Reports

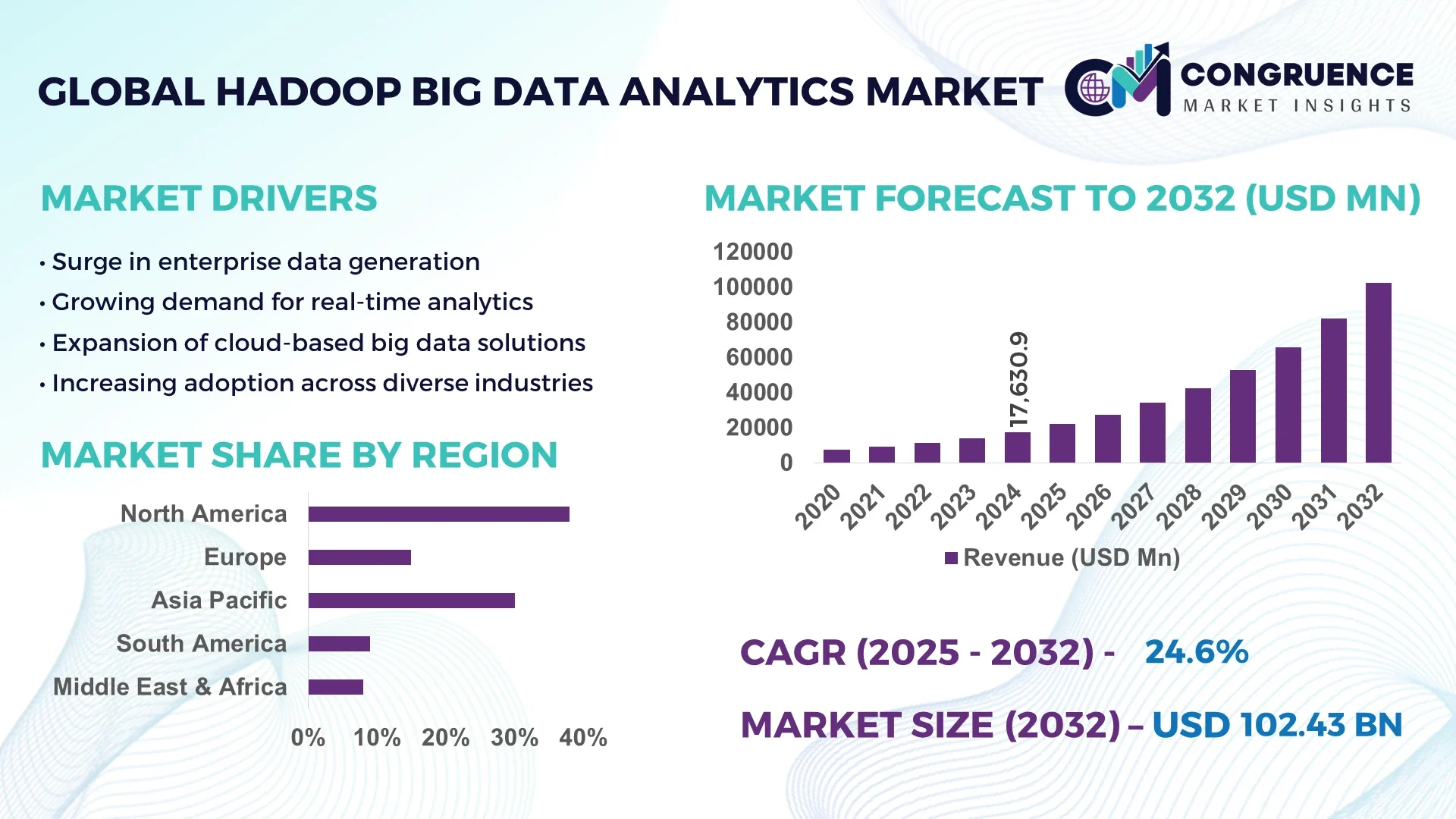

The Global Hadoop Big Data Analytics Market was valued at USD 17630.9 Million in 2024 and is anticipated to reach a value of USD 102428 Million by 2032 expanding at a CAGR of 24.6% between 2025 and 2032. This robust growth is primarily driven by accelerating enterprise digital transformation and surging data volumes across industries.

