Reports

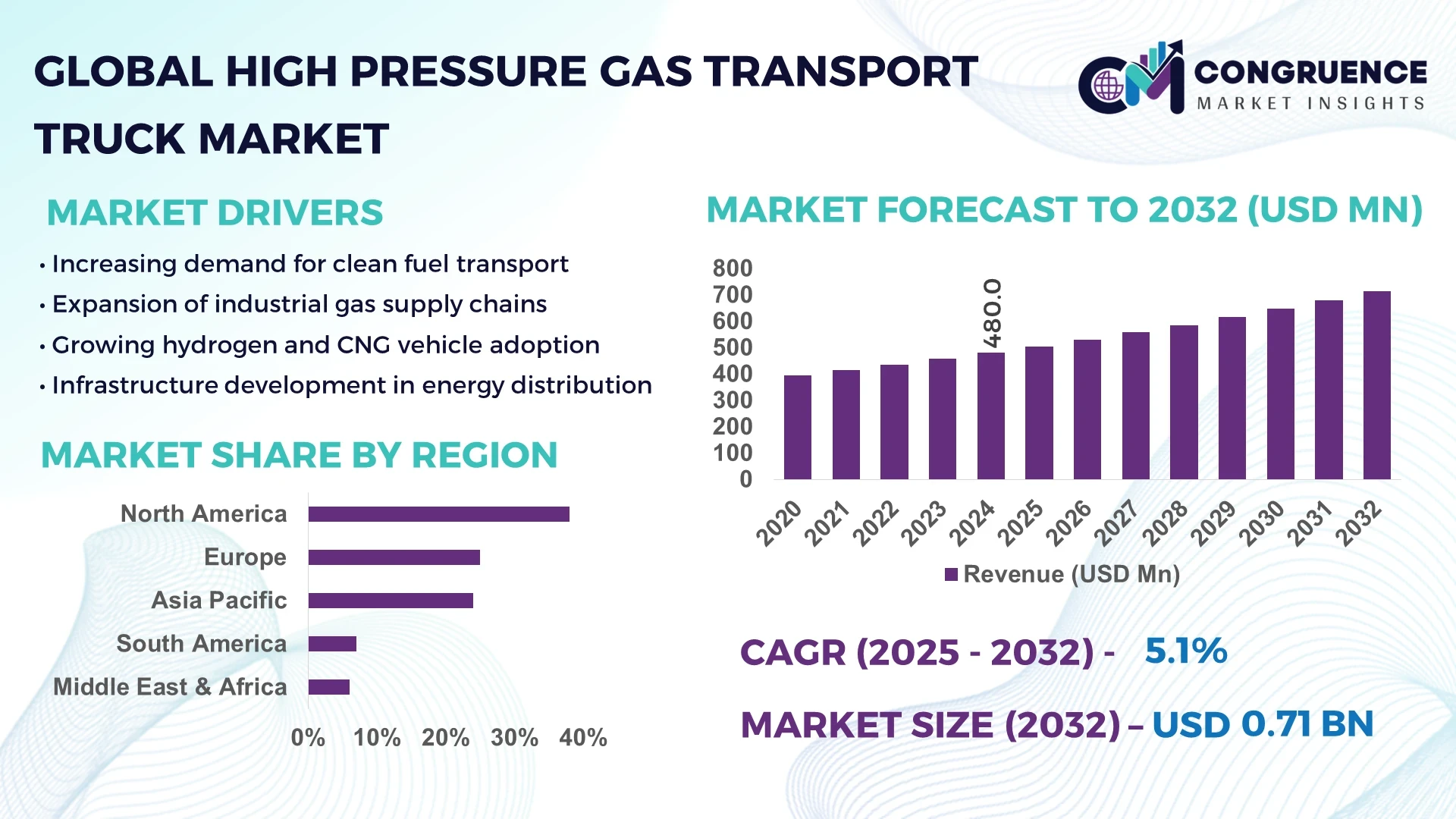

The Global High Pressure Gas Transport Truck Market was valued at USD 480.0 Million in 2024 and is anticipated to reach a value of USD 714.6 Million by 2032 expanding at a CAGR of 5.1% between 2025 and 2032.

The United States dominates the High Pressure Gas Transport Truck Market with significant production capacity supported by advanced manufacturing facilities and robust investment in clean energy transport technologies. Key applications include the transportation of compressed natural gas (CNG) and hydrogen for industrial and commercial sectors. The country has made substantial technological advancements in truck design, safety systems, and high-pressure tank integration, enabling more efficient and safer long-distance gas transport.

