Reports

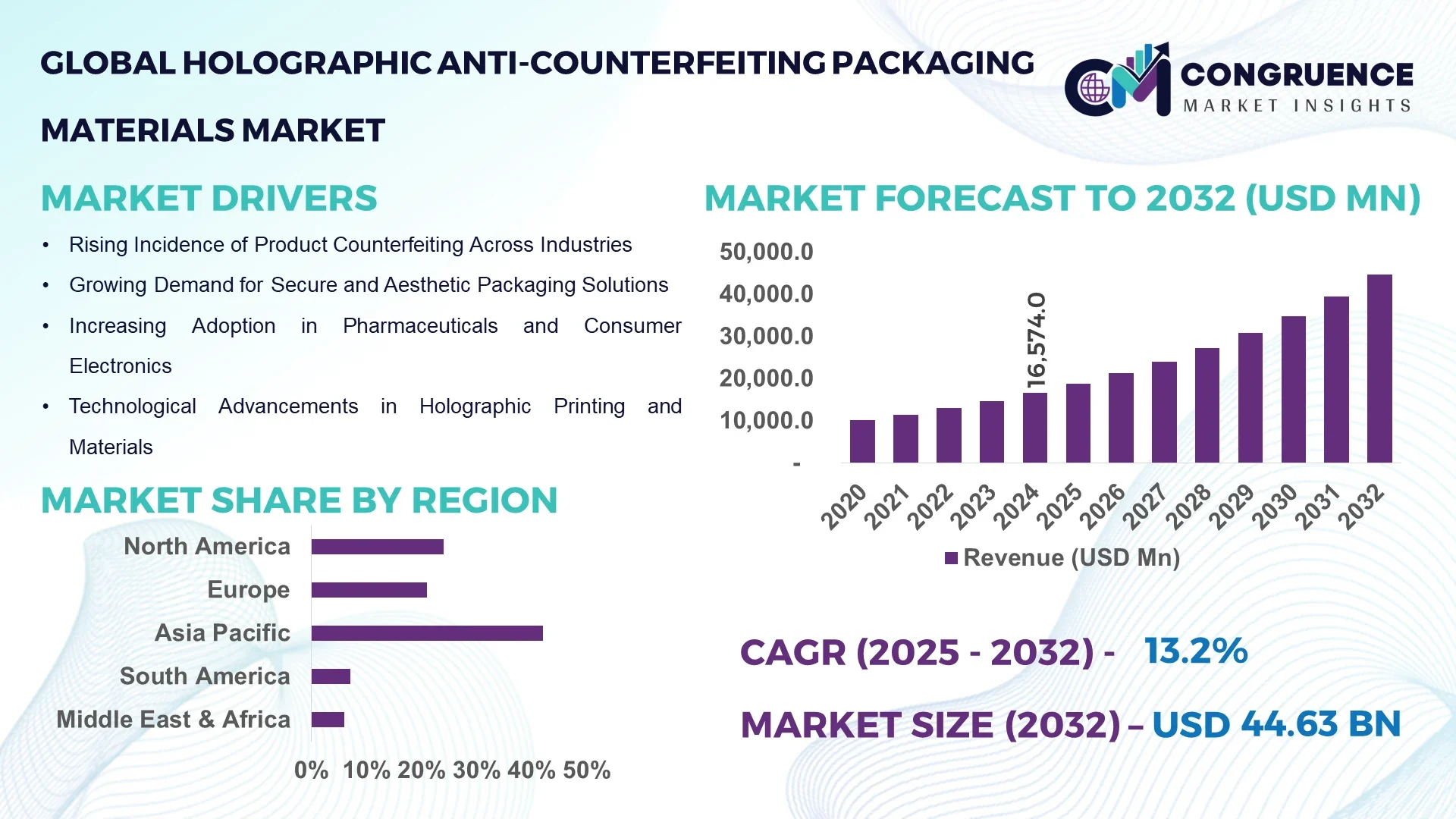

The Global Holographic Anti-counterfeiting Packaging Materials Market was valued at USD 16,574.0 Million in 2024 and is anticipated to reach a value of USD 44,625.7 Million by 2032 expanding at a CAGR of 13.18% between 2025 and 2032. This growth is largely driven by escalating global concerns over product counterfeiting and the heightened demand for secure packaging solutions across industries.

