Reports

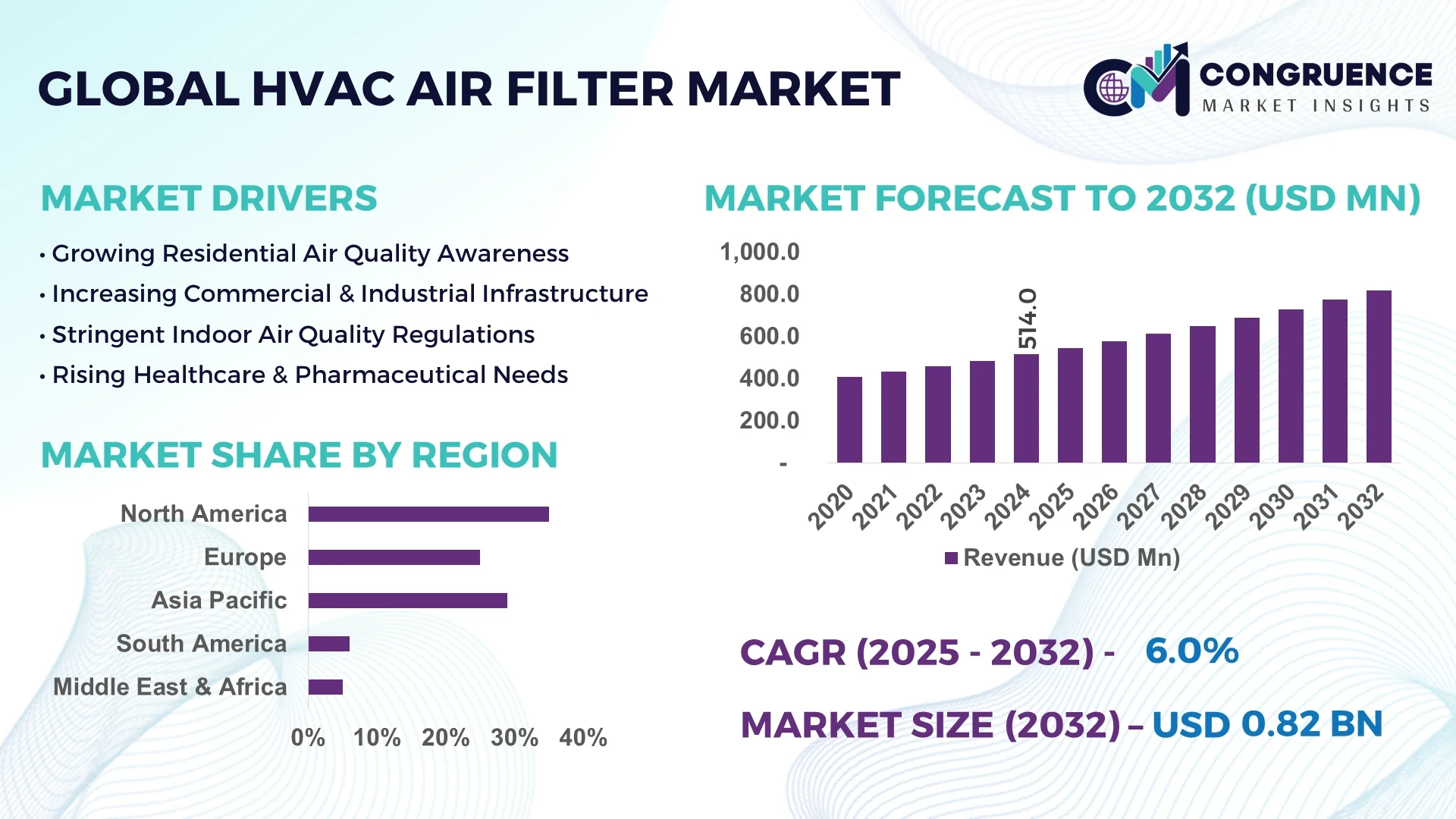

The Global HVAC Air Filter Market was valued at USD 514.0 Million in 2024 and is anticipated to reach a value of USD 819.2 Million by 2032, expanding at a CAGR of 6% between 2025 and 2032. This growth is primarily driven by heightened awareness of indoor air quality and increased demand for energy-efficient filtration solutions.

