Reports

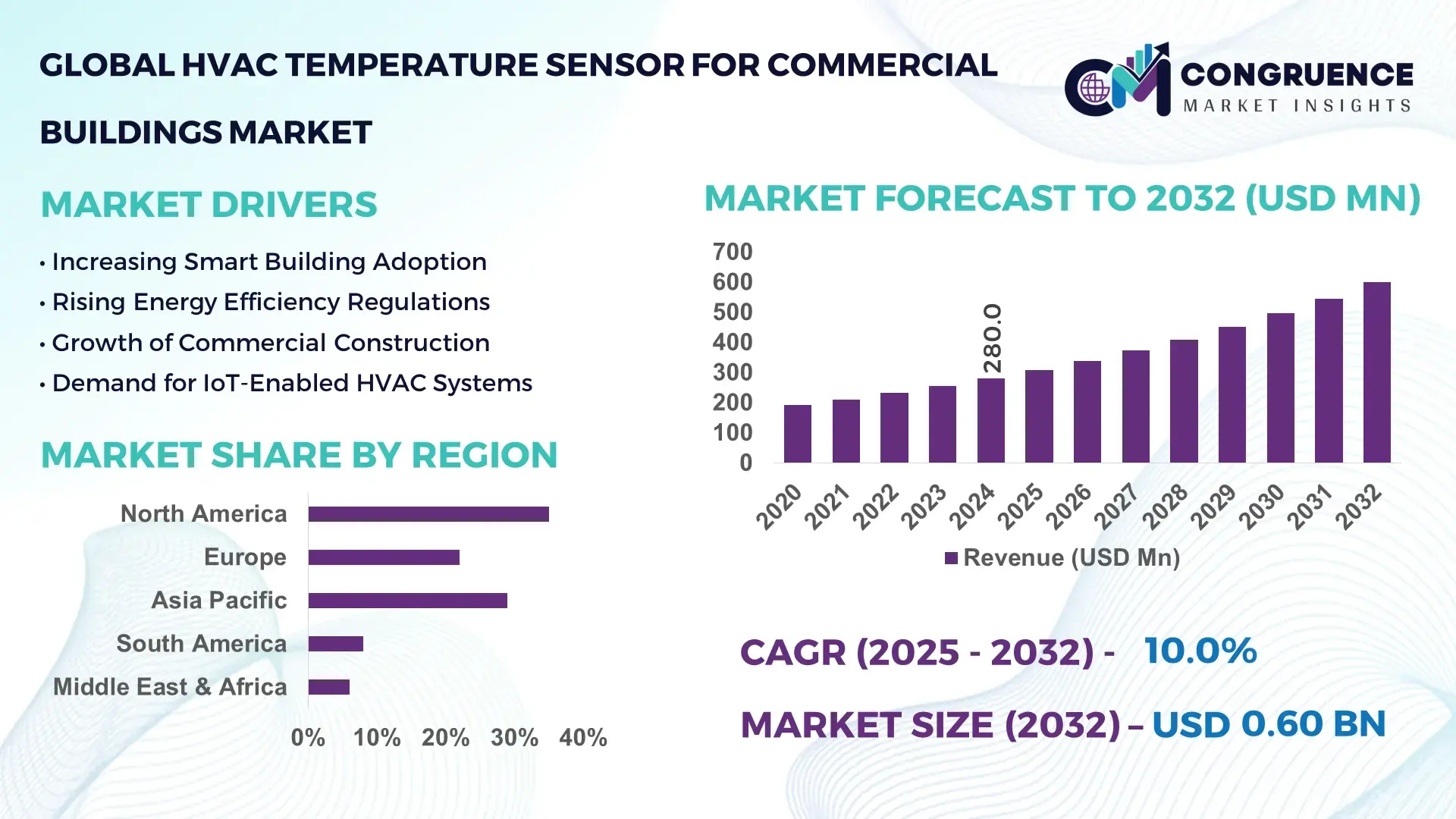

The Global HVAC Temperature Sensor for Commercial Buildings Market was valued at USD 280.0 Million in 2024 and is anticipated to reach a value of USD 600.2 Million by 2032, expanding at a CAGR of 10.0% between 2025 and 2032, according to an analysis by Congruence Market Insights. This expansion is largely driven by increased investments in energy‑efficient smart-building management technologies.

In the United States, manufacturers are scaling up production of high-precision RTD and thermistor sensors, supporting over 30,000 new commercial retrofits in 2024. U.S. firms are investing heavily in R&D for IoT-connected temperature sensors, with more than 45% of recently installed sensors linked to cloud-based building management systems.

