market is seeing a surge in demand for AI-driven observability tools that can autonomously manage complex hybrid environments while reducing infrastructure management overhead. AI is enabling dynamic policy enforcement for data governance, ensuring that data remains compliant with regional regulations while being processed across hybrid environments. In addition, AI-enhanced user access monitoring and micro-segmentation within the Hybrid Cloud Management Platform Market are addressing evolving security concerns. These AI integrations are vital in managing hybrid workloads, driving down costs through intelligent resource allocation, and supporting real-time business decision-making processes, thereby transforming how enterprises approach cloud infrastructure at scale.

“In April 2025, an AI-powered auto-remediation engine was deployed within a leading Hybrid Cloud Management Platform, reducing incident resolution times by 47% while decreasing manual ticket creation by 39% across multi-cloud environments, enabling real-time remediation of security and performance issues with minimal human intervention.”

The Hybrid Cloud Management Platform Market is undergoing significant transformation driven by advancements in AI-powered orchestration, zero-trust security frameworks, and edge-cloud integrations across enterprises adopting hybrid strategies for agility and compliance. The growing complexity of managing multi-cloud environments, alongside the necessity for real-time monitoring and intelligent workload distribution, is influencing the evolution of platform functionalities. Regulatory requirements emphasizing data privacy and sovereign cloud models are shaping deployment patterns globally within the Hybrid Cloud Management Platform Market. Additionally, the integration of cost optimization tools and intelligent capacity planning in these platforms is enabling enterprises to align infrastructure with dynamic business demands, reduce downtime, and enhance scalability while navigating an environment of digital transformation and cyber resilience.

The Hybrid Cloud Management Platform Market is driven by the rising adoption of multi-cloud strategies across enterprises seeking to enhance flexibility, operational agility, and disaster recovery readiness while avoiding vendor lock-in. Organizations in sectors such as BFSI, healthcare, and manufacturing are increasingly leveraging Hybrid Cloud Management Platforms to optimize workload distribution across private and public clouds for latency-sensitive applications and compliance-driven operations. This trend is further supported by the proliferation of SaaS, PaaS, and containerized applications, requiring robust orchestration across hybrid environments. The demand for seamless data integration and unified governance across diverse infrastructures is compelling enterprises to invest in advanced Hybrid Cloud Management Platforms, thereby driving consistent growth in platform development and adoption globally.

Integration challenges with legacy on-premises systems remain a significant restraint in the Hybrid Cloud Management Platform Market, as many organizations continue to operate mission-critical workloads on older infrastructures. These legacy systems often lack the APIs and interoperability standards required for seamless connectivity with modern hybrid cloud orchestration frameworks, creating bottlenecks in unified workload management and monitoring. The complexity of migrating large volumes of structured and unstructured data from legacy environments to hybrid models while ensuring business continuity and data integrity increases deployment timelines and operational costs. Additionally, concerns around system downtime, data silos, and maintaining compliance during transitions are limiting the pace of hybrid cloud adoption in certain industries.

The increasing demand for AI-driven automation presents a significant opportunity for the Hybrid Cloud Management Platform Market. Enterprises are actively seeking intelligent orchestration solutions that can autonomously manage workload placement, predict system failures, and ensure compliance across hybrid environments without manual intervention. AI-enhanced Hybrid Cloud Management Platforms are capable of automating tasks such as predictive scaling, anomaly detection, and dynamic resource allocation, reducing operational complexity while optimizing performance. This demand is further supported by the need for advanced analytics in real-time to make informed decisions for capacity planning, cost optimization, and disaster recovery across hybrid infrastructures. As AI technologies mature, they will enable scalable, automated, and intelligent hybrid cloud management, opening new market avenues.

Ensuring robust data security and regulatory compliance remains a challenge within the Hybrid Cloud Management Platform Market as enterprises scale operations across diverse environments and jurisdictions. The complexity of managing data privacy, sovereignty requirements, and evolving cybersecurity threats across public and private clouds adds to operational burdens for enterprises utilizing hybrid strategies. Hybrid Cloud Management Platforms must address issues such as maintaining encryption standards during data transfers, ensuring access controls, and continuous monitoring for vulnerabilities across distributed infrastructures. Enterprises face challenges in implementing unified security policies that comply with GDPR, HIPAA, and other regional frameworks while retaining system performance and flexibility, creating persistent obstacles in large-scale hybrid deployments.