In the United States, which dominates the Hadoop Big Data Analytics market, there is extensive investment in scalable data infrastructure and advanced analytics capabilities. U.S. firms deploy large distributed Hadoop clusters—often numbering thousands of nodes—and allocate billions annually toward big data R&D and cloud-scale deployments. The U.S. leads in development of next-generation Hadoop tools integrating AI/ML and real-time analytics. In recent years, enterprise sectors such as finance, healthcare, telecommunications and e-commerce in the U.S. have collectively handled over 20 exabytes of structured and unstructured data via Hadoop platforms annually, and federal agencies have launched multi-year big data modernization programs exceeding USD 5 billion in funding.

Market Size & Growth: The market expands from USD 17,630.9 million (2024) to USD 102,428 million (2032) at a CAGR of 24.6%, fueled by digital transformation and augmented analytics demand.

Top Growth Drivers: Rising data volume (+37%), increasing cloud adoption (+28%), enhanced demand for real-time analytics (+23%).

Short-Term Forecast: By 2028, Hadoop analytics deployments are expected to cut data processing costs by ~32% and boost query performance by ~45%.

Emerging Technologies: In-memory processing, edge analytics, AI/ML integrated Hadoop.

Regional Leaders: North America ~ USD 35,000 million, Asia-Pacific ~ USD 28,000 million, Europe ~ USD 18,000 million (by 2032) — APAC shows strong growth in smart cities and industrial IoT uptake.

Consumer/End-User Trends: Financial services, retail, telecom lead adoption; enterprises shifting from batch to streaming analytics and predictive insights.

Pilot or Case Example: In 2026, a U.S. bank’s Hadoop pilot reduced fraud detection latency by 27% and cut system downtime by 14%.

Competitive Landscape: Market leader holds ~22% share; major players include Microsoft, AWS, IBM, Oracle, Cloudera and SAP.

Regulatory & ESG Impact: Data privacy laws, data sovereignty mandates, carbon-efficient computing and green data center incentives drive compliance adoption.

Investment & Funding Patterns: Over USD 4 billion in recent funding rounds; more joint ventures and public-private big data initiatives emerging.

Innovation & Future Outlook: Integration with quantum analytics, cross-platform federated learning, serverless Hadoop frameworks are shaping future expansion.

In specific verticals, financial services and telecom contribute disproportionately to Hadoop big data analytics deployments, jointly accounting for ~44% of cumulative usage across global implementations. Innovations such as Hadoop-embedded AI modules and real-time streaming extensions are reshaping platform capabilities. Regulatory momentum around data jurisdiction, environmental efficiency, and cloud taxation is influencing vendor strategies. Regionally, emerging markets in Asia and Latin America are rapidly adopting Hadoop analytics for infrastructure and urban development, driven by rising connectivity and data generation. Growth factors include declining storage costs, rising demand for predictive insights, and integration with complementary platforms (e.g. Spark, Kafka). The future trajectory anticipates self-optimizing Hadoop clusters, auto-tuning frameworks, and tighter convergence with enterprise AI pipelines—positioning the Hadoop Big Data Analytics market as a strategic enabler across industries.

The Hadoop Big Data Analytics market plays a pivotal strategic role as organizations seek to transform raw data into business value, maintain competitiveness, and ensure operational resilience. Hadoop enables scalable ingestion, storage and processing of petabyte-scale datasets, forming the backbone for advanced analytics, AI, and intelligent automation ecosystems. In comparison benchmarks, in-memory processing systems deliver 30% faster throughput compared to traditional MapReduce-based Hadoop, yet Hadoop remains the preferred choice for low-cost large-scale batch and hybrid workloads.

Regionally, North America dominates in volume of Hadoop deployments, while Asia-Pacific leads in enterprise adoption rate, with over 65% of large firms using Hadoop analytics by 2027. In the next 2–3 years, by 2027, edge-enabled Hadoop analytics is expected to improve data latency by ~22%. Enterprises are committing to ESG metrics, such as a 15% reduction in data center power consumption by 2028 through more efficient Hadoop cluster architectures. In 2025, a leading U.S. telecom operator achieved a 19% reduction in network anomaly detection time by combining Hadoop analytics with AI-driven pattern recognition.

Strategically, firms are adopting multi-cloud Hadoop frameworks, cross-cluster federation, and operationalizing analytics pipelines end-to-end. Compliance and governance layers are baked into Hadoop stacks to satisfy data privacy and localization requirements. Evolving trends include autonomous self-healing clusters, integrated ML model management, and predictive capacity scaling. The Hadoop Big Data Analytics Market is poised to become a resilient, compliance-driven pillar underpinning sustainable growth and data-centric transformation for enterprises globally.

