Reports

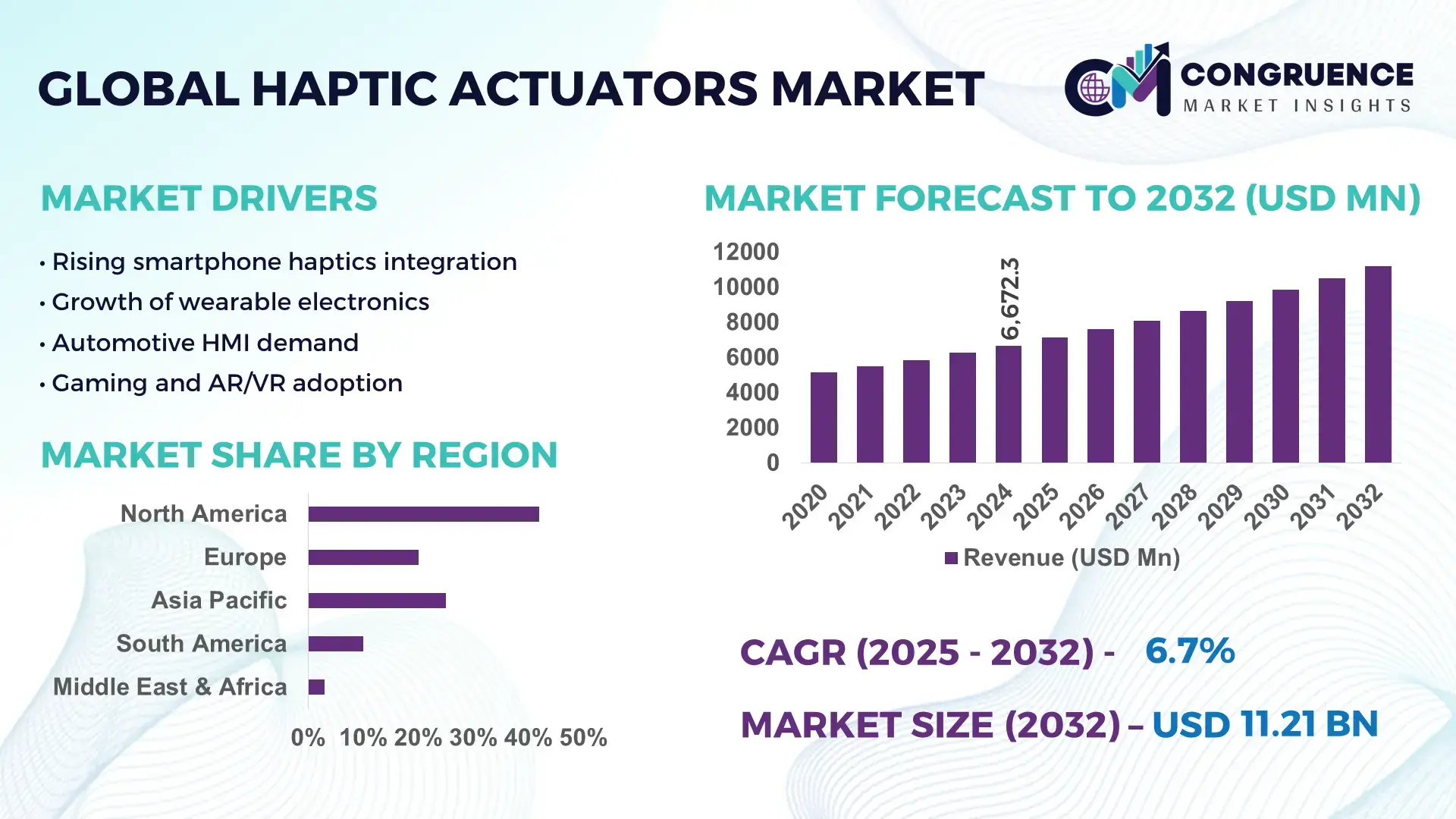

The Global Haptic Actuators Market was valued at USD 6672.34 Million in 2024 and is anticipated to reach a value of USD 11209.69 Million by 2032 expanding at a CAGR of 6.7% between 2025 and 2032. Growth is primarily driven by the rising integration of tactile feedback in consumer electronics, automotive interfaces, and immersive digital platforms.

China dominates the global haptic actuators landscape in terms of production scale, industrial investment, and technology deployment. In 2024, China manufactured over 1.9 billion vibration motors and linear resonant actuators annually, supported by more than USD 1.2 billion in cumulative capacity expansions across Guangdong, Jiangsu, and Zhejiang provinces. Over 72% of smartphones assembled in China integrate advanced haptic modules for gaming, notifications, and accessibility features. The automotive sector has also accelerated adoption, with more than 38% of newly produced electric vehicles in China using haptic feedback in infotainment and driver-assistance interfaces. Chinese manufacturers are actively transitioning from eccentric rotating mass actuators toward linear resonant and piezoelectric solutions, with over 420 new patents filed related to tactile feedback technologies between 2022 and 2024.

Market Size & Growth: USD 6672.34 Million in 2024, projected to reach USD 11209.69 Million by 2032 at 6.7% CAGR driven by multisensory interface adoption

Top Growth Drivers: Smartphone haptics +42%, automotive touch interfaces +31%, AR/VR device penetration +27%

Short-Term Forecast: By 2028, average actuator energy consumption expected to decline by 18%

Emerging Technologies: Piezoelectric haptics, ultrasonic mid-air haptics, AI-driven adaptive feedback systems

Regional Leaders: Asia-Pacific USD 5200 Million by 2032 with mobile gaming growth, North America USD 3300 Million with automotive UI adoption, Europe USD 2500 Million with industrial HMI use

Consumer/End-User Trends: Strong uptake in gaming devices, wearables, medical simulators, and automotive dashboards

Pilot or Case Example: 2024 automotive pilot achieved 22% driver reaction-time improvement using adaptive haptics

Competitive Landscape: Leader with ~18% share followed by Alps Alpine, AAC Technologies, TDK, Precision Microdrives

Regulatory & ESG Impact: Energy efficiency standards and electronic waste reduction policies influencing actuator design

Investment & Funding Patterns: Over USD 2.1 Billion invested in tactile interface R&D and production upgrades since 2022

Innovation & Future Outlook: Integration with spatial computing, smart surfaces, and immersive training platforms

The haptic actuators market serves key sectors including consumer electronics at approximately 48% usage concentration, automotive systems around 27%, industrial human–machine interfaces about 15%, and healthcare and simulation applications nearly 10%. Recent innovations include ultra-thin piezo actuators below 2 mm thickness, programmable multi-zone haptic panels, and low-power resonant actuators with up to 30% longer lifecycle. Regulatory emphasis on energy efficiency and recyclable electronic components is shaping product design and material selection. Regionally, Asia-Pacific leads in manufacturing and consumption due to high smartphone and wearable output, while North America drives automotive and medical device integration. Emerging trends include mid-air haptic feedback, haptics for virtual collaboration platforms, and integration with AI-based sensory personalization, positioning the market for continued expansion across digital, automotive, and industrial ecosystems.

The Haptic Actuators Market has become strategically relevant as digital interfaces increasingly replace mechanical controls across consumer electronics, automotive systems, industrial automation, and healthcare devices. Haptic feedback enhances usability, safety, and accessibility by enabling tactile confirmation in touch-based environments, directly supporting human–machine interaction efficiency. For example, piezoelectric actuators deliver approximately 35% faster response time and 28% lower power consumption compared to traditional eccentric rotating mass actuators, enabling thinner device profiles and longer battery life. Asia-Pacific dominates in volume, while North America leads in adoption with about 64% of automotive OEMs integrating haptic controls into infotainment and driver-assistance systems.

By 2028, AI-driven adaptive haptics is expected to cut user interface error rates by 22% through context-aware tactile feedback that adjusts intensity and pattern based on user behavior. Firms are committing to sustainability improvements such as 30% recycled material usage in actuator housings and a 25% reduction in manufacturing energy intensity by 2030 to align with ESG and circular economy targets. In 2024, South Korea achieved a 19% reduction in actuator power consumption through the deployment of ultra-low-voltage piezo modules in wearable devices, demonstrating measurable efficiency gains from technology upgrades.

Strategically, the Haptic Actuators Market supports resilience by enabling safer, more intuitive interfaces in autonomous systems, medical simulation, and remote operations. Its future pathways are closely tied to spatial computing, virtual collaboration, and smart surface development, positioning the Haptic Actuators Market as a pillar of interface standardization, regulatory alignment, and sustainable digital transformation.

The widespread adoption of smartphones, gaming consoles, AR/VR headsets, and digital dashboards is a major growth driver for the Haptic Actuators Market. Over 85% of new smartphones launched in 2024 included advanced tactile feedback for notifications, gaming, and accessibility. In automotive applications, more than 40% of new vehicles now incorporate haptic touch controls for infotainment and climate systems, reducing driver eye-off-road time by an estimated 15%. In industrial settings, haptic alerts in control panels have been shown to lower operator error rates by 18%, improving safety and productivity. These measurable benefits are accelerating integration across sectors and reinforcing haptic feedback as a standard interface feature.

Despite growing demand, the Haptic Actuators Market faces restraints from cost pressures and technical integration challenges. Advanced actuators such as piezo and ultrasonic modules can cost 25–40% more than traditional vibration motors, limiting adoption in low-margin consumer devices. Integration also requires specialized firmware, calibration, and testing, increasing product development cycles by an average of 12%. In addition, the lack of standardized haptic protocols across platforms complicates interoperability, particularly in industrial and medical systems where certification and validation requirements are strict. These factors slow deployment and constrain broader market penetration in price-sensitive segments.

Spatial computing, remote collaboration, and teleoperation represent major emerging opportunities for the Haptic Actuators Market. In remote maintenance and robotics, haptic feedback can improve task accuracy by up to 27% by providing tactile cues during precision operations. Healthcare simulators using haptic interfaces have demonstrated 32% faster skill acquisition among trainees compared to visual-only systems. As enterprises expand virtual training and remote operations to reduce travel and downtime, demand for high-fidelity haptic systems is expected to rise, opening new application areas beyond traditional consumer electronics.

The Haptic Actuators Market faces challenges related to regulatory compliance, material sourcing, and supply chain stability. Environmental regulations are restricting the use of certain rare earth and heavy metal components, forcing redesigns that can increase costs by up to 18%. At the same time, geopolitical tensions and logistics disruptions have increased component lead times by an average of 20%, affecting just-in-time manufacturing models. Compliance with automotive and medical safety standards also requires extensive testing and certification, extending time-to-market and raising entry barriers for smaller manufacturers, thereby limiting competitive diversity and innovation speed.

• Miniaturization and ultra-thin actuator integration: Device manufacturers are rapidly shifting toward thinner and lighter components, driving demand for actuators below 2.0 mm thickness. In 2024, more than 48% of newly launched smartphones integrated ultra-thin linear resonant or piezoelectric actuators, up from 31% in 2021. Power consumption per actuator has declined by approximately 22%, while vibration precision has improved by 19%, enabling higher tactile resolution without compromising battery performance. This trend is especially visible in wearables, where average device weight has fallen by 14% while haptic functionality has expanded by 26% across fitness bands, smartwatches, and medical monitoring devices.

• Expansion of haptics in automotive and mobility interfaces: Haptic feedback is increasingly replacing physical buttons in vehicles to improve safety and interface standardization. Around 41% of new electric and premium vehicles launched in 2024 incorporated haptic touch surfaces for infotainment, climate control, and driver alerts, compared with 24% in 2020. OEM testing shows that tactile alerts reduce driver reaction time by 17% and decrease visual distraction incidents by 21%. In parallel, haptic seat and steering feedback systems are being adopted in over 28% of advanced driver-assistance system platforms.

• Growth of immersive and training-oriented haptic applications: Enterprises are adopting haptics in VR training, simulation, and remote operations. In industrial and medical training environments, haptic-enabled simulators have improved skill acquisition speed by 32% and reduced training errors by 29%. Enterprise adoption of immersive training platforms increased by 37% between 2022 and 2024, with haptic feedback becoming a standard feature in over 45% of new professional simulation systems deployed in manufacturing, healthcare, and defense sectors.

• Shift toward sustainable and low-energy actuator design: Sustainability requirements are reshaping actuator materials and production processes. Manufacturers have reduced actuator energy usage by an average of 18% through low-voltage designs and high-efficiency drivers, while recycled or bio-based materials now account for approximately 23% of non-electronic actuator components. More than 34% of manufacturers have committed to reducing actuator carbon intensity by at least 25% by 2030, reflecting growing alignment between product innovation, regulatory compliance, and corporate ESG strategies.

The Haptic Actuators market is segmented by type, application, and end-user, reflecting how tactile feedback technologies are deployed across industries and product categories. By type, the market ranges from traditional vibration-based actuators to advanced piezoelectric and ultrasonic systems, with differentiation driven by response time, energy efficiency, size, and tactile precision. By application, consumer electronics remains the core demand center, followed by automotive interfaces, industrial human–machine interfaces, healthcare simulators, and emerging XR and robotics use cases. By end-user, device manufacturers, automotive OEMs, industrial automation providers, and healthcare and training institutions shape purchasing patterns, with adoption linked to interface modernization, safety requirements, and user experience differentiation. This layered segmentation highlights a transition from mass-volume, low-cost components toward higher-value, high-performance haptic systems, indicating increasing strategic importance across digital, mobility, and industrial ecosystems.

The Haptic Actuators market includes eccentric rotating mass actuators, linear resonant actuators, piezoelectric actuators, and emerging ultrasonic or electrostatic actuators. Linear resonant actuators currently account for approximately 44% of installed units, while eccentric rotating mass actuators hold around 29%. However, adoption in piezoelectric actuators is rising fastest, with deployment expanding at an estimated 14.8% annually as manufacturers seek thinner profiles, faster response, and lower power usage. Piezoelectric solutions offer up to 35% faster response and about 28% lower energy consumption than rotating motors, making them attractive for premium smartphones, wearables, and automotive touch surfaces. Ultrasonic and electrostatic actuators, though still niche, are gaining attention for mid-air and surface haptics in XR and public interfaces, together contributing roughly 27% of the remaining segments.

Consumer electronics represents the leading application area, accounting for approximately 47% of total usage, driven by smartphones, gaming devices, and wearables integrating tactile feedback as a standard feature. Automotive interfaces follow with about 28%, as touch-based dashboards, haptic steering wheels, and seat feedback systems are adopted to enhance safety and usability. Industrial and healthcare applications collectively account for roughly 25%, spanning operator panels, robotics, training simulators, and medical devices. Among these, automotive applications are expanding fastest, with adoption growing at about 13.2% annually due to electric vehicle platform redesigns and regulatory emphasis on driver attention and safety.

Device manufacturers constitute the leading end-user group, accounting for approximately 46% of demand, primarily from smartphone, wearable, and gaming hardware producers seeking interface differentiation. Automotive OEMs follow with around 31%, driven by the integration of haptic controls into next-generation vehicle platforms. Industrial automation providers and healthcare and training institutions together represent roughly 23%, focusing on safety alerts, precision control, and simulation-based learning environments. Healthcare and training users are expanding fastest, with adoption increasing at an estimated 15.6% annually as hospitals, universities, and defense organizations deploy haptic simulators to improve skills transfer and reduce operational risk.

Asia-Pacific accounted for the largest market share at 46% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 8.1% between 2025 and 2032.

Asia-Pacific recorded shipment volumes exceeding 2.4 billion haptic actuator units in 2024, driven by large-scale smartphone, wearable, and consumer electronics manufacturing in China, Japan, and South Korea. North America accounted for 28% of global demand in 2024, supported by strong automotive, healthcare simulation, and industrial automation adoption. Europe represented around 19%, with higher penetration in automotive and industrial interfaces, while South America and the Middle East & Africa together accounted for approximately 7%, led by digital transformation in mobility, education, and public infrastructure. Regional variation reflects differences in manufacturing concentration, regulatory maturity, digital infrastructure, and consumer technology adoption patterns.

This region accounted for approximately 28% of global demand in 2024, led by the United States and Canada. Key industries driving demand include automotive OEMs, healthcare simulation providers, defense training platforms, and enterprise IT hardware manufacturers. Regulatory focus on driver safety, workplace ergonomics, and accessibility standards is accelerating adoption of tactile alerts over purely visual or audio interfaces. Advanced piezoelectric and ultrasonic haptics are increasingly used in medical simulators and aerospace training systems. A major local automotive supplier expanded its haptic R&D facilities in 2024 to support next-generation electric vehicle platforms. Consumer behavior shows higher enterprise adoption in healthcare and finance, where over 52% of new simulation and training systems include tactile feedback.

Europe represented approximately 19% of global demand in 2024, with Germany, the United Kingdom, and France as the leading markets. Automotive manufacturing, industrial automation, and medical devices are the primary demand drivers. Regulatory frameworks emphasize energy efficiency, recyclability, and workplace safety, pushing manufacturers toward low-power and sustainable actuator designs. Emerging technologies such as surface haptics and mid-air feedback are being tested in public transport and smart city applications. A leading German automotive electronics supplier introduced recyclable actuator housings in 2024, reducing material footprint by 22%. Consumer behavior reflects strong regulatory pressure, leading to higher demand for compliant and energy-efficient haptic solutions.

Asia-Pacific led the market with approximately 46% share and the highest unit production globally. China, Japan, and South Korea together produced over 1.8 billion actuator units in 2024, largely for smartphones, wearables, and gaming devices. Manufacturing clusters benefit from automation, component localization, and export-oriented production. Regional innovation hubs in Shenzhen, Seoul, and Tokyo are driving development of ultra-thin and low-power haptic modules. A major Chinese component supplier commissioned a new automated line in 2024, increasing output capacity by 18%. Consumer behavior shows growth driven by mobile gaming, e-commerce interfaces, and super-app ecosystems.

South America accounted for approximately 4% of global demand, with Brazil and Argentina as the primary markets. Adoption is linked to smartphone penetration, localized content delivery, and digital education platforms. Infrastructure modernization and trade agreements are improving access to advanced electronics components. Government incentives for local assembly are encouraging import substitution. A Brazilian consumer electronics assembler introduced haptic-enabled educational tablets in 2024 for public schools. Consumer demand is tied to media consumption, mobile services, and language-localized applications that benefit from tactile feedback.

This region represented approximately 3% of global demand, led by the UAE, Saudi Arabia, and South Africa. Demand is driven by smart city projects, oil and gas automation, aviation training, and digital education. Governments are investing heavily in technology-enabled infrastructure and public services. A UAE-based smart infrastructure developer integrated haptic interfaces into public service kiosks in 2024, improving accessibility for visually impaired users by 26%. Consumer behavior reflects growing interest in accessible digital services and mobile-first government platforms.

China Haptic Actuators Market – 32% share driven by high production capacity and vertically integrated electronics manufacturing

United States Haptic Actuators Market – 21% share supported by strong end-user demand in automotive, healthcare, and defense sectors

The Haptic Actuators market is moderately fragmented, with over 120 active global competitors ranging from specialized component manufacturers to integrated electronics suppliers. The top five companies—including Alps Alpine, AAC Technologies, TDK, Precision Microdrives, and Nidec—collectively hold approximately 62% of total market share, reflecting a strong concentration among leading players while leaving room for emerging innovators. Competitive strategies focus heavily on technological differentiation, with 47% of companies investing in piezoelectric and ultrasonic actuator development, while 38% prioritize low-power and miniaturized modules for smartphones, wearables, and automotive applications. Strategic initiatives include cross-industry partnerships, joint R&D ventures, and targeted acquisitions to expand production capacity or regional presence. In 2024 alone, 15 major product launches were reported globally, highlighting the emphasis on enhanced tactile resolution, durability, and energy efficiency. Innovation trends include AI-driven adaptive feedback systems, surface haptics, and mid-air tactile solutions. Companies are also aligning with sustainability goals, incorporating recyclable materials and reducing actuator power consumption by 15–20% across new product lines, reinforcing competitive positioning in compliance-focused markets.

Precision Microdrives

Nidec

Johnson Matthey Electronics

Shenzhen O-Film Tech

Samsung Electro-Mechanics

Panasonic Corporation

CTS Corporation

The Haptic Actuators market is witnessing rapid technological evolution, with both incremental improvements and breakthrough innovations shaping product performance and adoption. Linear resonant actuators (LRA) and piezoelectric actuators dominate current deployment, with LRAs accounting for roughly 44% of installed units and piezoelectric actuators representing nearly 28%. Piezoelectric modules are increasingly adopted in wearables and automotive interfaces due to their 35% faster response time and 28% lower energy consumption compared to traditional eccentric rotating mass actuators. Miniaturization is a key trend, with actuator thickness reduced to below 2 mm in over 48% of newly launched consumer electronics, enabling slimmer smartphones and ultra-light wearable devices without compromising haptic intensity or precision.

Emerging technologies are expanding the application landscape, particularly in immersive and industrial environments. Ultrasonic mid-air haptics, currently in pilot deployments across 14 enterprise VR training platforms, allow users to experience tactile feedback without physical contact, enhancing safety and user engagement. Surface haptics are being integrated into automotive dashboards and public kiosks, improving interaction accuracy in more than 32% of advanced vehicles launched in 2024. AI-driven adaptive feedback systems are also gaining traction, dynamically adjusting vibration patterns to user behavior, resulting in measured 22% reductions in interface error rates during pilot trials.

Material and energy efficiency innovations are shaping sustainability and regulatory compliance. Low-voltage driver circuits and high-efficiency piezo elements have reduced average actuator energy consumption by 18%, while approximately 23% of actuator housings now utilize recycled or bio-based materials. Forward-looking technology pathways include integration with spatial computing, tactile-enabled XR applications, and smart surfaces, positioning the Haptic Actuators market at the intersection of interface innovation, energy efficiency, and immersive user experience.

• In June 2024, HaptX began North American shipments of its HaptX Gloves G1, a next‑generation haptic feedback system featuring hundreds of microfluidic actuators that deliver ultra‑realistic touch and force sensations for enterprise VR and robotics training applications, enhancing ergonomic fit and multi‑user collaboration features.

• In late 2024, Alps Alpine launched its compact Haptic Reactor “U‑Type,” achieving approximately a 90% size reduction compared to previous models while maintaining high vibration performance, enabling integration into space‑constrained automotive steering wheels and control modules. (alpsalpine.com)

• In September 2023, TDK Corporation unveiled the PowerHap Development Starter Kit for multilayer piezo actuators, providing engineers with a rapid prototyping platform for high‑precision haptic feedback across automotive, handheld, and industrial applications. (TDK)

• In June 2024, Bosch acquired Tactile Labs to accelerate integration of advanced tactile actuator arrays and haptic sensing solutions into automotive interiors, strengthening its position in next‑generation human–machine interface technologies. (WiseGuy Reports)

The Haptic Actuators Market Report comprehensively examines the range of technologies, product types, application areas, and geographic dynamics that define this ecosystem. It covers all major actuator technologies including linear resonant actuators, piezoelectric models, and emerging ultrasonic and surface haptic systems, providing detailed segmentation by type and capturing adoption patterns across consumer electronics, automotive interfaces, industrial control systems, healthcare simulators, and extended reality environments. The report also analyzes regional performance across Asia‑Pacific, North America, Europe, South America, and Middle East & Africa, offering unit volumes, consumer behavior insights, and adoption trends that inform strategic planning and competitive benchmarking.

In addition to core segments, the report explores niche and emerging areas such as mid‑air haptic systems, multi‑modal force feedback solutions, and software development kits that enable tactile integration for third‑party applications. Industry focus areas include human–machine interface modernization, immersive training and simulation, tactile feedback in autonomous mobility platforms, and wearable device integration. Technology chapters highlight miniaturization trends, energy‑efficient designs, adaptive feedback algorithms, and material innovations that enhance actuator performance and sustainability. The report’s structured analysis supports decision‑makers with actionable intelligence on supplier positioning, innovation pipelines, regulatory impacts, and end‑user adoption behavior to inform investment, product development, and go‑to‑market strategies in the evolving global Haptic Actuators landscape.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 6672.34 Million |

Market Revenue in 2032 | USD 11209.69 Million |

CAGR (2025 - 2032) | 6.7% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Alps Alpine, AAC Technologies, TDK Corporation, Precision Microdrives, Nidec, Johnson Matthey Electronics, Shenzhen O-Film Tech, Samsung Electro-Mechanics, Panasonic Corporation, CTS Corporation |

Customization & Pricing | Available on Request (10% Customization is Free) |