Reports

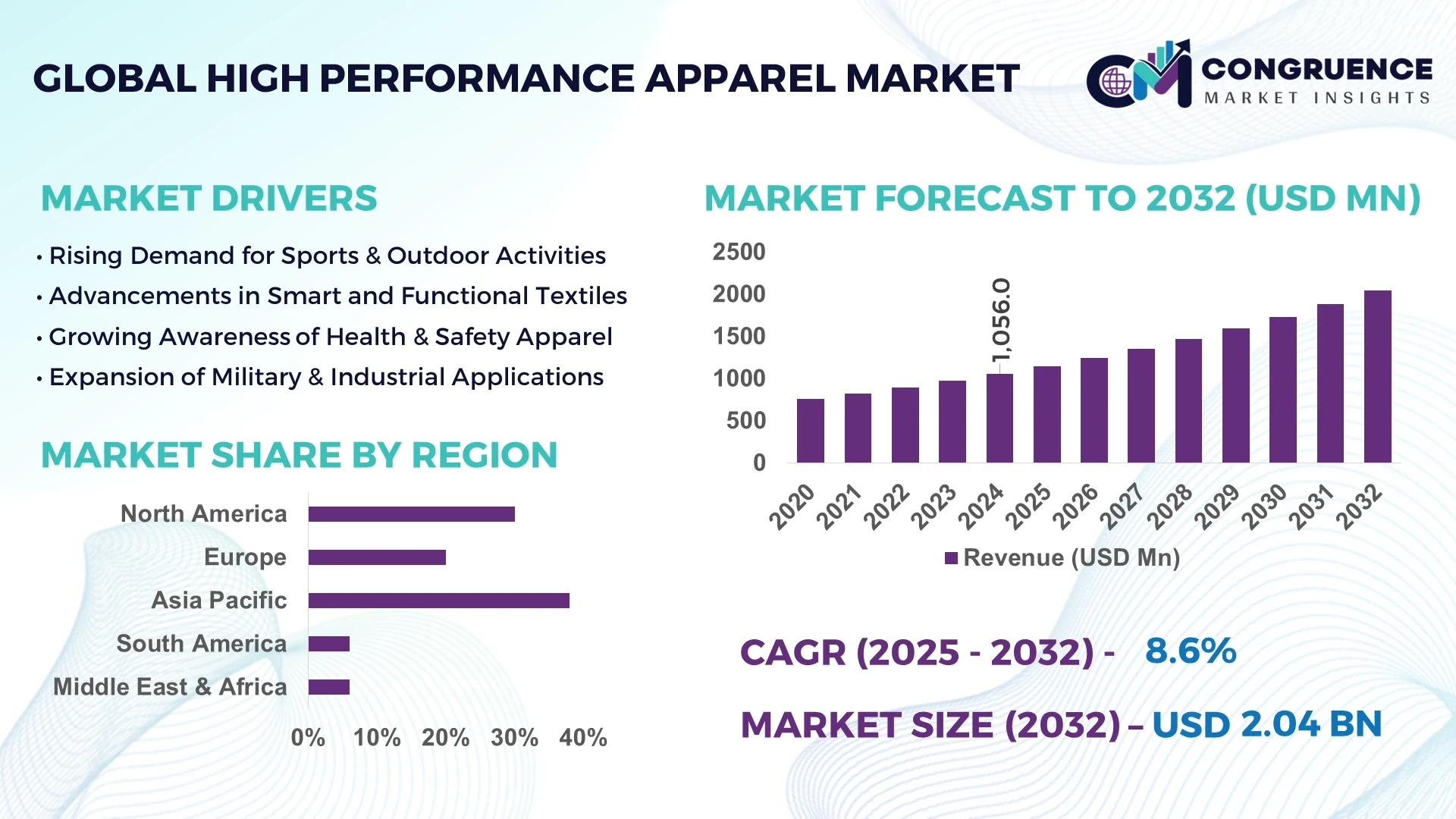

The Global High Performance Apparel Market was valued at USD 1,056.0 Million in 2024 and is anticipated to reach a value of USD 2,043.2 Million by 2032 expanding at a CAGR of 8.6% between 2025 and 2032.

