Reports

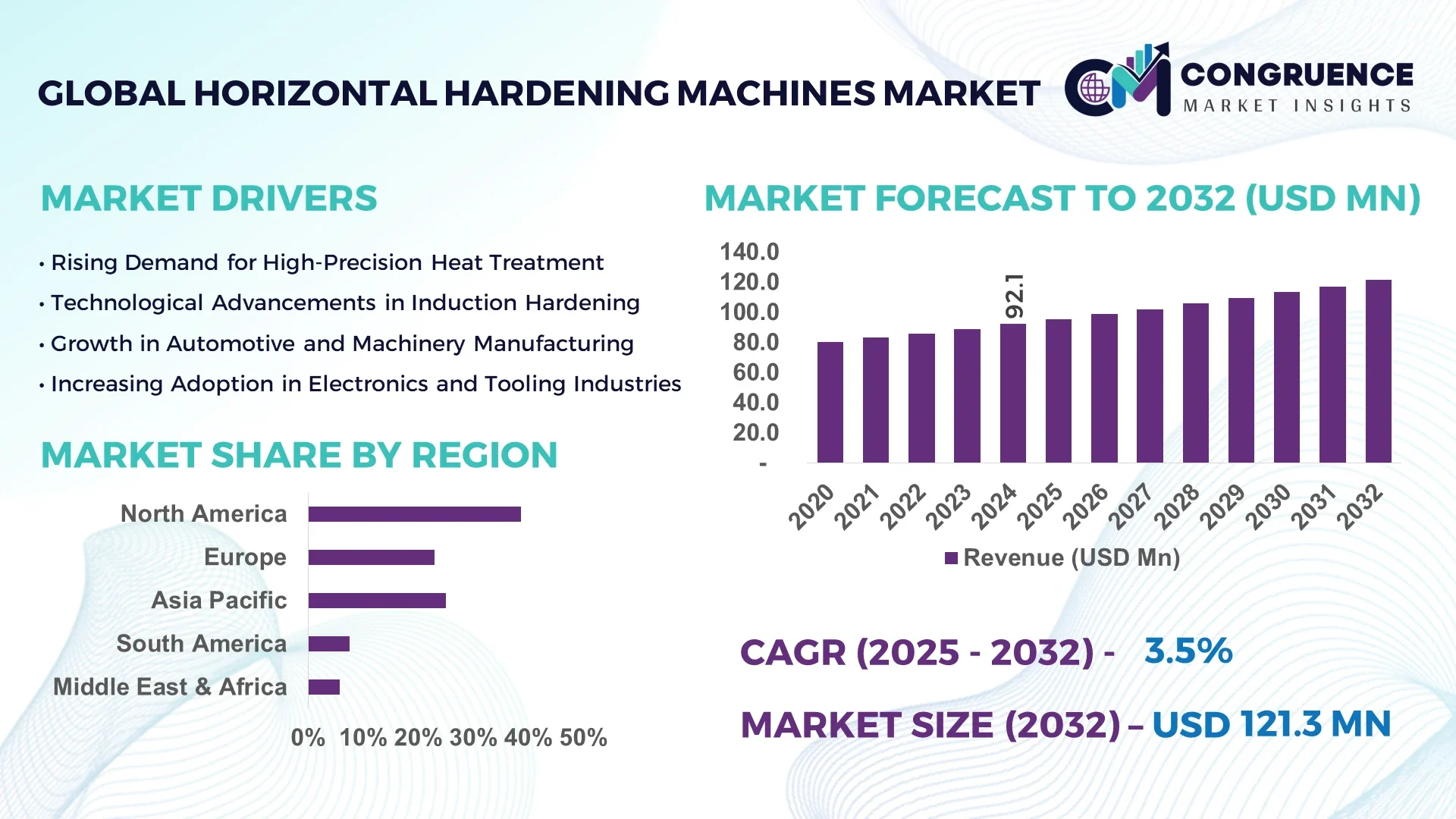

The Global Horizontal Hardening Machines Market was valued at USD 92.11 Million in 2024 and is anticipated to reach a value of USD 121.297 Million by 2032, expanding at a CAGR of 3.5% between 2025 and 2032.