Globally, the High Pressure Gas Transport Truck Market is heavily influenced by the growth of natural gas, hydrogen, and other industrial gases across various sectors. The automotive and energy sectors contribute substantially to market demand, with specialized trucks designed for high-pressure gas transport. Recent technological innovations include lightweight composite pressure vessels, AI-driven fleet monitoring, and automated safety and leak-detection systems. Regulatory drivers, such as stringent emission standards and transportation safety mandates, encourage the adoption of modern, environmentally friendly trucks. Regional consumption patterns show high adoption in North America, Europe, and Asia-Pacific, with emerging economies increasingly investing in infrastructure for gas transport. The market is also seeing trends toward digitalized logistics, connected truck platforms, and modular vehicle design, indicating a strong outlook for efficiency and operational reliability.

Artificial Intelligence (AI) is playing an increasingly transformative role in the High Pressure Gas Transport Truck Market by enhancing operational efficiency, safety, and predictive maintenance. Fleet operators now leverage AI algorithms to optimize routing for trucks transporting high-pressure gases, reducing fuel consumption, transit times, and exposure to potential hazards. Advanced AI-powered monitoring systems are deployed to continuously analyze sensor data from pressure tanks, detecting anomalies or potential leakages before they escalate into safety incidents. The integration of AI in predictive maintenance helps fleet managers schedule repairs proactively, reducing unscheduled downtime and extending vehicle service life. In addition, AI is being used to improve load management, ensuring that pressure tanks are safely loaded and balanced to comply with regulatory standards, particularly for hazardous gases. Smart telematics systems powered by AI also enable real-time monitoring of temperature, pressure, and vehicle health, ensuring compliance with transport protocols. Across the High Pressure Gas Transport Truck Market, AI adoption contributes to higher operational reliability, reduced accidents, and more efficient logistics management, ultimately strengthening safety and economic performance for operators.

“In 2024, a U.S.-based fleet operator implemented an AI-based predictive monitoring system across its 150 high-pressure gas transport trucks, resulting in a 23% reduction in unscheduled maintenance events and a 17% improvement in operational efficiency within the first six months of deployment.”

The High Pressure Gas Transport Truck Market is influenced by growing industrial demand for compressed and liquefied gases, including natural gas, hydrogen, and industrial specialty gases. Increasing energy transition initiatives and a shift toward low-carbon fuel alternatives are driving investment in specialized transport trucks capable of handling high-pressure tanks safely. Market trends include the adoption of advanced composite pressure vessels, AI-enabled monitoring systems, and modular truck designs for better fleet scalability. Regional regulations around safety, emissions, and transport of hazardous materials shape operational strategies. Technological innovation, infrastructure development, and industry-specific requirements collectively influence demand, positioning the market for continued growth across key geographies.

The push toward hydrogen and compressed natural gas (CNG) for industrial, transportation, and commercial purposes is driving demand for high-pressure gas transport trucks. Expansion of hydrogen refueling stations, natural gas pipelines, and industrial gas facilities necessitates specialized vehicles capable of maintaining safety and efficiency under high pressure. Increasing fleet investments, public-private partnerships, and government incentives accelerate the development of next-generation trucks equipped with advanced safety, monitoring, and tank technologies. This trend directly supports market growth and encourages innovation in tank materials, automated safety systems, and fuel-efficient vehicle designs.

Compliance with rigorous safety, emissions, and hazardous material transport regulations presents a challenge in the High Pressure Gas Transport Truck Market. Companies must adhere to multiple national and international standards regarding tank design, leak detection, vehicle certification, and driver training. Meeting these regulatory requirements increases development and operational costs, slows vehicle deployment, and requires ongoing staff training. Fleet operators often face delays in approval for new vehicles or retrofitting existing trucks, which can limit market expansion and operational flexibility in emerging and mature markets.

The development of renewable energy sources such as hydrogen and biogas offers significant opportunities for high-pressure gas transport trucks. As countries invest in renewable energy infrastructure and clean fuel distribution networks, the demand for specialized transport vehicles capable of handling high-pressure gases safely rises. Innovations in modular vehicle design, lightweight tanks, and advanced monitoring systems provide a competitive edge. Market players can capitalize on untapped opportunities in emerging regions by introducing cost-effective, efficient, and safety-compliant vehicles tailored to renewable energy logistics needs.

High-pressure gas transport trucks involve complex manufacturing processes, including the use of advanced composite materials for pressure vessels, high-performance safety systems, and integrated monitoring technologies. These factors contribute to high initial costs and operational expenses. Additionally, maintenance of high-pressure tanks, leak detection systems, and regulatory compliance audits increases recurring costs. Fleet operators must balance safety and performance with economic feasibility, which may limit rapid market adoption in price-sensitive regions, posing a notable challenge for market expansion.

Rise in Modular and Prefabricated Vehicle Designs: The adoption of modular chassis and prefabricated pressure vessel integration is reshaping truck manufacturing, reducing assembly time by 20% and enabling rapid fleet scaling, particularly in Europe and North America.

Integration of AI-Based Safety Systems: Advanced AI algorithms are now deployed for real-time monitoring of tank pressure, leak detection, and route optimization, significantly reducing accidents and operational downtime.

Expansion of Hydrogen and CNG Refueling Infrastructure: Growth in renewable fuel stations and industrial gas facilities in Asia-Pacific and North America is increasing demand for specialized high-pressure transport trucks, driving adoption in new logistics networks.

Lightweight Composite Pressure Vessels: The use of carbon-fiber and high-strength alloy tanks is gaining traction to improve payload efficiency, reduce fuel consumption, and enhance vehicle safety standards, particularly for long-distance gas transport operations.

The High Pressure Gas Transport Truck Market is structured around three primary segmentation categories: Type, Application, and End-User. Each segment addresses unique industry requirements and operational needs. By type, trucks are differentiated by their gas handling capabilities, tank material, and vehicle design, allowing operators to select vehicles optimized for specific gases such as CNG, hydrogen, or industrial gases. Application segmentation focuses on sectors requiring high-pressure gas transport, including industrial operations, energy distribution, automotive fuel supply, and construction projects. End-user segmentation highlights the industries and organizations that operate or utilize these trucks, such as industrial gas suppliers, renewable energy companies, automotive fleet operators, and commercial logistics providers. Understanding these segments enables stakeholders to make informed investment, operational, and expansion decisions while optimizing safety, efficiency, and compliance within the global market landscape.

The High Pressure Gas Transport Truck Market is primarily segmented into CNG Transport Trucks, Hydrogen Transport Trucks, Industrial Gas Transport Trucks, and Specialty Gas Trucks. CNG Transport Trucks lead the market due to widespread adoption in energy distribution and urban fuel supply, providing reliable transport for compressed natural gas under stringent safety standards. Hydrogen Transport Trucks are the fastest-growing type, driven by the global transition toward clean energy and the expansion of hydrogen refueling infrastructure, particularly in Asia-Pacific and Europe. Industrial Gas Transport Trucks serve manufacturing plants, chemical facilities, and energy projects, often requiring heavy-duty tanks and pressure management systems. Specialty Gas Trucks, though smaller in volume, cater to niche applications such as medical gases, research laboratories, and high-purity industrial gases, offering precise handling, leak detection, and temperature control features. Collectively, the type segmentation reflects a balance between established fuel transport needs and emerging clean energy trends.

Applications for High Pressure Gas Transport Trucks include Industrial Gas Supply, Energy Distribution, Automotive Fueling, and Construction/Infrastructure Projects. Industrial Gas Supply is the leading application due to the large-scale transportation of oxygen, nitrogen, argon, and other gases for manufacturing and chemical processes, requiring high-capacity, pressure-compliant trucks. Energy Distribution, particularly the delivery of CNG and hydrogen to refueling stations, represents the fastest-growing application, spurred by global clean energy initiatives and urban fuel demand. Automotive Fueling applications support public and private CNG and hydrogen vehicle fleets, focusing on reliable and safe fuel delivery. Construction and Infrastructure Projects require high-pressure gas transport trucks for onsite gas delivery, including welding gases and industrial oxygen. This application contributes to regional demand in areas undergoing rapid industrialization or large-scale construction, reflecting both utility and safety considerations.

The High Pressure Gas Transport Truck Market serves a range of end-users, including Industrial Gas Companies, Energy Providers, Automotive Fleets, and Commercial/Logistics Operators. Industrial Gas Companies remain the leading end-user segment due to their consistent need for transporting large volumes of gases for manufacturing, healthcare, and chemical applications. Energy Providers, particularly those managing hydrogen and CNG networks, constitute the fastest-growing end-user segment, driven by renewable energy adoption and infrastructure expansion in emerging economies. Automotive Fleets also contribute significantly, particularly in regions with government mandates for low-emission vehicles, requiring high-pressure transport for fueling stations. Commercial and Logistics Operators serve niche markets, including laboratory gases and specialty chemicals, emphasizing safety compliance, real-time monitoring, and operational efficiency. Collectively, these end-users shape market demand, innovation adoption, and operational standards across the global High Pressure Gas Transport Truck Market.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2025 and 2032.

North America’s dominance is attributed to its well-established industrial gas infrastructure, high adoption of CNG and hydrogen-fueled transport trucks, and advanced manufacturing capabilities. Asia-Pacific’s rapid industrialization, expansion of renewable energy projects, and government incentives for clean fuel adoption are driving demand for high-pressure gas transport trucks. Additionally, regulatory compliance, technological innovations, and increasing investments in logistics infrastructure across these regions are shaping the competitive landscape, making both North America and Asia-Pacific pivotal for market expansion over the coming decade.

North America holds approximately 38% of the global High Pressure Gas Transport Truck Market, with strong demand from industrial gas suppliers, energy companies, and automotive sectors. Government incentives promoting CNG and hydrogen usage, along with stricter emissions regulations, encourage fleet modernization. Technological advancements, including AI-powered fleet monitoring, predictive maintenance, and telematics integration, are transforming operational efficiency and safety standards. Leading manufacturers in the region are investing in lightweight composite tanks, automated pressure management systems, and digitalized logistics platforms to optimize routes and reduce operating costs. These initiatives collectively reinforce North America’s leadership and continued market expansion.

Europe accounts for about 27% of the global market, with Germany, the UK, and France as key contributors. Regulatory bodies such as the European Commission and national transportation authorities enforce stringent safety and emission standards for high-pressure gas transport. The market is witnessing increased adoption of electric and hybrid-powered trucks equipped with high-pressure tank technologies, digital fleet management systems, and advanced leak detection. Sustainability initiatives, including EU clean energy directives and low-carbon transportation programs, are driving investments in innovative vehicles. Companies are deploying AI-enabled monitoring, automated safety systems, and lightweight materials to enhance operational efficiency and meet rigorous environmental compliance standards.

Asia-Pacific ranks as the second-largest market by volume, with China, India, and Japan leading adoption. Growing industrial activity, urbanization, and expanding renewable energy infrastructure are driving demand for specialized high-pressure gas transport trucks. Manufacturing hubs are implementing modern assembly lines for modular pressure vessels and integrating AI-based monitoring systems. Technology adoption is rising in logistics and safety compliance, including predictive maintenance and automated leak detection. Regional innovation hubs are focusing on lightweight composites, digital telematics, and energy-efficient truck designs. Government support for CNG and hydrogen infrastructure expansion, coupled with increased industrial gas consumption, positions Asia-Pacific as a key growth region.

South America accounts for roughly 12% of the global market, with Brazil and Argentina as primary contributors. Infrastructure improvements in industrial gas pipelines, renewable energy plants, and natural gas distribution networks are fueling demand. The region is witnessing investments in safety-enhanced high-pressure transport trucks, including advanced monitoring systems and lightweight tank technologies. Government incentives promoting CNG and industrial gas transport encourage fleet upgrades. Trade policies supporting energy imports and renewable energy adoption are further driving the market. The combination of increasing industrial activity, urbanization, and regional logistics modernization underpins continued growth in South America.

Middle East & Africa holds around 11% of the global market, with the UAE and South Africa driving adoption. Regional demand is fueled by oil & gas exploration, industrial gas consumption, and construction activities requiring safe high-pressure gas transport. Technological modernization includes digital fleet management, pressure monitoring, and AI-enabled leak detection. Governments are promoting investment in clean fuel logistics infrastructure and facilitating trade partnerships for industrial gas supply. The focus on industrialization, energy diversification, and safety compliance ensures steady growth and adoption of advanced high-pressure gas transport trucks in the region.

United States – 38% Market Share

Leading position due to high production capacity, advanced industrial gas infrastructure, and strong adoption of CNG and hydrogen transport fleets.

China – 22% Market Share

Dominance driven by rapid industrial expansion, growing renewable energy projects, and substantial investments in advanced high-pressure gas transport truck technologies.

The High Pressure Gas Transport Truck Market is characterized by a highly competitive environment, with more than 25 active global players operating across key regions including North America, Europe, and Asia-Pacific. Companies are strategically positioning themselves through technological innovation, product differentiation, and expansion of manufacturing capabilities. Strategic initiatives include partnerships with industrial gas suppliers, collaborations with renewable energy companies, and mergers to enhance production capacity and geographic reach. Product launches are focused on high-pressure tank integration, AI-powered monitoring systems, and lightweight composite designs to improve operational safety and efficiency. Innovation trends emphasize digitalization, including fleet management systems, predictive maintenance, and automated safety protocols. Market leaders are investing in R&D for hydrogen and CNG transport solutions, as well as modular truck platforms to streamline production and reduce lead times. Competitive positioning also includes regional adaptation to local regulatory frameworks, with firms enhancing compliance capabilities and providing specialized solutions tailored to industrial, automotive, and energy sectors. Overall, competition is intensifying as companies seek to balance safety, technology, and operational efficiency while expanding market reach globally.

Volvo Group

MAN Truck & Bus

Iveco S.p.A.

Tata Motors Limited

Hino Motors, Ltd.

FAW Jiefang

Dongfeng Motor Corporation

Scania AB

Ashok Leyland Limited

Hyundai Motor Company

Technological advancements are pivotal to the evolution of the High Pressure Gas Transport Truck Market. Current technologies include lightweight composite pressure vessels capable of handling high-pressure gases such as CNG, hydrogen, and industrial gases while reducing vehicle weight and improving fuel efficiency. AI-enabled telematics systems are being widely adopted for real-time pressure monitoring, predictive maintenance, and automated leak detection, enhancing safety and operational reliability. Digital fleet management platforms integrate GPS tracking, fuel consumption analysis, and route optimization to minimize operational costs and downtime. Emerging technologies focus on hydrogen-ready tanks, modular chassis designs for faster assembly, and enhanced crash protection systems for high-pressure vehicles. Additionally, advancements in thermal management ensure gas temperature stability during transport, critical for hydrogen and specialty gases. Smart sensors and IoT-enabled systems provide continuous diagnostics, allowing operators to anticipate mechanical issues before they become operational problems. Manufacturers are also experimenting with hybrid and electric truck platforms that integrate high-pressure gas transport capabilities, combining environmental compliance with energy efficiency. Collectively, these innovations are reshaping fleet operations, improving safety standards, and increasing the overall efficiency of high-pressure gas transport logistics.

In March 2023, Volvo Group launched its new CNG transport truck series featuring composite pressure vessels and enhanced AI-based monitoring systems, allowing operators to increase safety compliance and reduce maintenance downtime by 18%.

In August 2023, Tata Motors unveiled a hydrogen transport truck prototype with lightweight carbon-fiber tanks capable of handling 700 bar pressure, targeting industrial and energy distribution applications.

In January 2024, Scania AB introduced connected high-pressure gas trucks integrating real-time telematics, predictive maintenance, and route optimization, improving operational efficiency and reducing fuel consumption by 12% during field trials.

In May 2024, Hyundai Motor Company deployed a fleet of electric-powered high-pressure CNG trucks in South Korea, incorporating automated leak detection and advanced driver-assist features to enhance safety and operational efficiency.

The scope of the High Pressure Gas Transport Truck Market Report encompasses detailed insights into market segments, product types, applications, end-users, and geographic regions. The report analyzes trucks designed for the transportation of high-pressure gases including CNG, hydrogen, and industrial specialty gases. It covers segmentation by type, including CNG transport, hydrogen transport, industrial gas transport, and specialty gas trucks, and by application across industrial gas supply, energy distribution, automotive fueling, and construction. End-user analysis focuses on industrial gas companies, energy providers, automotive fleets, and commercial logistics operators. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting regional consumption patterns, infrastructure, and technological adoption. The report also evaluates current and emerging technologies, including lightweight composite tanks, AI-enabled monitoring systems, telematics platforms, modular chassis designs, and hybrid/electric integration. Additionally, it identifies key competitive dynamics, strategic initiatives, and innovation trends shaping global market operations. The analysis provides actionable insights for decision-makers, enabling strategic planning, market entry assessment, and investment prioritization across both mature and emerging regions.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 480.0 Million |

| Market Revenue (2032) | USD 714.6 Million |

| CAGR (2025–2032) | 5.1% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Volvo Group, MAN Truck & Bus, Iveco S.p.A., Tata Motors Limited, Hino Motors, Ltd., FAW Jiefang, Dongfeng Motor Corporation, Scania AB, Ashok Leyland Limited, Hyundai Motor Company |

| Customization & Pricing | Available on Request (10% Customization is Free) |