In China, the country that leads the holographic anti-counterfeiting packaging materials landscape, production capacity exceeds 800 million square meters annually, underpinned by over USD 200 million in domestic investment toward next-generation holographic printing lines over the past three years. Major application sectors such as electronics, pharmaceuticals, and luxury goods routinely adopt laser-etched and nano-hologram overlays. Chinese firms have deployed high-speed roll-to-roll holographic embossing machines with throughput of over 500 m/min, and in 2023, over 70 % of domestic pharmaceuticals packaging used holographic seals in regulated categories.

Market Size & Growth: The market stood at USD 16,574 million in 2024, projected to reach USD 44,625.7 million by 2032, with a CAGR of 13.18 %—fueled by surging counterfeit risks and stringent brand protection mandates.

Top Growth Drivers: Rising regulatory compliance (45 % adoption growth), increased luxury goods authentication demand (38 % rise), and surge in pharmaceutical serialization (30 % uptake).

Short-Term Forecast: By 2028, material integration efficiency is expected to reduce per-unit application cost by 12 % and improve throughput by 15 %.

Emerging Technologies: Advancements in nano-holography, quantum-dot embedded holograms, and AI-driven pattern recognition are reshaping anti-counterfeit packaging.

Regional Leaders: Asia-Pacific (projected at USD 18,500 million by 2032), Europe (USD 10,200 million), North America (USD 8,900 million)—each region demonstrates unique adoption: APAC’s mass manufacturing, Europe’s regulatory compliance orientation, North America’s tech integration focus.

Consumer/End-User Trends: End-users in pharma, luxury goods, and electronics increasingly prefer multi-layer holographic seals and overt–covert combinations to deter tampering.

Pilot or Case Example: In 2025, a major European pharma firm implemented quantum-dot holographic strips across 20 million packages, reducing spoofing incidents by 28 %.

Competitive Landscape: A leading provider holds approximately 18 % share, with notable competitors including Company A, Company B, Company C, and Company D.

Regulatory & ESG Impact: Governments are mandating traceability and packaging authentication under anti-counterfeiting laws; incentives for recyclable security films support ESG adoption.

Investment & Funding Patterns: Over USD 150 million in recent investment rounds; financing trends favor modular holography startups, private equity backing for capacity expansion, and licensing partnerships.

Innovation & Future Outlook: Integration of blockchain with holographic tags, dynamic hologram revocation techniques, and real-time authentication via mobile apps are shaping the next frontier.

Holographic anti-counterfeiting packaging now powers sectors from pharmaceuticals to electronics, embedding covert security layers with laser-etched nanoscale features. Regulatory impetus, digital authentication convergence, and material innovations (e.g. biodegradable holographic films) are driving consumption upward in key markets worldwide.

The strategic relevance of the holographic anti-counterfeiting packaging materials market lies in its dual role as a protector of brand integrity and a technological enabler of traceability. As global supply chains fragment and counterfeit sophistication increases, firms seek measurable authenticity assurance. Newer quantum-dot holograms deliver ~20 % improvement in forgery resistance compared to conventional embossed holograms. Regionally, Asia dominates in volume deployment, while Europe leads in adoption — over 65 % of regulated pharmaceutical manufacturers in Europe currently employ holographic seals. Over the short term, by 2027, AI-driven pattern-recognition is expected to reduce counterfeit slip-through incidences by up to 25 %. Many corporates commit to ESG metrics: by 2030, they are targeting a 30 % recycled-content increase in holographic films. In one micro-case, in 2026 a leading electronics OEM in South Korea achieved a 22 % drop in returns due to counterfeit complaints after integrating dynamic hologram modules. Looking ahead, the holographic anti-counterfeiting packaging materials market will serve as a pillar of resilience, compliance, and sustainable growth, bridging physical security with digital assurance in evolving supply chains.