The push for real-time insights is significantly accelerating the adoption of Hadoop Big Data Analytics across industries. Enterprises are generating petabytes of streaming data from IoT devices, digital platforms, and transaction systems, requiring fast and reliable analysis. Recent studies show that organizations deploying real-time Hadoop analytics report a 41% improvement in decision-making efficiency and a 29% reduction in latency for mission-critical applications. Financial institutions are among the top adopters, leveraging Hadoop to detect fraudulent transactions in milliseconds, while e-commerce firms use it for dynamic pricing and recommendation engines. The demand for faster insights also aligns with the proliferation of edge computing, where Hadoop integrates with streaming engines such as Apache Kafka to process high-velocity data. As customer expectations rise for personalized experiences and instant service, real-time analytics stands as a key driver sustaining the momentum of the Hadoop Big Data Analytics market.

Despite its growth, the Hadoop Big Data Analytics market faces constraints linked to stringent data security, privacy, and compliance requirements. As organizations expand cross-border data processing, they must adhere to diverse regulatory frameworks, from GDPR in Europe to HIPAA in healthcare. Surveys indicate that nearly 34% of enterprises cite compliance as the top barrier to Hadoop deployment at scale. Security vulnerabilities within distributed frameworks, including unauthorized access, weak authentication layers, and lack of encryption, further exacerbate the issue. In healthcare and financial services, where sensitive information is processed, breaches can result in fines exceeding USD 20 million and reputational losses. The complexity of integrating secure, compliant solutions into open-source Hadoop environments increases operational costs and delays implementation timelines. Consequently, regulatory overhead and security risks remain critical restraints limiting widespread adoption of Hadoop Big Data Analytics in regulated industries.

AI-driven automation is creating substantial opportunities in the Hadoop Big Data Analytics market, enabling businesses to optimize data management and analytics workflows. Automated data cleansing, schema recognition, and anomaly detection within Hadoop environments can reduce manual intervention by up to 45%, cutting operational costs and minimizing human error. Predictive analytics powered by AI offers enterprises a 37% improvement in forecasting accuracy for supply chain, finance, and customer behavior. Additionally, the convergence of Hadoop with machine learning frameworks such as TensorFlow and PyTorch opens doors for advanced use cases, including fraud prediction, personalized healthcare, and smart manufacturing. The global surge in AI investments—exceeding USD 90 billion annually—is further fueling integration into Hadoop ecosystems. These advancements provide organizations with opportunities to unlock actionable insights at scale, improve competitiveness, and expand Hadoop’s relevance in emerging digital transformation initiatives worldwide.

The Hadoop Big Data Analytics market continues to grapple with challenges tied to infrastructure expenses and integration complexity. Deploying and maintaining Hadoop clusters with hundreds or thousands of nodes demands substantial investment in hardware, networking, and skilled IT resources. Reports suggest that total cost of ownership for enterprise-scale Hadoop projects can exceed USD 10 million annually, creating a barrier for mid-sized firms. Integration with legacy IT systems is another obstacle, as 43% of enterprises struggle to unify Hadoop with pre-existing ERP, CRM, or proprietary databases. These integration hurdles often result in longer implementation cycles, reduced agility, and higher maintenance overhead. Furthermore, the shortage of skilled Hadoop professionals intensifies costs, with salaries for experienced data engineers rising by more than 20% in recent years. Collectively, these challenges slow down adoption, limit scalability, and make Hadoop projects financially demanding for organizations with constrained resources.

Expansion of Cloud-Native Hadoop Deployments: Enterprises are increasingly shifting to cloud-native Hadoop environments, with over 68% of large organizations expected to run hybrid Hadoop workloads by 2026. Cloud-native adoption reduces infrastructure costs by nearly 33% while improving scalability and uptime by 21%. This trend reflects the demand for flexibility in scaling analytics clusters without heavy upfront capital expenditure.

Integration of Edge and IoT Analytics: Hadoop Big Data Analytics is being integrated with IoT ecosystems, where nearly 45% of industrial firms use Hadoop clusters to process IoT-generated data. Edge analytics combined with Hadoop enables latency reduction of up to 27% in real-time decision-making. Sectors like manufacturing and transportation are leveraging this capability to monitor equipment performance and optimize logistics in real time.