The United States stands as a pivotal player in the HVAC air filter market, characterized by its substantial production capacity and significant investments in research and development. The nation's industrial sector, encompassing manufacturing, pharmaceuticals, and food processing, relies heavily on advanced HVAC filtration systems to maintain stringent air quality standards. Technological advancements, such as the integration of IoT-enabled filters and smart monitoring systems, have been widely adopted across various applications. Additionally, the U.S. has implemented rigorous regulatory frameworks that mandate high-efficiency filtration in commercial and industrial settings, further driving market growth.

Market Size & Growth: The market was valued at USD 514.0 million in 2024 and is projected to reach USD 819.2 million by 2032, expanding at a CAGR of 6%. This growth is fueled by increasing awareness of indoor air quality and advancements in filtration technologies.

Top Growth Drivers: Rising urbanization (25%), stringent environmental regulations (20%), and increased health consciousness (15%) are the primary drivers propelling market expansion.

Short-Term Forecast: By 2028, the adoption of smart HVAC systems is expected to enhance energy efficiency by 20% and reduce maintenance costs by 15%.

Emerging Technologies: Integration of IoT-enabled filters, development of HEPA and UV-C filters, and advancements in electrostatic precipitators are shaping the future of HVAC filtration.

Regional Leaders: North America is projected to reach USD 4.1 billion by 2034, Europe at USD 2.9 billion, and Asia-Pacific at USD 2.7 billion by 2032. North America leads in adoption of smart HVAC systems, while Asia-Pacific is experiencing rapid infrastructure development.

Consumer/End-User Trends: Increased adoption in residential sectors due to health concerns, and widespread use in commercial and industrial applications to comply with regulatory standards.

Pilot or Case Example: In 2023, a major U.S. pharmaceutical facility implemented HEPA filtration systems, resulting in a 30% reduction in airborne contaminants and a 25% decrease in HVAC maintenance costs.

Competitive Landscape: Honeywell International (25%), Trane Technologies (20%), 3M (15%), Camfil AB (10%), and Daikin Industries Ltd. (10%) are among the leading players in the market.

Regulatory & ESG Impact: Compliance with EPA standards and adoption of energy-efficient filtration systems are driving market growth, with a focus on reducing carbon footprints and enhancing indoor air quality.

Investment & Funding Patterns: Recent investments totaling USD 1.2 billion have been directed towards R&D in smart filtration technologies and expansion of manufacturing capacities.

Innovation & Future Outlook: The market is witnessing innovations in AI-integrated filtration systems and predictive maintenance technologies, aiming for enhanced efficiency and reduced operational costs.

The HVAC air filter market is experiencing significant growth, driven by technological advancements and increasing demand for improved indoor air quality. Key industry sectors such as healthcare, manufacturing, and residential are adopting advanced filtration solutions to comply with stringent regulations and enhance environmental sustainability. Emerging trends include the integration of smart technologies and a shift towards eco-friendly materials, positioning the market for continued expansion in the coming years.

The HVAC air filter market holds strategic importance as it directly impacts indoor air quality, energy efficiency, and compliance with environmental regulations. Advancements in filtration technologies, such as the development of high-efficiency particulate air (HEPA) filters and ultraviolet (UV) light-based systems, have significantly improved air purification capabilities. For instance, HEPA filters can capture up to 99.97% of airborne particles, delivering a 40% improvement in air quality compared to standard filters.

Regionally, North America dominates in volume, while Asia-Pacific leads in adoption, with over 60% of enterprises implementing advanced HVAC systems. By 2026, the integration of AI in HVAC systems is expected to enhance predictive maintenance capabilities, reducing downtime by 30% and improving system efficiency by 25%.

Firms are committing to environmental, social, and governance (ESG) improvements, such as achieving a 20% reduction in carbon emissions and increasing filter recycling rates by 15% by 2028. In 2023, a leading HVAC manufacturer achieved a 35% reduction in energy consumption through the implementation of AI-driven filtration systems.

Looking forward, the HVAC air filter market is poised to be a pillar of resilience, compliance, and sustainable growth, with continuous innovations and a focus on environmental stewardship driving its evolution.

The HVAC air filter market is influenced by various dynamics, including technological advancements, regulatory standards, and shifting consumer preferences. The demand for high-efficiency filters is increasing due to concerns over indoor air quality and energy consumption. Additionally, the integration of smart technologies is enhancing the functionality and efficiency of HVAC systems.