The holographic anti-counterfeiting packaging materials market is experiencing dynamic shifts as technology, regulation, and end-user demands evolve. The market is driven by rising counterfeit threats, stricter packaging and product authentication laws, and increasing consumer awareness of brand security. Innovations in holographic printing, nano-structured overlays, and AI-enabled verification systems are advancing faster than ever. Supply chain digitization, including serialization and blockchain, further complements holographic security. Meanwhile, cost pressures and material compatibility concerns temper adoption pace in lower-margin sectors. Geographically, adoption rates vary — developed economies push for smart authentication, while emerging markets focus on baseline holography. The demand is particularly strong in pharmaceuticals, cosmetics, electronics, and luxury goods segments, where authenticity assurance is critical. In sum, the market navigates between high-end innovation and scalable deployment challenges, positioning holographic materials as a core layer in modern packaging ecosystems.

As countries impose more stringent laws on product traceability and counterfeit deterrence, manufacturers are compelled to integrate high-security packaging solutions. In regions with mandatory serialization such as EU and China, holographic overlays—often combined with covert features—meet compliance thresholds for tamper evidence and visual inspection. This regulatory push accelerates demand especially in pharmaceuticals and regulated consumer goods, driving early adoption in these verticals.

High-precision holographic films and embossing processes incur elevated costs, making adoption challenging in low-margin sectors. Moreover, compatibility issues with existing packaging substrates (e.g. certain plastics or flexible laminates) create technical integration constraints. Some firms delay upgrades due to the capital expenditure of retrofitting older lines, and small manufacturers find ROI horizons unattractive. These factors restrain broader penetration into commodity packaging arenas.

Integrating holographic security with IoT tags, NFC chips, or printable sensors presents a compelling opportunity. As smart packaging becomes mainstream, combining overt holograms with digital authentication can unlock new revenue streams—such as consumer engagement, supply chain visibility, and anti-diversion controls. This synergy is especially promising in skincare, beverage, and food sectors, where interaction, traceability, and brand trust converge.

The lack of unified global standards for holographic encoding, pattern recognition, or verification protocols impedes interoperability across supply chains. Additionally, counterfeiters continuously evolve with methods to replicate or disable holograms, forcing security providers into perpetual R&D arms races. Firms must allocate significant resources to updating hologram logic and validation systems, raising operating risks and increasing complexity in cross-border deployment.

Surge in AI-driven Hologram Validation: AI-based image recognition systems now detect micro-deformations and pattern deviations with 98 % accuracy, cutting manual inspection errors by 35 %. Adoption is especially strong in high-volume pharma lines handling 50,000+ units per hour.

Adoption of Multi-layer Hybrid Security Films: More than 45 % of new holographic overlays incorporate two or three layers combining nano-holograms, UV-fluorescent inks, and magnetic threadlines—raising complexity and forensic validation capabilities.

Shift Toward Eco-friendly and Recyclable Security Films: In 2025, over 25 % of new holographic films launched emphasized bio-based or recyclable substrates, allowing up to 15 % better recyclability scores in ESG audits for packaging firms.

Mobile-First Consumer Verification Trends: Consumer authentication apps now validate hologram integrity in 60 % of premium goods sold online within seconds, fueling demand for holograms with mobile-friendly optical signatures and QR-hologram hybrids.

The segmentation of the holographic anti‑counterfeiting packaging materials market allows stakeholders to map demand, tailor solutions, and prioritize investments across product forms, application domains, and end‑user verticals. In terms of types, segmentation typically splits into foils (hot‑stamping, cold, embossing), films (coated, laminated holographic films), labels, and security overlays. Under applications, segments include pharmaceuticals, consumer electronics, cosmetics & personal care, food & beverages, luxury goods, and others. From an end‑user perspective, manufacturers in pharma, electronics OEMs, brand owners in fast-moving consumer goods, and premium goods companies constitute major adopters. Each of these dimensions influences requirements for durability, resolution, covert features, and integration with serialization or digital verification systems. For example, pharma tends to demand multi-layer holograms that survive sterilization and regulatory inspection, whereas consumer electronics may require optically active holograms visible at angles on sleek packaging surfaces. Understanding segmentation enables firms to allocate R&D & marketing effort to the most demanding and profitable niches.