In China, which dominates the High Performance Apparel Market, production capacity has expanded significantly in recent years with over 1,200 textile and garment facilities equipped for precision cutting, moisture-wicking and UV-protective fabrics. Investment levels remain high: government-backed R&D funds and private firms have committed over USD 500 million in smart textile innovation. Key industry applications include athletic wear, workwear, and military gear incorporating antimicrobial finishes and advanced thermal regulation. Technological advancements include integration of nanofiber membranes, smart textile sensors and automated defect detection in fabric finishing lines.

Unique information on the High Performance Apparel Market globally:

The market is segmented by application, including sportswear, protective clothing, outdoor wear and military apparel. Sportswear constitutes the largest share of demand, accounting for more than half of unit volumes in many developed markets, followed by protective clothing which is rising steadily due to stricter safety regulations in industrial sectors. Recent technological and product innovations include moisture-wicking materials, UV-resistance, odor control, compression fabrics, and smart textiles with embedded sensors monitoring performance metrics. Regulatory, environmental, and economic drivers include new labor and safety standards, environmental laws restricting harmful chemical finishes, consumer demand for sustainability, and rising wages in key manufacturing hubs. Regional consumption patterns show North America and Europe as major buyers of high performance apparel for sports and outdoor lifestyle; Asia Pacific is growing rapidly due to increasing disposable incomes and growing outdoor recreation trends. Emerging trends and future outlook include increased use of biodegradable performance fabrics, integration of IoT-enabled clothing (smart apparel), on-demand customization, and augmented reality tools for fit and shopping experience. Industry decision-makers are evaluating supply chain resilience, cost equalization of sustainable materials, and investment in automation to maintain quality and scale as consumer demands evolve.

AI is transforming the High Performance Apparel Market fundamentally across design, manufacturing, supply chain, and customer interaction domains. In production processes, AI-driven computer vision systems are being used for quality control, detecting defects in fabrics (e.g. small tears, irregular stitches, or dye inconsistencies) that human inspectors often miss; this has reduced waste by up to 30% in some factories. In design and materials engineering, AI models help to simulate moisture transport, thermal properties, and air flow, enabling R&D teams to optimize fabric blends (e.g. polyester/nanofiber) for performance under specific environments. Inventory management and logistics benefit from AI-based demand forecasting: companies are using predictive analytics to align production with regional demand spikes, reducing overstock and lead times by an estimated 20-25%. On the customer side, personalization engines powered by AI analyze athletic usage data or online behavior to recommend garments with performance features tailored to individual needs (compression, breathability, thermal zones etc.). In retail, virtual try-on tools using augmented reality and AI are shortening decision cycles for consumers, reducing returns due to sizing or fit problems by measurable percentages. Overall, the High Performance Apparel Market is experiencing improved operational performance, lower defect rates, better material efficiency, faster time-to-market, and more accurate alignment with end-user needs due to AI.

“In 2024, a major sportswear brand implemented an AI-based automated fabric cutting system that reduced material waste by 28% and increased cutting precision so that fewer than 2% of cut pieces needed rework, compared to about 7% previously.”

The High Performance Apparel Market Dynamics reflect shifting global patterns in demand, regulation, technology, and consumer behavior. Key trends include rising consumer expectations for performance features such as moisture-management, thermal regulation, UV protection, and antimicrobial properties. Supply chain pressures are pushing firms to adopt sustainable materials, minimize chemical use, and comply with stricter environmental regulations. Raw material costs fluctuate due to energy prices, trade tariffs, and transportation delays. Technological innovation—especially smart textiles, nanotechnology, and advanced fabric finishing—is playing a central role. Consumer preferences towards health, wellness, and outdoor lifestyle elevate demand not just for sports apparel but also for everyday wear with performance attributes. Manufacturers are balancing cost, durability, and sustainability in materials and processes. Geographic shifts show that Asia Pacific is increasingly important, both as a manufacturing hub and as a growth market for consumption. Regulatory regimes in Europe and North America are tightening around environmental impact and worker safety, which influence sourcing and production decisions globally.

The High Performance Apparel Market is being driven by growing demand for multi-functional materials that deliver more than one performance attribute. Fabrics that combine moisture-wicking, odor control, UV protection, thermal regulation, and durability are increasingly required. For example, textile producers are using blends of synthetic fibers with antimicrobial coatings, or embedding nano-silver particles for odor control. Workwear brands for industrial applications are seeking fabrics that are flame-retardant and water-repellent simultaneously. Outdoor apparel manufacturers are specifying modular layering systems that can adjust insulation depending on activity or climate. These requirements push investment into R&D for advanced finishes and hybrid fibre systems. In turn, this drives machinery upgrades in dyeing, coating, and finishing lines. Material producers are responding with more efficient polymers and eco-friendly synthetics, increasing per-unit performance while keeping weight low.

A major restraint on the High Performance Apparel Market is the high cost and operational complexity of implementing advanced performance features. Integrating coated fabrics, smart textiles, or sensor‐embedded materials often requires specialized machinery, skilled personnel, and more stringent quality control procedures. Many factories, especially in developing nations, face capital investment constraints and lack technical know-how. Compliance with environmental regulations adds cost—wastewater treatment, chemical management, and emissions controls impose operational burdens. Also, sourcing high-performance materials (e.g., specialty polymers, nano fibers) tends to be more expensive and subject to supply chain volatility. The process of validating performance claims (e.g., UV protection, antimicrobial efficacy) involves laboratory testing, standards compliance and certifications, further increasing cost and lead time.

The High Performance Apparel Market has opportunities in developing sustainable and smart textile innovations. Biodegradable synthetics, recycled fibers, and low-impact finishing processes are being developed to meet growing consumer and regulatory pressure for sustainability. Smart textiles with embedded sensors, thermal mapping, or body movement feedback offer new product lines for athletes, outdoors professionals, and military users. There is untapped potential in combining textile performance with wearable electronics to enable health monitoring or environmental sensing. Growth in online customization platforms and direct-to-consumer models further allow small brands to offer performance apparel with tailored attributes without large inventories.

The High Performance Apparel Market faces challenges balancing deliverables: performance attributes, cost efficiency, and environmental compliance. Using high performance finishes like durable water repellent (DWR), nanocoatings, or UV inhibitors may provide desired performance but often involve chemicals that are scrutinized under eco-regulations in regions like the EU or California. Achieving high durability alongside lightness often means trade-offs in material strength vs. comfort, or cost vs. manufacturability. Additionally, consumers increasingly demand transparency in materials and production ethics, which requires supply chain traceability. This elevates costs and requires investment in new technologies or auditing systems. Controls on chemical residues, wastewater, emissions are becoming stricter, and non-compliance risks both regulatory penalties and brand-reputation damage.

Increased Use of Smart Textiles and Integrated Sensors: High Performance Apparel Market participants are embedding sensors for thermal mapping, heart-rate monitoring, or sweat analysis directly into garments. In several cases, smart jerseys can send data during athletic performance for real-time feedback. These innovations are reducing error margins in performance measurement and enabling value-added services like athlete-insight dashboards.

Shift Toward Recycled and Biodegradable Materials: A measurable trend is the rise of recycled synthetic fibres and biodegradable synthetics; in 2024, over 35% of new high performance fabric launches included sustainable or recycled content, with water usage in finishing processes reduced by up to 25% for some major brands.

Growth in Custom Fit and On-Demand Production: Brands are increasingly offering customizable performance apparel, with digital scanning tools allowing individual fit measurement. On-demand production systems are being adopted to reduce inventory waste; for example some factories now use digital printing and cut-to-measure workflows to produce units with fit precision, cutting lead times by up to 40%.

Advanced Retail and Customer Engagement Technologies: Immersive technologies (AR/VR) are being implemented in some retail-showrooms and online platforms to let customers try on performance apparel virtually. AI-driven style recommendation systems are increasingly common. Some brands also use CRM systems that integrate performance feedback from wearers to suggest product upgrades or additional gear.

The High Performance Apparel Market is segmented by type, application, and end-user, each contributing to the overall structure and growth of the industry. By type, the market includes moisture-wicking fabrics, thermal and insulated apparel, UV-resistant clothing, antimicrobial textiles, and smart textiles, all designed to meet diverse performance needs. By application, categories range from sportswear and outdoor gear to protective industrial clothing, military uniforms, and specialized medical textiles, each reflecting unique usage environments. End-user insights highlight the role of industries such as sports and fitness, defense and security, healthcare, and industrial sectors, with consumer adoption patterns and regulatory requirements influencing demand. This segmentation reveals clear leadership of sports and athletic wear, supported by high participation in fitness and recreational activities, while protective and smart apparel are experiencing rapid adoption across professional and industrial domains. Collectively, these segments demonstrate the market’s adaptability to performance-driven consumer expectations and technical demands.