Germany continues to lead in the global horizontal hardening machines landscape, supported by advanced manufacturing infrastructure, significant R&D investments in surface treatment technologies, and widespread integration of hardening systems across the automotive, aerospace, and heavy engineering sectors.

The Horizontal Hardening Machines Market is steadily evolving due to strong adoption in core industrial verticals such as automotive production, energy infrastructure, and high-precision machinery. These sectors demand superior metal hardness, surface strength, and durability, which horizontal hardening machines deliver with precision. Recent innovations such as multi-frequency induction systems, automated quenching stations, and IoT-integrated control panels have improved operational speed, safety, and flexibility. Additionally, regulations emphasizing energy-efficient industrial operations are driving the transition from conventional to smart hardening solutions. Regional demand continues to accelerate, especially in Asia-Pacific, driven by rapid industrialization and an expanding automotive component manufacturing base. Emerging trends include the use of hybrid induction systems, intelligent diagnostics, and robot-assisted part handling, signaling a future where automation, sustainability, and accuracy will define market success.

Artificial Intelligence (AI) is redefining process efficiency and control within the Horizontal Hardening Machines Market. By leveraging AI-driven software, manufacturers are improving real-time decision-making, reducing waste, and enhancing the uniformity of heat treatment processes. Smart algorithms dynamically adjust variables like induction power, quenching time, and coil positioning, allowing highly precise and repeatable hardening cycles. This not only ensures superior product quality but also significantly reduces the need for manual intervention.

In modern facilities, AI-powered computer vision systems inspect every component processed, identifying microscopic surface anomalies and ensuring adherence to required specifications. This level of quality control is crucial in safety-critical sectors such as aerospace and automotive drivetrain manufacturing. Furthermore, AI-enabled predictive maintenance tools monitor wear patterns and sensor feedback in real-time, allowing technicians to schedule servicing before breakdowns occur—minimizing unplanned downtime and extending equipment life.

Another key advancement is the integration of AI-backed digital twins, allowing manufacturers to simulate thermal hardening processes under multiple parameters before execution. This innovation supports optimal energy use, shortens design cycles, and boosts operational agility. With increased adoption of smart factory technologies, the Horizontal Hardening Machines Market is witnessing a shift from reactive to proactive operations, leading to improved consistency, reduced energy bills, and enhanced ROI for industrial heat treatment applications.

“In February 2024, a German-based engineering firm integrated an AI-driven temperature control module into its horizontal hardening machines, resulting in a 27% increase in thermal uniformity and a 19% reduction in energy consumption across pilot production lines in its automotive component division.”

The increasing need for high-durability metal parts in automotive drivetrains, suspension systems, gears, shafts, and heavy-duty industrial tools is a strong growth driver for the Horizontal Hardening Machines Market. Automotive manufacturers are under constant pressure to improve fuel efficiency, which relies on lightweight yet hard-wearing components—achievable through controlled hardening. Similarly, machinery OEMs require hard-faced components to withstand repetitive motion and mechanical stress. Horizontal hardening machines meet these requirements by delivering consistent surface hardness with minimal material distortion. According to recent industry assessments, the average adoption rate of hardening machines in automotive part manufacturing plants has grown by over 15% across North America and East Asia. Additionally, manufacturers are increasingly integrating hardening stations into automated production lines, further amplifying efficiency and output.

Despite their advantages, horizontal hardening machines present significant capital investment challenges, particularly for small and mid-sized enterprises (SMEs). These machines often involve complex cooling systems, high-frequency induction power supplies, and CNC or PLC-based controllers, all of which add to upfront and maintenance costs. Installation and calibration of such systems require skilled labor, which is in short supply in many regions. Furthermore, the need for stable power infrastructure and space-efficient layouts creates additional operational burdens. As a result, adoption among cost-sensitive manufacturers, especially in developing economies, remains limited. Reports from 2024 indicate that over 35% of SMEs in the Asia-Pacific region still rely on traditional or outsourced hardening services due to these financial and logistical constraints.

The rise of Industry 4.0 presents significant opportunities for innovation and efficiency gains in the Horizontal Hardening Machines Market. By integrating hardening machines with smart factory ecosystems, manufacturers can gain access to real-time diagnostics, remote monitoring, adaptive process control, and AI-based performance analytics. These capabilities are not only improving machine uptime but also enabling process transparency and quality consistency across high-volume production runs. Furthermore, cloud-based platforms and IoT sensors are being used to track machine health, predict maintenance needs, and optimize energy consumption, especially in 24/7 industrial environments. Surveys conducted in 2024 show a 22% increase in adoption of smart hardening machines across Western Europe’s manufacturing clusters, signaling growing global interest in digital transformation of surface treatment operations.

One of the key challenges facing the Horizontal Hardening Machines Market is compliance with increasingly strict environmental and energy efficiency regulations. Induction-based hardening processes, while more efficient than traditional furnaces, still consume substantial electricity and emit localized heat, which must be managed responsibly. Governments in Europe, North America, and parts of Asia are enforcing tighter rules around industrial energy use, emissions, and cooling fluid disposal. Adhering to these regulations requires machine redesigns, higher upfront costs for eco-efficient technologies, and increased documentation and compliance audits. This regulatory pressure particularly affects older hardening systems that lack modern control mechanisms, forcing manufacturers to invest in upgrades or face operational penalties, thus complicating ROI calculations.

• Rise in Modular and Prefabricated Construction: The growing popularity of modular and prefabricated building techniques is driving measurable demand for horizontal hardening machines in off-site metal fabrication processes. In Europe and North America, builders are increasingly using pre-engineered components to minimize on-site labor and reduce construction timelines. Horizontal hardening machines play a pivotal role in heat-treating structural steel parts, brackets, and frame connectors to meet stringent mechanical requirements. Automated hardening solutions are now preferred in prefab production lines, improving output by up to 28% and reducing rework ratios in high-volume applications.

• Adoption of Multi-Frequency Induction Systems: Manufacturers are transitioning from single-frequency to multi-frequency induction hardening machines to gain more process control and improve metallurgical outcomes. Multi-frequency systems allow customized heating patterns that match complex part geometries, improving hardness consistency and reducing cycle time by up to 22%. This shift is particularly prominent in the production of precision components like gears, axles, and camshafts. Increased flexibility in programming and frequency tuning is making these machines ideal for high-mix, low-volume operations.

• Integration of Human-Machine Interfaces (HMI): Horizontal hardening machines are increasingly being outfitted with advanced Human-Machine Interfaces (HMI) that support intuitive controls, real-time analytics, and operator safety. This trend reflects a broader industry move toward user-centric design and automation. Machines equipped with touchscreen HMIs and visual feedback systems have improved throughput by up to 19% in automated lines, while also enabling rapid training and error reduction in industrial settings.

• Growth in Custom Hardening Solutions for Lightweight Alloys: There is a notable rise in the use of aluminum, titanium, and hybrid metal alloys in industries like aerospace and electric vehicle manufacturing. These materials require customized heat treatment protocols, prompting manufacturers to develop specialized horizontal hardening machines with tailored induction coils and adjustable quenching mechanisms. Demand for such machines has risen by over 30% in lightweight mobility component manufacturing hubs across East Asia and North America.

The Horizontal Hardening Machines Market is segmented based on type, application, and end-user industries, each playing a vital role in defining the demand landscape. By type, the market includes single-frequency and multi-frequency machines, as well as CNC-based models and portable hardening systems. In terms of application, the market serves automotive parts, machinery components, defense systems, construction tools, and energy infrastructure. From an end-user perspective, the key industries leveraging horizontal hardening solutions include automotive manufacturing, aerospace & defense, heavy equipment OEMs, and general fabrication shops. Each of these segments is influenced by specific requirements around surface hardness, heat treatment cycle speed, and part geometry, driving tailored innovation across the product and service spectrum.

