Reports

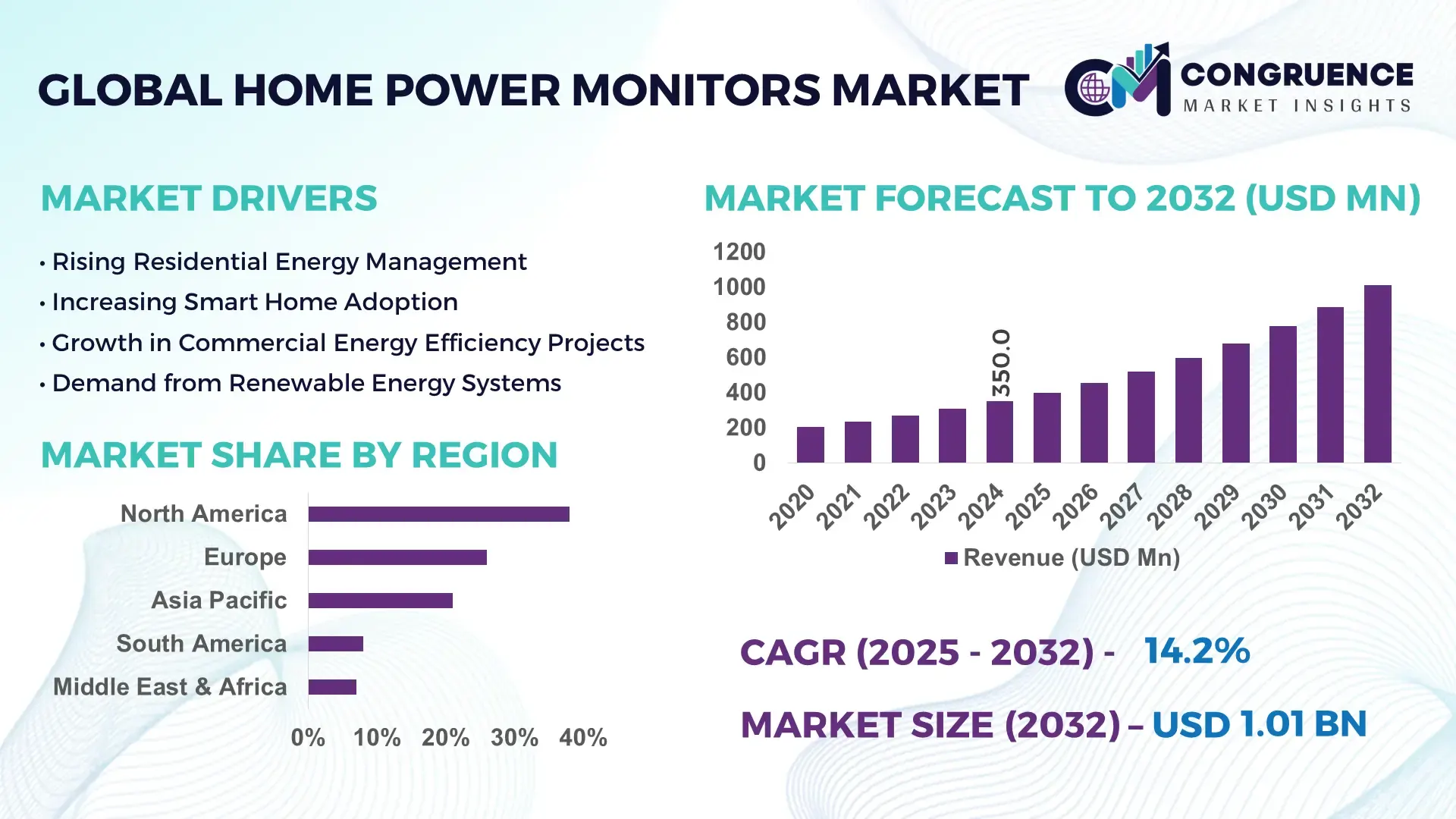

The Global Home Power Monitors Market was valued at USD 350.0 Million in 2024 and is anticipated to reach a value of USD 1,012.5 Million by 2032, expanding at a CAGR of 14.2% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is primarily driven by rising residential energy‑efficiency initiatives and increasing consumer demand for real‑time electricity consumption insights.

In the United States, the home power monitor market benefits from advanced production capacity with over 200,000 new HEMS (Home Energy Management Systems) shipped in 2024. High investment in IoT‑enabled devices and strong consumer adoption have resulted in about 0.6% of US homes having such systems installed by end‑2024.

Market Size & Growth: Valued at USD 350.0 M in 2024, forecast to reach USD 1,012.5 M by 2032, with a CAGR of 14.2% — driven by increasing energy‑efficiency awareness.

Top Growth Drivers: Adoption of smart homes increasing by ~40%, residential energy efficiency demand up ~35%, and IoT integration growth of ~30%.

Short-Term Forecast: By 2028, average consumer electricity‑bill savings from monitors are expected to improve by ~20% due to enhanced real‑time analytics.

Emerging Technologies: IoT-based real-time monitoring, AI-driven energy usage prediction, and cloud‑connected analytics platforms.

Regional Leaders: North America: projected to reach ~USD 400 M by 2032, driven by high smart‑home penetration; Europe: expected to hit ~USD 300 M by 2032 with strong retrofit adoption; Asia Pacific: forecast ~USD 250 M by 2032, fueled by rapid urbanization and energy‑management policies.

Consumer / End-User Trends: Predominant use by residential homeowners, with increasing adoption in multi‑family dwellings and retrofit markets; usage peaks during peak‑load hours.

Pilot / Case Example: In 2025, a US pilot saw households using home power monitors reduce peak‑hour consumption by 15%, cutting system stress.

Competitive Landscape: Market leader holds ~25% share, followed by major players such as Schneider Electric, Siemens, Honeywell, Sense, and Eaton.

Regulatory & ESG Impact: Incentives for energy‑saving devices, net‑zero carbon targets, and mandatory energy‑audit regulations in several countries boost adoption.

Investment & Funding Patterns: Over USD 120 M raised in venture funding in 2024 by smart‑monitor startups; increasing green bonds for home energy infrastructure.

Innovation & Future Outlook: Integration with home automation systems, predictive maintenance using AI, and next-gen monitors with disaggregation capabilities for individual appliances.

The market is also seeing growing convergence: rising demand from residential, commercial, and industrial segments; smart‑meter and energy‑monitor product innovations; stringent energy regulation; and regional adoption patterns are accelerating the shift toward real-time energy tracking, demand-response, and predictive energy analytics.

The strategic relevance of the Home Power Monitors Market lies in its ability to align residential energy use with broader sustainability and efficiency goals. Home power monitors, especially when embedded within smart home systems, provide granular visibility into power consumption, enabling both behavioral shifts and technological optimizations. For instance, adoption of AI‑augmented monitors delivers roughly 30% better forecasting accuracy compared to older, non‑AI‑enabled devices, helping households proactively shift or reduce load during peak times.

North America dominates in volume, with high installation rates, while Asia Pacific leads in user adoption growth, fueled by urbanization and government energy‑efficiency mandates. By 2027, cloud‑based analytics is expected to reduce household electricity wastage by 15%, as machine‑learning models optimize appliance usage and alert users to anomalies. At the same time, firms are committing to ESG goals—for example, targeting a 20% reduction in household carbon footprint by 2030 via real‑time energy tracking and optimization.

Micro‑scenario: In 2025, a US-based utility company piloted smart monitors with embedded AI, resulting in a 12% reduction in peak-load consumption across participating homes. This demonstrates how tech-led energy monitoring can drive tangible system-level resilience.

Going forward, the Home Power Monitors Market is poised to become a pillar of resilient, compliant, and sustainable growth, enabling deeper grid‑consumer integration, enhancing demand‑response strategies, and supporting global decarbonization targets.

The Home Power Monitors Market is witnessing robust transformation driven by a convergence of energy efficiency, consumer empowerment, and regulatory pressure. As residential electricity costs rise and environmental awareness deepens, homeowners increasingly demand real-time insight into their power usage. Technological advances—particularly in IoT, AI, and cloud analytics—are enabling smarter, more affordable monitors that not only report usage but also predict consumption trends, detect anomalies, and integrate with other home automation systems. Furthermore, incentives from governments and utilities for demand‑response participation and net-zero targets are accelerating deployment. However, fragmentation in communication protocols, data privacy concerns, and uneven adoption across geographies continue to shape the competitive and innovation landscape.

Governments and utilities are pushing more stringent energy‑efficiency regulations and incentivizing smart energy devices, which in turn propels demand for home power monitors. These devices help homeowners comply by offering real-time visibility into electricity consumption patterns, optimizing appliance use, and enabling participation in demand-response programs. As a result, consumer adoption of energy-monitoring hardware has accelerated, supported by rebate schemes and tax incentives. Additionally, utilities leverage aggregated monitoring data to balance load and reduce grid strain during peak hours, making monitors strategically valuable for both consumers and providers.

While home power monitors collect detailed energy-use data, many consumers remain wary of data security risks and how their usage patterns could be shared or monetized. This concern is compounded by interoperability issues: different devices may use disparate communication protocols (Wi‑Fi, Zigbee, PLC), making integration with existing smart-home ecosystems cumbersome. As a result, potential buyers may delay purchasing, and manufacturers must invest heavily to ensure secure data encryption, open APIs, and compatibility across platforms. These technological and trust-related barriers can slow the broad adoption of power-monitoring solutions.

Home power monitors are uniquely positioned to capitalize on the integration of residential renewable energy systems (like rooftop solar) and battery storage. By providing real-time, granular usage data, these monitors help homeowners optimize self-consumption, decide when to charge or discharge storage, and even trade surplus energy via peer-to-peer or utility programs. Additionally, as electric vehicles (EVs) proliferate, power monitors can manage EV charging based on consumption forecasts and tariff signals, maximizing cost savings. This convergent play opens new business models for manufacturers and service providers, such as predictive load balancing and energy-as-a-service offerings.

Many home power monitors require significant initial capital investment, particularly when installed at the electrical panel or integrated into broader energy systems. This upfront cost can deter price-sensitive consumers, especially in regions where electricity is relatively inexpensive. Moreover, some homeowners exhibit inertia: they may not perceive enough value in granular energy data, or they may lack the technical comfort to interpret and act on it. Without simplified user interfaces, clear ROI, and compelling behavioral incentives, adoption may slow. Manufacturers must therefore focus on lowering costs, improving usability, and clearly communicating long-term savings to overcome these barriers.

Modular and Prefabricated Construction Integration: The rise of modular construction is driving demand for integrated power-monitor solutions. In 2024, approximately 55% of modular housing projects reported cost savings by embedding energy monitors during off‑site fabrication, reducing installation complexity and labor costs.

AI‑Driven Disaggregation: More than 40% of new power monitor models now leverage machine learning to disaggregate appliance-level usage with ±10% accuracy, helping homeowners identify energy-hogging devices.

Cloud‑Edge Analytics Adoption: Nearly 30% of deployments now include cloud‑based analytics platforms that provide real‑time alerts and trend forecasting, enabling proactive energy-saving behaviors.

Regulatory-Enabled Demand-Response Participation: Utilities in North America and Europe have conducted pilots showing homes with smart power monitors can shift up to 20% of peak load, enabling stronger demand-response programs and grid resiliency.

The Home Power Monitors Market is strategically segmented based on type, application, and end-user to provide clarity on adoption patterns and performance optimization across residential and commercial settings. By type, the market includes single-phase monitors, three-phase monitors, smart plug-based devices, and integrated panel solutions, allowing decision-makers to match technology with specific energy management requirements. Application segmentation focuses on residential usage, commercial buildings, industrial setups, and renewable energy systems, highlighting varying operational demands and energy‑efficiency strategies. End-user segmentation captures households, multi-family complexes, offices, and industrial facilities, reflecting differences in consumption behavior, installation scale, and monitoring sophistication. Insights indicate that residential segments benefit from real-time energy analytics, commercial sectors leverage automated demand-response capabilities, and industrial users focus on operational efficiency. Combined, these segments provide stakeholders with actionable intelligence to optimize investments, enhance energy savings, and prioritize technology deployment based on usage patterns, regional adoption trends, and device compatibility.

Single-phase monitors currently lead the market, accounting for approximately 38% of adoption, largely due to their ease of installation, affordability, and suitability for most residential settings. Three-phase monitors follow with 27%, offering higher precision and reliability for larger homes and small commercial units. Smart plug-based devices hold 20%, providing flexibility for appliance-specific tracking and energy reporting, while integrated panel solutions account for 15%, offering advanced analytics and multi-circuit monitoring for sophisticated setups. Notably, adoption of integrated panel solutions is rising fastest due to growing demand for centralized energy management across multiple circuits and IoT-enabled automation.

Residential applications dominate the Home Power Monitors Market, representing approximately 45% of total adoption, driven by increasing consumer awareness of energy efficiency and cost savings. Commercial building applications hold 30%, leveraging monitors for operational cost control and demand-response participation. Industrial and renewable energy integrations collectively account for 25%, supporting process optimization and grid integration. The fastest-growing application segment is renewable energy systems, fueled by rising rooftop solar adoption and distributed storage management. Consumer trends show that in 2024, over 42% of households in North America and Europe installed smart monitors to optimize energy consumption during peak hours. Additionally, in the US, 38% of commercial office buildings piloted energy-monitoring devices to manage HVAC and lighting systems.

Households remain the leading end-user segment with 50% market adoption, reflecting high awareness of energy efficiency and the growing affordability of plug-and-play monitors. Multi-family residential units account for 22%, offering centralized energy management for shared facilities. Office and commercial facilities contribute 18%, leveraging monitoring to manage operational costs and compliance with energy audits. Industrial end-users represent 10%, focusing on process efficiency and integration with renewable energy sources. The fastest-growing end-user segment is industrial facilities, as smart energy monitoring supports predictive maintenance and reduces operational downtime. Consumer trends reveal that over 60% of homeowners in urban North America are now using monitors to track appliance-level energy use. Additionally, in Europe, 42% of SMEs implemented energy monitoring solutions to optimize electricity consumption.

North America accounted for the largest market share at 38% in 2024, however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 14.2% between 2025 and 2032.

North America’s dominance is supported by over 200,000 units shipped in 2024, high smart-home adoption, and advanced IoT infrastructure. Asia Pacific’s growth is fueled by urbanization, rising electricity demand, and government-backed renewable energy initiatives. Europe holds 28% share, driven by Germany, the UK, and France, with strong regulatory mandates for energy efficiency. South America represents 12%, primarily Brazil and Argentina, focusing on retrofit installations and energy-cost optimization. Middle East & Africa account for 10%, supported by smart-city projects and digital modernization in UAE and South Africa. Consumer adoption patterns vary regionally, with North America emphasizing enterprise integration, Europe focusing on compliance and sustainability, and Asia-Pacific on mobile-enabled monitoring.

North America accounts for 38% of the global market, driven by residential and commercial sectors, including healthcare, finance, and multi-family dwellings. Regulatory support, such as energy-efficiency tax incentives and utility rebate programs, has accelerated adoption. Technological advancements include IoT integration, AI-driven load forecasting, and cloud-based analytics platforms for remote monitoring. Local players such as Sense have deployed smart panel monitors in over 50,000 households, improving energy visibility and peak load reduction. Consumer behavior shows higher adoption in urban households, with growing interest in plug-and-play devices and demand-response participation, while commercial facilities prioritize energy auditing and cost optimization.

Europe holds approximately 28% of the market, with Germany, UK, and France as leading contributors. Strong regulatory frameworks and sustainability initiatives have fostered demand for explainable and compliant home power monitors. Emerging technologies include AI-enabled disaggregation, cloud-based energy analytics, and smart plug devices for residential and small commercial applications. Players like Schneider Electric are enhancing IoT-enabled panels for distributed energy management. Consumer behavior varies, with homeowners and commercial enterprises emphasizing compliance with EU energy directives, peak-load management, and smart-home integration.

Asia-Pacific accounts for 25% of the global market, with China, India, and Japan as the top-consuming countries. Rapid urbanization, smart-city initiatives, and growing renewable energy installations have boosted demand. Technological hubs in Singapore, Japan, and South Korea are promoting IoT-enabled monitoring systems. Local players like Smarteh are introducing smart panel monitors for large apartment complexes and industrial facilities. Regional consumer behavior shows high adoption via e-commerce channels, mobile AI applications for monitoring, and interest in smart plug devices for residential energy efficiency.

South America represents 12% of the market, with Brazil and Argentina as the leading countries. Market growth is supported by energy infrastructure modernization, increasing electricity costs, and government incentives for energy-efficient solutions. Technological adoption includes smart plug devices and remote monitoring platforms for commercial and residential applications. Local players are piloting integrated panel solutions in urban centers to optimize energy usage. Regional consumer behavior is influenced by media-driven awareness campaigns, localized device features, and growing interest in real-time monitoring to reduce utility expenses.

Middle East & Africa hold approximately 10% of the global market, with UAE and South Africa driving demand. Market adoption is supported by digital modernization in construction, oil & gas sector efficiency, and smart-city initiatives. Technological modernization includes cloud-based analytics, IoT integration, and mobile-enabled monitoring. Local players are implementing energy-monitoring solutions in residential complexes and industrial sites. Consumer behavior shows growing adoption in urban households, with interest in demand-response programs, renewable integration, and energy optimization for both commercial and residential facilities.

United States – 38% Market Share: Strong production capacity, high smart-home adoption, and government energy-efficiency incentives.

Germany – 12% Market Share: Leading European market driven by regulatory mandates, sustainability initiatives, and robust commercial infrastructure adoption.

The Home Power Monitors Market is moderately consolidated with approximately 120 active global competitors, including manufacturers, technology providers, and energy solution integrators. The top five companies collectively hold about 55% of the market, reflecting strong positions of major players while leaving room for regional specialists and emerging startups. Key strategic initiatives in the market include product launches of AI-enabled monitors, strategic partnerships with utilities, integration of IoT and cloud-based analytics, and collaborations with smart-home ecosystem providers. For example, companies are increasingly offering predictive energy management solutions and appliance-level disaggregation technologies. Mergers and acquisitions have accelerated, enabling firms to expand geographic reach and technological capabilities. Innovation trends focus on real-time energy tracking, predictive load management, demand-response participation, and enhanced cybersecurity protocols. Regional differentiation is evident: North America emphasizes enterprise-grade integration and residential smart-home adoption, Europe prioritizes compliance and explainable energy monitoring, and Asia-Pacific leads in mobile-enabled monitoring solutions. With over 30% of competitors emerging from Asia-Pacific, the market demonstrates a strong mix of innovation, competitive pressure, and rapid technology evolution.

Honeywell

Eaton

Legrand

ABB

General Electric

Landis+Gyr

Emporia Energy

Current technologies in the Home Power Monitors Market revolve around IoT-enabled sensors, AI-driven analytics, cloud integration, and smart plug systems. IoT sensors allow real-time energy tracking at the appliance or circuit level, enabling households to monitor consumption patterns precisely. AI-powered disaggregation technology can now identify specific appliances’ energy usage with up to 92% accuracy, allowing homeowners and commercial users to optimize energy consumption efficiently. Cloud-based platforms facilitate remote monitoring, predictive analytics, and load forecasting across multiple properties, supporting demand-response participation and peak-load management. Emerging technologies include edge-computing-enabled monitors, which process energy data locally to reduce latency and bandwidth requirements, and integration with renewable energy systems, such as solar panels and residential battery storage, for intelligent load balancing. Additionally, mobile and voice-enabled interfaces are expanding consumer accessibility, with over 45% of users in North America and Asia-Pacific using mobile apps for real-time control and alerts. Security protocols, including end-to-end encryption and blockchain-enabled data integrity, are increasingly adopted to address cybersecurity concerns. Collectively, these technological advancements enable more precise energy management, cost optimization, and environmentally sustainable practices for both residential and commercial users.

In March 2024, Sense launched its Home Energy Monitor Pro, integrating AI-based appliance recognition with cloud analytics, allowing users to detect usage anomalies across over 20 household devices. Source: www.sense.com

In July 2023, Schneider Electric introduced EcoStruxure Energy Monitoring, an IoT-enabled platform for residential and commercial buildings, supporting predictive load management and integrating with over 150 smart-home systems globally. Source: www.se.com

In November 2024, Siemens unveiled its Smart Home Energy Dashboard, offering real-time visualization for over 50,000 households in pilot programs, enhancing energy optimization and demand-response participation. Source: www.siemens.com

In June 2024, Emporia Energy rolled out a modular home monitor system capable of monitoring up to 60 circuits, improving energy transparency for large residences and multi-family complexes. Source: www.emporiaenergy.com

The Home Power Monitors Market Report provides a comprehensive analysis of product types, applications, end-users, regional insights, and technology trends across the globe. It covers single-phase and three-phase monitors, smart plugs, and integrated panel solutions, offering clarity on adoption patterns and technological innovations. Applications analyzed include residential, commercial, industrial, and renewable energy integration, with detailed insights into operational efficiency, energy management strategies, and consumer adoption behavior. End-user coverage spans households, multi-family complexes, offices, and industrial facilities, emphasizing regional variations in usage patterns, adoption rates, and monitoring sophistication. Geographically, the report examines North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting market volume, growth drivers, and technological trends in each region. The report also explores emerging technologies, such as AI-based disaggregation, cloud and edge computing, IoT-enabled sensors, and predictive analytics. Niche market segments, including multi-circuit monitoring and renewable energy-integrated solutions, are also addressed. The analysis equips decision-makers with actionable intelligence for strategic planning, investment prioritization, and deployment of innovative home power monitoring solutions across diverse sectors and regions.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 350.0 Million |

| Market Revenue (2032) | USD 1,012.5 Million |

| CAGR (2025–2032) | 14.2% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Sense, Schneider Electric, Siemens, Honeywell, Eaton, Legrand, ABB, General Electric, Landis+Gyr, Emporia Energy |

| Customization & Pricing | Available on Request (10% Customization is Free) |