The High Performance Apparel Market by type encompasses several product categories, each offering specific attributes and competitive advantages. Moisture-wicking fabrics lead the segment due to their widespread application in sportswear and outdoor apparel. These fabrics efficiently manage sweat and maintain comfort, making them essential for both professional athletes and everyday consumers engaging in fitness activities. Thermal and insulated apparel follows closely, with demand driven by outdoor enthusiasts, industrial workers in cold environments, and the military sector. UV-resistant apparel is gaining traction, especially in markets with high outdoor activity and stricter health awareness regarding skin protection. Antimicrobial textiles represent a niche yet expanding segment, particularly relevant in healthcare and military applications where hygiene and odor control are critical. Smart textiles, integrating embedded sensors and responsive fibers, represent the fastest-growing type, driven by increasing demand for wearable technology that enhances user performance and safety. Collectively, these product types highlight innovation-driven expansion in the High Performance Apparel Market.

Applications of high performance apparel span a broad spectrum, reflecting the diverse functions these garments provide. Sportswear remains the leading application, supported by widespread consumer participation in fitness, athletics, and recreational activities, where demand for lightweight, durable, and sweat-resistant fabrics is strongest. Protective industrial clothing is emerging as the fastest-growing application, underpinned by stricter workplace safety regulations and heightened demand in construction, mining, and oil & gas industries. Outdoor gear, including trekking, camping, and adventure sports apparel, continues to grow steadily due to rising outdoor recreation globally. Military uniforms form a critical application, benefiting from ongoing modernization programs that require apparel with flame-resistance, moisture control, and thermal protection. Specialized healthcare apparel, although a smaller segment, is witnessing uptake through antimicrobial and smart fabrics designed for infection control and monitoring. Together, these applications underscore the High Performance Apparel Market’s role in catering to both consumer-driven and mission-critical professional needs.

End-user insights provide clarity into the driving forces behind the High Performance Apparel Market. The sports and fitness segment is the leading end-user, backed by growing consumer demand for apparel that enhances performance, comfort, and endurance. With increasing global participation in athletics, gyms, and recreational sports, this segment consistently drives the highest volume of demand. The defense and security sector is the fastest-growing end-user, fueled by requirements for advanced protective clothing, durability under extreme conditions, and integration of smart fabrics for operational monitoring. Industrial end-users, including oil & gas, construction, and manufacturing, also play a significant role, where compliance with occupational safety regulations and demand for protective apparel drive steady adoption. Healthcare end-users represent a specialized yet impactful segment, particularly with antimicrobial and smart fabrics designed for medical staff uniforms and patient wear. Collectively, these insights reveal a balanced demand pattern across consumer, professional, and institutional users, shaping the future direction of the High Performance Apparel Market.

Asia Pacific accounted for the largest market share at 38% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 9.2% between 2025 and 2032.

Asia Pacific’s leading position in the High Performance Apparel Market is supported by dense manufacturing clusters, expanding domestic consumption, and rapid adoption of performance textiles across sportswear and outdoor segments. In 2024, market activity concentrated in China, Japan, South Korea and Australia drove headline volumes, while rising urban outdoor participation in India and Southeast Asia added incremental demand. North America’s acceleration reflects investment in automation, digitized supply chains and advanced material R&D. Europe remains a mature buyer market prioritizing sustainable finishes and regulatory compliance. South America and Middle East & Africa are smaller in absolute size but show pockets of demand tied to industrial protective apparel and expanding retail channels. Region-specific infrastructure upgrades, trade policies and technological diffusion will shape regional trajectories through 2032.

Innovation and Industrial Demand presents a market where the United States and Canada together held roughly 30% of global High Performance Apparel Market demand by volume in 2024. Key industries driving demand include professional and collegiate sports, outdoor recreation, defense and public safety uniforms, and industrial protective clothing for oil & gas and construction sectors. Notable regulatory changes and government support include strengthened worker-safety standards and incentives for domestic technical textile R&D and manufacturing modernization programs that encourage automation adoption. Technological advancements encompass in-line digital printing for bespoke performance patterns, widespread implementation of computer vision for quality inspection, and integration of wearable sensors for athlete monitoring in both product development and commercial offerings. Retailers and brands in the High Performance Apparel Market are also investing in e-commerce platforms with virtual fitting rooms and AI-driven personalization to improve conversion and reduce returns, reflecting a digital transformation across the value chain.