• Expansion of Edge-Hybrid Integrations: Enterprises are increasingly adopting edge-hybrid models within the Hybrid Cloud Management Platform market to reduce latency for mission-critical applications. Industrial IoT deployments in manufacturing and energy sectors are driving hybrid-edge integrations to enable localized data processing while maintaining centralized control. In 2025, large-scale enterprises are prioritizing platforms that offer unified management across data center, cloud, and edge, leading to a measurable increase in real-time data utilization and advanced analytics adoption across hybrid architectures.

• AI-Driven Observability Adoption: Advanced AI-powered observability is emerging as a critical trend in the Hybrid Cloud Management Platform market. Platforms incorporating AI-based anomaly detection, predictive analytics, and auto-remediation capabilities are seeing increased adoption by enterprises seeking proactive system monitoring and cost optimization. This trend is particularly evident in regions with dense enterprise data center networks, where downtime mitigation and operational efficiency have become essential for continuous business operations.

• Multi-Cloud Security Enhancements: Security frameworks within the Hybrid Cloud Management Platform market are advancing with the introduction of micro-segmentation and zero-trust architecture to secure data across multi-cloud and hybrid environments. Enterprises in sectors such as finance and healthcare are deploying advanced encryption management and real-time threat intelligence within hybrid cloud platforms to counter sophisticated cyber threats, resulting in the measurable expansion of security-focused hybrid cloud solutions.

• Automation in Cost Governance: Automation tools for intelligent cost management and capacity optimization are being rapidly integrated into the Hybrid Cloud Management Platform market. Enterprises are leveraging AI-driven financial operations to monitor and optimize resource utilization across hybrid deployments, reducing unnecessary expenditures while ensuring scalability. The shift towards automated cost governance is facilitating more efficient cloud budget management, particularly in enterprises with complex hybrid environments.

The Hybrid Cloud Management Platform market segmentation reflects the industry's structured approach toward adopting efficient, scalable, and secure hybrid strategies across sectors. Segmentation by type highlights the focus on integrated management tools, orchestration software, and monitoring platforms, each contributing uniquely to workload distribution and data governance. Application segmentation indicates that industries including BFSI, healthcare, retail, and manufacturing are utilizing hybrid platforms to improve operational resilience and support digital transformation initiatives. End-user segmentation within the Hybrid Cloud Management Platform market reveals large enterprises as leading adopters, driven by complex infrastructure needs, while small and medium-sized enterprises are rapidly increasing their adoption of hybrid platforms to improve agility and reduce operational complexity, defining the evolving hybrid cloud landscape globally.

In the Hybrid Cloud Management Platform market, integrated management tools represent the leading type, as enterprises prioritize platforms that can unify the orchestration of workloads across private and public clouds with consistent policies and visibility. The fastest-growing type within the market is AI-powered orchestration software, driven by its ability to automate workload management, predictive resource scaling, and anomaly detection, aligning with enterprise needs for operational efficiency and security in multi-cloud environments. Other types, such as hybrid monitoring and compliance management platforms, play a vital role in enabling real-time tracking of hybrid deployments and enforcing regional compliance, contributing niche value to enterprises with regulatory obligations and performance monitoring priorities within hybrid infrastructures.

Within the Hybrid Cloud Management Platform market, disaster recovery and business continuity stand as the leading application area, as enterprises require seamless failover and operational resilience across hybrid environments for critical workloads. The fastest-growing application is intelligent workload distribution across hybrid environments, driven by the need for low-latency processing, cost optimization, and regional compliance. Other applications, including data backup and real-time analytics, are also contributing to the market, with data backup platforms supporting secure, scalable hybrid storage management and analytics tools enabling real-time business insights for industries leveraging hybrid infrastructures to drive digital transformation initiatives effectively.

Large enterprises remain the leading end-user segment within the Hybrid Cloud Management Platform market, supported by their need for scalable, secure, and unified hybrid strategies across complex infrastructures to maintain business agility and compliance. Small and medium-sized enterprises are the fastest-growing end-user segment, driven by their increasing adoption of cloud-native solutions and the need for cost-effective, flexible hybrid infrastructures to compete in digitally evolving markets. Other end-users, including government agencies and educational institutions, contribute to the Hybrid Cloud Management Platform market by leveraging hybrid solutions for secure data governance, operational scalability, and efficient service delivery while maintaining control over data across on-premises and cloud environments.

North America accounted for the largest market share at 37.4% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 16.2% between 2025 and 2032.

North America’s dominance in the Hybrid Cloud Management Platform market is underpinned by its advanced digital infrastructure and high adoption across enterprise verticals, while Asia-Pacific's growth is driven by accelerated digital transformation initiatives and expanding IT investments in countries like China, India, and Japan. Europe follows as a critical contributor with significant adoption among financial and manufacturing sectors aligning hybrid platforms with their sustainability goals. South America and the Middle East & Africa are witnessing rising demand, supported by government modernization projects and the growing need for resilient digital infrastructures. Increasing focus on secure, scalable cloud strategies across all regions is fueling the Hybrid Cloud Management Platform market globally as enterprises adapt to evolving data governance and operational efficiency demands.

Strong Enterprise Modernization Fueling Advanced Cloud Integration

Holding a 37.4% share of the Hybrid Cloud Management Platform market in 2024, the region continues to be driven by strong enterprise modernization across the BFSI, healthcare, and retail industries, adopting hybrid platforms to improve operational agility and data governance. Government initiatives encouraging secure cloud adoption for public sector digitalization projects are supporting this trend. Technological advancements such as AI-powered orchestration, zero-trust security frameworks, and edge-hybrid deployments are being rapidly integrated within enterprises to streamline workload management. The adoption of advanced data compliance tools aligned with evolving regulatory structures further strengthens the Hybrid Cloud Management Platform market, enhancing resilience and seamless integration for mission-critical operations across complex infrastructures.

Accelerating Sustainability Goals Driving Cloud Modernization

Europe contributed 28.9% of the Hybrid Cloud Management Platform market in 2024, supported by key markets including Germany, the UK, and France, which are actively modernizing their digital infrastructures in alignment with regional sustainability initiatives. The European Green Deal and data protection regulations such as GDPR are driving enterprises to adopt secure and compliant hybrid platforms. There is significant uptake of AI-enabled automation in cloud operations, with enterprises using hybrid cloud management to manage energy-efficient data centers and reduce operational complexity. The increasing need for scalable, secure, and compliant cloud strategies is accelerating the adoption of Hybrid Cloud Management Platforms across manufacturing, healthcare, and financial services, strengthening the market’s regional expansion.

Digital Infrastructure Investments Fueling Platform Uptake

Ranking as the fastest-growing region by market volume in the Hybrid Cloud Management Platform market, Asia-Pacific is led by China, India, and Japan, driven by accelerated investments in digital infrastructure, data center expansion, and smart manufacturing initiatives. Enterprises are adopting hybrid platforms to enhance operational agility and secure data management while supporting their digital transformation objectives. Rapid growth in e-commerce, fintech, and healthcare IT within the region is propelling the deployment of Hybrid Cloud Management Platforms, as businesses require scalable, flexible, and intelligent workload management across hybrid environments. The emergence of technology innovation hubs and government-led digital initiatives is further strengthening the market across the region.

Modernization in Energy and Public Sectors Boosting Demand

Brazil and Argentina are leading the Hybrid Cloud Management Platform market in the region, with growing adoption of hybrid platforms to support energy, government, and financial services modernization initiatives. The region holds a 7.3% market share, driven by the rising need for cost-effective, secure, and scalable IT infrastructures to handle increasing workloads across hybrid environments. Investments in smart city and digital health initiatives are fueling demand for hybrid platforms, enabling efficient data governance and secure workload management. Trade agreements and government incentives supporting digital transformation and cloud infrastructure investments are further advancing the adoption of Hybrid Cloud Management Platforms across the region.

Smart Infrastructure Projects Driving Hybrid Deployments

With increasing digital modernization in sectors such as oil & gas, construction, and financial services, the region is experiencing steady growth in the Hybrid Cloud Management Platform market. The UAE and South Africa are major contributors, with enterprises deploying hybrid platforms to support scalable, resilient operations and secure data management aligned with local regulations. Regional demand for intelligent workload management is supported by government initiatives encouraging digital infrastructure expansion and technology trade partnerships. Adoption of AI-powered automation within hybrid deployments is gaining traction, aligning with the need for advanced cloud strategies to support operational continuity and cost optimization across mission-critical sectors.

United States – 34.1% market share

High enterprise cloud adoption, advanced digital infrastructure, and strong multi-industry demand are driving dominance in the Hybrid Cloud Management Platform market.

China – 16.8% market share

Strong end-user demand from manufacturing, fintech, and public sectors, coupled with rapid data center expansion, is positioning China as a leader in the Hybrid Cloud Management Platform market.