The multi-frequency horizontal hardening machines lead this segment due to their ability to handle complex component geometries and offer adaptable heating profiles. These machines have become the preferred choice in automotive and aerospace sectors, where part precision and consistency are critical. Their ability to reduce processing time while improving microstructure quality makes them highly efficient for industrial-scale operations. The fastest-growing segment is CNC-integrated horizontal hardening machines, driven by the demand for automated, precise, and repeatable hardening processes. As manufacturers pursue leaner workflows, CNC-based models offer programmable control, reducing setup time and human error. They are especially popular in high-throughput environments that demand zero-defect production. Other types, such as single-frequency machines and portable hardening systems, maintain relevance in cost-sensitive or specialized applications. Single-frequency units are commonly used in low-volume workshops, while portable systems are suitable for on-site hardening needs, particularly in construction and maintenance sectors.

The automotive components application dominates the Horizontal Hardening Machines Market, owing to the volume of gears, shafts, axles, and bearings that require uniform surface hardening for durability and performance. Horizontal hardening machines are widely implemented in production lines to ensure consistent thermal treatment of drivetrain parts and steering components, where strength is non-negotiable. The fastest-growing application is electric mobility and EV component hardening, where lightweight alloy parts need precise induction hardening to improve structural integrity. The push for electrification has increased demand for hardened motor components, battery connectors, and precision assemblies, all of which benefit from advanced horizontal hardening processes. Other significant application areas include industrial machinery parts, where wear resistance is essential, and defense equipment, where high-impact durability is critical. Additionally, construction tools and heavy-duty fasteners are also increasingly treated using horizontal hardening technologies to meet evolving mechanical performance standards.

The automotive manufacturing sector stands as the leading end-user in the Horizontal Hardening Machines Market. High volumes of critical drivetrain and powertrain components are continuously processed using hardening machines to meet durability and safety benchmarks. The demand for high-speed, energy-efficient machines with automation compatibility is particularly strong among Tier-1 suppliers. The fastest-growing end-user is the aerospace and defense industry, which requires hardened parts made of specialized alloys that perform under extreme mechanical stress. Recent investments in defense procurement and aircraft manufacturing have increased the need for high-precision hardening solutions capable of processing small-batch, high-spec components. Other notable end-users include heavy machinery OEMs, especially in agriculture and mining, where hardened structural parts improve operational reliability. General metal fabrication workshops and custom component manufacturers also contribute to the market, particularly through demand for compact, versatile machines that support job-shop and prototyping needs.

Asia-Pacific accounted for the largest market share at 38.7% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 4.1% between 2025 and 2032.

Asia-Pacific continues to dominate the global Horizontal Hardening Machines Market owing to its expansive manufacturing base and rising industrial automation in countries like China, India, and Japan. China, in particular, leads in volume due to large-scale production facilities catering to automotive, construction, and energy industries. Regional growth is also propelled by government-backed smart manufacturing initiatives and robust export demand. Meanwhile, North America is rapidly accelerating in adoption due to its strong push toward automation, high investment in AI-integrated hardening technologies, and presence of Tier-1 automotive suppliers shifting toward precision and energy-efficient manufacturing equipment.

Digital automation shaping thermal treatment technologies

In North America, the Horizontal Hardening Machines Market held a 22.6% share in 2024, driven predominantly by demand across the automotive and aerospace sectors. The rise of electric vehicle manufacturing and aerospace component hardening has accelerated adoption, particularly in the U.S. and Mexico. Government incentives promoting advanced manufacturing, especially under clean energy initiatives and reshoring policies, are further fueling demand. Additionally, advancements in machine learning and digital twin technologies are transforming the region’s hardening processes, enabling predictive maintenance and energy-efficient workflows. Regulatory focus on reducing industrial emissions has also led to increased investment in closed-loop and eco-friendly thermal processing systems.

Smart induction systems driving precision metallurgy

Europe captured approximately 19.8% of the Horizontal Hardening Machines Market in 2024, with Germany, France, and the UK being the primary contributors. The region’s emphasis on sustainable manufacturing, guided by regulatory frameworks such as the EU Green Deal and REACH compliance, is encouraging the use of energy-optimized and environmentally friendly machines. Advanced automation and AI integration are being widely adopted across European production lines to enhance precision and reduce energy consumption. Furthermore, Germany’s dominance in high-tech machinery manufacturing and France’s push for digital transformation in industrial sectors are reshaping demand patterns across the continent.

Rising industrialization fueling demand for heat treatment automation

Asia-Pacific leads the Horizontal Hardening Machines Market by volume, with countries like China, Japan, South Korea, and India accounting for over 38.7% of global demand in 2024. China remains the highest consumer, supported by strong domestic manufacturing and exports of heavy machinery, automotive components, and industrial equipment. India and Southeast Asia are emerging as new hotspots for investment due to their infrastructure boom and government-led industrial automation initiatives. The region is also home to major innovation hubs in robotics and IoT integration, enhancing the functionality and adaptability of horizontal hardening equipment in localized and export-driven markets.

Infrastructure development ignites demand for precision hardening equipment

South America represented 7.2% of the Horizontal Hardening Machines Market in 2024, led by Brazil and Argentina. Growth in construction, mining, and agricultural machinery sectors is driving the use of horizontal hardening machines for structural steel and component hardening. In Brazil, federal incentives and increasing foreign investments in manufacturing infrastructure are catalyzing modernization across fabrication units. Meanwhile, Argentina’s focus on improving its industrial productivity is spurring demand for technologically advanced, yet cost-effective, hardening equipment. Regional trade agreements and reduced import duties for automation systems are further strengthening the outlook.

Oil sector expansion and manufacturing evolution fuel market momentum

The Middle East & Africa held 6.4% of the Horizontal Hardening Machines Market in 2024, with the UAE and South Africa at the forefront of growth. In the UAE, strong demand from the oil & gas sector for hardened drilling and pump components is boosting investment in advanced thermal treatment equipment. South Africa’s growing mining and industrial sectors are also driving machine adoption. The regional market is witnessing modernization, with digital automation being introduced in legacy facilities. Local regulatory bodies are encouraging technology transfer and partnerships to elevate manufacturing capabilities in alignment with Vision 2030 and similar national development goals.

China – 23.5% Market Share

Strong end-user demand across automotive and machinery manufacturing, combined with large-scale production infrastructure.

United States – 18.1% Market Share

High production capacity and rapid adoption of AI-integrated horizontal hardening technologies in aerospace and industrial sectors.

The Horizontal Hardening Machines Market features a moderately consolidated competitive landscape with over 45 active global and regional manufacturers offering varying capabilities in machine design, automation integration, and thermal processing precision. Leading players in this market have been investing heavily in product innovation and smart manufacturing technologies, particularly focusing on AI-driven process optimization, digital twin applications, and energy-efficient hardening systems. Companies are increasingly differentiating themselves through customizable hardening solutions for complex geometries and high-throughput operations in industries such as automotive, construction, and aerospace.

Strategic initiatives like multi-national partnerships, localized manufacturing expansions, and technology licensing agreements have intensified competition. Notably, the past two years have witnessed several key mergers and acquisitions aimed at expanding product portfolios and entering untapped regional markets. In addition, manufacturers are integrating real-time data analytics and cloud-based process monitoring features into their horizontal hardening machines to meet Industry 4.0 compliance standards. Competitive dynamics are further influenced by service excellence, after-sales support, and turnkey installation offerings which are becoming key value propositions for buyers seeking long-term operational reliability.

EMA Indutec GmbH

Aichelin Group

EFD Induction

Nabertherm GmbH

Inductoheat Inc.

ELTA Group

GH Induction Atmospheres

HeatTek Inc.

Shenzhen Hengjin Automation Co., Ltd.

