Reports

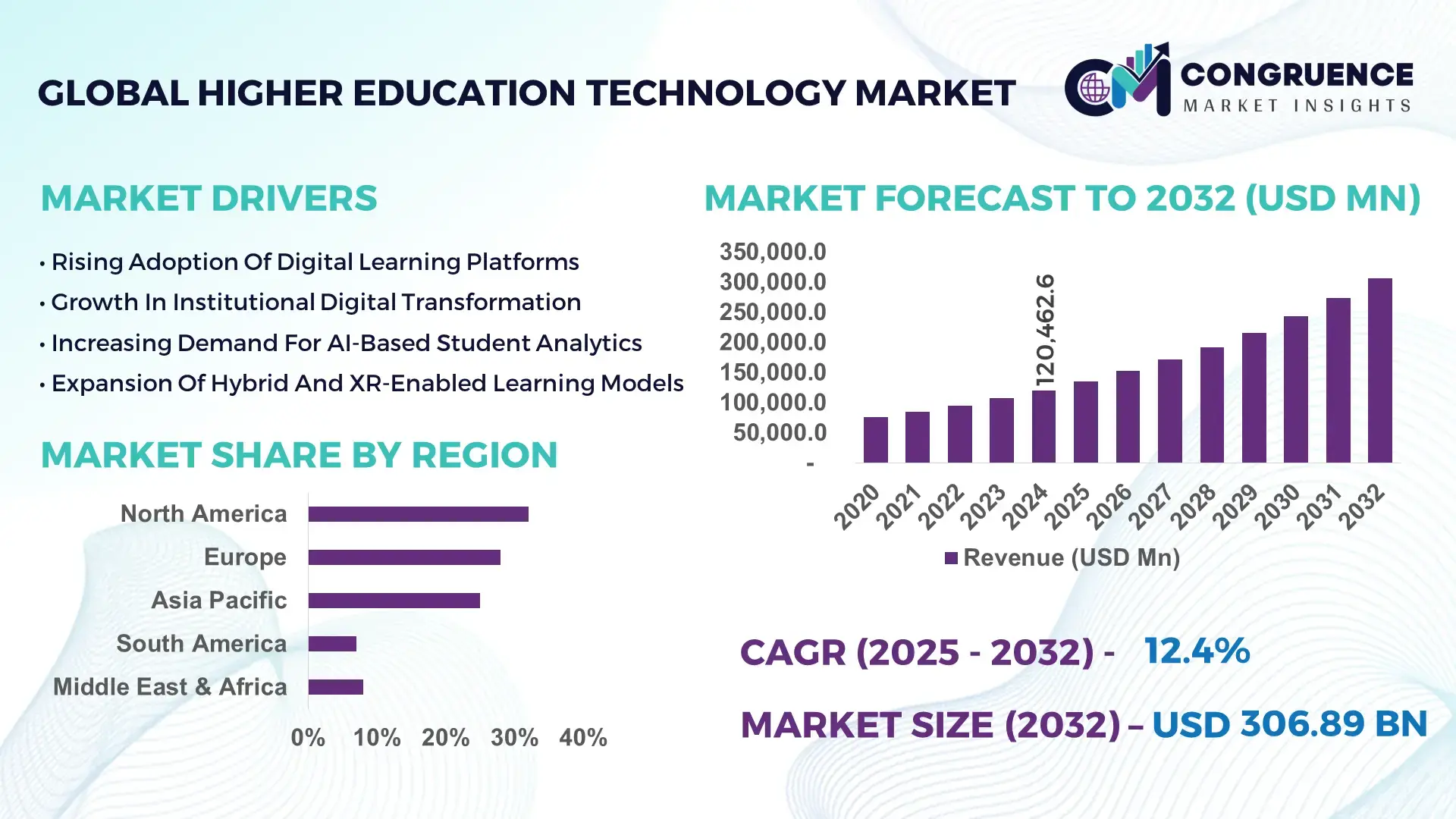

The Global Higher Education Technology Market was valued at USD 120,462.6 Million in 2024 and is anticipated to reach a value of USD 306,890.0 Million by 2032 expanding at a CAGR of 12.4% between 2025 and 2032, according to an analysis by Congruence Market Insights. Growth is supported by accelerating digital transformation, AI-integrated learning experiences, and rapid modernization of institutional IT infrastructure.

The United States hosts one of the most advanced higher-education technology ecosystems, driven by large-scale institutional digital investments exceeding USD 18.2 Billion in 2024, with more than 4,300 universities adopting cloud-based LMS, analytics platforms, and smart campus solutions. Over 72% of U.S. higher-education institutions utilize AI-driven student analytics, and more than 58% of learners access hybrid or fully digital coursework through institution-led technology channels. The country also leads in EdTech R&D spending, surpassing USD 3.1 Billion in 2023, with strong adoption across STEM, business, and healthcare programs.

Market Size & Growth: Valued at USD 120.4 Billion in 2024 and projected to reach USD 306.8 Billion by 2032, expanding at a CAGR of 12.4% driven by sustained digital transformation and scalable cloud integration.

Top Growth Drivers: AI-enabled learning adoption up 47%, hybrid learning usage improving operational efficiency by 33%, and smart campus automation adoption rising 29%.

Short-Term Forecast: By 2028, digital learning platforms are expected to improve institutional cost efficiency by 22% and learning outcome analytics accuracy by 31%.

Emerging Technologies: Generative AI tutors, extended reality (XR)-based immersive learning, and blockchain-secured credentialing are gaining rapid traction.

Regional Leaders: North America projected to reach USD 128.6 Billion by 2032 with advanced AI adoption; Europe expected to reach USD 74.3 Billion supported by digital standards; Asia-Pacific projected at USD 62.1 Billion with strong enrollment-driven technology upgrades.

Consumer/End-User Trends: Universities increasingly deploy adaptive learning engines; 64% of students use mobile-first academic platforms; continuing education technology usage is accelerating globally.

Pilot or Case Example: In 2024, a Canadian university piloted an AI-powered retention analytics system, reducing dropouts by 18% within one semester.

Competitive Landscape: Leading player controls approximately 11% of the market, followed by major competitors including Blackboard, Anthology, Instructure, Oracle, and Adobe.

Regulatory & ESG Impact: Strong compliance standards and digital accessibility mandates are accelerating inclusive technology adoption across global universities.

Investment & Funding Patterns: More than USD 6.4 Billion invested globally in 2023–2024 across EdTech modernization, cloud migration, and AI learning platforms.

Innovation & Future Outlook: Next-generation predictive learning engines, interoperable credential ecosystems, and XR-based STEM training programs are expected to shape global higher-education modernization.

The Higher Education Technology market is experiencing accelerated adoption across universities, research institutions, and digital learning centers, with strong contributions from learning management systems, AI-powered student services, and immersive training platforms. Rapid innovation in generative learning models, smart campus IoT systems, and cloud-native enrollment platforms is reshaping the competitive landscape. Regulatory mandates for accessibility, cybersecurity requirements, and data protection frameworks are reinforcing technology standardization. Growth is further enhanced by rising enrollment in digital programs and increased institutional spending on modern learning infrastructure.

The Higher Education Technology Market holds strategic importance as global universities modernize digital infrastructures and integrate AI-enabled tools to enhance learning outcomes, administrative efficiency, and institutional competitiveness. Advanced learning platforms, immersive digital classrooms, and integrated analytics ecosystems are enabling measurable gains, with AI-supported learning pathways delivering up to 35% improvement in personalized academic performance compared to legacy systems. Cloud-first architectures are replacing traditional on-premise setups, enabling institutions to scale enrollment, optimize resource utilization, and reduce IT maintenance by as much as 28%.

Regional dynamics continue to evolve: North America dominates in volume, while Asia-Pacific leads in adoption with 62% of institutions integrating hybrid or fully digital learning models. Europe demonstrates strong compliance-driven adoption, supported by structured digital education frameworks. By 2027, AI-driven learning analytics are expected to improve student retention and early-intervention accuracy by over 30%, while smart campus IoT systems may reduce facility operating costs by up to 22%.

ESG-linked commitments are influencing procurement decisions, with institutions targeting 25% reductions in energy consumption across technology systems by 2030. In 2024, a leading Asian university achieved a 31% improvement in student success metrics through a large-scale deployment of AI-enabled course mapping and behavioral analytics tools.

Overall, the Higher Education Technology Market is evolving into a cornerstone for institutional resilience, regulatory alignment, and sustainable long-term academic and operational growth.

The Higher Education Technology Market is shaped by rapid digital transformation, rising student demand for flexible learning formats, and strong institutional commitments toward technology-enabled modernization. Cloud-based solutions, AI-driven academic analytics, and mobile-first learning applications are accelerating adoption across universities and research ecosystems. Increased spending on cybersecurity, digital identity management, and data governance is further influencing institutional technology priorities. Emerging technologies—such as extended reality (XR), blockchain credentialing, and generative AI—are creating new opportunities for immersive education and secure ecosystem interoperability. Meanwhile, global enrollment shifts, workforce skill demands, and policy-driven digital education initiatives continue to influence market behavior and long-term investment strategies.

Rising demand for personalized learning pathways is significantly accelerating adoption across the Higher Education Technology Market. Institutions are integrating advanced AI-driven engines to deliver adaptive course content, customized academic recommendations, and performance-based learning feedback. More than 61% of global universities report increased use of student analytics to optimize engagement and reduce academic dropouts. Personalized digital tools are improving study efficiency by up to 27% in large public universities and enhancing learning satisfaction metrics by more than 34%. Increased interest in hybrid and competency-based learning, supported by mobile-first academic platforms, is expanding the need for scalable, intelligent learning systems. Higher professional education programs—including engineering, biomedical sciences, and management—are increasingly deploying AI-augmented tools that monitor student learning behaviors, track performance, and identify learning gaps. These improvements in learning outcomes and institutional management continue to push universities toward larger technology investments that support deep personalization and measurable academic impact.

The Higher Education Technology Market faces significant constraints due to the increasing frequency and complexity of cyberattacks targeting academic institutions. Universities hold vast volumes of sensitive data, with more than 48% reporting attempted breaches in the past 12 months, driven by vulnerabilities in legacy systems, decentralized IT networks, and third-party integrations. Rising threats—including ransomware, identity theft, and data exfiltration—are pushing institutions to increase security-related spending by more than 30%, which often delays funding for modernization projects. Compliance with privacy regulations, institution-level data governance mandates, and strict cybersecurity protocols introduces additional operational burdens. Many universities struggle with outdated infrastructure and insufficient cybersecurity expertise, increasing the risk of disruptions to digital learning ecosystems. These challenges hinder the full-scale adoption of innovative digital technologies, limit cross-platform integrations, and slow the pace of market expansion.

AI-driven ecosystem integration is creating substantial growth opportunities within the Higher Education Technology Market. Institutions are increasingly adopting unified digital architecture frameworks that connect LMS platforms, enrollment systems, library databases, assessment engines, and student support services within a cohesive, analytics-rich environment. More than 57% of universities planning large-scale digital upgrades highlight AI integration as the core investment priority for the next decade. The rise of generative AI in content creation, automated tutoring, and performance forecasting is fostering new use cases across diverse academic disciplines. Additionally, smart campus ecosystems—integrating IoT sensors, behavioral analytics, and automated facility management—offer opportunities to reduce operating costs by up to 26%. These interconnected systems enable institutions to improve student engagement, streamline administrative processes, and support flexible learning at scale. The expansion of blockchain-based credential verification and global education mobility platforms further strengthens international academic partnerships and digital credential interoperability.

High technology acquisition and integration costs continue to pose challenges across the Higher Education Technology Market. Universities often require extensive infrastructure upgrades, advanced networking capabilities, and multi-layered software ecosystems to support next-generation learning platforms. The average institution spends between 18% and 25% of its annual technology budget on integration- and compatibility-related tasks alone. Legacy systems, which remain prevalent in many regions, create additional complexities when linking AI-driven analytics tools, LMS engines, XR platforms, and smart campus systems. The shortage of specialized IT and EdTech professionals further slows deployment timelines, particularly in developing economies. Additionally, faculty training, content redesign, and user adoption efforts add to the total cost of ownership. These financial and operational burdens can delay modernization initiatives, limit innovation adoption, and create disparities in technology advancement across institutions globally.

• Expansion of AI-Powered Learning Ecosystems: Institutions are rapidly integrating AI-driven tutoring systems and predictive analytics engines, with adoption rising by 44% between 2022 and 2024. More than 70% of universities report measurable improvements in academic performance tracking, while AI-enabled support systems cut administrative workload by up to 29%. Increasing use of generative AI for automated assessments, content development, and learner guidance is reshaping academic delivery models across regions.

• Rapid Growth of XR and Immersive Learning Platforms: Demand for virtual laboratories, simulation-based STEM learning, and immersive professional training surged by 38% in 2024. Universities implementing VR-based laboratory modules recorded a 32% improvement in practical skill competency and a 25% reduction in physical lab resource usage. Adoption is strongest in engineering, medical sciences, and architecture programs, particularly across North America and Europe.

• Acceleration of Smart Campus Automation: Smart campus deployments—including IoT-enabled monitoring, biometric access controls, and automated facility management—expanded by 41% globally. Institutions leveraging connected sensors reported a 23% reduction in annual energy consumption and a 17% enhancement in facility safety. These digital transformation initiatives are becoming core components of long-term sustainability roadmaps.

• Rise of Blockchain-Enabled Credentialing and Student Identity Systems: Blockchain adoption in universities increased by 36% in 2024, primarily for secure credential verification and digital identity management. More than 12 million digital academic records were issued globally through blockchain systems, ensuring tamper-proof authentication and cross-border mobility. Adoption is gaining momentum in Asia-Pacific and Europe due to rising demand for secure international credential portability.

The Higher Education Technology Market is segmented across type, application, and end-user categories, each contributing to the sector’s technological and operational transformation. Types include learning management systems, student information systems, classroom technologies, AI-driven academic analytics tools, and virtual learning platforms. Applications span admissions, learning delivery, assessment, research, and campus management. End-users consist of universities, colleges, vocational institutions, and continuing education centers. Adoption varies by digital maturity and institutional scale, with advanced economies demonstrating higher integration rates of AI, cloud platforms, and smart campus tools. These segments collectively reveal a market driven by innovation, student-centric digital transformation, and growing infrastructure modernization needs globally.

Learning management systems (LMS) hold the leading position, accounting for 38% of total adoption in 2024 due to their essential role in digital course delivery, assessment, and student engagement. Student information systems (SIS) account for 27%, supported by institutional requirements for enrollment management, analytics, and compliance monitoring. Classroom technologies—such as interactive displays, virtual labs, and AI-enabled teaching tools—represent 18% of adoption, contributing to enhanced hybrid learning environments. Analytics and AI-enabled platforms hold 12% share but represent the fastest-growing segment, expanding at an estimated CAGR of 18.6% driven by demand for predictive analytics, personalized learning pathways, and campus automation capabilities. Remaining types, including XR-based platforms and blockchain credential systems, collectively contribute 5%, primarily serving niche academic and administrative applications.

Digital learning delivery constitutes the leading application category, accounting for 42% of adoption with high utilization across engineering, science, and management programs. Administrative and enrollment applications hold 26%, supported by increasing demand for automated admissions, scheduling, and compliance workflows. Research and laboratory digitalization represent 17% adoption, while assessment and student performance analytics account for 15%. Research applications are the fastest-growing segment, expanding at an estimated CAGR of 17.2%, driven by digitization of research workflows, virtual simulation tools, and data analytics engines. Remaining applications collectively contribute a 10% share. In 2024, more than 38% of global institutions piloted AI-powered academic analytics for student support. Over 60% of digitally-enabled learners preferred hybrid or mobile-first academic platforms for flexible study.

Universities dominate end-user adoption, accounting for 45% of total market share, driven by large-scale digital infrastructure upgrades, STEM program expansion, and strong faculty-technology integration. Colleges represent 28% adoption, with rapid digitization of general education and professional development courses. Vocational institutions and continuing education centers together hold 18% share, expanding steadily due to rising professional reskilling demand. Continuing education platforms represent the fastest-growing end-user segment, expanding at an estimated CAGR of 17.8% as working professionals shift to flexible, digital-first learning formats. Remaining institutional categories collectively contribute 9%. In 2024, more than 38% of global learners utilized digital academic support systems. Over 63% of adult learners preferred mobile-based continuing education tools for flexible scheduling.

North America accounted for the largest market share at 32% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 14–15% between 2025 and 2032.

In 2024, North American higher education institutions invested heavily in educational technology, with over 4,200 colleges and universities reporting active EdTech modernization initiatives. The region launched more than 1,100 AI-enabled learning analytics projects and implemented cloud-based LMS platforms in nearly 85% of its higher education institutions. Europe maintained a strong presence with over 3,000 institutions deploying hybrid learning systems and smart campus infrastructure. Meanwhile, Asia-Pacific saw more than 3,500 universities and tertiary institutions integrating mobile-first learning platforms, and its student population using EdTech tools surged by 48% in 2024. Latin America and the Middle East & Africa accounted for the balance, with over 1,500 institutions collectively beginning EdTech rollout programs, particularly in blended learning and digital credentialing.

How Is Smart Campus Innovation Reshaping University Technology Adoption?

North America controls roughly 32% of the global higher education technology market, underpinned by high digital maturity across U.S. and Canadian universities. Demand is driven by STEM faculties, research universities, and professional education programs. Government policies promoting digital learning grants and support for cloud infrastructure further boost adoption. Technologically, institutions in this region are deploying AI-driven student analytics, predictive retention tools, and immersive classroom solutions. Major U.S. EdTech providers are offering integrated platforms with adaptive learning and analytics across thousands of campuses. In North America, institutional behavior shows high enterprise adoption in areas like business schools and medical education, with more than 70% of faculty using EdTech dashboards regularly and students increasingly preferring mobile-first access to courses.

Why Is Regulatory Compliance Driving Intelligent EdTech Uptake in Key Markets?

Europe commands an estimated 28% share of the higher education technology market, with fast adoption in Germany, the UK, France, and the Nordics. Regulatory bodies mandate data privacy compliance and accessibility standards, pushing universities to adopt explainable AI and secure data governance frameworks. Emerging tech such as XR laboratories and blockchain credentialing systems are being piloted by major European institutions. A German higher education provider recently adopted AI-enabled learning analytics across more than 30 campuses to predict student performance and optimize support services. European end users often favour tools that emphasize transparency, sustainability, and compliance due to strong regulatory oversight and institutional governance priorities.

How Are Expanding Student Populations Driving EdTech Modernization in Higher Education Hubs?

Asia-Pacific stands as a rapidly growing region in the higher education technology market, with substantial volume driven by populous markets like China, India, Japan, and Southeast Asia. Over 3,500 universities across the region are modernizing digital infrastructure, with increasing deployment of cloud-first LMS platforms and AI-supported adaptive learning engines. Innovation hubs in Bengaluru, Shanghai, and Seoul are producing scalable EdTech models tailored for mass enrollment and lower cost. Local EdTech firms in India and China are developing generative AI-based tutoring and assessment systems, supporting millions of learners. In this region, students show strong preference for mobile-first educational apps, combining e-commerce payment methods and AI recommendation engines to access courses and micro-credentials on demand.

How Are Latin American Institutions Investing in Localized Digital Learning and Credentialing?

In South America, countries such as Brazil, Argentina, and Chile are driving EdTech adoption in higher education, representing an estimated 7–8% regional share. Governments and universities are investing to build digital classrooms, blended learning campuses, and credential-verification systems. Local EdTech companies are offering Spanish- and Portuguese-language LMS and AI-tutoring services to support digital transformation in over 200 universities. Infrastructure improvements in broadband and public higher education funding are enabling growth. Student behavior in this region often emphasizes affordability, mobile compatibility, and culturally localized content, leading to strong uptake of hybrid learning and digital courseware.

How Is Technology Transforming Higher Education in Emerging Knowledge Economies?

Middle East & Africa capture approximately 8% of the global higher education technology market, with major growth in the UAE, South Africa, Saudi Arabia, and Egypt. Regional demand is driven by national strategies to build knowledge economies, with investments in smart campuses, digital credentialing, and AI-powered student support. Local universities are adopting cloud-based learning systems, hybrid class delivery, and blockchain credential frameworks. EdTech firms in the region are partnering with governments to deliver AI-facilitated blended learning across more than 150 higher education institutions. Learner behavior here is shaped by high mobile penetration, growing international student mobility, and strong interest in globally recognized digital credentials.

United States – ~30% share - Dominance driven by robust R&D funding, a large number of research universities, and strong institutional tech adoption.

China – ~18% share - Rapid scaling of EdTech across universities, investments in AI tutoring, and growing private-public partnerships.

The Higher Education Technology market is moderately consolidated at the top while remaining fragmented across regional and niche segments. There are roughly 120–150 active competitors globally offering LMS, analytics, XR, credentialing, and classroom-collaboration solutions. The top five providers collectively command an estimated 40–48% combined share, reflecting concentration among platform incumbents while leaving substantial opportunity for specialized vendors. Strategic initiatives across the market in 2023–2024 included at least 35 major product launches, 18 strategic partnerships linking content and platform providers, and 11 M&A transactions aimed at integrating AI or expanding cloud infrastructure footprints. Competition is driven by differentiation in AI-driven analytics, generative-content capabilities, institutional integrations (SIS/ERP), and compliance-ready privacy tooling. Key positioning moves include bundling of predictive-retention modules with LMS suites, subscription-based pricing for adaptive learning engines, and managed-service offers for hybrid campus operations. Regional players in Asia and Latin America are expanding via localized language support and lower-cost deployment models, while global incumbents emphasize enterprise-grade security, analytics fidelity, and scalability for multi-campus deployments. Measurable indicators of competitive intensity include platform interoperability scores, average time-to-deploy (reported at 8–14 weeks for mid-sized campuses), customer renewal rates (above 82% for leading enterprise platforms), and annual release cadence (many leaders ship 3–6 major updates per year). These dynamics underscore a market where scale, institutional integrations, and continuous AI innovation determine long-term competitive positioning.

D2L (Brightspace)

Anthology

Microsoft (Education)

Google For Education

2U (including edX offerings)

Udemy

Chegg

Kaltura

Top Hat

Elsevier

EdCast

Technology trends shaping higher education are converging around intelligent learning experiences, secure credentialing, immersive skill labs, and scalable campus infrastructure. Generative AI and LLM integrations are being embedded into LMS content pipelines to auto-generate formative assessments, lecture summaries, and personalized study guides; in many pilot programs these tools reduce instructor prep time by 20–35%. Adaptive learning engines now analyze multi-modal learner signals—engagement, assessment performance, and resource usage—to produce individualized learning paths, with institutions reporting improvements in early-warning accuracy and retention interventions. Extended Reality (XR) platforms are scaling for STEM and clinical curricula: virtual labs and simulation modules are enabling institutions to deliver hands-on competency training to cohorts of 100–1,000 students without proportional increases in physical lab costs.

On the infrastructure side, cloud-native LMS architectures and headless learning platforms support API-first integrations with SIS, identity providers, and analytics lakes; centralized orchestration reduces per-site administrative overhead and enables A/B testing of learning interventions across campuses. Edge compute and optimized content-delivery networks are also important for low-latency video and VR streaming—critical where campuses serve distributed, remote learners. Blockchain and verifiable-credential frameworks are evolving for secure transcripting and cross-border recognition of micro-credentials; pilot networks now account for tens of thousands of digitally issued academic records in interoperable formats. Security and compliance technologies—privacy-preserving analytics, federated learning, and enterprise-grade access controls—are increasingly default requirements for institutional procurement, given rising breach attempts. Finally, analytics and institutional research stacks are integrating student-success metrics with operational KPIs (enrollment, yield, and retention) enabling data-driven budgeting and evidence-based pedagogy decisions for university leadership and academic units.

• In April 2024, Instructure announced an exclusive Canvas collaborative learning experience powered by Lucid Software, making the Lucid Education Suite available to Canvas customers at no extra cost and embedding visual collaboration tools across the LMS. Source: www.instructure.com

• In December 2023 and expanded in early 2024, Microsoft launched and broadened Copilot access for education—enabling faculty and eligible higher-education students to use Copilot for lesson planning, content creation, and classroom assistance under commercial data-protection terms. Source: www.microsoft.com/education

• In May 2024, Pearson expanded generative AI study tools into global editions of its higher-education titles, deploying beta AI study features across tens of thousands of students internationally and integrating automated study-assistants into selected course materials. Source: plc.pearson.com

• In May 2024, D2L Brightspace received industry recognition and announced platform enhancements at its Fusion event, highlighting new authoring and accessibility features and reinforcing Brightspace’s enterprise LMS positioning for higher education. Source: www.d2l.com

The report covers the full higher education technology ecosystem, including product categories such as learning management systems (LMS), student information systems (SIS), adaptive learning engines, assessment platforms, XR simulation labs, virtual classroom and proctoring tools, video and media platforms, institutional analytics and IR suites, digital credentialing and blockchain-based transcript systems, and smart-campus IoT integrations. Geographic coverage spans North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa with granular metrics on institutional digital maturity, cloud adoption rates, number of institutions deploying AI analytics, and the scale of XR lab rollouts. Application domains include undergraduate and graduate teaching, research-oriented lab simulation, continuing professional education, corporate university partnerships, and online and hybrid degree delivery. The report analyzes end-user segments—public research universities, private non-profit institutions, community colleges, vocational and technical schools, and lifelong-learning providers—detailing procurement cycles, deployment models (on-premise, cloud, and hybrid), and preferred commercial models (license, SaaS subscription, visioned managed services). It also examines enabling technologies—LLMs, federated learning, identity and access management, interoperability standards (LTI, xAPI), and content management pipelines—assessing integration complexity, institutional staffing readiness, and typical implementation timelines. Finally, practical decision frameworks are provided for institutional leaders and investors to evaluate vendor fit, scale pilots, and prioritize investments across student success, operational efficiency, and strategic digital transformation objectives.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 120,462.6 Million |

|

Market Revenue in 2032 |

USD 306,889.9 Million |

|

CAGR (2025 - 2032) |

12.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Instructure, Coursera, Pearson, D2L (Brightspace), Anthology, Microsoft (Education), Google For Education, 2U (including edX offerings), Udemy, Chegg, Kaltura, Top Hat, Elsevier, EdCast |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |