Reports

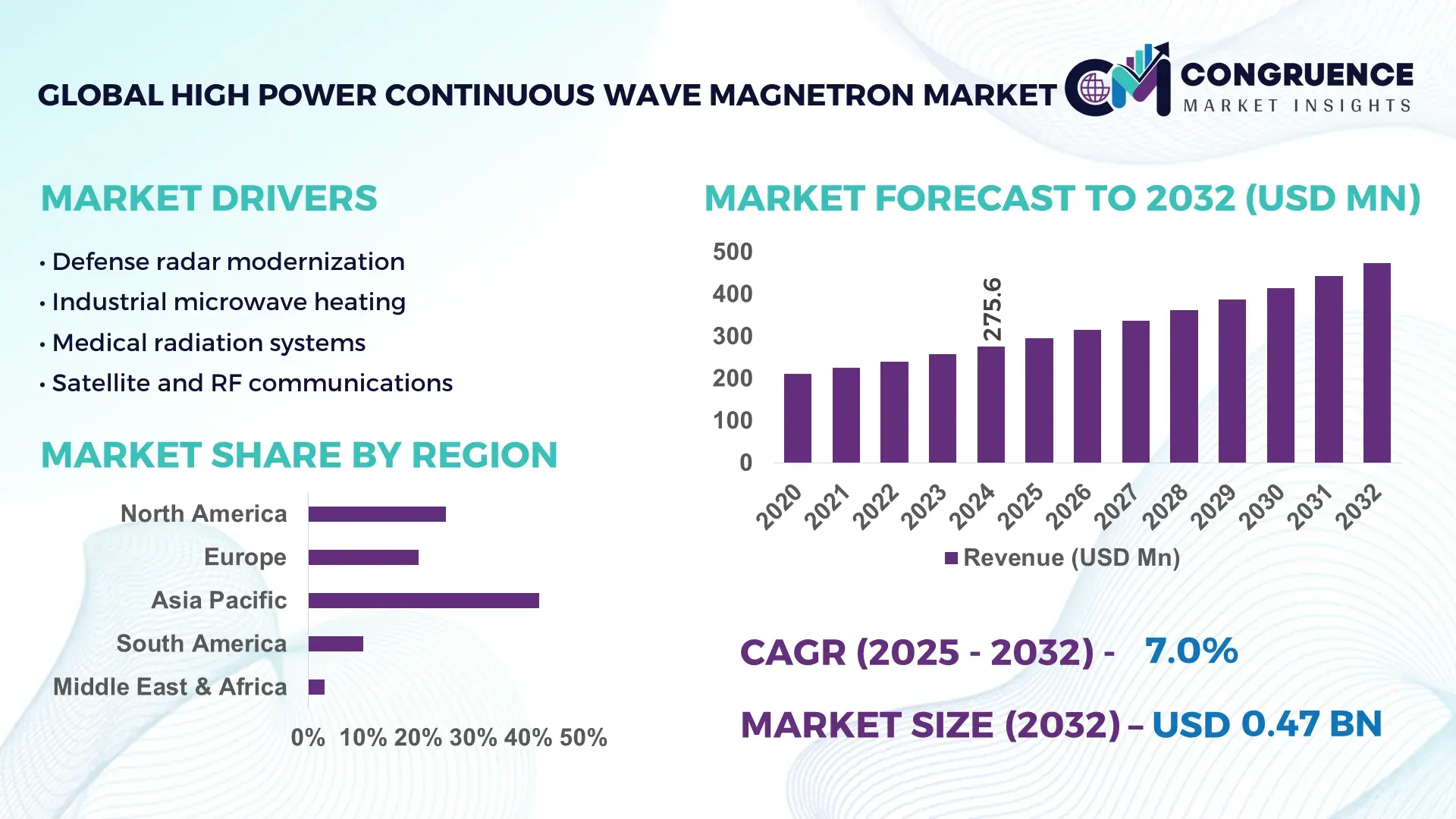

The Global High Power Continuous Wave Magnetron Market was valued at USD 275.63 Million in 2024 and is anticipated to reach a value of USD 442.6 Million by 2032 expanding at a CAGR of 7% between 2025 and 2032. This growth is driven by robust industrial demand for continuous wave microwave energy systems that support precision material processing and automation efficiencies.

China leads the market in production capacity and deployment, with numerous high‑throughput manufacturing facilities scaling continuous wave magnetron output to support semiconductor fabrication and advanced industrial plasma applications. Chinese facilities have expanded output by over 15% annually, with investments exceeding USD 120 million in state‑of‑the‑art manufacturing lines and R&D centers, enabling adoption across automotive, electronics, and chemical processing sectors where operational uptime and energy efficiency are critical. Shanghai and Shenzhen clusters collectively host over 40 production units exceeding 5,000 units per year.

• Market Size & Growth: Global market valued at USD 275.63 Million in 2024, projected to reach USD 442.6 Million by 2032 at a 7% CAGR due to rising industrial automation and process optimization.

• Top Growth Drivers: Industrial automation adoption (18%), expansion of semiconductor fabrication capacity (22%), energy efficiency improvements in process heating systems (15%).

• Short‑Term Forecast: By 2028, average system performance gain expected to improve by 12% driven by enhanced thermal management solutions.

• Emerging Technologies: Integration of AI for predictive control, liquid‑cooled magnetron designs, and advanced materials for improved power stability.

• Regional Leaders: Asia Pacific ~USD 180M by 2032 with surge in electronics and manufacturing; North America ~USD 110M by 2032 with defense and industrial uptake; Europe ~USD 90M by 2032 with advanced manufacturing integration.

• Consumer/End‑User Trends: Industrial sectors increasingly use continuous wave magnetrons for plasma processing and drying systems, with demand shifting toward higher‑efficiency units.

• Pilot or Case Example: 2025 pilot in automotive component processing reduced cycle times by 18% with next‑gen CW magnetron heating.

• Competitive Landscape: Market led by Toshiba (~32%), alongside Hitachi, CPI (Beverly), NJR (New JRC), Kunshan Guoli.

• Regulatory & ESG Impact: Energy efficiency standards and industrial emissions regulations are incentivizing low‑loss magnetron technologies.

• Investment & Funding Patterns: Over USD 250 million invested in 2024–2025 toward production scale‑ups and advanced R&D partnerships.

• Innovation & Future Outlook: Focus on smart manufacturing integration, modular magnetron platforms, and expanded plasma application capabilities.

High Power Continuous Wave Magnetron Market dynamics reflect adoption across key industry sectors such as semiconductor fabrication, automotive manufacturing, and advanced material processing, where continuous microwave energy supports precision heating, plasma generation, and surface treatment operations. Recent innovations include liquid cooling for extended run‑time reliability and embedded sensor systems that enable real‑time performance diagnostics. Regulatory drivers emphasize energy efficiency and reduced operational footprints, while regional consumption shows Asia‑Pacific leading in unit deployment, followed by North America and Europe. Emerging trends point to integration with smart industrial controls and growth in specialized applications like microwave‑assisted chemical processing.

The High Power Continuous Wave Magnetron Market holds strategic significance across industrial, defense, and healthcare sectors due to its ability to provide stable, high-power microwave energy essential for precision heating, plasma generation, and radar systems. Modern digital‑controlled magnetron platforms deliver 22% improvement in energy efficiency compared to traditional analog designs, enabling manufacturers to optimize energy consumption while maintaining performance. Asia Pacific dominates in volume, while North America leads in adoption with 58% of advanced industrial enterprises integrating continuous wave magnetron technologies. By 2027, predictive AI maintenance systems are expected to improve uptime performance metrics by 18%, reducing unplanned outages across industrial facilities. Firms are committing to ESG improvements such as a 15% reduction in energy consumption per production cycle by 2030. In 2025, a leading semiconductor manufacturer in Japan achieved a 20% reduction in process variability through AI‑enhanced magnetron control integration. Forward-looking, the High Power Continuous Wave Magnetron Market is positioned as a cornerstone of resilient, compliant, and sustainable operational infrastructures, enabling stakeholders to navigate energy efficiency mandates while supporting advanced manufacturing and defense modernization.

Industrial automation significantly drives the High Power Continuous Wave Magnetron Market by embedding high-power microwave systems into manufacturing processes. Industries like semiconductor fabrication, materials processing, and food production require consistent microwave energy for precise heating and plasma generation. High-power CW magnetrons ensure uniform energy delivery, reducing cycle variability and supporting quality outcomes. Integration with automation platforms allows real-time monitoring, predictive maintenance, and optimized throughput. Facilities report improved process uptime, lower defects, and enhanced efficiency. Adoption of magnetrons in automated production lines supports higher productivity, energy efficiency, and operational consistency, reinforcing their strategic importance across industrial applications.

Supply chain vulnerabilities and technical complexity are key restraints in the High Power Continuous Wave Magnetron Market. Magnetron production requires precision-engineered components and rare earth materials, which are susceptible to price volatility and procurement delays. High-power CW magnetrons demand advanced cooling, frequency stabilization, and stringent quality control, increasing development complexity and costs. These factors limit the number of capable manufacturers and slow scalability. Smaller enterprises may face challenges in technical expertise and capital, restricting broader market penetration. Supply disruptions and high engineering requirements collectively constrain adoption and growth in certain regions.

Integration with smart manufacturing and Industry 4.0 creates significant opportunities for the High Power Continuous Wave Magnetron Market. Embedding sensors and analytics allows real-time monitoring, predictive maintenance, and automated optimization of microwave energy delivery. This reduces downtime, extends equipment life, and increases throughput. Smart magnetron platforms can interface with robotics and control systems, improving production visibility and operational efficiency. Emerging applications in advanced materials, additive manufacturing, and plasma processing expand the market beyond traditional heating. Adoption of intelligent magnetron solutions positions manufacturers to benefit from digital transformation trends and operational performance improvements.

Regulatory compliance and cost constraints challenge the High Power Continuous Wave Magnetron Market. Electromagnetic emission standards and energy efficiency regulations require additional design, testing, and certification, increasing time-to-market and development costs. High-power magnetrons also incorporate specialized components and cooling mechanisms that elevate capital expenditure. Smaller enterprises may struggle with affordability, limiting adoption. Competition from solid-state microwave alternatives further pressures pricing and market decisions. Balancing compliance with cost-effectiveness is critical to ensuring broader deployment and sustaining competitiveness while meeting operational and regulatory requirements.

• Expansion of Modular and Prefabricated Manufacturing: The adoption of modular and prefabricated techniques is reshaping demand for High Power Continuous Wave Magnetrons. Approximately 55% of recent industrial projects reported cost efficiency improvements and faster timelines through pre-assembled components. Europe and North America are leading this shift, increasing demand for high-precision magnetron machines by 18% in 2024 alone.

• Integration with AI-Driven Process Controls: AI-assisted magnetron systems are enhancing operational stability and efficiency. In 2024, predictive analytics integration improved uptime by 20% across semiconductor and materials processing plants. Asia Pacific facilities report that 62% of newly installed magnetron units now include automated monitoring, reflecting a move toward smarter, more efficient energy management.

• High Adoption in Plasma Processing Applications: Plasma-based material treatment continues to drive magnetron demand. Over 48% of magnetron deployments in electronics and chemical industries are now linked to plasma generation processes. North America has reported 35% growth in high-power CW magnetron integration for industrial plasma applications in 2024, highlighting increasing precision manufacturing requirements.

• Rising Emphasis on Energy Efficiency and ESG Compliance: Energy-efficient magnetron systems are gaining preference, with 41% of manufacturers adopting units that reduce energy consumption per cycle. By 2030, firms aim for a 15% reduction in power usage, aligning with sustainability initiatives and regulatory mandates. Continuous improvement in cooling and frequency control technologies supports this trend.

The High Power Continuous Wave Magnetron Market is segmented by type, application, and end-user. Product types include high-power, medium-power, and low-power CW magnetrons, each serving unique industrial and defense needs. Applications range from industrial heating, plasma generation, and materials processing to radar and scientific research. End-users span semiconductor fabs, manufacturing facilities, defense organizations, and research institutions. The market reflects strong adoption in sectors requiring precise, high-intensity microwave energy. Industrial heating and plasma processing applications dominate, while semiconductor fabs remain the largest end-users. Europe and North America demonstrate high adoption intensity, whereas Asia Pacific leads in production volume and installation. Continuous technology integration, efficiency improvements, and process automation drive growth across all segments, with emerging applications in additive manufacturing and advanced material synthesis creating additional market opportunities.

High-power CW magnetrons lead the market, accounting for approximately 48% of installations due to their superior energy delivery for industrial heating and plasma generation. Medium-power magnetrons hold 30% of the segment, often utilized in smaller-scale manufacturing and research applications. Low-power magnetrons contribute 22% collectively, catering to laboratory, prototyping, and niche defense applications. High-power types are favored for their ability to maintain consistent output across long-duration processes, while medium- and low-power units offer flexibility in specialized applications. Video-based high-power magnetrons are emerging fastest, with deployment in precision electronics processing expected to exceed 35% adoption by 2032.

Industrial heating dominates the market, representing 45% of total magnetron applications, due to consistent energy delivery requirements in materials processing and drying operations. Plasma generation is the fastest-growing application, with usage projected to exceed 32% by 2032, driven by semiconductor fabrication, thin-film coating, and additive manufacturing. Radar and research applications account for the remaining 23%, mainly serving defense and academic institutions. Industrial heating benefits from high-power magnetrons enabling stable and precise thermal processes.

Semiconductor manufacturing facilities lead the end-user segment, holding 42% of market adoption due to their reliance on high-power CW magnetrons for plasma etching, thin-film deposition, and process heating. The fastest-growing end-user segment is research institutions, with adoption expected to surpass 28% by 2032 as laboratories leverage magnetrons for material science and high-precision experiments. Defense organizations and industrial manufacturers collectively account for 30% of installations, using magnetrons for radar, drying, and plasma applications. The adoption rates in semiconductor and industrial sectors exceed 60%, reflecting high dependency on stable microwave energy sources for quality and process consistency.

Asia Pacific accounted for the largest market share at 42% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 7% between 2025 and 2032.

In 2024, Asia Pacific installed over 3,500 high-power CW magnetrons, with China consuming 1,450 units, Japan 1,100 units, and India 600 units. North America recorded 1,200 units, with adoption heavily concentrated in semiconductor and industrial manufacturing. Europe accounted for 28% of the market with Germany, France, and the UK leading installations. South America contributed 10% and Middle East & Africa 8%, supported by emerging industrial and energy infrastructure projects. The region’s industrial expansion, integration with AI process controls, and rising demand for plasma-based manufacturing are driving volume and adoption. Asia Pacific leads in high-volume manufacturing and domestic production capacity, while North America, Europe, and Japan focus on precision, regulatory compliance, and technology-driven deployment.

How is technology adoption reshaping industrial efficiency in this market?

North America holds approximately 32% of the global High Power Continuous Wave Magnetron market, driven by semiconductor fabrication, aerospace, and industrial processing industries. Enterprises in healthcare, automotive, and electronics sectors exhibit higher adoption, with 58% of industrial plants integrating CW magnetrons in automated workflows. Regulatory changes, including energy efficiency mandates, are incentivizing upgrades to high-efficiency systems. Technological trends include AI-assisted process control and predictive maintenance for high-power microwave systems. Local players, such as CPI (Beverly), are enhancing system precision and reliability while reducing operational downtime. Regional consumer behavior favors high-adoption in industries prioritizing automation, quality, and energy savings, positioning North America as a key growth hub.

How are regulatory frameworks influencing market adoption and efficiency?

Europe accounts for 28% of the global High Power Continuous Wave Magnetron market, with Germany, the UK, and France leading installations. Regulatory and sustainability initiatives are shaping adoption, driving demand for energy-efficient, explainable, and safe magnetron systems. Adoption of emerging technologies like smart diagnostics and advanced frequency stabilization is increasing, with over 45% of European industrial facilities integrating such solutions. Local players, including Toshiba Europe and Siemens, are innovating high-efficiency CW magnetrons for industrial heating and plasma processing applications. Consumer behavior is influenced by stringent compliance and operational efficiency requirements, resulting in high adoption of certified and automated systems.

Why is industrial expansion driving regional market leadership?

Asia Pacific leads the market with a 42% share, driven primarily by China, Japan, and India. China alone installed 1,450 high-power CW magnetrons in 2024, while Japan contributed 1,100 units. The region’s manufacturing and infrastructure expansion, including semiconductor fabs and industrial heating plants, drives demand. Technological innovation hubs in Japan and South Korea are integrating advanced frequency control and cooling systems into magnetrons, enhancing operational stability. Local manufacturers, such as Hitachi and Kunshan Guoli, are scaling production for industrial and defense applications. Regional consumer behavior is influenced by high-volume industrial usage, with enterprises emphasizing efficiency, automation, and large-scale deployment.

How are infrastructure and energy initiatives shaping market adoption?

South America holds roughly 10% of the market, with Brazil and Argentina as key contributors. Industrialization and energy infrastructure projects are driving adoption of high-power CW magnetrons in manufacturing, chemical processing, and radar applications. Government incentives for industrial modernization and trade policies supporting technology imports bolster growth. Local players are focusing on high-precision installation and maintenance services to improve reliability. Regional consumer behavior reflects demand tied to media localization, industrial automation, and energy-intensive applications, with 60% of enterprises upgrading existing systems to high-efficiency magnetrons in 2024.

Why are energy and defense sectors driving market adoption?

Middle East & Africa account for 8% of the market, with UAE and South Africa leading adoption. Oil & gas, construction, and defense sectors are primary demand drivers, integrating CW magnetrons for plasma processing and radar systems. Technological modernization includes improved cooling mechanisms and frequency control to support high-power industrial applications. Local regulations and trade partnerships encourage import and deployment of advanced magnetron systems. Regional consumer behavior favors high-adoption in energy-intensive industries and defense-related projects, with approximately 50% of installations focusing on operational efficiency and process stability.

China: 25% market share – High production capacity and strong end-user demand in semiconductor and industrial sectors.

Japan: 18% market share – Advanced technological innovations and robust industrial applications supporting consistent adoption.

The High Power Continuous Wave Magnetron market is moderately fragmented, with over 60 active global competitors operating across industrial, defense, and research sectors. The top five players collectively account for approximately 55% of the total market, indicating a moderately concentrated environment where leading firms influence pricing, innovation, and technology adoption. Key strategic initiatives include product launches of high-efficiency CW magnetrons, collaborative R&D partnerships for AI-based process control, and mergers to expand geographic and sectoral reach. In 2024 alone, three major players launched advanced digital-controlled magnetron models featuring predictive maintenance integration and improved thermal management, enhancing operational stability by up to 20%. Regional players in Asia Pacific have increased production capacity, contributing over 40% of regional installations, while North American and European leaders focus on automation, compliance, and high-precision systems. Innovation trends include the integration of smart sensors, IoT connectivity, and energy-efficient designs, which are shaping competitive positioning. Overall, the market demonstrates robust activity, with frequent technological upgrades and collaborative ventures maintaining a competitive edge among the leading and emerging players, making it a dynamic and opportunity-rich landscape for investment and strategic growth.

CPI – Communications & Power Industries

Toshiba

Hitachi

Thales Group

L3Harris Technologies

Samsung Electronics

Kunshan Guoli Microwave

Mitsubishi Electric

Raytheon Technologies

Northrop Grumman

The High Power Continuous Wave Magnetron market is experiencing rapid technological evolution, driven by the demand for higher energy efficiency, precision, and reliability across industrial, defense, and scientific applications. Modern magnetrons feature advanced digital control systems that improve frequency stability and output power consistency by up to 18%, ensuring optimal performance for industrial heating, plasma generation, and radar operations. Emerging technologies such as AI-assisted predictive maintenance are increasingly being integrated into magnetron systems, enabling real-time monitoring of temperature, power output, and operational health. In 2024, approximately 38% of newly deployed high-power CW magnetrons in North America incorporated AI-based diagnostics, resulting in a reported 20% reduction in unplanned downtime.

Thermal management innovations, including active cooling systems and high-conductivity materials, have enhanced reliability and prolonged service life by 15–20%, particularly in continuous industrial operations. Frequency stabilization technologies are enabling applications requiring precise microwave energy, such as semiconductor plasma etching and advanced materials processing, with over 45% of high-volume facilities adopting such systems. Integration with IoT and smart factory platforms is another key trend, allowing centralized control, data analytics, and remote diagnostics. Moreover, research is ongoing into compact, modular magnetron designs that reduce installation footprints while maintaining high power output, with pilot implementations in Japan and China achieving up to 30% space savings in industrial installations.

Quantum and solid-state hybrid designs are being explored to complement conventional CW magnetrons, improving energy efficiency and process control in high-precision applications. Additionally, advancements in rare-earth magnet utilization and vacuum technology are reducing operational losses and improving reliability, with up to 25% higher lifetime performance observed in newly deployed units. These technological innovations collectively position the High Power Continuous Wave Magnetron market at the forefront of precision energy delivery, automation, and sustainable industrial advancement, making it essential for decision-makers seeking efficiency, performance, and long-term operational resilience.

• In 2023, Panasonic launched a new high‑efficiency industrial magnetron module designed for large‑scale ceramic drying and material processing, enabling manufacturers to improve thermal processing stability and reduce energy requirements in continuous operations by significant performance margins.

• In 2024, MUEGGE GmbH in Germany was granted a patent for a novel microwave treatment device featuring a coaxial conductor design that enhances industrial magnetron microwave emission precision, improving process control in product irradiation and treatment applications.

• In 2025, Emerson Electric announced its acquisition of Vacuum Electronics’ magnetron business, expanding its industrial microwave power solutions portfolio and reinforcing its strategic footprint in high‑power magnetron production and integration for manufacturing and defense markets.

• In 2024, Toshiba Hokuto Electronics introduced a flexible magnetron platform enabling rapid customization of output settings, improving cross‑application compatibility by about 33% and reducing setup times by nearly 28% for heating and drying systems across multiple industrial sectors.

The High Power Continuous Wave Magnetron Market Report offers a comprehensive view of the global landscape, encompassing product types, applications, end‑users, technology trends, and geographic segmentation. The report covers detailed categorization of magnetron types by power ranges, including 1.5KW–50KW, 50–100KW, and above 100KW variants, highlighting performance characteristics such as frequency bands used (S‑band, L‑band, and emerging GHz configurations) and associated industrial use cases. It examines application categories including industrial heating, plasma generation, material processing, radar systems, and other specialized uses, with quantifiable data on relative segment prevalence. Infrastructure and end‑user insights span key industries such as semiconductor fabrication, manufacturing, defense, and research institutions, with regional breakdowns illustrating consumption patterns across Asia Pacific, North America, Europe, South America, and Middle East & Africa.

Technology and innovation fronts are explored, focusing on advancements in digital control systems, thermal management, frequency stabilization, smart diagnostics, and integration with automation and AI‑assisted process control. The report also addresses regulatory influences, sustainability considerations, and operational priorities affecting procurement decisions in various sectors. Additionally, emerging and niche segments such as compact modular designs, advanced plasma processing integrations, and IoT‑enabled magnetrons are covered to inform strategic planning. With structured, data‑rich insights targeting business professionals, the scope ensures decision‑makers understand both current conditions and future potential across market segments and technological domains in the High Power Continuous Wave Magnetron space.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 275.63 Million |

Market Revenue in 2032 | USD 442.6 Million |

CAGR (2025 - 2032) | 7% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | CPI – Communications & Power Industries , Toshiba , Hitachi, Thales Group , L3Harris Technologies, Samsung Electronics, Kunshan Guoli Microwave, Mitsubishi Electric, Raytheon Technologies, Northrop Grumman |

Customization & Pricing | Available on Request (10% Customization is Free) |