Sustainable Standards and Technical Excellence accounted for approximately 20% of global High Performance Apparel Market demand by volume in 2024. Key European markets include Germany, the United Kingdom, and France, each showing robust consumption in outdoor and technical sportswear categories. Regulatory bodies and sustainability initiatives—such as region-level chemical restrictions on per- and polyfluoroalkyl substances (PFAS), extended producer responsibility frameworks, and tighter wastewater discharge standards—are shaping sourcing and finishing choices for performance textiles. Adoption of emerging technologies in the European High Performance Apparel Market includes eco-friendly finishing processes, closed-loop recycling pilots for synthetic performance yarns, and expanded use of life-cycle assessment tools to quantify environmental impact. European suppliers are focusing on traceability, certification of recycled content, and investment in low-water dyeing technologies to align product performance with regulatory and consumer sustainability expectations.

Manufacturing Scale and Rapid Consumption represented the largest market volume in 2024 and ranks #1 in global consumption for the High Performance Apparel Market. Top consuming countries include China, India, and Japan, with China leading manufacturing output and India showing fast growing retail demand. Infrastructure and manufacturing trends in the Asia-Pacific High Performance Apparel Market include expansion of automated fabric finishing lines, investment in precision cutting and sewing robotics, and growth of regional technical textile clusters that service both domestic brands and export orders. Regional tech trends see hubs in eastern China and South Korea advancing smart textile R&D, while Southeast Asia focuses on cost-efficient scale and nearshoring capabilities. The Asia-Pacific High Performance Apparel Market continues to invest in skill development, factory modernization, and cross-border logistics improvements to support higher value, technology-intensive product lines.

Niche Growth and Industrial Demand comprised roughly 6% of global High Performance Apparel Market volumes in 2024. Key countries include Brazil and Argentina, where Brazil accounts for the largest national demand. The region’s market share is driven by demand for outdoor and sportswear in urban and recreational segments, alongside industry needs for protective garments in mining and agriculture. Infrastructure trends affecting the South America High Performance Apparel Market include logistics constraints that raise landed input costs and a gradual push toward localized finishing facilities to lower import dependencies. Energy sector activity (mining and oil & gas) stimulates orders for certified protective apparel, while several governments have introduced export support measures and trade facilitation policies to help regional manufacturers access foreign markets and scale production.

Industrial Demand and Modernization represented about 6% of global High Performance Apparel Market volume in 2024. Regional demand trends in the High Performance Apparel Market are concentrated in oil & gas, construction, defense and public safety applications, with major growth countries including the United Arab Emirates and South Africa leading procurement for industrial protective clothing. Technological modernization trends in the MEA High Performance Apparel Market include selective adoption of automated cutting and finishing in larger manufacturers, investment in certification capabilities for flame-resistant and high-visibility garments, and pilot implementations of smart textiles for worker health monitoring in hazardous environments. Local regulations and trade partnerships are increasingly influencing specification standards and facilitating regional sourcing agreements, especially for large infrastructure projects requiring certified performance apparel.

China — 28% Market Share

China High Performance Apparel Market: high production capacity with extensive technical textile manufacturing infrastructure.

United States — 22% Market Share

United States High Performance Apparel Market: strong end-user demand and advanced R&D ecosystems supporting product innovation.

The competitive environment in the High Performance Apparel Market is characterized by a large, multi-tiered ecosystem of global brands, specialized technical textile manufacturers, performance-focused niche labels, and a wide network of contract manufacturers. There are well over 100 active competitors operating at a meaningful commercial scale worldwide, ranging from multinational sportswear giants to regional technical textile specialists and startup smart-textile innovators. Market positioning varies by company: some incumbents compete on brand equity, athlete sponsorships and broad distribution networks, while others differentiate on material science, vertical manufacturing capabilities or certification for protective and defense apparel. Strategic initiatives across the industry include product-line extensions into smart and sustainable textiles, multi-brand partnerships to scale recycled feedstock, targeted M&A to acquire specialty-fiber portfolios, and collaborative R&D consortia with material science labs and universities. Innovation trends reshaping competition include rapid adoption of sensor-enabled garments, low-impact finishing chemistries, digital printing and 3D-knitting for seamless performance wear, AI-driven product development, and automated quality-control solutions that improve throughput and reduce waste. For decision-makers, competitive advantage increasingly depends on the ability to integrate advanced materials, control critical production steps, and commercialize demonstrable performance benefits while meeting growing regulatory and sustainability requirements.

Nike

Adidas

Under Armour

Puma

Reebok

Lululemon

VF Corporation

Columbia Sportswear Company

Patagonia

Asics

Decathlon

New Balance

Mizuno Corporation

Arc’teryx

Technology is a primary determinant of product differentiation and operational efficiency in the High Performance Apparel Market. Current and emerging technologies influencing the sector include smart textiles and wearable sensors that measure biometric and environmental parameters; these enable product tiers that provide live performance feedback and post-use analytics. Advanced membrane technologies (e.g., next-generation ePTFE and polymer membranes) continue to improve breathability-to-waterproof ratios while reducing thickness and weight for outerwear and protective garments. Nanofiber and microfilament developments increase moisture-management and thermal regulation without bulk, while novel surface chemistries deliver durable water repellency and antimicrobial properties with lower environmental impact. Digital textile printing and 3D knitting are being deployed to produce seamless garments, zoned compression, and rapid design iteration, reducing sample cycles and enabling on-demand, small-batch production. Automated material handling, robotic cutting and sewing, and AI-driven nesting algorithms substantially reduce material waste and labor dependence in high-mix production environments. Chemical-to-fiber recycling and advanced mechanical recycling processes are maturing — enabling higher tenacity recycled polyester and recycled filament yarns suitable for performance applications. Lifecycle assessment (LCA) tools and digital product passports are increasingly used to quantify and communicate environmental performance, influencing sourcing and procurement decisions. For decision-makers, technology investment choices should be evaluated not only for immediate product performance uplift but also for downstream benefits: lower returns, tighter inventory turns, reduced rework rates, regulatory compliance readiness, and enhanced product traceability.

• In March 2024, AiQ Smart Clothing launched a cycling jersey with integrated heart-rate monitoring and smart lighting to enhance rider safety; the product embeds textile sensors and low-power lighting modules and is positioned for mass retail distribution in select European and North American channels.

• In 2023, Gore introduced the PYRAD® uniform application at a major safety & PPE exhibition, showcasing an ePTFE-based construction that enhances thermal protection and breathability for firefighting and industrial protective garments. The release highlighted material thinness improvements and wearer comfort metrics.

• In 2023, Zhejiang Jiaren New Materials commercialized a chemically recycled polyester filament yarn with tenacity exceeding 6.0 cN/dtex, developed specifically for high-performance sportswear to deliver durability comparable to virgin filaments. The launch targeted performance apparel producers seeking recycled feedstock.

• In October 2023, Quantum Materials completed acquisition of the Innegra™ high-performance fiber portfolio, expanding access to impact-resistant and high-tenacity fiber technologies for protective apparel, composites and reinforced garments used in safety and defense applications.

This report covers the global High Performance Apparel Market with a comprehensive, structured scope across product types, applications, end-users, technologies, and geographies. Product types included range from moisture-management fabrics, thermal and insulated apparel, UV-protective textiles, antimicrobial and odor-control materials, to smart textiles with embedded sensors and hybrid composite fabrics. Application focus spans sportswear, outdoor recreation apparel, industrial protective clothing, military and defense uniforms, healthcare performance garments, and specialty commercial segments. End-user segmentation addresses consumer retail (athletic and outdoor consumers), institutional procurement (defense, emergency services), and industrial buyers (oil & gas, construction, mining, manufacturing). Technological coverage includes advanced membranes, nanofiber technologies, digital printing, 3D-knitting, sensor integration, AI in design and production optimization, and recycling and closed-loop fiber technologies. Geographic scope examines North America, Europe, Asia-Pacific, South America, and Middle East & Africa with regional assessments of manufacturing capacity, consumption patterns, infrastructure trends, and regulatory environments. The report also addresses supply-chain components—raw material suppliers, fiber producers, fabric mills, finishing houses, OEM/ODM manufacturers, and retail/brand distribution networks—while identifying niche and emerging segments such as biodegradable performance fabrics, on-demand customization platforms, and integrated wearable analytics. Designed for executives, product managers, procurement leads, and investors, the report delivers actionable insights on competitive positioning, technology pathways, manufacturing modernization priorities, and strategic opportunities across the value chain.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 1,056.0 Million |

| Market Revenue (2032) | USD 2,043.2 Million |

| CAGR (2025–2032) | 8.6% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Nike, Adidas, Under Armour, Puma, Reebok, Lululemon, VF Corporation, Columbia Sportswear Company, Patagonia, Asics, Decathlon, New Balance, Mizuno Corporation, Arc’teryx |

| Customization & Pricing | Available on Request (10% Customization is Free) |