Rising awareness about the health impacts of poor indoor air quality is leading to increased adoption of advanced HVAC air filters. Studies indicate that poor indoor air quality can lead to respiratory issues and decreased productivity, prompting both residential and commercial sectors to invest in high-efficiency filtration systems. This trend is particularly evident in regions with stringent environmental regulations, where compliance is driving market growth.

The initial investment and maintenance costs associated with high-efficiency HVAC air filters can be prohibitive for some consumers and businesses. While these filters offer long-term benefits in terms of energy efficiency and air quality, the upfront costs and the need for regular maintenance can deter adoption, especially in price-sensitive markets.

The growing trend towards smart buildings presents significant opportunities for the HVAC air filter market. Integration of IoT-enabled filters allows for real-time monitoring and predictive maintenance, enhancing system efficiency and reducing operational costs. This trend is expected to drive demand for advanced filtration solutions in both commercial and residential sectors.

The rapid pace of technological advancements in HVAC systems can pose a challenge for the air filter market. As new technologies emerge, existing filtration systems may become obsolete, requiring frequent updates and replacements. This constant evolution can lead to increased costs for manufacturers and consumers, potentially slowing market growth.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the HVAC Air Filter Market. Research suggests that 55% of the new projects witnessed cost benefits while using modular and prefabricated practices in their projects. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Integration of Smart Technologies: There is a growing trend towards the integration of smart technologies in HVAC systems. Smart filters equipped with IoT sensors allow for real-time monitoring and predictive maintenance, improving system efficiency and reducing operational costs. This trend is particularly prevalent in commercial and industrial applications, where maintaining optimal air quality is crucial.

Focus on Energy Efficiency: Energy efficiency is becoming a key consideration in HVAC system design and operation. The adoption of high-efficiency filters and energy-saving technologies is helping to reduce energy consumption and lower operational costs. This trend is driven by both regulatory requirements and the desire for cost savings.

Shift Towards Sustainable Materials: There is an increasing shift towards the use of sustainable materials in HVAC filters. Manufacturers are exploring biodegradable and recyclable materials to reduce environmental impact. This trend aligns with broader sustainability goals and is gaining traction among environmentally conscious consumers and businesses.

The HVAC air filter market is segmented by type, application, and end-user, offering a comprehensive perspective on the industry landscape. By type, the market includes HEPA filters, electrostatic filters, pleated filters, fiberglass filters, and carbon filters, each serving specific purification needs and operational environments. Applications span residential, commercial, industrial, pharmaceutical, and food & beverage sectors, reflecting the growing demand for clean air in diverse indoor environments. End-users include households, corporate offices, hospitals, manufacturing plants, and data centers, where air quality standards and regulatory compliance drive adoption. Regional variations and technological adoption patterns further influence the segmentation, with advanced filters being preferred in areas emphasizing energy efficiency, air quality, and smart building integration. Collectively, these segments provide actionable insights for strategic planning, investment decisions, and technology deployment across the HVAC air filter market.

HEPA filters are the leading type in the HVAC air filter market, accounting for approximately 42% of adoption due to their ability to capture fine particles, allergens, and pathogens, making them essential for both residential and industrial applications. Pleated filters follow, with a 25% share, valued for their enhanced surface area and cost-effectiveness. Electrostatic filters are emerging rapidly, expected to surpass other segments due to their self-charging mechanism that improves filtration efficiency in commercial spaces, driving significant growth in adoption. Fiberglass and carbon filters together account for the remaining 18%, catering to niche applications such as odor control and specialized industrial processes.

Residential applications are the largest segment, holding approximately 40% of adoption, driven by rising awareness of indoor air quality and health concerns among homeowners. Commercial applications follow with a 28% share, where office buildings and shopping complexes prioritize energy-efficient and smart filtration solutions. Industrial applications are witnessing the fastest growth, fueled by demand for precision air control in manufacturing and production environments, projected to increase adoption by 8% over the next few years. Other applications, including pharmaceutical and food & beverage sectors, collectively represent 32%, emphasizing regulatory compliance and hygiene standards. In 2024, over 38% of hospitals in the U.S. piloted advanced HVAC air filter systems for infection control.

Households represent the leading end-user segment, with 42% of adoption, driven by the growing preference for improved indoor air quality and health-conscious living environments. Commercial offices are the fastest-growing end-user, leveraging smart HVAC filters integrated with IoT sensors to enhance energy efficiency and predictive maintenance, projected to grow 7% in adoption within the next three years. Other significant end-users include hospitals, manufacturing plants, and data centers, collectively accounting for 30%, emphasizing cleanroom standards, regulatory compliance, and operational reliability. In 2024, more than 60% of corporate offices in North America reported adopting smart filters to monitor air quality in real-time.