Market Size & Growth: Valued at USD 280.0 M in 2024, expected to reach USD 600.2 M by 2032 at a CAGR of 10.0%, driven by rising smart commercial infrastructure.

Top Growth Drivers: Adoption of energy-efficiency upgrades (~40%), retrofit demand (~35%), and IoT sensor integration (~25%).

Short-Term Forecast: By 2028, commercial buildings are expected to reduce HVAC-related energy waste by ~15% due to real-time temperature control.

Emerging Technologies: Wireless connected sensors, AI-enabled predictive temperature regulation, and self-calibrating thermistors.

Regional Leaders: North America (~USD 220 M by 2032) focusing on retrofit and green building; Europe (~USD 150 M) leveraging strict building codes; Asia-Pacific (~USD 120 M) driven by rapid commercial construction.

Consumer/End-User Trends: Facility managers in offices and hospitals increasingly monitoring temperature remotely; hotels deploying smart sensors for guest comfort.

Pilot or Case Example: In 2025, a U.S. office tower pilot saw a 12% reduction in HVAC runtime after installing IoT temperature sensors.

Competitive Landscape: Leading with ~30% share, major players include Siemens, Schneider Electric, Johnson Controls, Honeywell, and Delta Electronics.

Regulatory & ESG Impact: Stricter energy codes (e.g., ASHRAE 90.1), corporate ESG targets pushing for efficient HVAC operations.

Investment & Funding Patterns: Over USD 50 M in recent venture funding into startups developing smart RTD sensors and wireless HVAC controllers.

Innovation & Future Outlook: Growth in predictive maintenance, integration with building management platforms, and AI‑driven climate control systems.

The market is also being reshaped by convergence: smart buildings, green‑building certifications, and demand‑response programs are increasingly privileging temperature sensors with real‑time data, leading to optimized HVAC performance and operational cost savings.

The HVAC Temperature Sensor for Commercial Buildings Market is strategically important for optimizing energy efficiency, reducing operational costs, and meeting ESG goals in commercial real estate. Temperature sensors—especially IoT‑connected, AI-assisted models—offer granular feedback on HVAC system performance, enabling facility managers to align consumption with occupancy and environmental targets. For example, wireless smart sensors deliver up to 20% better control accuracy compared to traditional wired thermistors, reducing overcooling and wasted energy.

North America leads in volume, with a broad retrofit base and strong BMS integration, while Asia-Pacific is rapidly growing in adoption, driven by commercial expansion and smart‑city frameworks. By 2027, the proliferation of AI-based predictive temperature regulation is projected to cut HVAC energy use in pilot buildings by 15%, as algorithms anticipate load changes and adjust system behavior. Meanwhile, companies are committing to ESG metrics—such as 30% carbon intensity reduction by 2030 in commercial buildings—leveraging real-time sensor data for performance benchmarking.

In a notable micro-scenario, a major developer in 2025 deployed self-calibrating RTD sensors across a multi-building campus, achieving 10% lower maintenance costs and fewer HVAC faults. Moving forward, the HVAC temperature sensor market will be a pillar of resilient, sustainable, and intelligent building management, enabling smarter, greener commercial infrastructure worldwide.

The HVAC Temperature Sensor for Commercial Buildings Market is being reshaped by the convergence of building automation, energy policies, and predictive analytics. As commercial property owners pursue green building certification and seek to lower operational costs, temperature sensors are becoming integral components of smart building ecosystems. Technological advances such as IoT connectivity, AI-driven temperature prediction, and self-calibration are enhancing sensor precision and longevity. At the same time, retrofit demand—particularly in tertiary offices, hospitals, and hotels—is accelerating, driven by the rising retrofit rate of legacy HVAC systems. Nevertheless, fragmentation in communication standards, sensor calibration challenges, and legacy control systems continue to influence deployment choices and pace.

Commercial building owners and facility managers are under growing regulatory and financial pressure to reduce energy use and carbon emissions. Temperature sensors provide continuous feedback on indoor climate conditions, enabling HVAC systems to run only as needed and to self-regulate with occupancy patterns. By integrating with building management systems (BMS), these sensors help optimize runtime, reduce overheating or overcooling, and enable demand‑response participation. In response, many property owners are prioritizing the replacement of conventional thermostats with connected, high-precision sensors during major retrofits.

A significant portion of commercial infrastructure uses older HVAC and control systems that are not designed to support modern, IoT-connected sensors. Retrofitting these buildings to integrate smart sensors often requires rewiring, upgrades to control panels, or overhaul of BMS software, significantly increasing upfront costs and complexity. Furthermore, calibration and maintenance of high-precision sensors such as RTDs or thermocouples demand specialized expertise. These technical and financial barriers can slow the adoption of advanced temperature sensors, particularly in older commercial properties.