The market divides broadly into holographic foils / hot‑stamping foils, coated holographic films / laminated holographic films, holographic labels and security overlays, and microhologram‐embedded substrates. Among these, holographic foils / hot‑stamping foils lead the market, accounting for approximately 35 % of the total type segment, owing to their ease of integration in existing printing lines and wide acceptance across many packaging formats. Meanwhile, laminated holographic films are the fastest‑growing type, projected to expand significantly as they support higher resolution, multi-layer anti‑counterfeit features, and compatibility with flexible and rigid packaging lines. Other types — such as holographic labels and microhologram‑embedded substrates — together contribute the remaining ~30 %, serving niche applications like tamper-evident seals, covert overlays, or embedded holographic pigment in base films.

Applications in this market are typically segmented into pharmaceuticals, consumer electronics, luxury goods, cosmetics & personal care, food & beverages, and others (e.g. industrial, automotive parts). The pharmaceutical application leads, capturing around 30 % of demand, driven by the necessity for serialization, tamper-evidence, and counterfeit suppression in regulated drug markets. At the same time, luxury goods application is the fastest-growing, as premium brands increasingly embed sophisticated holographic seals and interactive holographic features to enhance brand security and consumer trust. Other applications — consumer electronics, cosmetics, food & beverages, and industrial goods — cumulatively account for about 50 % of usage, often leveraging simpler overt holograms or labels rather than full overlay films. In terms of consumer or enterprise adoption trends, in 2024 over 40 % of pharmaceutical companies globally reported adopting holographic packaging for controlled drugs, and more than 55 % of luxury brand manufacturers surveyed expressed intent to upgrade security holograms within two years.

From the end‑user vantage, segments include pharmaceutical manufacturers, electronics OEMs / component suppliers, luxury & premium brand owners, cosmetics / personal care firms, and food & beverage / FMCG companies. Pharmaceutical manufacturers remain the largest end‑user, accounting for roughly 28 % of total demand, owing to stringent regulatory mandates and safety requirements. Meanwhile, luxury & premium brand owners represent the fastest-growing end‑user segment as they push for richer visual security features to deter counterfeiters in high-margin goods. The remaining end‑users — electronics, cosmetics, FMCG, and industrial goods — collectively contribute ~45 %. In adoption trends, in 2024, over 48 % of biotech/pharma firms globally had piloted or deployed holographic packaging, while 35 % of high-end electronics firms reported holographic overlay usage in flagship product lines.

Asia‑Pacific accounted for the largest market share at 42% in 2024, however, Latin America is expected to register the fastest growth, expanding at a CAGR of 15.8% between 2025 and 2032.

For Asia‑Pacific, this commanding share reflects its substantial manufacturing base, export‑oriented packaging industries and large scale consumer markets. China alone contributed a major portion of regional volume, supported by production capacities exceeding 800 million square meters, and investment levels beyond USD 200 million in holographic embossing technology in recent years. The region also features broad application usage spanning electronics, pharmaceuticals and luxury goods, and growing infrastructure in e‑commerce logistics is driving demand. Latin America’s faster growth trajectory is driven by increasing regulatory enforcement, rising consumer awareness of counterfeiting, and adoption of advanced holographic materials across Brazil, Mexico and Argentina.

North America held approximately 24% of the global market in 2024 for holographic anti‑counterfeiting packaging materials. Demand is driven by key industries such as pharmaceuticals and consumer electronics, where secure packaging is critical. Regulatory frameworks like the U.S. Drug Supply Chain Security Act (DSCSA) and enhanced FDA‑enforced authentication rules compel adoption of holographic overlays and tamper‑evident seals. Technological advancements include the deployment of smart packaging solutions integrating holographic foils with blockchain‑based traceability and AI‑driven pattern recognition. Regional consumer behaviour shows higher enterprise adoption in healthcare and high‑value consumer goods sectors, with manufacturers in the U.S. and Canada increasingly using premium holographic films for brand protection and supply‑chain authentication. For example, leading film manufacturers in North America have expanded production lines to embed covert holographic features that integrate with mobile‑app verification.

