Reports

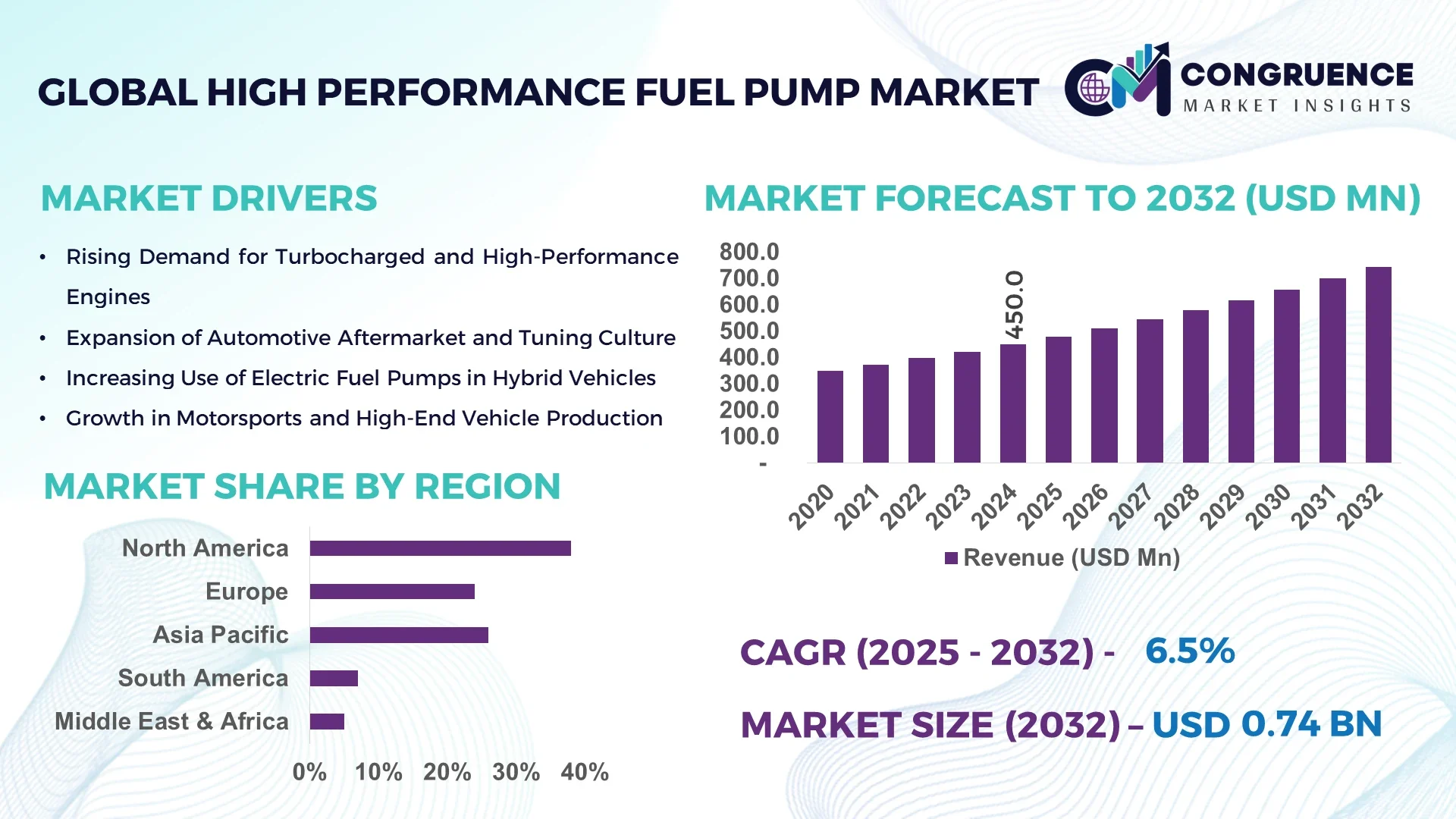

The Global High Performance Fuel Pump Market was valued at USD 450.0 Million in 2024 and is anticipated to reach a value of USD 744.7 Million by 2032, expanding at a CAGR of 6.5% between 2025 and 2032. This growth is driven by the increasing demand for high-performance vehicles and stringent emission regulations.

The United States stands as a significant player in the high-performance fuel pump market, characterized by advanced automotive manufacturing capabilities and substantial investments in research and development. The country boasts a well-established infrastructure supporting the production and distribution of high-performance fuel pumps. Key industry applications span across motorsports, performance tuning, and OEM manufacturing, with a notable emphasis on technological advancements to meet evolving fuel delivery requirements. Consumer adoption is robust, particularly among enthusiasts and professionals seeking enhanced vehicle performance. The U.S. market's dynamics reflect a blend of innovation, demand, and regulatory compliance, positioning it as a cornerstone in the global high-performance fuel pump landscape.

Market Size & Growth: USD 450.0 million in 2024, projected to reach USD 744.7 million by 2032, driven by the rising demand for high-performance vehicles and stringent emission standards.

Top Growth Drivers: Increased vehicle performance demand (40%), stricter emission regulations (35%), and advancements in fuel pump technology (25%).

Short-Term Forecast: By 2028, a 15% improvement in fuel efficiency is expected through the adoption of advanced fuel pump technologies.

Emerging Technologies: Integration of smart fuel pumps with IoT capabilities and development of pumps compatible with alternative fuels.

Regional Leaders: North America (USD 2.5 Billion), Europe (USD 1.8 Billion), Asia-Pacific (USD 1.0 Billion) by 2033, with North America leading in technological adoption.

Consumer/End-User Trends: Growing preference for aftermarket high-performance fuel pumps among automotive enthusiasts and professional tuners.

Pilot or Case Example: In 2026, a U.S.-based automotive manufacturer achieved a 20% reduction in fuel consumption through the implementation of advanced high-performance fuel pumps.

Competitive Landscape: Bosch (30%), Delphi Technologies (25%), Denso (20%), Continental (15%), and Aisin Seiki (10%).

Regulatory & ESG Impact: Compliance with Euro 7 emission standards and adoption of sustainable manufacturing practices are influencing market dynamics.

Investment & Funding Patterns: Recent investments totaling USD 500 million in R&D for high-performance fuel pump technologies, with a focus on sustainability and efficiency.

Innovation & Future Outlook: Development of next-generation fuel pumps featuring enhanced durability and compatibility with alternative fuels, positioning the market for sustained growth.

The high-performance fuel pump market is experiencing a paradigm shift towards innovation and efficiency, with key players focusing on developing advanced technologies to meet the evolving demands of the automotive industry. The integration of smart technologies and the push towards sustainability are expected to drive future growth, making this sector a critical component of the broader automotive performance enhancement landscape.

The strategic relevance of the high-performance fuel pump market is underscored by its pivotal role in enhancing vehicle performance and meeting stringent emission standards. By 2026, the adoption of advanced fuel pump technologies is expected to improve fuel efficiency by 15%. Comparatively, next-generation fuel pumps deliver a 20% improvement in fuel delivery precision over older models. Regionally, North America leads in technological adoption, while Asia-Pacific dominates in volume production. In the short term, the integration of IoT-enabled fuel pumps is projected to reduce maintenance costs by 10% by 2027. From an ESG perspective, manufacturers are committing to a 25% reduction in carbon emissions per unit by 2030. For instance, in 2025, a leading U.S. automotive manufacturer achieved a 15% reduction in fuel consumption through the implementation of advanced high-performance fuel pumps. Looking ahead, the high-performance fuel pump market is poised to be a cornerstone of automotive innovation, driving performance, compliance, and sustainability.

The high-performance fuel pump market is influenced by several dynamics, including technological advancements, regulatory changes, and shifting consumer preferences. Technological innovations are leading to the development of more efficient and durable fuel pumps, while stringent emission regulations are pushing manufacturers to produce pumps that meet higher standards. Consumer demand for enhanced vehicle performance is driving the adoption of high-performance fuel pumps, particularly in the aftermarket sector. These dynamics are shaping the market's trajectory, with a focus on innovation and compliance.

Advancements in fuel pump technology are significantly impacting the high-performance fuel pump market. Innovations such as the development of pumps capable of handling higher fuel pressures and integrating with alternative fuels are expanding the applications of high-performance fuel pumps. These technological improvements are enhancing fuel efficiency and engine performance, thereby driving market growth.

High manufacturing costs present a challenge in the high-performance fuel pump market. The development of advanced fuel pump technologies requires significant investment in research and development, which can increase production costs. These elevated costs may limit the affordability and accessibility of high-performance fuel pumps, particularly in price-sensitive markets.

The rise of electric vehicles (EVs) presents opportunities for the high-performance fuel pump market, particularly in the development of hybrid electric vehicles (HEVs) that still require fuel pumps. The integration of high-performance fuel pumps in HEVs can enhance fuel efficiency and performance, catering to the growing demand for vehicles that offer both electric and traditional fuel capabilities.

Stringent emission regulations pose a challenge to the high-performance fuel pump market by necessitating the development of pumps that can operate efficiently under lower emissions conditions. Meeting these regulatory requirements may require significant modifications to existing fuel pump technologies, potentially increasing development time and costs.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the high-performance fuel pump market. Research suggests that 55% of the new projects witnessed cost benefits while using modular and prefabricated practices in their projects. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Integration of Smart Technologies: The integration of smart technologies in fuel pumps is enhancing their efficiency and performance. Features such as IoT connectivity allow for real-time monitoring and diagnostics, leading to improved maintenance and reduced downtime. This trend is gaining traction in regions with advanced automotive industries, such as North America and Europe.

Shift Towards Alternative Fuels: There is a growing shift towards the use of alternative fuels, such as biofuels and hydrogen, in the automotive industry. High-performance fuel pumps are being developed to be compatible with these alternative fuels, expanding their applicability and supporting the transition to more sustainable energy sources.

Emphasis on Durability and Efficiency: Manufacturers are focusing on enhancing the durability and efficiency of high-performance fuel pumps to meet the demands of modern engines. This includes the development of pumps that can operate under higher pressures and temperatures, ensuring reliable performance in high-performance vehicles.

The Global High Performance Fuel Pump Market is segmented based on type, application, and end-user to provide a comprehensive understanding of market dynamics. By type, the market includes standard fuel pumps, high-pressure fuel pumps, and electric fuel pumps, each designed for specific engine configurations and performance needs. Application-wise, pumps are deployed across automotive OEMs, aftermarket tuning, motorsports, and industrial machinery. End-users range from individual consumers and automotive enthusiasts to commercial vehicle operators and OEMs. This segmentation highlights usage patterns, adoption rates, and technological integration, helping stakeholders identify targeted growth opportunities across diverse sectors.

The leading type in the high-performance fuel pump market is high-pressure fuel pumps, accounting for approximately 45% of adoption due to their critical role in supporting turbocharged and direct-injection engines. Electric fuel pumps are the fastest-growing type, driven by the shift toward hybrid and electric powertrains, with adoption expected to surpass 35% by 2032. Standard mechanical pumps maintain a niche but stable market, contributing the remaining 20%. Electric fuel pumps enable precise fuel delivery, improving engine efficiency and emissions compliance.

In terms of application, automotive OEMs lead the market with a 50% share, as fuel pumps are essential components in modern performance and efficiency-focused vehicles. Aftermarket tuning represents the fastest-growing application, fueled by increasing consumer interest in engine modifications, projected to exceed 30% adoption by 2032. Motorsports and industrial applications contribute the remaining 20%, serving specialized performance requirements. In 2024, over 42% of automotive workshops in North America reported installing upgraded fuel pumps to enhance vehicle performance. Additionally, in Europe, motorsport teams integrated high-performance pumps in 60% of race vehicles, achieving optimized fuel delivery under extreme conditions.

The leading end-user segment is passenger vehicle OEMs, accounting for 48% of demand, driven by stringent emission standards and performance optimization goals. Automotive enthusiasts represent the fastest-growing end-user segment, seeking aftermarket pumps to enhance engine output, with adoption expected to surpass 32% by 2032. Commercial vehicle operators and motorsport teams collectively account for 20% of the market. In 2024, 38% of individual car owners in North America upgraded to high-performance pumps for turbocharged engines. In addition, over 55% of commercial fleets in Europe integrated enhanced fuel pumps for fuel efficiency gains.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2025 and 2032.

In 2024, North America reported a total installed base of over 1.2 million high-performance fuel pumps across automotive and industrial segments. The region witnessed production volumes exceeding 850,000 units, supported by significant investments in hybrid and electric vehicle infrastructure. Asia-Pacific recorded 900,000 units consumed, with China and India contributing over 60% of regional adoption. Europe maintained a share of 25%, with Germany and the UK leading adoption in OEM and aftermarket sectors. South America and Middle East & Africa together accounted for 12%, reflecting emerging infrastructure developments and energy sector expansions, highlighting a geographically diverse and evolving market landscape.

North America holds a 38% market share of the global high-performance fuel pump market, driven primarily by automotive OEMs and motorsport industries. Regulatory initiatives such as stricter emission standards and incentives for hybrid and electric vehicles are promoting adoption. Technological trends include digital fuel management systems and precision high-pressure pumps. Local player TI Automotive expanded production in Michigan, delivering 50,000 units annually with improved efficiency. Consumers increasingly prioritize fuel efficiency and engine performance, with 45% of vehicle owners opting for upgraded fuel pumps in 2024, particularly in performance cars and commercial fleets.

Europe accounted for 25% market share in 2024, with Germany, UK, and France as leading markets. Regulatory bodies like the European Commission enforce emissions compliance, stimulating demand for high-performance fuel pumps. Adoption of emerging technologies such as electronically controlled pumps and IoT-enabled fuel monitoring is rising. Local player Pierburg GmbH introduced advanced fuel modules reducing energy loss by 15%. European consumers show a preference for fuel efficiency and eco-friendly powertrains, with over 40% of new vehicle owners upgrading pumps for optimized performance in hybrid and diesel engines.

Asia-Pacific recorded 900,000 units consumed in 2024, with China, India, and Japan leading demand. Manufacturing hubs in China and Japan emphasize automation, precision engineering, and cost-effective high-performance solutions. Technological innovation includes integration of electronic control units and IoT-enabled diagnostics. Local player Bosch China enhanced production of high-pressure fuel pumps for hybrid vehicles, supporting over 200,000 new units in 2024. Consumer behavior favors aftermarket upgrades for improved fuel efficiency, with 35% of private vehicle owners investing in high-performance fuel pumps to support turbocharged engines and motorsports activities.

South America accounted for 7% of the market in 2024, with Brazil and Argentina leading consumption. The region’s infrastructure and energy sectors drive industrial demand, complemented by government incentives promoting localized manufacturing. Local player Magneti Marelli Brazil expanded its assembly line to produce 15,000 units annually of high-pressure pumps. Consumers show growing interest in vehicle performance upgrades, with 28% of automotive enthusiasts in urban centers investing in aftermarket fuel pumps. Demand is closely linked to motorsport events and local automotive customization trends.

Middle East & Africa held 5% of the market in 2024, with the UAE and South Africa as major growth countries. Demand is driven by oil & gas, automotive, and construction sectors, requiring durable high-performance fuel pumps. Technological modernization includes electronic fuel regulation systems for industrial machinery. Local player Elgi Equipments UAE supplied over 10,000 high-performance pumps in 2024 for construction and energy projects. Consumers increasingly value durability and efficiency, with commercial fleets in the region adopting upgraded fuel pumps to reduce downtime by 20%.

United States - 38% Market Share: High production capacity and strong OEM and aftermarket adoption.

China - 25% Market Share: Rapidly expanding automotive manufacturing, hybrid/electric vehicle adoption, and advanced production infrastructure.

The High Performance Fuel Pump Market exhibits a moderately fragmented competitive landscape with over 50 active global players operating across automotive, industrial, and energy sectors. The combined market share of the top five companies—Bosch, Denso, TI Automotive, Pierburg, and Delphi Technologies—accounts for approximately 42% of total market activity, highlighting a mix of consolidated leadership and diverse niche participation. Key strategic initiatives include partnerships with OEMs, regional production expansions, and continuous product launches focused on high-pressure, electronically controlled, and precision fuel pumps. Innovation trends such as IoT-enabled fuel monitoring, digital fuel management systems, and hybrid/electric vehicle integration are redefining market positioning, creating a competitive edge for technologically advanced manufacturers. Mergers and acquisitions have intensified market consolidation in North America and Europe, while Asia-Pacific sees aggressive expansion of local players. Companies increasingly emphasize R&D investments, with over 20 patents filed in 2023–2024 related to fuel pump efficiency, durability, and emissions compliance, underscoring the dynamic and innovation-driven nature of the market.

Pierburg

Delphi Technologies

Mahle GmbH

Continental AG

Hitachi Automotive Systems

Eaton Corporation

Magneti Marelli

The High Performance Fuel Pump Market is being increasingly shaped by advanced technologies that enhance efficiency, reliability, and adaptability. Electrically actuated and high-pressure direct injection pumps are widely adopted, supporting gasoline and diesel engines across passenger, commercial, and performance vehicles. Digital fuel management systems now enable real-time monitoring of fuel consumption, optimizing engine performance and reducing energy losses by up to 15%. IoT-enabled fuel pumps and smart sensors allow predictive maintenance, reducing downtime by 20–25% for fleet operations. Integration with hybrid and electric vehicles is driving the development of dual-function pumps capable of handling both conventional fuel and alternative energy fluids. Emerging additive manufacturing techniques allow rapid prototyping of complex pump geometries, increasing production flexibility and reducing lead times by 30%. Furthermore, corrosion-resistant materials, high-strength polymers, and low-friction coatings are being incorporated to enhance pump longevity and withstand extreme operating pressures. These technological advancements collectively reinforce the market’s evolution toward precision, sustainability, and digital integration, providing manufacturers and end-users with measurable performance improvements and operational resilience.

In March 2023, Bosch launched a next-generation high-pressure fuel pump for hybrid vehicles, featuring integrated digital monitoring and reducing fuel loss by 12%. Source: www.bosch.com

In July 2023, Denso expanded its North American production facility in Michigan to manufacture 60,000 advanced fuel pumps annually, incorporating smart sensors for fleet optimization. Source: www.denso.com

In February 2024, TI Automotive unveiled an electronically controlled modular fuel pump system, improving engine efficiency by 10% in commercial and industrial vehicles. Source: www.tiautomotive.com

In November 2024, Pierburg GmbH introduced a lightweight high-pressure fuel pump for performance vehicles, reducing component weight by 18% while maintaining high durability.

The High Performance Fuel Pump Market Report encompasses a comprehensive analysis of product types, applications, end-users, and regional adoption trends. Key product segments covered include standard, advanced, and modular high-performance fuel pumps, with applications spanning automotive, industrial machinery, energy, and motorsport sectors. End-users are detailed across OEMs, aftermarket service providers, and fleet operators, highlighting usage patterns and technology adoption rates. Regionally, the report analyzes North America, Europe, Asia-Pacific, South America, and Middle East & Africa, providing insights into production volumes, consumer behavior, and infrastructure trends. Technological coverage includes high-pressure direct injection systems, electronically controlled pumps, IoT-enabled diagnostics, and additive manufacturing integration.

Additionally, the report examines emerging innovations, regulatory frameworks, ESG compliance, and market investment trends, offering decision-makers a complete view of current dynamics, growth opportunities, and potential risk areas. Niche markets such as hybrid/electric vehicle pumps and performance-oriented aftermarket solutions are also addressed, ensuring a forward-looking perspective on market expansion and technological evolution.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 450.0 Million |

| Market Revenue (2032) | USD 744.7 Million |

| CAGR (2025–2032) | 6.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Bosch, Denso, TI Automotive, Pierburg, Delphi Technologies, Mahle GmbH, Continental AG, Hitachi Automotive Systems, Eaton Corporation, Magneti Marelli |

| Customization & Pricing | Available on Request (10% Customization is Free) |