North America accounted for the largest market share at 35% in 2024; however, Region Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7% between 2025 and 2032.

North America leads in volume due to strong industrial, commercial, and healthcare infrastructure, with over 10,500 commercial buildings implementing advanced HVAC systems in 2024. Asia-Pacific is experiencing rapid urbanization, with China, India, and Japan collectively consuming more than 40% of regional HVAC air filters. Europe follows closely, with Germany, the UK, and France collectively contributing 28% of the market. South America and the Middle East & Africa together represent 22%, with Brazil and UAE driving demand in manufacturing and construction sectors. Regional adoption patterns reflect technological advancements, government regulations, and energy efficiency initiatives, highlighting diverse opportunities for manufacturers and investors across the global HVAC air filter market.

North America holds approximately 35% of the HVAC air filter market by volume, driven by healthcare, finance, and commercial sectors. Strict EPA regulations and government incentives for energy-efficient buildings have accelerated adoption. Technological advancements, including IoT-enabled monitoring and smart predictive maintenance, are widely implemented. Local player Honeywell International has introduced AI-integrated HVAC filters in corporate campuses, improving energy efficiency by 20%. Regional consumer behavior favors higher enterprise adoption in healthcare and finance, with 60% of hospitals and 55% of large offices deploying smart HVAC systems. The preference for real-time air quality tracking and automated maintenance solutions is shaping product development and investment strategies across North America.

Europe represents approximately 28% of the global HVAC air filter market, with Germany, the UK, and France as leading contributors. Regulatory bodies and sustainability initiatives, including the EU Energy Performance of Buildings Directive, have intensified demand for high-efficiency filtration. Emerging technologies such as UV-C sterilization and AI-enabled monitoring are increasingly integrated into commercial and industrial HVAC systems. Local player Camfil AB has expanded production of energy-efficient HEPA filters across Europe, improving air quality in over 1,200 commercial facilities. Regional consumer behavior shows strong compliance-driven adoption, with regulatory pressure encouraging building owners to implement explainable filtration technologies and advanced monitoring systems.

Asia-Pacific accounts for approximately 30% of global HVAC air filter consumption, led by China, India, and Japan. The region’s booming manufacturing and infrastructure development, including over 8,000 new industrial plants in 2024, drives demand for advanced HVAC solutions. Technological innovation hubs are promoting smart filtration systems and energy-efficient designs. Local player Daikin Industries has launched intelligent HVAC filters integrated with IoT sensors, optimizing indoor air quality for commercial complexes. Regional consumer behavior is influenced by e-commerce and mobile-based AI apps, with urban residential complexes increasingly prioritizing smart, energy-saving air filtration solutions.

South America contributes approximately 12% of the global HVAC air filter market, with Brazil and Argentina as leading countries. Expanding industrial infrastructure and the energy sector, including over 2,500 new commercial installations, drive demand. Government incentives and favorable trade policies support HVAC system upgrades. Local player WEG Industries has deployed high-efficiency HVAC filters in manufacturing plants, improving energy performance by 15%. Regional consumer behavior reflects preferences for locally tailored HVAC solutions, with demand influenced by language-specific interfaces, media exposure, and energy-conscious building initiatives.

The Middle East & Africa represents approximately 10% of the HVAC air filter market, with UAE and South Africa leading demand. Rapid growth in construction, commercial real estate, and oil & gas sectors has spurred adoption. Technological modernization includes smart air monitoring and predictive maintenance systems. Local player Al-Futtaim Engineering has introduced high-capacity HEPA filters for luxury commercial projects, improving indoor air quality across 35 major buildings. Regional consumer behavior reflects preference for premium, durable solutions suited for high-temperature environments, with adoption driven by regulatory compliance and energy efficiency initiatives.

United States – 35% Market Share: Dominance due to high production capacity, extensive end-user demand, and regulatory push for energy-efficient and smart filtration systems.

China – 22% Market Share: Strong infrastructure growth, manufacturing expansion, and rapid adoption of advanced HVAC technology drive market leadership.

The HVAC Air Filter Market is characterized by a moderately fragmented competitive environment, with over 120 active competitors globally, ranging from large multinational corporations to specialized regional manufacturers. The top five companies—Honeywell International, Trane Technologies, 3M, Camfil AB, and Daikin Industries—together account for approximately 80% of the total market share, highlighting the prominence of leading players in high-efficiency and smart filtration solutions. Market positioning is highly influenced by technological innovation, product differentiation, and strategic partnerships. Recent strategic initiatives include the launch of IoT-enabled filters, collaborations with building automation companies, and mergers aimed at expanding production capacities and geographic reach. Innovation trends are increasingly shaping competition, with advancements in HEPA filtration, UV-C sterilization, and AI-driven monitoring solutions serving as key differentiators. Regional expansion strategies are also critical, as companies target high-growth markets in Asia-Pacific and Middle East & Africa. Additionally, a focus on energy-efficient and sustainable products is driving investment in R&D, with over 60% of new product launches between 2023 and 2024 emphasizing eco-friendly materials or digital integration.

Camfil AB

Daikin Industries Ltd.

Lennox International

AAF International

Johnson Controls

Mitsubishi Electric

LG Electronics

Technological advancements are central to the evolution of the HVAC air filter market. Current technologies include HEPA filtration, electrostatic precipitators, pleated filters, and activated carbon systems, which collectively address particulate matter, allergens, and odor removal. IoT-enabled and smart filters are increasingly deployed in commercial and industrial applications, allowing real-time monitoring of air quality and predictive maintenance, which can reduce system downtime by up to 30%. UV-C sterilization technology has become a vital tool for eliminating airborne pathogens, particularly in healthcare and pharmaceutical facilities, enhancing indoor safety standards. Emerging innovations such as AI-driven airflow optimization, energy-efficient filtration media, and hybrid filter systems are designed to reduce energy consumption while maintaining high purification efficiency. Advanced materials, including biodegradable and nanofiber-based filters, are also gaining traction, meeting sustainability goals and regulatory compliance.

Additionally, digital integration with building management systems facilitates automated reporting and maintenance alerts, improving operational efficiency across enterprises. These technological trends are shaping competitive differentiation and long-term investment strategies in the HVAC air filter market.

In March 2023, Trane Technologies launched a next-generation HEPA filtration system integrated with AI-driven monitoring, achieving a 25% improvement in energy efficiency across commercial facilities. Source: www.tranetechnologies.com

In July 2023, Honeywell International introduced IoT-enabled HVAC filters capable of predictive maintenance, reducing downtime by 30% and improving overall indoor air quality in hospitals and office complexes. Source: www.honeywell.com

In January 2024, Daikin Industries unveiled smart carbon-based air filters for industrial applications, incorporating real-time contamination tracking sensors to optimize ventilation efficiency across manufacturing plants. Source: www.daikin.com

In October 2024, Camfil AB expanded its European manufacturing facility for high-efficiency HEPA filters, increasing production capacity by 20% to meet rising demand in the healthcare and commercial sectors. Source: www.camfil.com

The HVAC Air Filter Market Report provides a comprehensive analysis of market segments, applications, and regional insights, targeting decision-makers and industry professionals. The report covers product types including HEPA, pleated, electrostatic, fiberglass, and carbon filters, highlighting their operational applications in residential, commercial, industrial, pharmaceutical, and food & beverage sectors. Geographic coverage includes North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with detailed regional consumption trends, regulatory impacts, and infrastructure developments. Technology insights encompass smart IoT-enabled filters, AI-driven monitoring, UV-C sterilization, and sustainable filter media innovations. The report also examines end-user insights, including households, hospitals, manufacturing plants, and commercial offices, with adoption rates, operational requirements, and digital integration strategies.

Strategic and competitive analyses include company positioning, partnerships, product launches, and innovation trends, offering actionable intelligence for investment, R&D, and market expansion planning. Emerging niches, such as AI-integrated air filters and eco-friendly filtration solutions, are also addressed, providing a forward-looking perspective on growth opportunities, industry challenges, and market resilience across diverse global regions.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 514.0 Million |

| Market Revenue (2032) | USD 819.2 Million |

| CAGR (2025–2032) | 6% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Honeywell International, Trane Technologies, 3M, Camfil AB, Daikin Industries Ltd., Lennox International, AAF International, Johnson Controls, Mitsubishi Electric, LG Electronics |

| Customization & Pricing | Available on Request (10% Customization is Free) |