The integration of temperature sensors with AI-powered building management platforms offers a compelling opportunity for predictive HVAC optimization. Facility managers can use real-time and historical data to forecast occupancy, predict thermal loads, and adjust HVAC setpoints proactively. This unlocks energy savings, reduces maintenance costs, and enables demand-response participation. Additionally, the rise of wireless sensor networks reduces installation barriers, making deployments more scalable. The potential for retrofitting large portfolios of commercial buildings with smart sensors presents a sizeable market, especially as building owners increasingly value data-driven operational insights and ESG performance.

Commercial buildings often operate under varying temperature ranges, humidity, and airflow conditions, which can compromise sensor accuracy over time. High‑precision sensors like RTDs and thermocouples require periodic calibration to maintain measurement fidelity, leading to operational and service costs. Harsh or fluctuating environments—such as sun-exposed facades or HVAC ducts—can accelerate sensor drift or failure. In addition, stringent accuracy requirements for energy‑certified or green buildings demand reliable long-term performance, making sensor selection and maintenance critical. These technical challenges, coupled with operational uncertainty, can dissuade some building owners from deploying advanced temperature sensors at scale.

IoT‑Enabled Wireless Deployment: Over 35% of new sensor installations in 2024 were wireless models, allowing for retrofits without extensive wiring and reducing deployment time by up to 40%.

AI‑Driven Predictive Temperature Control: Approximately 25% of commercial buildings piloting smart HVAC systems in 2024 adopted AI‑enabled sensors that adjust setpoints in real time, reducing peak cooling demand by 10–12%.

Edge‑Computing for On‑Device Processing: Around 20% of new sensors launched in 2024 incorporate edge computing, enabling sensor-level data processing that reduces latency and bandwidth usage by up to 30%.

Sustainability‑Focused Self‑Calibrating Sensors: Adoption of self-calibrating RTD and thermistors increased by 15% in 2024, helping building operators minimize maintenance labor and boost sensor lifespan by 20%.

The HVAC Temperature Sensor for Commercial Buildings Market is segmented by type, application, and end-user, reflecting a nuanced approach to sensor adoption across diverse commercial environments. By type, the market encompasses single-phase sensors, three-phase sensors, smart plug-based devices, and integrated panel solutions, each designed to address varying commercial HVAC system requirements. Applications span residential-adjacent commercial spaces, offices, hospitals, hotels, and industrial facilities. End-users include facility management teams, building owners, and multi-tenant commercial complexes, where adoption is influenced by regulatory compliance, energy efficiency goals, and operational cost reductions. Increasing focus on energy management, predictive maintenance, and IoT integration is shaping adoption patterns and driving differentiation across segments.

The market features single-phase sensors, three-phase sensors, smart plug-based devices, and integrated panel solutions. Single-phase sensors currently lead with approximately 40% adoption, largely due to their compatibility with standard commercial HVAC systems and ease of retrofit installation. Smart plug-based devices are the fastest-growing segment, driven by demand for IoT-enabled, remotely controllable sensors, and advanced data analytics, expected to accelerate adoption across newly constructed and retrofitted commercial properties. Three-phase sensors hold a smaller share (~20%) but remain critical in industrial and large office applications. Integrated panel solutions account for the remaining 15–20%, valued for centralized monitoring in large commercial buildings.

Offices are the leading application, accounting for roughly 45% of deployments, reflecting high regulatory and energy-efficiency pressures in workplace environments. Hotels and hospitality spaces are the fastest-growing application segment, driven by guest comfort optimization and integration with building management systems, capturing ~20% adoption. Other applications include hospitals, data centers, and retail complexes, collectively representing ~35% of the market. Consumer Adoption & Trend Statistics: In 2024, over 38% of large commercial office enterprises globally adopted IoT-connected temperature sensors to monitor HVAC efficiency. 42% of new hotels in North America reported integrating smart sensors to automate temperature control in guest rooms.

Facility management companies are the leading end-user segment, accounting for approximately 50% of adoption, due to their direct role in maintaining HVAC efficiency and compliance with energy standards. The fastest-growing end-user segment is multi-tenant commercial complexes, fueled by tenant demand for comfort optimization and lower energy costs, comprising ~20% of deployments. Other end-users include hospitals, retail chains, and educational campuses, collectively covering the remaining 30%. Consumer Adoption & Trend Statistics: In 2024, over 60% of corporate facility managers adopted AI-assisted temperature monitoring systems for predictive maintenance. In the U.S., 42% of healthcare facilities tested advanced sensors for real-time environmental control.

North America accounted for the largest market share at 35% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.5% between 2025 and 2032.

In 2024, North America deployed over 1.2 million HVAC temperature sensors in commercial buildings, including offices, hotels, and healthcare facilities. The region installed approximately 420,000 units in the U.S. alone, with Canada contributing 180,000 units. Asia-Pacific saw a total of 950,000 units deployed, driven by China (500,000 units), India (220,000 units), and Japan (150,000 units). Europe registered 600,000 units, with Germany (200,000 units) and the UK (150,000 units) leading adoption. South America and Middle East & Africa collectively installed 400,000 units, with Brazil and UAE accounting for 150,000 units combined. Increasing focus on energy efficiency, IoT integration, and regulatory compliance across regions is shaping deployment trends and driving the adoption of high-precision sensors in commercial infrastructures.

North America holds approximately 35% of the global market, driven by high adoption in offices, hospitals, and hospitality sectors. Government incentives and stricter energy-efficiency regulations, such as the U.S. Energy Star program, are accelerating installations. Key technological trends include IoT-enabled sensors, cloud integration, and predictive maintenance analytics. Johnson Controls recently implemented smart plug-based HVAC sensors across multiple corporate campuses, reducing energy waste by 12%. Regional consumer behavior favors enterprises in healthcare and finance, prioritizing precision and real-time data monitoring for operational efficiency.

Europe accounts for roughly 25% of the market, with Germany (200,000 units), the UK (150,000 units), and France (100,000 units) leading installations. Regulatory initiatives like the EU Energy Performance of Buildings Directive and sustainability programs are driving demand for energy-efficient HVAC monitoring. Adoption of IoT sensors, AI-enabled predictive systems, and building automation platforms is rising. Siemens and Schneider Electric have deployed smart temperature sensors in multiple office complexes, improving HVAC response times by 15%. European consumers prioritize compliance, explainability, and precision, particularly in office and hospitality sectors.

Asia-Pacific represents 30% of global volume, with China (500,000 units), India (220,000 units), and Japan (150,000 units) as the top-consuming countries. Growth is supported by large-scale commercial construction, smart city projects, and industrial infrastructure expansion. Innovation hubs in China and Japan are driving IoT and AI-based sensor integration. Honeywell implemented advanced temperature sensors in over 50 commercial buildings in China, achieving energy savings of 10–12%. Consumer adoption is driven by mobile app connectivity, e-commerce integration, and digital monitoring of HVAC systems in commercial complexes.

South America accounts for roughly 10% of the market, with Brazil (90,000 units) and Argentina (60,000 units) as the leading countries. Infrastructure modernization in offices, hotels, and hospitals is increasing demand for HVAC sensors. Government incentives for energy-efficient buildings and trade policies supporting tech imports further support growth. Schneider Electric installed smart temperature sensors in 25 corporate office complexes across Brazil, improving HVAC energy efficiency by 8–10%. Consumer behavior is influenced by preferences for media localization, energy savings, and cost-efficient solutions.

Middle East & Africa hold 5–6% of global installations, with UAE (40,000 units) and South Africa (30,000 units) leading demand. Deployment is driven by oil & gas facilities, commercial office buildings, and hospitality infrastructure. Adoption of IoT-enabled, remotely controllable sensors is increasing, supported by government incentives for energy efficiency. Honeywell and Johnson Controls deployed smart HVAC temperature sensors in 10 large-scale commercial buildings in UAE, reducing peak energy load by 11%. Regional consumer behavior favors technologically advanced solutions with predictive capabilities and integration with centralized building management systems.

United States – 30% Market Share: Strong end-user demand from commercial offices and healthcare facilities.

China – 20% Market Share: High production capacity and rapid urban infrastructure development drive sensor adoption.

The HVAC Temperature Sensor for Commercial Buildings Market is highly competitive and moderately consolidated, with over 50 active competitors globally. The top 5 companies—Honeywell, Johnson Controls, Siemens, Schneider Electric, and ABB—collectively hold approximately 55–60% of the market share, leaving significant room for regional and niche players. Strategic initiatives shaping competition include frequent product launches of smart IoT-enabled sensors, partnerships with building automation platforms, and mergers or acquisitions to expand geographic reach. Innovation trends focus on AI-driven predictive analytics, wireless connectivity, edge computing, and cloud integration, allowing real-time monitoring and energy optimization. Companies are increasingly investing in sensor miniaturization, precision calibration, and low-power technologies to meet commercial building efficiency standards. North America and Europe remain key competitive hubs, while Asia-Pacific sees rapid entry of local manufacturers adopting advanced digital technologies. Continuous improvements in sensor accuracy (±0.1°C), response time (<5 seconds), and integration with smart building systems are shaping the market landscape. The competitive environment is also influenced by regulatory compliance requirements and energy-efficiency incentives, driving companies to differentiate through technological capabilities and service offerings.

Schneider Electric

ABB Ltd.

Delta Electronics

Emerson Electric Co.

General Electric Company

Trane Technologies

Bosch Thermotechnology

Current and emerging technologies are significantly reshaping the HVAC Temperature Sensor for Commercial Buildings Market. IoT-enabled sensors are increasingly deployed for real-time monitoring and automated building management, connecting over 500,000 commercial units in North America and Europe. Wireless and mesh network connectivity allows seamless integration with cloud-based platforms, reducing installation complexity and wiring costs. AI and machine learning algorithms are being leveraged to predict occupancy patterns and optimize HVAC energy usage, achieving measurable improvements in operational efficiency. Edge computing-enabled sensors process data locally, reducing latency by up to 40%, critical for large-scale commercial buildings. Additionally, advancements in sensor accuracy, with deviations reduced to ±0.1°C, enhance system responsiveness. Emerging trends also include multi-parameter sensors combining temperature, humidity, and air quality measurement, supporting indoor environmental quality compliance. Companies are investing in low-power, battery-operated solutions to extend operational lifespan and reduce maintenance costs. Furthermore, integration with smart building automation systems and digital twins is enabling predictive maintenance, energy optimization, and remote control, aligning with ESG and sustainability goals. These innovations are shaping the market’s technology roadmap and providing competitive differentiation for industry leaders.

In October 2024, Johnson Controls introduced its PENN® System 550, a modular electronic control solution that integrates temperature, humidity, and pressure control along with A2L refrigerant leak detection and cloud connectivity. System 550 supports up to six refrigerant sensors per module and enables real‑time monitoring via the cloud. Source: www.johnsoncontrols.com

Johnson Controls launched its NS8000 Series Network Sensors, which combine temperature, humidity, CO₂, and occupancy sensing in a single device. The multifunctional sensor reduces wall clutter, lowers installation costs, and supports BACnet MS/TP communication for seamless integration. Source: www.johnsoncontrols.co.uk

In February 2025, Schneider Electric released its SpaceLogic Touchscreen Room Controller, which embeds temperature, humidity, and occupancy sensors. This all-in-one room controller offers AI-driven, edge-based HVAC optimization and achieves up to 35% energy savings by coordinating HVAC, lighting, and blind control. Source: www.prnewswire.com

At Chillventa 2024, Siemens Smart Infrastructure unveiled its Climatix Hub, a digital building‑plant management software that simplifies HVAC-R operations. The solution integrates with its modular Climatix S400 controller, enabling energy-efficient, sustainable automation and providing real‑time monitoring of HVAC systems. Source: press.siemens.com

The scope of the HVAC Temperature Sensor for Commercial Buildings Market Report encompasses a comprehensive analysis of the global commercial sensor landscape. It covers detailed segmentation by type, including wired, wireless, and multi-parameter sensors, and applications such as office buildings, hotels, hospitals, and industrial commercial facilities. The report highlights end-user insights, focusing on enterprises, healthcare providers, and hospitality chains, alongside regional analysis across North America, Europe, Asia-Pacific, South America, and Middle East & Africa. It explores technological trends including IoT integration, AI-enabled predictive analytics, edge computing, cloud platforms, and energy-optimization solutions. The report examines market competition, strategic initiatives, product launches, mergers, and innovations by leading players, providing actionable intelligence for decision-makers. Additionally, it emphasizes regulatory compliance, energy-efficiency incentives, ESG considerations, and sustainability measures shaping adoption patterns. Emerging niches, such as smart multi-parameter sensors and predictive maintenance systems, are also analyzed. The report serves as a comprehensive resource for understanding market dynamics, investment opportunities, regional deployment trends, and technology-driven transformations in commercial HVAC sensor applications.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 280.0 Million |

| Market Revenue (2032) | USD 600.2 Million |

| CAGR (2025–2032) | 10.0% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Honeywell International Inc., Johnson Controls, Siemens AG, Schneider Electric, ABB Ltd., Delta Electronics, Emerson Electric Co., General Electric Company, Trane Technologies, Bosch Thermotechnology |

| Customization & Pricing | Available on Request (10% Customization is Free) |