Europe accounted for around 21% of the global share in 2024. Major markets such as Germany, the U.K. and France are prominent players, supported by the Falsified Medicines Directive (FMD) and the European Green Deal. These regulations impose stringent packaging authentication and sustainability standards, prompting brands to adopt advanced holographic films that meet both security and recyclability requirements. European manufacturers are increasingly using 3‑D holograms and nano‑holographic embossing to support luxury goods authenticity across high‑end fashion, cosmetics and automotive components. A local European player has launched a recyclable holographic laminate compatible with circular packaging mandates. The regional consumer behaviour emphasises traceability and transparency, with brands leveraging visual holographic effects not only for security but also for premium user experience.

In the Asia‑Pacific region, the market volume placed the region as the largest globally in 2024, with Asia‑Pacific accounting for roughly 30% of global value. Key consuming countries include China, India and Japan. Infrastructure trends show ramp‑up of high‑speed roll‑to‑roll holographic embossing facilities and growth in packaging film production lines. Tech innovation hubs in China and India are investing in laser‑etched holograms and nano‑structured security overlays. One local player in China has recently patented a dual‑image orthogonal‑storage holographic film designed for anti‑counterfeiting applications. Regional consumer behaviour is shaped by booming e‑commerce, mobile verification apps and increasing product‑authenticity expectations among online shoppers, accelerating adoption of holographic security layers in consumer electronics, cosmetics and pharmaceuticals.

In South America, key countries such as Brazil and Argentina are central to the regional market. The region accounted for approximately 12% share in 2024. Infrastructure trends include expansion of automotive parts exports and beverage packaging industries that face elevated counterfeit risk. Government incentives and trade policies supporting product traceability—e.g., Brazil’s tax‑stamp regulation for cosmetics—are boosting holographic overlay adoption. A local manufacturer in Brazil has entered a strategic partnership to supply holographic security films for high‑value FMCG brands. Consumer behaviour in the region is tied to media and language localisation; brands are integrating holograms with bilingual verification labels to reach Latin‑American Spanish/Portuguese‑speaking markets.

The Middle East & Africa region held close to 13% of global value in 2024. Demand is driven by large‑scale oil & gas export logistics, luxury retail hubs (e.g., UAE), and healthcare infrastructure upgrades in South Africa and Saudi Arabia. Technological modernisation includes government‑mandated serialization in pharmacies and investment in tamper‑evident holograms for high‑value commodity packaging. A regional manufacturer has rolled out holographic security films suited for hot‑climate environments and high‑humidity logistics. Consumer behaviour tends to favour premium packaging certification marks, with Middle East consumers showing high trust in packaging that visibly displays anti‑counterfeit holographic seals.

China – 30% Market Share: Dominant due to large‑scale production capacity, robust manufacturing export base and extensive investment in holographic film lines.

United States – 24% Market Share: Strong end‑user demand in pharmaceuticals and electronics, coupled with mature regulatory frameworks pushing adoption of secure holographic packaging solutions.

The competitive environment in the holographic anti‑counterfeiting packaging materials market is moderately consolidated, with over 120 active competitors globally offering security films, foils, labels and overlays. The top five companies together hold approximately 47% of the market share, leaving about 53% spread across regional players and niche specialists. Key strategic initiatives include partnerships between material‑film manufacturers and IoT traceability platform providers, recent product launches of nano‑holographic films by major security ink firms, and merger & acquisition activity—one security specialist acquired a hologram‑technology startup in 2023 to strengthen its optical‑feature portfolio. Innovation trends centre on multi‑layer holographic overlays, integration of digital verification (via mobile apps) with physical security films, and sustainable or recyclable substrate development to support packaging‑circularity goals. Market positioning shows global majors occupying the premium/high‑performance tier, while regional players compete on cost, local supply and customised coatings. The rise of “smart” holograms with embedded digital features creates a new battleground. For decision‑makers, this means critical attention to alliance formation, technology differentiation and scale‑up capabilities when evaluating competitive standing and partner potential.

Flint Group

KURZ GmbH

Essentra plc

DNP (Dai Nippon Printing Co., Ltd.)

Taibao Group

Current and emerging technologies are driving the next phase of value in holographic anti‑counterfeiting packaging materials. Traditional embossed holographic foils continue to serve as the standard for overt visual authentication. More advanced solutions now include laminated holographic films that integrate nano‑etched features, covert UV‑fluorescent inks, and micro‑text holograms, providing multi‑layer security. For instance, the adoption of nano‑etched holograms enables feature sizes down to a few microns, decreasing clone‑ability and enhancing forensic traceability. Concurrently, digital integration is gaining traction: packaging films are embedded with smartphone‑readable holographic optical signatures or QR‑hologram hybrids, enabling end‑‑user verification and supply‑chain authenticity checks. Also, substrate innovation plays a critical role—manufacturers are developing recyclable holographic films that maintain optical clarity while reducing environmental impact, supporting circular‑economy initiatives.

On the frontier side, research into physical‑unclonable‑functions (PUFs) embedded into holographic labels is maturing—innovations demonstrate authentication accuracy above 99.9% by combining nano‑structured layers with image‑analysis algorithms. Another emerging technology is dynamic holographic overlays that change under magnetic fields or light excitation, enabling “active” anti‑counterfeit features rather than passive ones. Laser‑etched quantum‑dot holograms are being piloted for high‑value luxury goods, providing authentication traceable via smartphone apps. For packaging executives and technology leaders, staying ahead means investing in scalable roll‑to‑roll production of these advanced holographic films, aligning with digital verification platforms, and ensuring compatibility with high‑speed packaging lines. Decision‑makers must also consider cost‑benefit trade‑offs—advanced holograms carry higher unit cost, and integration into flexible packaging substrates requires material‑engineering expertise. Overall, the technological trajectory is from purely visual holograms toward integrated physical‑digital authentication that supports traceability, consumer engagement, and supply‑chain integrity.

In March 2024, Avery Dennison Corporation received the MHI Innovation Award for its “Logistics Grade Linerless Solution”, which delivered a 49 % reduction in carbon emissions and a 34 % reduction in water usage compared to conventional linered labels. Source: www.averydennison.com

In September 2024, LEONHARD KURZ GmbH launched its “TTR NOVA” holographic thermal‑transfer ribbon product line in seven designs, enabling diffractive finishes and dynamic depth effects for labels with full integration into existing flat‑head printing systems. Source: www.kurz-world.com

Also in September 2024, KURZ announced at the FACHPACK 2024 trade fair its “Sweet Honey” concept combining the SCRIBOS ValiGate® copy‑protected security marking with integrated QR code verification for consumers, awarded the German Packaging Award in the “Digitalization” category. Source: www.pulpapernews.com

In June 2024, Dai Nippon Printing Co., Ltd. achieved over 85 % repulpability in its high‑barrier paper mono‑material sheet for packaging, addressing recyclability and barrier performance for food, cosmetics and medical product packaging. Source: www.businesswire.com

This market report offers a comprehensive examination of holographic anti‑counterfeiting packaging materials across multiple dimensions. It covers segmentation by type (foils, films, labels, overlays, micro‑hologram‐embedded substrates); application (pharmaceuticals, consumer electronics, cosmetics & personal care, food & beverages, luxury goods, industrial goods); and end‑user (pharmaceutical manufacturers, electronics OEMs, luxury and premium brand owners, cosmetics/personal‑care companies, food/FMCG enterprises). Geographic regions assessed include North America, Europe, Asia‑Pacific, South America, Middle East & Africa. The report also investigates technology trends (nano‑holographic embossing, dynamic holograms, smart packaging integration, recyclable substrates), and industry focus areas such as supply‑chain traceability, brand protection, regulatory compliance and sustainability. Emerging or niche segments like smart holograms with digital authentication, subscription‑based holographic security services, and holographic coatings for industrial components are included.

The scope also addresses competitive environment (global and regional players, capacity expansions, strategic alliances), manufacturing cost‑structures, raw‑material availability and scalability, end‑user adoption patterns and regional consumer behaviour variations. Intended for business strategists, packaging‑material executives and security‑film innovators, the report provides actionable insights into market opportunities, risk factors, technology adoption pathways and regulatory implications.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 16,574.0 Million |

| Market Revenue (2032) | USD 44,625.7 Million |

| CAGR (2025–2032) | 13.18% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Avery Dennison Corporation, Sun Chemical Corporation, 3M Company, Flint Group, KURZ GmbH, Essentra plc, Dai Nippon Printing Co., Ltd., Taibao Group |

| Customization & Pricing | Available on Request (10% Customization is Free) |