SMS Elotherm GmbH

Ajax TOCCO Magnethermic

SAET Group S.p.A.

Technological innovation is rapidly transforming the Horizontal Hardening Machines Market, particularly through integration of advanced control systems, AI-based process monitoring, and energy-efficient heating technologies. One of the most significant developments is the implementation of adaptive induction heating systems, which automatically adjust energy output based on component geometry and material properties. This ensures uniform hardness and minimizes energy waste, contributing to more sustainable operations.

In addition, digital twin technology is being adopted to simulate heat treatment cycles before physical application. This reduces trial-and-error phases in new product development, shortens production time, and enhances quality assurance. Sensors embedded within the machines allow real-time monitoring of temperature, cycle duration, and material stress levels, enabling predictive maintenance and reducing machine downtime by up to 30%.

Robotics and machine learning algorithms are also influencing automation in handling components, ensuring consistent loading/unloading and cycle repeatability. Moreover, many new horizontal hardening machines now support IoT-enabled remote diagnostics, enabling centralized management across multiple facilities. The shift toward modular machine design has allowed customization for specific industrial use cases, such as gear shafts, axles, and structural bars, especially in the automotive and heavy machinery sectors. These innovations are collectively improving efficiency, quality, and sustainability within heat treatment processes.

• In February 2023, EMA Indutec launched a new line of high-frequency horizontal hardening machines equipped with AI-based thermal profiling. This system improved temperature consistency by 18% across various workpiece diameters, enhancing metallurgical properties in high-precision automotive components.

• In August 2023, SMS Elotherm GmbH introduced a compact hardening machine model for mid-sized production lines. This unit integrates closed-loop cooling and real-time data logging, resulting in a 25% reduction in energy consumption during continuous operations.

• In March 2024, GH Induction Atmospheres unveiled its cloud-enabled control platform compatible with existing horizontal hardening machines. This update enabled remote diagnostics, predictive alerts, and performance tracking, reducing unplanned maintenance incidents by 40%.

• In May 2024, Inductoheat Inc. expanded its Michigan plant with new robotics-assisted hardening lines. These lines feature synchronized gantry systems that improve part throughput by 35%, particularly benefiting the demand for heavy truck drivetrain components.

The Horizontal Hardening Machines Market Report provides a comprehensive evaluation of the global landscape across various technological, industrial, and geographic dimensions. It examines in detail the integration of automation, AI-driven controls, and IoT functionalities that are shaping next-generation hardening equipment. The report covers machines tailored for horizontal induction hardening processes, widely used in treating cylindrical or shaft-type components across sectors like automotive, aerospace, railway, energy, and heavy machinery. This report offers an in-depth analysis of core product types such as high-frequency, medium-frequency, and dual-frequency machines. It further segments the market by application, highlighting use cases in gear hardening, axle hardening, crankshaft treatment, and precision tool manufacturing. Each segment is evaluated based on production volume, adoption rate, and operational preferences across industries. Technological transitions—including the rise of digital twin simulation, real-time thermal control systems, and smart factory integrations—are mapped out with regional implementations.

Regionally, the report includes data and insights from North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, tracking demand surges driven by industrial modernization, local manufacturing growth, and evolving infrastructure projects. Special focus is given to high-growth countries and niche markets that are rapidly adopting horizontal hardening solutions due to favorable regulatory conditions and rising demand for durable, precision-engineered metal parts. Overall, the report equips stakeholders with the data necessary to assess market opportunities, competitive positioning, technological readiness, and geographic expansion potential across the global Horizontal Hardening Machines industry.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 92.11 Million |

|

Market Revenue in 2032 |

USD 121.297 Million |

|

CAGR (2025 - 2032) |

3.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Heraeus Noblelight GmbH, GEW (EC) Limited, Vulcan Catalytic Systems, Fannon Products, LLC, Eltosch Grafix GmbH, Emit Inc., Solaronics Inc., Casso-Solar Technologies LLC, Red-Ray Manufacturing Company, BBC Industries, Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |