Reports

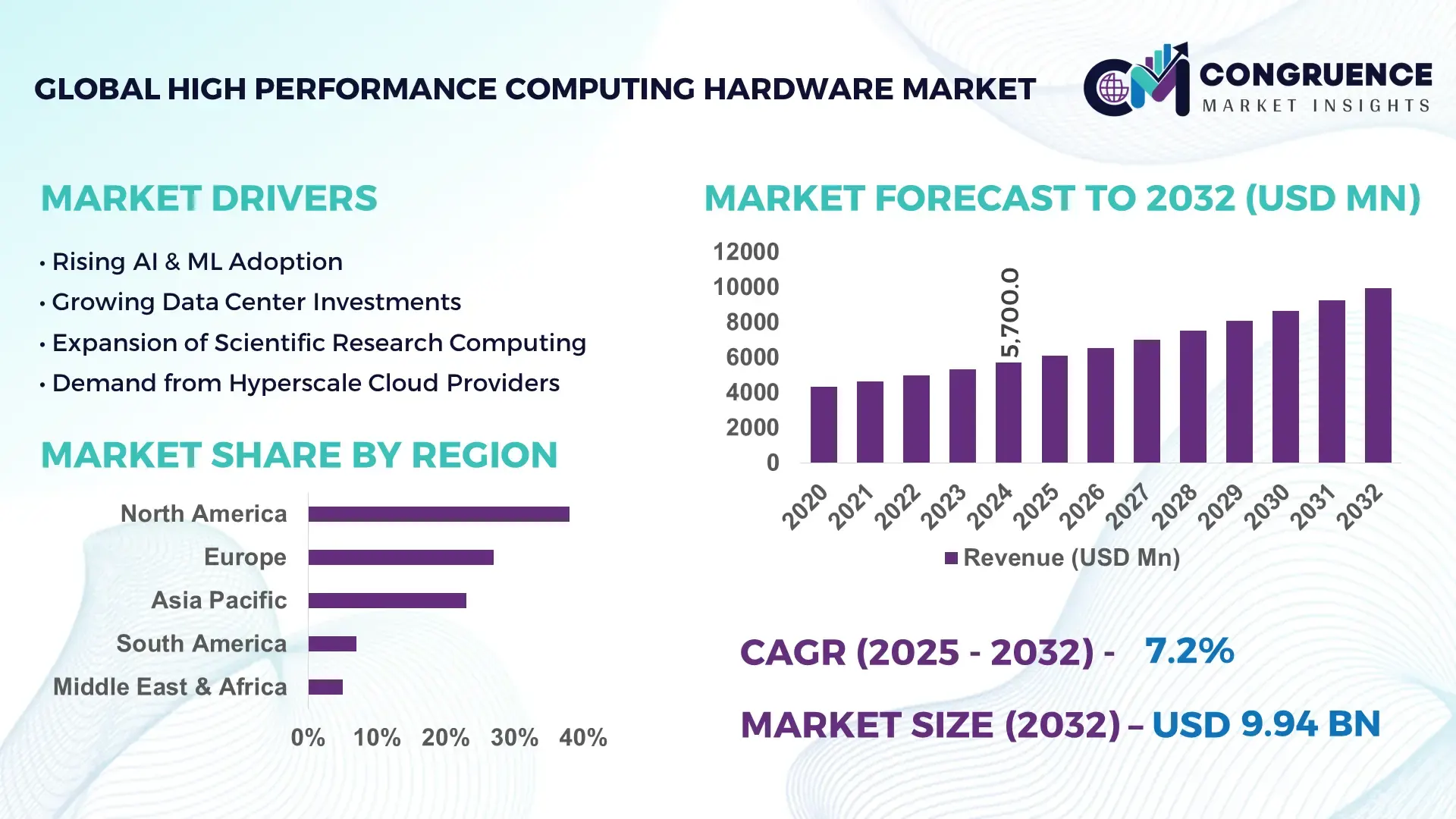

The Global High Performance Computing Hardware Market was valued at USD 5,700.0 Million in 2024 and is anticipated to reach a value of USD 9,941.1 Million by 2032 expanding at a CAGR of 7.2% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is primarily driven by increasing computational workloads across AI, climate modeling, and advanced engineering environments.

The United States maintains the world’s largest High Performance Computing Hardware ecosystem, supported by substantial federal and private investments exceeding USD 12.5 billion in advanced compute systems between 2020 and 2024. The country’s production capacity includes more than 60 exascale-class deployments and 480+ petascale nodes across national labs and hyperscale facilities. Its HPC infrastructure supports quantum simulation, genome research, aerospace modeling, and semiconductor design, with over 70% of Tier-1 research institutions integrating next-generation accelerators and liquid-cooling systems to boost energy efficiency and throughput.

Market Size & Growth: Valued at USD 5.7 billion in 2024 and projected to reach USD 9.94 billion by 2032 at a CAGR of 7.2%, driven by expanding AI-centric workloads.

Top Growth Drivers: 68% rise in AI/ML adoption, 42% improvement in processing efficiency, and 37% increase in cloud-based HPC utilization.

Short-Term Forecast: By 2028, compute performance per watt is expected to improve by 45% due to next-generation accelerator architectures.

Emerging Technologies: Rapid adoption of quantum-accelerated nodes, CXL-enabled memory pooling, and liquid-submersion cooling solutions.

Regional Leaders: North America expected to reach USD 3.2 billion by 2032 with high AI adoption; Europe projected at USD 2.6 billion driven by research programs; Asia Pacific to hit USD 2.9 billion led by hyperscale expansions.

Consumer/End-User Trends: Strong uptake among government research, automotive simulations, and BFSI risk-modeling applications.

Pilot or Case Example: In 2027, a European aerospace pilot achieved 39% faster simulation throughput using hybrid CPU-GPU clusters.

Competitive Landscape: Market leader holds ~18% share, followed by major players including Dell Technologies, HPE, Lenovo, Fujitsu, and IBM.

Regulatory & ESG Impact: Efficiency regulations encourage a shift toward systems delivering 30% lower energy consumption by 2030.

Investment & Funding Patterns: Global HPC infrastructure investments reached USD 8.4 billion recently, with rising venture funding in AI-optimized hardware start-ups.

Innovation & Future Outlook: Advancements in chiplet-based processors, neuromorphic add-ons, and scalable memory fabrics are expected to reshape compute paradigms.

The High Performance Computing Hardware Market is experiencing accelerated adoption from aerospace, healthcare analytics, and energy modeling sectors, supported by rapid advancements in GPU-dense clusters, chiplet processors, and advanced cooling technologies. Regulatory focus on energy-efficient compute infrastructure, combined with expanding procurement by national research institutes, is shaping stronger regional consumption patterns and fostering next-generation innovation across the ecosystem.

The High Performance Computing Hardware Market plays a central role in global digital transformation, enabling breakthroughs across AI, climate forecasting, healthcare modeling, semiconductor fabrication, and defense simulation. Strategic relevance is further strengthened by the measurable efficiency gains achieved through modern compute architectures. For example, CXL-enabled memory fabrics deliver up to 55% improvement compared to traditional non-coherent memory expansion, enabling larger simulation models and reducing compute bottlenecks. Regionally, North America dominates in volume, while Asia Pacific leads in adoption with 64% of enterprises/users integrating HPC-accelerated workloads across manufacturing and fintech segments.

By 2028, AI-driven dynamic scheduling is expected to cut job queue congestion by 35%, significantly improving cluster throughput for research institutions and enterprise users. Sustainability is becoming a priority, with firms committing to energy efficiency improvements such as 28% reduction in cooling energy by 2030 through liquid-immersion and direct-to-chip cooling systems.

A micro-scenario demonstrates the market’s advancement: In 2026, Japan achieved a 41% reduction in simulation time through its national AI-HPC integration initiative, enabling faster pharmaceutical discoveries and seismic modeling accuracy improvements.

Going forward, the High Performance Computing Hardware Market is positioned as a foundation for resilience, compliance, innovation, and sustainable digital growth, supporting mission-critical applications that demand extreme performance and energy-optimized infrastructure.

The High Performance Computing Hardware Market is shaped by evolving compute architectures, escalating data volumes, and rising adoption of AI and simulation workloads across industries. Demand is being influenced by advanced accelerators, high-bandwidth memory technologies, and energy-efficient cooling systems, which together are redefining cluster design principles. Industry trends also reflect growing investments in exascale-grade systems for scientific research, increased deployment of hybrid cloud HPC environments, and stronger integration with quantum-simulation frameworks. This market dynamic highlights the convergence of performance, efficiency, and scalability as key decision-making variables for enterprises and government institutions.

The accelerating complexity of AI, ML, and simulation workloads is significantly advancing the demand for high-performance computing hardware. Modern deep-learning models require up to 4× more compute power per generation, encouraging the deployment of GPU-dense clusters and high-bandwidth memory. Engineering simulations in aerospace, automotive, and energy sectors now involve models exceeding 500 million elements, increasing reliance on scalable CPU-GPU hybrid architectures. Furthermore, genomic sequencing pipelines generate over 25 petabytes of annual data, necessitating advanced compute accelerators for real-time analysis. These computational demands directly support greater investments in exascale-ready processors, high-speed interconnects, and scalable storage systems.

The High Performance Computing Hardware Market faces constraints arising from infrastructure limitations, operational complexity, and high energy requirements. HPC clusters often demand power densities above 60 kW per rack, outpacing the capabilities of many legacy data centers. Advanced cooling infrastructure, such as liquid-immersion systems, requires specialized deployment conditions and high upfront investment. Additionally, maintaining cluster efficiency demands skilled personnel, yet global shortages in HPC-specialized engineers continue to widen. Interoperability issues across heterogeneous architectures further complicate deployment, with enterprises reporting integration delays of 20–30% in hybrid environments. These factors collectively slow adoption rates and elevate operational overheads.

The emergence of exascale computing and quantum-assisted simulation presents major opportunities for the High Performance Computing Hardware Market. Nations are advancing exascale programs expected to increase compute capability by 10× compared to current petascale systems, creating demand for high-bandwidth accelerators, chiplet-based CPUs, and advanced interconnect fabrics. Quantum-HPC hybrid models also open pathways for solving optimization and material-science problems previously considered infeasible. Over 120 global research institutions are entering quantum-HPC pilots, driving demand for cryogenic-ready processors and highly modular compute nodes. These opportunities are further enhanced by industry-wide efforts to develop energy-efficient architectures through liquid cooling and silicon photonics.

The High Performance Computing Hardware Market encounters challenges stemming from high system acquisition costs and intricate integration demands. Advanced CPU-GPU cluster nodes can exceed USD 250,000 per unit due to specialized components such as tensor cores, HBM stacks, and high-speed fabrics. Integrating these systems into existing environments requires extensive customization, often extending deployment cycles by 6–12 months. The shift toward heterogeneous compute architectures also complicates workload scheduling and optimization, with enterprises reporting performance inefficiencies of up to 18% in unoptimized clusters. These challenges necessitate continued innovation in modular design, automation tooling, and cost-efficient deployment models.

Expansion of Accelerator-Rich Architectures: Demand for GPU-intensive and accelerator-driven systems is rising sharply, with enterprises deploying configurations delivering up to 38% higher parallel-processing efficiency and 52% faster AI inference throughput. Adoption of mixed-precision compute engines and HBM3 memory growth above 40% annually reflects the shift toward performance-dense nodes.

Growth in Liquid-Cooling Deployments: Liquid-cooling technologies are seeing a 47% increase in adoption due to rising rack power densities surpassing 50 kW. Immersion systems deliver 30–35% cooling energy savings and support higher thermal loads, enabling denser installations in research and hyperscale facilities adopting HPC workloads.

Rise of CXL-Enabled Scalable Memory Architectures: CXL-based memory pooling is expanding rapidly, with deployments projected to increase by 58% as enterprises aim to support large-scale models requiring over 20 TB of shared memory. This trend enhances flexibility and reduces memory bottlenecks across AI and simulation clusters.

Integration of Quantum-Hybrid Workflows: Quantum-hybrid HPC workflows are experiencing 33% annual growth in pilot deployments, enabling faster material-science and optimization outcomes. Early trials demonstrate up to 29% reduction in computation cycles for chemistry simulations and advanced analytics workloads integrating classical–quantum scheduling engines.

The High Performance Computing Hardware Market is structured around type, application, and end-user categories, each reflecting distinct technological and operational priorities influencing adoption. On the basis of type, the market is shaped by advanced processors, accelerators, storage solutions, and high-speed interconnects, each contributing to performance optimization in enterprise and research environments. Across applications, demand is centered on simulation, AI training, data analytics, and engineering workflows, driven by the rising scale of scientific and industrial computation. End-user adoption is influenced by sector-specific requirements, with domains such as government research, aerospace, healthcare, BFSI, and manufacturing embracing HPC infrastructure for enhanced modeling accuracy, risk forecasting, and real-time analytics. The overall segmentation highlights the strong convergence of high-density compute architectures with energy-efficient cooling, scalable memory technologies, and domain-specific workloads that shape procurement decisions and long-term infrastructure planning.

High Performance Computing Hardware encompasses several key types, including CPUs, GPUs, accelerators, high-performance storage arrays, and interconnect fabrics. CPUs currently lead the market, accounting for 46% of adoption, driven by their essential role in orchestration, general-purpose compute operations, and compatibility across legacy and modern workloads. GPUs hold 32% due to their superior parallel-processing capabilities for AI training and large-scale simulations. However, specialized accelerators such as tensor processors represent the fastest-growing segment, expanding at an estimated 11.8% CAGR, supported by rising demand for AI-optimized compute nodes and memory-intensive workloads. High-performance storage and interconnect solutions represent the remaining categories, collectively contributing 22% as critical enablers of throughput, bandwidth optimization, and data-parallel workloads. Growth in accelerator adoption is being driven by surging AI model complexity, with inference workloads growing more than 280% between 2021 and 2024. Memory bandwidth requirements exceeding 3 TB/s for next-generation AI models further amplify demand for custom accelerators and HBM-based architectures. Storage systems are also evolving, with NVMe-over-Fabric implementations rapidly increasing in hyperscale deployments.

The High Performance Computing Hardware Market supports a wide range of applications, including scientific simulation, AI and ML model training, data analytics, climate modeling, engineering design, and financial risk algorithms. Scientific simulation currently leads with a 41% share, powered by its reliance on petascale and emerging exascale infrastructures for physics, aerospace, genomics, and energy modeling. AI training accounts for 29%, while engineering design and analytics together represent 25%. However, AI-driven analytics is the fastest-growing application segment, expanding at an estimated 12.6% CAGR, fueled by rapid enterprise digitalization, increasing model size, and rising use of multimodal ML frameworks. Remaining niche applications contribute a combined 5%, including cybersecurity modeling, seismic analysis, and computational chemistry. In 2024, more than 38% of enterprises globally reported piloting HPC-enabled AI systems for internal automation and customer-facing use cases. In healthcare, 42% of hospitals in the US are testing AI-assisted diagnostic tools that combine imaging data with electronic health records for faster outcomes. This demand is further driven by increased precision requirements in aerospace simulations, where HPC clusters support models above 600 million finite elements.

The end-user landscape for High Performance Computing Hardware spans government research institutions, academia, aerospace and defense, healthcare, manufacturing, BFSI, and energy sectors. Government and research institutions lead with a 39% share, supported by national programs in climate modeling, astrophysics, nuclear research, and exascale development. Academia and healthcare collectively account for 28%, while BFSI, manufacturing, and energy sectors contribute 26% due to expanding needs for real-time analytics, digital twins, and predictive modeling. The fastest-growing end-user segment is healthcare, expanding at an estimated 13.4% CAGR, propelled by rising adoption of AI-enabled diagnostics, genomics, and medical simulation systems. Remaining industries represent a combined 7%, often engaging in niche or early-stage HPC deployments. Industry trends show strong momentum: in 2024, more than 38% of enterprises globally reported piloting HPC-driven AI systems for operational improvements. Meanwhile, over 60% of Gen Z consumers prefer brands that use advanced compute-enabled AI systems for personalized services, demonstrating growing end-user expectations. In manufacturing, digital twin deployments increased by 33% between 2022 and 2024, requiring sophisticated compute backbones.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.4% between 2025 and 2032.

Europe followed with 29%, driven by rapid digital infrastructure upgrades, while South America and the Middle East & Africa collectively contributed 14% through expanding enterprise AI workloads. Higher adoption of exascale systems, increasing deployment of GPU-dense clusters, and rising investments in national supercomputing programs enhanced regional competitiveness. Asia-Pacific’s surge is supported by strong semiconductor manufacturing bases, rapid hyperscale data center expansion exceeding 24,000 MW IT load capacity, and government-backed HPC modernization initiatives. Europe recorded more than 420 petaflops of new HPC capacity additions in 2024, demonstrating strong cross-border research collaborations. Meanwhile, North America maintained over 55% adoption of HPC in finance and healthcare analytics, reflecting mature enterprise integration of high-density compute nodes and advanced accelerators.

North America held approximately 38% of the global High Performance Computing Hardware Market in 2024, supported by strong adoption across healthcare, aerospace, BFSI, life sciences, and defense. Demand is driven by large enterprise AI deployments, increasing use of digital twins, and higher requirements for real-time risk modeling. Federal investments in national labs and strategic semiconductor initiatives continue to accelerate HPC infrastructure expansion. Regulatory frameworks strengthening data protection and AI risk management also influence adoption patterns. Key technological advancements include rapid upgrades to GPU-dense systems, high-bandwidth memory configurations exceeding 2 TB/s, and widespread adoption of chiplet-based architectures. A notable regional player expanded its AI-optimized HPC cluster to more than 600 petaflops to support pharmaceutical research and high-resolution medical imaging. Consumer behavior trends indicate higher adoption in healthcare and finance, where institutions deploy HPC to accelerate diagnostics, fraud analytics, and algorithmic trading. Enterprises increasingly prioritize energy-efficient cooling systems, with liquid cooling adoption rising 27% between 2022 and 2024.

Europe accounted for 29% of the global High Performance Computing Hardware Market in 2024, with Germany, France, and the UK representing over 68% of the region’s total consumption. Strong policy support for data sovereignty, climate modeling, and sustainable digital infrastructure fuels demand for high-performance systems. The European Green Computing initiatives and cross-border R&D programs have accelerated the deployment of energy-efficient exascale-ready systems. Regulatory pressure requires transparent and explainable AI model outputs, increasing reliance on HPC clusters for computational governance and model validation. The region continues to upgrade its semiconductor and quantum research capabilities, with more than 350 petaflops of new HPC capacity added in 2024 alone. A leading European supercomputing center introduced new AI-accelerated nodes to support automotive and materials science simulations. Consumer behavior signals a demand for explainable and regulation-compliant AI, shaping regional purchasing decisions. Emerging trends include liquid-immersion cooling, optical interconnects, and federated HPC models across research networks.

Asia-Pacific is the fastest-growing region in the High Performance Computing Hardware Market, accounting for 25% of global consumption in 2024 and ranking first in installed HPC volume expansion. China, Japan, India, and South Korea remain dominant markets, collectively contributing more than 78% of the region’s HPC capacity. Strong manufacturing ecosystems, rapid hyperscale data center growth, and increased semiconductor fabrication capabilities support significant regional progress. China continues to scale petascale and exascale systems, while India’s national AI mission fuels large-scale HPC adoption across healthcare and governance. New innovation hubs in Singapore, Shenzhen, and Bengaluru are accelerating advancements in AI-dedicated processors and low-latency interconnect technologies. A notable regional HPC provider recently deployed over 400 petaflops of GPU-powered compute to support autonomous vehicle training and telecom network optimization. Consumer behavior indicates strong momentum in e-commerce, mobile AI applications, and digital payments, increasing the need for high-throughput compute across enterprises.

South America contributed approximately 7% of global High Performance Computing Hardware Market demand in 2024, led by Brazil and Argentina, which together account for 62% of the region’s HPC deployment. Investments in energy sector modeling, financial analytics, and agriculture optimization solutions are driving steady adoption. Brazil’s expanding cloud and data center ecosystem is accelerating HPC utilization, particularly in the oil and gas sector where high-fidelity seismic modeling requires advanced compute infrastructure. Several governments introduced incentives for digital innovation and AI ecosystem development, supporting procurement of GPU-accelerated systems. A notable regional institution recently integrated a 50-petaflop compute cluster to support climate and crop yield simulations. Consumer behavior trends reveal increasing use of media, streaming, and language localization technologies, all of which require high-performance computation for real-time processing. Emerging adoption in education and public research further strengthens regional growth.

The Middle East & Africa represented 5% of the global High Performance Computing Hardware Market in 2024, driven primarily by the UAE, Saudi Arabia, South Africa, and Israel. Regional demand is strongly influenced by oil & gas reservoir modeling, smart city infrastructure, construction analytics, and cybersecurity modernization. Countries such as the UAE continue investing heavily in national AI strategies, resulting in rapid expansion of HPC-backed research labs and digital government services. Technological modernization includes adoption of GPU-based clusters, AI-optimized storage systems, and expansion of sovereign cloud infrastructure. A leading energy firm in the Gulf region deployed a new 80-petaflop HPC system to support subsurface imaging and real-time drilling optimization. Regional consumer behavior trends indicate growing demand for AI-enabled public services, advanced digital payments, and automated logistics, requiring large-scale compute backbones. Cross-border collaborations and digital trade partnerships further enhance HPC adoption.

United States – 32% Market Share: Strong leadership in semiconductor design, enterprise AI deployments, and national research infrastructure drives dominance in the High Performance Computing Hardware Market.

China – 27% Market Share: Extensive manufacturing capacity, rapid data center expansion, and large-scale government-backed HPC programs reinforce China’s leading position in the High Performance Computing Hardware Market.

The High Performance Computing Hardware Market presents a moderately consolidated competitive environment with approximately 70 to 90 active global competitors offering servers, accelerators, storage solutions, and integrated HPC systems. The combined market share of the top 5 companies is estimated at around 55%, indicating that while a handful of leading firms dominate core offerings, there remains significant room for smaller players and niche specialists. Key players are increasingly engaged in partnerships, product launches, and strategic acquisitions to retain leadership and expand their footprint. For example, one vendor introduced a new portfolio of liquid-cooled supercomputing systems in late 2024, enhancing performance per rack by over 25%. Another strategic initiative involved a contract to deliver a next-generation flagship supercomputer for a national research lab, securing multi-year hardware supply and service commitments. Innovation trends in the market include chiplet-based CPUs, high-bandwidth memory (HBM) stacks, high-speed interconnect fabrics, and immersion cooling technologies – all shaping hardware differentiation. Additionally, systems integrators are bundling HPC hardware with “HPC-as-a-Service” platforms, enabling enterprise buyers to shift from capital expenditure to usage-based models. With continuous R&D and ecosystem extensions, companies aim to secure long-term commitments from research institutions, hyperscalers, and government programs, turning hardware procurement into strategic engagement rather than a one-time sale.

NVIDIA Corporation

Intel Corporation

Fujitsu Limited

Supermicro, Inc.

AMD (Advanced Micro Devices, Inc.)

Current and emerging technologies are reshaping the High Performance Computing Hardware Market by enabling higher performance, greater efficiency, and more flexible deployment models. Key current technologies include GPU-dense clusters, high-bandwidth memory (HBM2/3), NVLink or comparable high-speed interconnects, and liquid-immersion or direct liquid-cooled systems. For instance, modern systems now integrate memory bandwidth in excess of 3 TB/s per node, enabling large-scale AI model training and high-fidelity simulation workflows. On the storage side, NVMe-over-Fabric and parallel file systems provide IOPS improvements of 30–40% per rack over previous generations.

Emerging technologies with business impact include chiplet-based CPU/accelerator packages, heterogeneous compute architectures combining CPUs, GPUs and tensor-cores, and scalable memory pooling via CXL (Compute Express Link) fabrics. These enable consolidated workflows blending scientific simulation and AI training on a single platform. For example, memory-pooled nodes enable shared access to 20 TB+ of coherent memory per rack. Additionally, modular rack-level architectures allow system expansion in blocks of 2–4 MW IT load, supporting hyperscale and research use-cases.

Another notable trend is the integration of HPC and AI workflows; organizational studies show over 90 % of academic HPC centres have introduced AI-enabled workloads on existing compute infrastructure, requiring hardware capable of mixed precision and large batch sizes. Thermal and power constraints are being addressed through liquid cooling, enabling rack power densities exceeding 80 kW while reducing cooling energy by up to 30 %. Edge and hybrid cloud HPC extensions are also gaining traction, enabling distributed high-performance hardware to support regional data sovereignty and low-latency workloads for industrial simulations.

In summary, the hardware market is transitioning from purely raw compute to performance-per-watt and ecosystem support, with decision-makers focusing on accelerator integration, scalable memory fabrics, energy-efficient cooling, and hybrid deployment models. Vendors competing in this space must demonstrate clear differentiation in throughput, latency, workload flexibility, and managed service capability to meet enterprise and research buyer requirements.

In November 2024, Hewlett Packard Enterprise (HPE) delivered the “El Capitan” supercomputer to Lawrence Livermore National Laboratory — a fully direct liquid‑cooled exascale system achieving 1.742 exaflops and 58.89 gigaflops per watt, ranking among the top energy-efficient machines. Source: www.hpe.com

In October 2024, HPE introduced the industry’s first 100% fanless direct liquid cooling architecture, cutting cooling power per blade by 37%, reducing utility costs and carbon emissions. Source: www.hpe.com

In December 2024, HPE was contracted by the Leibniz Supercomputing Centre (LRZ) to build the “Blue Lion” supercomputer: a 100% liquid-cooled HPE Cray system using NVIDIA accelerators, projected to deliver ~30× more compute power than its predecessor. Source: www.hpe.com

In March 2024, IBM signed an MoU with India’s C‑DAC to accelerate HPC processor design and system development across research organizations, academic institutions, and start-ups in India, with a focus on Power processors and open‑source ecosystem building. Source: in.newsroom.ibm.com

This report examines the High Performance Computing Hardware Market from the perspective of product type, application domain, end-user segment and geographic region. On the product side, it addresses compute servers, accelerators (GPUs, tensor processors), high-performance storage arrays, interconnect fabrics and cooling infrastructure such as rack-level liquid immersion systems. In applications, the report covers scientific simulation (physics, climate, aerospace), AI model training and inference (large language models, generative AI), engineering and design workflows (automotive, semiconductor, energy), data analytics and financial modelling. End-user segments include government and research institutions, academia, aerospace & defense, healthcare, manufacturing, BFSI, energy and hyperscale cloud providers. The geographic scope spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, analysing regional infrastructure trends, national programmes, and adoption behaviour. It also highlights niche and emerging segments such as edge-HPC deployments, HPC-as-a-Service models, hybrid cloud-HPC systems and quantum-classical hybrid architectures. The report offers decision-makers a structured view of market size by segmentation, technology trends, vendor strategies, procurement criteria, sustainability and ESG considerations, and investment patterns across global regions and industry verticals.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 5,700.0 Million |

| Market Revenue (2032) | USD 9,941.1 Million |

| CAGR (2025–2032) | 7.2% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Dell Technologies, Hewlett Packard Enterprise, IBM Corporation, NVIDIA Corporation, Intel Corporation, Fujitsu Limited, Supermicro, Inc., AMD (Advanced Micro Devices, Inc.) |

| Customization & Pricing | Available on Request (10% Customization is Free) |