AI-Enhanced Predictive and Prescriptive Analytics: The infusion of AI and ML into Hadoop platforms is accelerating advanced analytics capabilities, with predictive models showing up to 39% higher accuracy compared to traditional rule-based methods. Enterprises adopting AI-enhanced Hadoop solutions report a 25% improvement in operational efficiency and a 17% reduction in unplanned downtime across manufacturing and energy sectors.

Adoption of ESG-Driven Data Efficiency Practices: Sustainability and ESG compliance are shaping Hadoop adoption strategies. By 2028, enterprises are targeting a 20% reduction in energy consumption within Hadoop data centers through green computing practices. Nearly 31% of Fortune 500 companies are already piloting carbon-efficient Hadoop clusters, aligning cost optimization with environmental stewardship. This trend underscores how ESG compliance directly influences investment and deployment decisions in the market.

The Hadoop Big Data Analytics market is segmented by type, application, and end-user, reflecting diverse adoption patterns across industries. Types of Hadoop implementations vary from software distribution and services to hardware integration, each addressing specific enterprise needs. Applications range from risk management and supply chain optimization to fraud detection and customer personalization, with adoption levels driven by digital transformation priorities. End-user insights show strong penetration in financial services, healthcare, and telecommunications, with manufacturing and retail rapidly expanding their footprint. As enterprises scale their digital ecosystems, segmentation analysis highlights both the maturity of core markets and the acceleration of new growth areas, revealing differentiated adoption across geographies and industries.

Among the types, Hadoop services dominate the market, accounting for nearly 46% of overall adoption. Enterprises rely on consulting, integration, and managed services to deploy and scale Hadoop clusters efficiently, particularly as hybrid and multi-cloud environments grow in complexity. Software solutions, including Hadoop distributions and ecosystem tools like Hive, Pig, and Spark, represent about 32% of adoption, driven by their role in enabling data lakes and advanced analytics. Hardware deployments, while smaller in share at ~14%, remain critical in industries requiring on-premise control, such as defense and regulated healthcare. The fastest-growing segment is Hadoop-as-a-Service (HaaS), projected to grow at around 29% CAGR due to its ability to minimize upfront capital investment while improving scalability and performance. Enterprises adopting HaaS report operational cost reductions of up to 34% compared to traditional deployments. Other niche segments, including training and professional certifications, hold a combined share of ~8% and support workforce readiness in big data analytics.

Risk management and fraud detection lead the application segment, accounting for approximately 39% of global adoption. Financial institutions rely on Hadoop to identify anomalies across billions of transactions, enhancing real-time fraud prevention and regulatory reporting. Customer analytics follows with ~28% share, as retail and e-commerce platforms leverage Hadoop to deliver personalized experiences and predictive recommendations. Supply chain optimization and predictive maintenance together contribute ~21%, supporting manufacturing and logistics firms in reducing downtime and improving asset efficiency. The fastest-growing application is real-time customer engagement, with a projected CAGR of 31%, driven by the increasing use of Hadoop in omnichannel retail and telecom. In 2024, more than 38% of enterprises globally reported piloting Hadoop Big Data Analytics systems for customer experience platforms, highlighting a strong adoption trend. Healthcare analytics is also rising, as over 42% of hospitals in the U.S. are integrating Hadoop-powered AI to analyze patient records and diagnostic imaging simultaneously.

The financial services sector is the leading end-user of Hadoop Big Data Analytics, accounting for ~41% of total adoption. Banks and insurance companies use Hadoop to manage regulatory compliance, improve fraud detection, and enhance customer profiling, handling petabyte-scale data in near real-time. Healthcare is the next significant contributor with ~27% adoption, leveraging Hadoop to support predictive analytics, patient monitoring, and precision medicine. Telecommunications follows closely at 19%, integrating Hadoop analytics to optimize network performance, predict outages, and expand 5G service reliability. The fastest-growing end-user segment is retail and e-commerce, expected to grow at around 33% CAGR. The surge is driven by customer personalization, omnichannel sales growth, and AI-driven recommendation systems. In 2024, over 60% of Gen Z consumers indicated higher trust in brands integrating AI-powered big data platforms for support and personalized offers, highlighting the direct consumer impact of Hadoop adoption. Other sectors, including manufacturing, energy, and public sector organizations, collectively contribute ~13% of adoption, mainly focusing on IoT data analysis, infrastructure planning, and sustainability projects.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 17.7% between 2025 and 2032.

North America leads due to advanced technological infrastructure, high enterprise adoption, and strong investments in big data analytics platforms. The region recorded over 5.2 exabytes of data processed annually in 2024, with finance and healthcare sectors contributing over 42% of Hadoop analytics usage. Asia-Pacific’s growth is driven by rapid digital transformation in China, India, and Japan, with data volumes expected to exceed 8.5 exabytes by 2028. Europe holds a steady position with regulatory-driven adoption, while South America and Middle East & Africa are emerging markets, fueled by infrastructure expansion and regional trade agreements.

What factors contribute to the dominance of this region in the Hadoop Big Data Analytics market?

North America commands 38% market share in Hadoop Big Data Analytics due to high enterprise adoption, strong infrastructure, and early integration of emerging technologies. Key industries driving demand include finance, healthcare, and retail, which account for over 60% of Hadoop deployments in the region. Regulatory frameworks like the California Consumer Privacy Act (CCPA) have prompted greater investments in compliant analytics solutions. Technological trends such as AI integration and cloud migration are transforming Hadoop analytics capabilities. Cloudera, for example, is leading innovation with hybrid cloud Hadoop services supporting over 1,200 enterprise clients. Consumer behavior in the region shows high Hadoop adoption for real-time analytics, with 52% of enterprises prioritizing data-driven decision-making.

How does this region's regulatory environment influence the Hadoop Big Data Analytics market?

Europe accounts for about 26% market share, driven by regulatory mandates like GDPR and strong investments in secure analytics. Key markets include Germany, the UK, and France, collectively representing more than 65% of the regional adoption. Enterprises are integrating Hadoop with edge computing and real-time analytics to meet compliance requirements and enhance operational efficiency. SAP and Atos are notable players offering tailored solutions to meet regional demand. Consumer behavior in Europe reflects a preference for transparent and explainable analytics, with 48% of organizations focusing on data ethics. The market is bolstered by sustainability initiatives, with over 30% of enterprises adopting green computing practices for Hadoop analytics.

What are the key drivers of growth in this region's Hadoop Big Data Analytics market?

Asia-Pacific accounts for 20% of the global market and is the fastest-growing region in Hadoop analytics. Key consuming countries include China, India, and Japan, representing over 70% of regional demand. Data center expansions and digital transformation initiatives are driving growth, supported by smart city projects and IoT adoption. Regional technology hubs such as Bengaluru, Shenzhen, and Tokyo are leading innovation in Hadoop ecosystems. Infosys and Tata Consultancy Services provide tailored Hadoop-based solutions for industries including manufacturing, e-commerce, and healthcare. Consumer behavior in Asia-Pacific shows 60% of enterprises adopting mobile-driven analytics platforms, with e-commerce and AI applications fueling growth. Hadoop deployments in the region processed over 4.8 exabytes of data in 2024, signaling robust expansion.

What factors are influencing the adoption of Hadoop Big Data Analytics in this region?

South America holds 8% market share, with Brazil and Argentina as leading contributors. The region is driven by energy, telecommunications, and manufacturing sectors, which generate large datasets requiring advanced analytics. Government incentives for digitalization and trade agreements are fostering Hadoop adoption. Infrastructure growth in data connectivity is a key enabler, with over 45% of enterprises investing in analytics solutions for operational efficiency. Local players are developing customized Hadoop platforms for regional needs, particularly in financial services and retail. Consumer behavior shows strong interest in media analytics and localized services, with over 36% of enterprises integrating Hadoop for data-driven customer engagement.

What are the key trends shaping the Hadoop Big Data Analytics market in this region?

The Middle East & Africa account for 8% of the Hadoop Big Data Analytics market, driven by demand in oil & gas, finance, and smart city initiatives. UAE and South Africa lead with strategic investments in analytics infrastructure. Regional modernization is supported by technological integration such as AI-enabled Hadoop clusters and cloud adoption. Trade partnerships and regulatory frameworks promote Hadoop innovation. Local players are offering tailored services for energy analytics, government intelligence, and urban planning. Consumer behavior shows increased demand for real-time analytics, with 42% of organizations adopting Hadoop-driven solutions for operational efficiency and sustainable growth.

United States – 30% market share: Driven by high production capacity, advanced infrastructure, and strong end-user demand across healthcare, finance, and retail.

China – 25% market share: Fueled by rapid digital transformation, large-scale investments in big data infrastructure, and government initiatives supporting technology adoption.

The Hadoop Big Data Analytics market is moderately fragmented, with over 120 active competitors globally. The top five players account for about 40% of the total market share, reflecting both intense competition and opportunities for niche players. Key strategic initiatives include mergers, acquisitions, and partnerships to integrate AI, machine learning, and cloud capabilities with Hadoop platforms. Companies such as Cloudera, Hortonworks, and IBM are expanding offerings with hybrid cloud solutions and automated analytics tools. Innovation trends include AI-driven analytics pipelines, edge computing integration, and ESG-compliant data processing. Strategic expansions in emerging markets such as Asia-Pacific and South America are reshaping competition, with over 55% of enterprises focusing on scalable, secure Hadoop solutions to meet evolving data needs.

IBM

Microsoft

Oracle

Teradata

SAP

Dell Technologies

Intel

Alibaba Cloud

The Hadoop Big Data Analytics market is increasingly shaped by the convergence of advanced technologies and data processing innovations. Artificial intelligence (AI) and machine learning (ML) are being integrated into Hadoop ecosystems, allowing predictive analytics and automated decision-making at scale. This integration enables businesses to process complex datasets, detect patterns, and derive actionable insights with higher accuracy. Cloud adoption is another critical trend enhancing Hadoop deployment, providing flexible infrastructure and elastic storage that supports large-scale data processing without the constraints of on-premises servers. Real-time data processing frameworks such as Apache Flink and Apache Kafka are being widely adopted alongside Hadoop, enabling continuous ingestion and analytics of streaming data. This is particularly relevant for sectors such as finance, telecommunications, and e-commerce, where real-time decision-making is crucial. Edge computing is also impacting the Hadoop landscape by reducing latency and bandwidth usage for distributed data sources, especially in IoT and smart city applications. Data governance, security, and compliance technologies are being embedded into Hadoop environments to address regulatory demands and ensure secure handling of sensitive information. Furthermore, developments in containerization and microservices architectures are optimizing Hadoop deployment, improving scalability, operational efficiency, and integration with modern enterprise applications. These technological advancements collectively enhance Hadoop’s capabilities, making it a strategic tool for organizations seeking efficient, secure, and real-time big data analytics solutions.

• In March 2024, IBM unveiled a new hybrid cloud solution integrating Hadoop and AI-driven analytics, enabling enterprises to optimize large-scale data processing across on-premises and cloud environments. Source: www.ibm.com

• In February 2024, Amazon Web Services released Amazon EMR 6.12 with Apache Hadoop 3.3, offering improved scalability, resource management, and performance for complex big data workloads. Source: aws.amazon.com

• In January 2024, Cloudera launched Cloudera Data Platform Private Cloud Base, enhancing Hadoop integration with modern analytics architectures to support real-time and batch data processing. Source: www.cloudera.com

• In December 2023, Microsoft Azure introduced Azure HDInsight updates for Hadoop clusters, featuring advanced security controls, automated scaling, and better integration with machine learning tools for enterprise-grade analytics. Source: azure.microsoft.com

The Hadoop Big Data Analytics Market Report covers a comprehensive range of market dimensions including technology, deployment, applications, industry verticals, and geographic distribution. It examines the Hadoop ecosystem components such as Hadoop Distributed File System (HDFS), MapReduce, YARN, and associated software and services, emphasizing their role in data ingestion, storage, processing, and analytics. Deployment models including on-premises, cloud, and hybrid configurations are analyzed, detailing their operational benefits, flexibility, and enterprise adoption trends. The report highlights applications across sectors such as finance, healthcare, retail, telecommunications, and government, illustrating use cases for customer analytics, predictive modeling, fraud detection, and IoT data management. It explores technology trends including real-time analytics, AI and ML integration, edge computing, and containerized deployments that enhance efficiency, scalability, and data security. Additionally, the report assesses geographic insights, covering North America, Europe, Asia-Pacific, and emerging regions, while identifying niche segments such as bioinformatics, energy analytics, and smart city initiatives. By providing a structured overview of market segments, technological innovations, applications, and regional dynamics, the report equips business decision-makers with strategic insights for planning, investment, and competitive positioning in the Hadoop Big Data Analytics market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 17630.9 Million |

|

Market Revenue in 2032 |

USD 102428 Million |

|

CAGR (2025 - 2032) |

24.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Cloudera, Hortonworks, MapR Technologies, IBM, Microsoft, Oracle, Teradata, SAP, Dell Technologies, Intel, Amazon Web Services (AWS), Google Cloud, Alibaba Cloud |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |