Reports

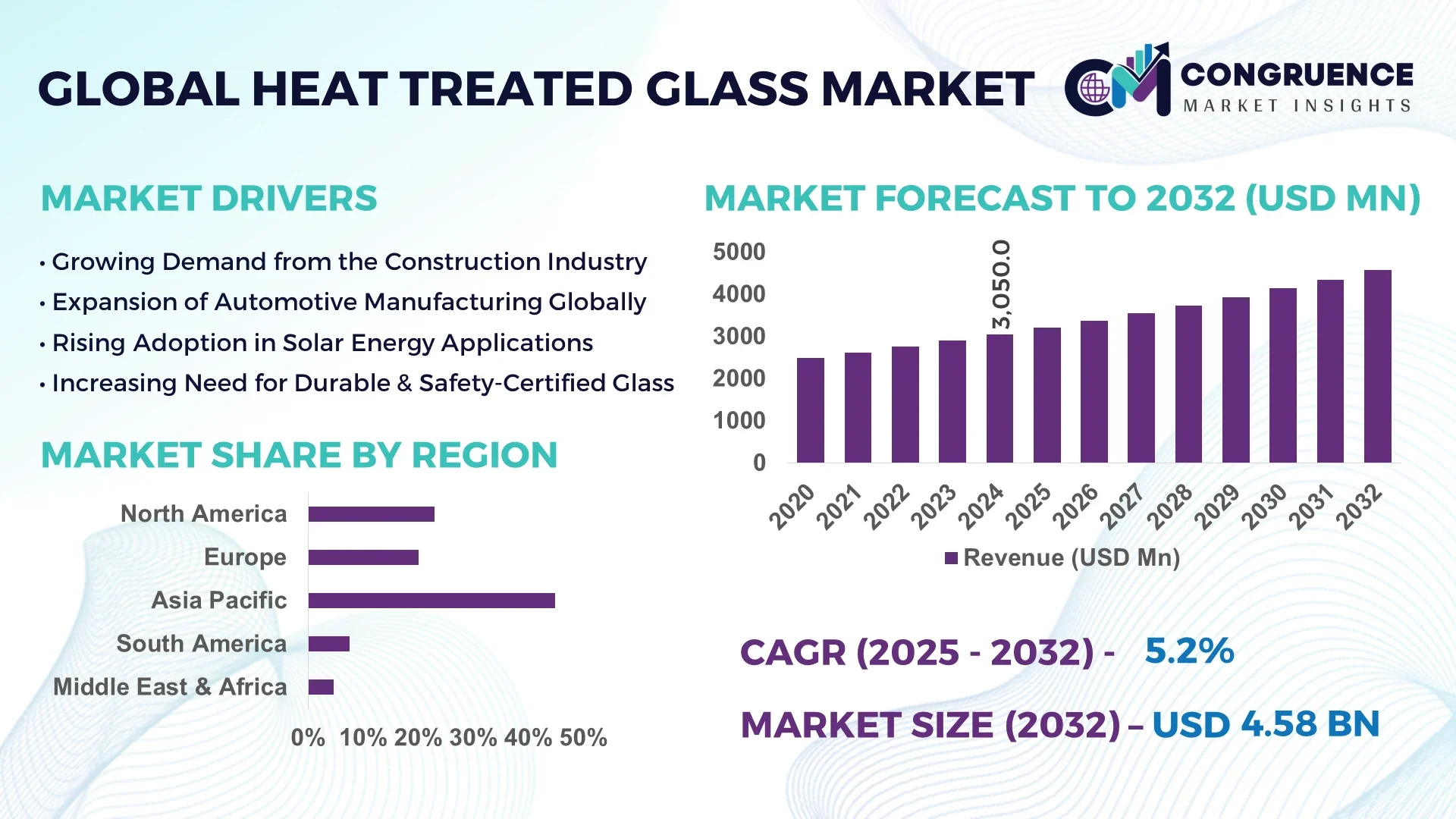

The Global Heat Treated Glass Market was valued at USD 3,050.0 Million in 2024 and is anticipated to reach a value of USD 4,575.4 Million by 2032 expanding at a CAGR of 5.2% between 2025 and 2032.

China maintains a dominant position in the Heat Treated Glass Market, driven by its extensive production infrastructure and large-scale investments in float glass processing facilities. The country boasts over 200 advanced glass tempering lines, supported by government-led smart manufacturing initiatives and a robust export framework across automotive and construction sectors.

The Heat Treated Glass Market plays a pivotal role across various industry verticals, including construction, automotive, aerospace, and consumer electronics. The construction sector, particularly in urban infrastructure and commercial real estate, accounts for a significant portion of global demand, benefiting from safety regulations that mandate tempered glass use in façades, doors, and windows. Meanwhile, automotive manufacturers are integrating heat treated glass in windshields and sunroofs due to its superior strength and thermal resistance. Technological innovations such as laser-cutting precision, self-cleaning coatings, and electrochromic glazing are reshaping product offerings. Regulatory bodies in the U.S., EU, and Asia-Pacific are enforcing safety and energy-efficiency mandates, driving accelerated adoption. Environmental considerations, especially reduced carbon emissions through efficient glass production and recycling processes, are further influencing market development. Regionally, consumption is growing fastest in Southeast Asia and the Middle East, where urbanization and infrastructure spending are expanding. Looking forward, digitization, including AI-based quality inspection and process control, along with rising demand for customizable and smart glass products, is expected to sustain market momentum and create new revenue streams.

Artificial Intelligence (AI) is significantly transforming the Heat Treated Glass Market by enhancing operational efficiency, product consistency, and predictive maintenance capabilities. In manufacturing facilities, AI-powered computer vision systems are now deployed to monitor the tempering process in real-time, ensuring optimal glass strength and reducing defects by up to 40%. Advanced machine learning algorithms help manufacturers optimize furnace temperature settings, load distribution, and cooling rates, resulting in reduced energy consumption by nearly 18% across multiple production sites. Predictive analytics tools are also being used to forecast machine maintenance schedules, thereby reducing downtime by up to 30% and improving plant productivity. Furthermore, AI facilitates quality assurance by instantly detecting micro-cracks and impurities during the glass tempering cycle, which historically required manual inspection and posed higher risks of oversight.

In terms of supply chain logistics, AI integration has led to more efficient inventory and order tracking systems, minimizing lead times and optimizing raw material procurement. As demand for customized glass shapes and finishes grows, AI-driven CAD systems enable faster prototyping and reduced cycle times. These technological advancements are not only increasing throughput but also aligning with sustainability goals, as AI tools help reduce energy waste and support eco-friendly manufacturing practices in the Heat Treated Glass Market.

“In 2024, a major Chinese glass processing facility implemented an AI-based optical inspection system capable of analyzing over 2,000 glass sheets per hour for defects, achieving a 98.6% accuracy rate and reducing manual inspection labor by 70%.”

The Heat Treated Glass Market is experiencing steady momentum, driven by technological upgrades, regulatory influences, and rising demand across critical sectors such as construction, automotive, and aerospace. Innovations in smart coatings, solar control features, and multi-layered tempering processes are pushing manufacturers to invest in upgraded production facilities. The transition towards green building materials and energy-efficient glass types is influencing market dynamics, especially in Europe and Asia-Pacific. Regional policy shifts focusing on safety compliance and sustainable infrastructure have elevated demand for heat treated glass in commercial real estate and transportation hubs. At the same time, evolving consumer expectations around aesthetics, durability, and safety are shaping product innovation strategies within the industry.

The rapid acceleration of global infrastructure development and high-rise commercial real estate projects has significantly influenced the Heat Treated Glass Market. Countries across Asia-Pacific, particularly India and Indonesia, are investing heavily in urban development programs that emphasize energy-efficient and safety-compliant materials. Heat treated glass, known for its durability and safety profile, is becoming a default material for façades, curtain walls, and interior partitions. In the U.S., over 70% of new commercial buildings initiated since 2023 have incorporated heat treated or safety glass components. Additionally, the UAE and Saudi Arabia are implementing smart city initiatives, integrating advanced architectural designs that require tailored glass solutions. These factors continue to reinforce long-term demand across the construction value chain.

One of the primary restraints in the Heat Treated Glass Market is the high capital expenditure required to install and maintain advanced tempering and processing equipment. State-of-the-art tempering furnaces, automated cutting lines, and AI-integrated inspection systems demand significant upfront investment, often exceeding USD 5 million per production line. Smaller and mid-scale manufacturers face difficulty adopting such technologies, limiting market entry and scalability. Additionally, the frequent need for calibration, maintenance, and skilled operators adds to operational costs. Regulatory requirements for precision and safety also necessitate continuous upgrades, further inflating financial burdens on manufacturers. These capital constraints can deter innovation adoption and limit competitiveness in cost-sensitive regions.

The increasing integration of heat treated glass in automotive and electric vehicle (EV) design presents a substantial growth opportunity for the Heat Treated Glass Market. EV manufacturers are adopting heat treated glass for panoramic roofs, lightweight windshields, and smart windows equipped with UV-blocking coatings. Advanced tempering ensures impact resistance and thermal stability—critical requirements in EVs operating under varying conditions. In Europe, over 40% of newly registered EVs in 2024 featured glass components manufactured using enhanced tempering techniques. Furthermore, vehicle interiors are evolving toward futuristic designs that incorporate larger, curved, and interactive glass panels, expanding the demand for highly specialized glass solutions. This shift is creating a lucrative segment within the automotive sector for heat treated glass suppliers.

A major challenge in the Heat Treated Glass Market is navigating varying regulatory standards across global markets. While countries like Germany and Japan enforce strict compliance protocols for thermal stress, impact resistance, and optical clarity, other regions such as parts of Africa and Latin America lack uniform testing and certification frameworks. This inconsistency complicates cross-border supply chains and limits the global scalability of manufacturers. Companies often need to produce multiple product variants to meet regional standards, resulting in higher customization costs and longer lead times. Moreover, delays in obtaining approvals or certifications for new products in certain jurisdictions can stall market entry and affect revenue cycles.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Heat Treated Glass Market. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Integration of Smart and Electrochromic Glass Features: Manufacturers are increasingly embedding smart capabilities into heat treated glass panels, such as dynamic light control and UV/IR filtering. Electrochromic coatings are gaining popularity in corporate buildings and luxury vehicles, contributing to improved energy savings. In 2025, over 12% of new installations in high-end commercial buildings included heat treated glass with embedded sensor technologies.

Growing Use in Solar and Renewable Energy Infrastructure: Heat treated glass is being incorporated into photovoltaic (PV) modules and solar façade systems for improved durability and performance. Several solar power plants in the Middle East and Southeast Asia have transitioned to tempered glass panels for improved resistance to sandstorms and thermal stress, enhancing lifespan by over 30% compared to standard glass.

Automation and AI Integration in Production Lines: The adoption of AI and robotics in heat treated glass production lines is accelerating. In 2024, automated quality control systems reduced defect rates by 25% across multiple large-scale facilities. Additionally, AI-enhanced temperature control has shortened the glass tempering cycle by 12%, contributing to higher throughput and energy efficiency across Asia-Pacific manufacturing hubs.

The Heat Treated Glass Market is segmented based on type, application, and end-user, each providing vital insights into demand patterns and strategic positioning. The market encompasses a broad range of glass types designed to meet industry-specific requirements such as thermal resistance, impact durability, and aesthetic precision. Applications range from building and construction to automotive and renewable energy systems, each demanding unique mechanical and thermal properties. End-user categories span from real estate developers to automotive OEMs and electronics manufacturers, with varying levels of customization and performance criteria. This structured segmentation enables suppliers and stakeholders to align product development, marketing, and distribution strategies with the evolving priorities of key industries and regions.

In the Heat Treated Glass Market, the primary product types include fully tempered glass, heat-strengthened glass, chemically strengthened glass, and laminated tempered glass. Among these, fully tempered glass leads the segment due to its widespread use in architectural and automotive applications. Its high mechanical strength and shatter-resistance make it the preferred choice for exterior facades, commercial windows, and vehicle windows.

The fastest-growing type is laminated tempered glass, primarily driven by its dual-layer structure that enhances safety and sound insulation. This type is increasingly used in high-end construction projects and luxury vehicles where occupant protection and acoustic performance are critical. Its popularity is also rising in urban regions with stringent building codes.

Heat-strengthened glass holds a niche role in applications where moderate thermal resistance is needed but full tempering is not required, such as certain interior partitions and furniture. Chemically strengthened glass, although more expensive, is gaining limited traction in electronics and precision optical applications where high surface compression is necessary.

The Heat Treated Glass Market serves a range of applications including building & construction, automotive, aerospace, solar energy systems, furniture & interiors, and electronics. The building & construction segment is the dominant application, with large-scale deployment in commercial façades, partitions, windows, and doors. The growing demand for impact-resistant, energy-efficient materials in urban infrastructure and green buildings fuels this segment’s leading position.

Automotive applications are the fastest-growing, driven by advancements in vehicle design, safety standards, and the rapid proliferation of electric vehicles. Manufacturers are increasingly incorporating panoramic sunroofs, laminated windshields, and smart windows made from heat treated glass to enhance both safety and aesthetics.

In solar energy systems, heat treated glass is used in photovoltaic panels and solar concentrators due to its thermal endurance and clarity. Furniture & interior design applications utilize it for tabletops, shelving, and bathroom enclosures, while electronics employ specialty glass in displays and protective casings, albeit in smaller volumes.

The Heat Treated Glass Market caters to a diverse group of end-users including construction companies, automotive manufacturers, glass processors, solar panel producers, and electronics firms. Construction companies are the leading end-users, given their extensive requirement for high-performance glass across both residential and commercial infrastructure. The adoption of sustainable and safe building practices has significantly increased their reliance on advanced heat treated solutions.

Automotive manufacturers represent the fastest-growing end-user group, driven by evolving safety regulations, lightweighting goals, and consumer demand for design innovation. The shift toward electric and autonomous vehicles is pushing OEMs to use more advanced glass components with thermal and acoustic functionalities.

Glass processors play a critical role in customizing and finishing base glass products for diverse downstream industries. Solar panel producers benefit from the thermal and structural stability of heat treated glass, especially in utility-scale installations. Electronics firms, while a smaller segment, require ultra-thin and chemically toughened variants for specific high-end applications such as mobile screens and AR/VR devices.

Asia-Pacific accounted for the largest market share at 44.8% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2025 and 2032.

The Asia-Pacific region continues to dominate due to its vast industrial base, construction booms, and strong presence of manufacturing hubs in China, India, and Japan. Meanwhile, North America's growth is being fueled by advanced technological integration in glass processing, smart infrastructure initiatives, and increased usage of heat treated glass in electric vehicles and commercial buildings. Each region presents unique dynamics shaped by localized industry drivers, regulatory developments, and consumer preferences. Growth trajectories are further influenced by infrastructure investments, energy-efficiency goals, and shifting sustainability standards, contributing to the evolving competitive landscape of the global Heat Treated Glass Market.

The North America Heat Treated Glass Market held approximately 21.3% of the global market share in 2024, propelled by strong demand from the construction and automotive industries. Smart building developments in the U.S. and Canada are increasingly incorporating energy-efficient and durable glass materials, driving widespread use of fully tempered and laminated glass. Regulatory agencies have imposed stricter codes for safety glazing and thermal insulation, encouraging adoption in public and commercial infrastructure. The rise in electric vehicle manufacturing across the U.S. is also accelerating demand for lightweight, impact-resistant glass solutions. Technological advancements such as automated tempering lines and AI-driven quality control are rapidly transforming production capabilities, while digital design tools enable customized fabrication for complex architectural requirements. These developments are positioning North America as a high-potential growth region in the global Heat Treated Glass Market.

Europe accounted for 19.5% of the global Heat Treated Glass Market share in 2024, with Germany, the UK, and France being the key contributors. The region's market is strongly influenced by sustainability mandates and the European Green Deal, which emphasize energy efficiency in building materials. Regulatory bodies such as the European Committee for Standardization (CEN) have enforced rigorous glazing standards that boost heat treated glass usage in both commercial and residential sectors. Emerging technologies like electrochromic coatings and vacuum insulating glass are gaining traction among EU-based manufacturers and construction firms. Smart urban development projects across Scandinavia and Western Europe continue to increase demand for aesthetically appealing and high-performance glass solutions. With strong support for innovation, Europe remains a prominent player in the advancement of eco-friendly and high-strength glazing systems.

The Asia-Pacific Heat Treated Glass Market leads globally in terms of volume, accounting for 44.8% of total consumption in 2024. China, India, and Japan are the top-consuming countries, collectively driving growth through infrastructure expansion, industrial modernization, and rising automotive production. In China, massive investments in high-speed rail, commercial real estate, and smart cities have spurred extensive use of tempered glass. India is witnessing rapid growth in urban development and high-rise construction projects, significantly increasing demand for laminated and heat-strengthened glass. Japan continues to innovate in specialty glass used in technology-integrated construction and automotive systems. Regional innovation hubs such as Shenzhen and Bengaluru are fostering advanced manufacturing techniques and integrating AI and robotics into glass processing. These dynamics position Asia-Pacific as the epicenter of both consumption and innovation in the Heat Treated Glass Market.

In 2024, South America contributed approximately 6.7% to the global Heat Treated Glass Market, with Brazil and Argentina leading the regional landscape. The market is driven by rising infrastructure investments, particularly in commercial real estate and public transportation projects. Brazil has launched several metro rail and airport upgrades, incorporating large volumes of safety glass in stations and terminals. Argentina's automotive sector is steadily recovering, contributing to demand for impact-resistant and thermally stable glass. The renewable energy sector, including solar installations in Chile and Brazil, is also adopting heat treated glass for its durability and efficiency. Government incentives promoting construction modernization and energy-efficient materials are supporting regional growth, though import dependence and limited local manufacturing capacity present operational challenges.

The Middle East & Africa region accounted for 7.7% of the Heat Treated Glass Market in 2024, with notable contributions from the UAE, Saudi Arabia, and South Africa. Demand is largely driven by expansive construction activities in smart cities, commercial towers, and tourism infrastructure, especially in Dubai, Riyadh, and Doha. The oil & gas sector also utilizes specialized heat treated glass for control rooms and protective applications. Countries like the UAE are actively incorporating sustainable design into public projects, mandating use of high-performance glazing. Technological modernization is gaining momentum, with investments in regional glass processing facilities equipped with automated lines and advanced inspection tools. Trade partnerships across the Gulf Cooperation Council (GCC) and local regulations promoting safety glass usage in public structures continue to create a supportive policy environment for market expansion.

China – 35.2% Market Share

High production capacity and extensive integration in construction and automotive industries drive its dominance in the Heat Treated Glass Market.

United States – 17.4% Market Share

Strong end-user demand from smart buildings and electric vehicle manufacturing supports its leading role in the Heat Treated Glass Market.

The Heat Treated Glass Market features a moderately consolidated competitive landscape with over 150 active players globally, including both multinational corporations and regional manufacturers. Competition is shaped by factors such as product differentiation, technological innovation, and distribution capabilities. Leading players maintain strong positioning through vertically integrated operations, advanced manufacturing lines, and established partnerships with construction and automotive OEMs. Strategic initiatives such as cross-border joint ventures, expansion of production capacity, and localized R&D centers are common across Asia-Pacific and North America.

In 2023 and 2024, there was a noticeable uptick in strategic acquisitions and mergers aimed at strengthening product portfolios and entering emerging markets. Technological innovation remains a core competitive lever, with companies increasingly adopting AI-enabled quality inspection systems, automated tempering furnaces, and energy-efficient glass coatings. Product customization and smart glass integration are key trends, especially in sectors demanding aesthetic and functional versatility. Market leaders are also investing in sustainability by adopting green manufacturing practices and recyclable material sourcing to meet evolving regulatory expectations and customer preferences.

Saint-Gobain S.A.

AGC Inc.

Guardian Industries

NSG Group

Şişecam Group

Xinyi Glass Holdings Limited

Fuyao Glass Industry Group Co., Ltd.

Taiwan Glass Ind. Corp.

Vitro Architectural Glass

Cardinal Glass Industries

The Heat Treated Glass Market is undergoing a transformation driven by advancements in automation, AI integration, and material science. One of the most impactful technologies is AI-powered quality control systems, capable of identifying micro-defects in glass panels with up to 98% accuracy. These systems have reduced production waste and inspection time by more than 30% in large-scale manufacturing facilities. Automated tempering furnaces with real-time data monitoring are also enhancing efficiency and ensuring uniform thermal stress distribution across glass surfaces.

Laser-based edge cutting and polishing technologies are improving glass finish quality while reducing breakage during installation. In addition, multi-layer coating technologies enable features like solar control, anti-glare properties, and self-cleaning surfaces—expanding the usability of heat treated glass in architectural, automotive, and solar applications.

Emerging technologies such as electrochromic and thermochromic smart glass are gaining traction, especially in commercial real estate and luxury vehicles. These smart materials dynamically adjust to environmental light and heat, enhancing user comfort and energy efficiency. Further, green manufacturing innovations—including low-emission float glass processes and recycling of glass cullet—are being adopted across Asia and Europe to meet regulatory standards and sustainability targets. These advancements are redefining operational benchmarks and competitive strategies across the Heat Treated Glass Market.

• In February 2024, AGC Inc. launched a next-generation tempering furnace line with built-in AI analytics, enabling automated diagnostics and improving production yield by 18% across its Southeast Asia operations.

• In August 2023, Guardian Glass introduced a new anti-reflective heat treated glass for solar panels, which increased light transmission efficiency by 6.4% and is now being adopted in Middle Eastern solar farms.

• In October 2023, NSG Group expanded its Vietnam plant with a new facility dedicated to smart heat treated glass used in automotive HUD applications, expected to produce over 900,000 units annually.

• In March 2024, Saint-Gobain unveiled a recyclable fully tempered glass product line that reduces manufacturing energy consumption by 22%, targeting LEED-certified building projects in Europe and North America.

The Heat Treated Glass Market Report provides a comprehensive analysis across multiple dimensions, including product types, applications, end-user industries, regional trends, and technology integration. The report evaluates fully tempered, laminated, heat-strengthened, and chemically strengthened glass types, with attention to their performance characteristics and niche applications. Application segments covered include building and construction, automotive, solar energy, furniture, and consumer electronics, offering insights into specific market demands and usage contexts.

The geographic coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting local production capabilities, consumption trends, regulatory environments, and competitive dynamics. The report also examines emerging regional markets such as Southeast Asia and Eastern Europe, which are gaining traction due to construction and manufacturing expansions.

Technology insights focus on smart coatings, automation, AI-driven inspection systems, and green manufacturing practices. The scope includes analysis of innovation-driven growth in smart cities, EV adoption, and sustainable construction. It also identifies market entry opportunities, regional supply chain patterns, and strategic investment zones for stakeholders. Designed for industry professionals, investors, and policymakers, the report delivers actionable intelligence to support informed business decisions and strategic planning in the evolving Heat Treated Glass Market landscape.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 3,050.0 Million |

| Market Revenue (2032) | USD 4,575.4 Million |

| CAGR (2025–2032) | 5.2% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Saint-Gobain S.A., AGC Inc., Guardian Industries, NSG Group, Şişecam Group, Xinyi Glass Holdings Limited, Fuyao Glass Industry Group Co., Ltd., Taiwan Glass Ind. Corp., Vitro Architectural Glass, Cardinal Glass Industries |

| Customization & Pricing | Available on Request (10% Customization is Free) |