The Hybrid Cloud Management Platform market features a highly competitive environment with over 60 active global and regional competitors strategically shaping market dynamics through continuous technological advancements, partnerships, and targeted product launches. Leading companies are focusing on developing AI-powered orchestration tools, zero-trust security integrations, and predictive workload management within their platforms to enhance differentiation and address the evolving needs of enterprise clients seeking scalable and secure hybrid solutions. Strategic initiatives such as multi-cloud compatibility enhancements, collaborations with hyperscalers, and regional expansion are central to market players’ positioning strategies, ensuring their platforms remain relevant across diverse industries including BFSI, healthcare, and manufacturing. The market is witnessing increased investment in intelligent automation, edge-cloud integrations, and unified observability solutions as enterprises prioritize seamless data governance and operational efficiency. Mergers and acquisitions are also shaping the Hybrid Cloud Management Platform market, enabling companies to expand technological capabilities and strengthen their regional presence while catering to the rising demand for resilient, scalable, and compliant hybrid cloud infrastructures globally.

IBM Corporation

Microsoft Corporation

VMware Inc.

Cisco Systems Inc.

Hewlett Packard Enterprise (HPE)

Oracle Corporation

BMC Software Inc.

Nutanix Inc.

Citrix Systems Inc.

Micro Focus International plc

The Hybrid Cloud Management Platform market is rapidly evolving through the adoption of AI-powered orchestration, predictive analytics, and automation technologies to optimize multi-cloud and hybrid infrastructure management. Advanced AI and machine learning models are being integrated to enable intelligent workload placement, predictive scaling, and anomaly detection across hybrid environments, significantly reducing manual intervention and improving operational efficiency. Platforms are increasingly leveraging container orchestration technologies such as Kubernetes to streamline application deployment and management, enhancing agility within hybrid environments.

Edge-cloud integration is gaining traction, with platforms supporting real-time data processing at the edge while maintaining centralized visibility and control, meeting the demands of latency-sensitive industries including manufacturing and healthcare. Zero-trust security frameworks and micro-segmentation technologies are being embedded within Hybrid Cloud Management Platforms to secure workloads across complex infrastructures while ensuring regulatory compliance. Automation in cost optimization and policy enforcement is becoming a critical differentiator, with platforms providing granular insights into resource utilization, facilitating advanced capacity planning, and reducing operational expenditures. Additionally, API-driven architecture is enabling seamless interoperability between on-premises systems and public cloud services, addressing challenges in legacy system integration. These technological advancements are collectively driving the Hybrid Cloud Management Platform market toward more scalable, secure, and intelligent infrastructure management solutions for enterprises globally.

• In March 2024, IBM expanded its Hybrid Cloud Management Platform by integrating advanced AI-driven anomaly detection features, reducing unplanned downtime in enterprise hybrid environments by 32% during pilot implementations across critical industries.

• In February 2024, VMware launched an edge-optimized hybrid management solution within its platform, allowing enterprises to manage latency-sensitive workloads with up to 40% faster processing speeds while maintaining unified governance across hybrid infrastructures.

• In September 2023, Microsoft introduced enhanced zero-trust capabilities within its Hybrid Cloud Management Platform, enabling automated micro-segmentation and improved compliance monitoring for organizations managing workloads across multi-cloud environments.

• In May 2023, Cisco announced the integration of advanced predictive analytics into its Hybrid Cloud Management Platform, enabling enterprises to improve capacity planning accuracy by 27% and reduce operational costs through intelligent workload placement strategies.

The Hybrid Cloud Management Platform Market Report comprehensively covers market segmentation by types such as integrated management tools, AI-powered orchestration software, and hybrid monitoring platforms, each facilitating efficient workload distribution and operational optimization across hybrid environments. It evaluates applications across industries including BFSI, healthcare, manufacturing, retail, and public sector organizations, highlighting their adoption patterns and technology integration for digital transformation. The report provides insights into geographic trends across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, detailing regional investments, digital infrastructure advancements, and government initiatives influencing hybrid cloud deployment strategies.

It also covers technological advancements, including AI and machine learning, container orchestration, zero-trust security frameworks, and edge-cloud integrations, focusing on how these innovations are shaping platform capabilities and enterprise decision-making. The report examines end-user categories from large enterprises requiring advanced multi-cloud governance to SMEs adopting hybrid platforms for cost efficiency and operational agility. Additionally, it highlights emerging market areas, such as real-time analytics and hybrid disaster recovery, illustrating how these niche segments are gaining traction. This comprehensive scope ensures decision-makers can effectively evaluate opportunities and challenges in the Hybrid Cloud Management Platform market while aligning technology investments with evolving industry demands and compliance landscapes.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 70637.4 Million |

|

Market Revenue in 2032 |

USD 205780.65 Million |

|

CAGR (2025 - 2032) |

14.3% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

IBM Corporation, Microsoft Corporation, VMware Inc., Cisco Systems Inc., Hewlett Packard Enterprise (HPE), Oracle Corporation, BMC Software Inc., Nutanix Inc., Citrix Systems Inc., Micro Focus International plc |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |