Reports

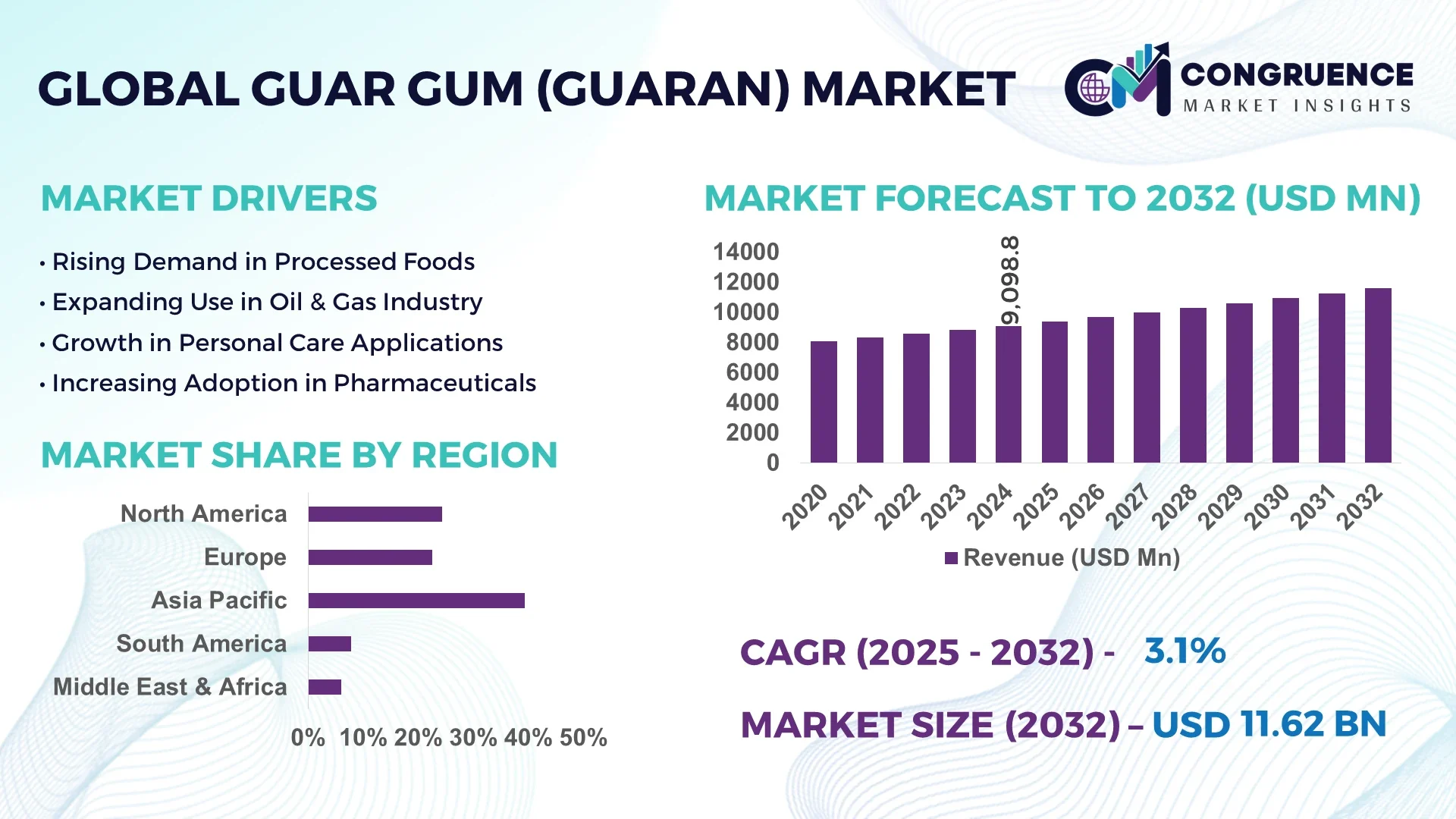

The Global Guar Gum (Guaran) Market was valued at USD 9,098.83 Million in 2024 and is anticipated to reach a value of USD 11,615.96 Million by 2032 expanding at a CAGR of 3.1% between 2025 and 2032.

India dominates the global guar gum market, accounting for nearly 80% of worldwide production. The country’s extensive cultivation regions such as Rajasthan and Gujarat are critical to sustaining the global supply of natural guar gum. India’s strong processing infrastructure and export networks reinforce its leadership in the guar gum industry.

Guar gum, a versatile natural polysaccharide derived from guar beans, holds significant importance in various industrial sectors. The food and beverage industry widely uses guar gum as a natural thickener and stabilizer in products like dairy, baked goods, and sauces. The oilfield sector employs industrial-grade guar gum for hydraulic fracturing fluids to enhance viscosity and improve extraction efficiency. Additionally, guar gum’s applications extend to pharmaceuticals, textiles, and cosmetics, where it acts as a binder, emulsifier, and film-former. The growing demand for eco-friendly and biodegradable ingredients is further fueling innovation and adoption of sustainable guar gum varieties. Increasing consumer preference for gluten-free and organic food products also positively impacts market expansion. Furthermore, ongoing investments in guar gum processing technologies aim to enhance purity and functional performance, catering to diverse application needs.

Artificial Intelligence (AI) is playing an increasingly pivotal role in transforming the guar gum market by improving cultivation, processing, and supply chain efficiencies. In agriculture, AI-powered tools analyze climatic data, soil composition, and crop health to help farmers optimize guar bean yields and reduce resource consumption. This precision agriculture approach leads to consistent, high-quality guar gum production with minimal environmental impact. In manufacturing plants, AI-based automation and real-time monitoring systems enhance process control by ensuring accurate viscosity levels and impurity detection, resulting in superior guar gum grades that meet strict industrial standards. AI-driven predictive analytics are revolutionizing inventory and demand management, enabling companies to minimize waste, avoid stockouts, and streamline logistics. The integration of machine learning algorithms accelerates research and development by simulating guar gum molecular interactions to develop novel formulations tailored for specific end-user requirements such as food texture improvement or enhanced oil recovery. Overall, AI applications in the guar gum market are boosting operational productivity, reducing costs, and supporting sustainable business models aligned with global eco-conscious trends.

"In 2024, a major agritech firm implemented an AI-powered platform in key guar-producing regions of India to provide farmers with real-time data on crop health and weather forecasts, significantly increasing yield predictability and reducing input waste."

The Guar Gum (Guaran) market is influenced by multiple dynamic factors that shape its growth trajectory and industry landscape. Increasing consumer preference for natural and clean-label food additives is driving guar gum demand across food processing sectors. The expanding oil and gas exploration activities continue to support industrial-grade guar gum consumption as a critical component in hydraulic fracturing fluids. Meanwhile, innovations in guar gum extraction and processing technologies are enhancing product quality and widening application scopes. However, the market faces challenges such as fluctuating raw material prices and inconsistent agricultural yields due to climatic conditions. Additionally, the emergence of alternative hydrocolloids and synthetic thickeners exerts competitive pressure on guar gum. Evolving regulations related to food safety and sustainable sourcing are also affecting production practices. Overall, these market dynamics present a complex environment with significant growth potential balanced against operational and environmental challenges.

The primary driver of the guar gum market is the rising demand for natural thickening and stabilizing agents in the food industry. Guar gum is extensively used in baked goods, dairy products, and gluten-free foods due to its excellent water retention and texture-enhancing properties. Increasing consumer inclination toward organic and plant-based ingredients is further elevating its usage. Additionally, the pharmaceutical industry’s growing need for guar gum as a binder, emulsifier, and controlled-release agent in tablet formulations significantly boosts market demand. The cosmetic industry also utilizes guar gum for its moisturizing and film-forming properties. With over 50% of guar gum consumption globally attributed to food and pharmaceuticals combined, this rising trend strongly supports steady market expansion.

One major restraint for the guar gum market is the instability in guar bean production, which depends heavily on weather patterns and regional agricultural practices. Poor monsoon seasons, droughts, or excessive rainfall in major cultivation areas like India can drastically reduce yield, leading to raw material shortages. This fluctuation in guar bean availability results in price volatility for guar gum, impacting profitability across the supply chain. Additionally, the dependence on a limited number of producing countries exposes the market to geopolitical and trade uncertainties. These supply inconsistencies pose challenges for manufacturers aiming to maintain continuous production and meet growing global demand for guar gum-based products.

The guar gum market holds promising opportunities through expanding applications beyond traditional sectors. Rising interest in plant-based and sustainable ingredients has opened new avenues in personal care, cosmetics, and biodegradable packaging industries. Companies are investing in research to develop novel guar gum derivatives and eco-friendly blends that cater to these growing segments. Moreover, the use of guar gum as a natural alternative to synthetic additives in clean-label food products offers significant potential. Increasing urbanization and disposable income in emerging economies are driving demand for convenience foods and beverages containing guar gum. These opportunities encourage innovation and diversification, enabling market players to capture untapped consumer bases and enhance profitability.

The guar gum market faces several challenges, including rising costs of guar beans due to agricultural uncertainties and market demand-supply imbalances. This volatility impacts the affordability and pricing strategies of guar gum products. Furthermore, the presence of synthetic hydrocolloids such as xanthan gum and carboxymethyl cellulose offers competitive alternatives with similar functional properties. These substitutes are often preferred for cost-effectiveness or specific technical advantages in certain applications. Additionally, stringent regulatory requirements for quality and safety impose compliance costs on manufacturers. Balancing the need to maintain product quality while controlling expenses remains a persistent challenge for the guar gum industry.

• Growth in Clean-Label and Organic Food Products:Increasing consumer preference for clean-label ingredients is driving the use of natural guar gum as a preferred thickener and stabilizer in food products. Guar gum’s ability to enhance texture and shelf-life without artificial additives is expanding its adoption in gluten-free, dairy-free, and plant-based food segments globally. Retail sales of clean-label foods incorporating guar gum have seen a significant rise, especially across North America and Europe.

• Expansion of Guar Gum Applications in Oilfield Technologies:The oil and gas industry continues to rely heavily on guar gum for hydraulic fracturing fluids. Recent trends include the development of enhanced guar gum formulations with improved thermal stability and reduced residue, which optimize fracturing efficiency and minimize environmental impact. This is particularly notable in unconventional shale gas extraction regions such as the United States and parts of Asia-Pacific.

• Innovations in Sustainable Guar Gum Processing:Sustainability initiatives are influencing manufacturing processes, with companies adopting water-efficient extraction techniques and eco-friendly drying methods to reduce the carbon footprint of guar gum production. There is also a growing trend toward sourcing guar beans from certified sustainable farms, which aligns with increasing regulatory scrutiny and consumer demand for ethically produced ingredients.

• Rising Demand for Guar Gum in Personal Care and Cosmetics:Guar gum’s moisturizing and film-forming properties are increasingly valued in personal care products such as shampoos, lotions, and facial creams. The global cosmetics industry is witnessing higher incorporation of guar gum as a natural emulsifier and stabilizer, driven by the shift toward botanical and cruelty-free formulations. This trend is especially pronounced in emerging markets where consumer awareness about natural ingredients is growing rapidly.

The Guar Gum (Guaran) market is segmented by type, application, and end-user insights to better understand demand patterns and growth opportunities. Key types include ground guar gum powder, guar gum splits, and refined guar gum, each with distinct functional properties. Application segments cover food and beverages, oilfield, pharmaceuticals, cosmetics, and textile industries. End-user categories primarily consist of food manufacturers, oilfield service providers, pharmaceutical companies, and personal care product makers. Analyzing these segments reveals evolving preferences and usage trends that influence market dynamics globally, driven by innovation, regulatory changes, and shifting consumer demand.

The Guar Gum (Guaran) market includes three primary types: ground guar gum powder, guar gum splits, and refined guar gum. Ground guar gum powder leads the market, accounting for over 55% of total demand due to its versatility in food thickening, stabilizing, and emulsifying. Its high water solubility and viscosity make it ideal for bakery products, sauces, and dairy. Guar gum splits, the coarser form, are mainly used in the oilfield sector, contributing to nearly 30% of the market, prized for their effectiveness in hydraulic fracturing fluids. Refined guar gum, though currently a smaller segment, is the fastest-growing due to rising demand for high-purity guar gum in pharmaceuticals and cosmetics. Innovations in refining processes have increased its functional properties, fueling growth in premium applications.

In terms of application, the food and beverage sector dominates guar gum consumption, representing approximately 45% of the market share. This segment benefits from growing consumer demand for natural additives in gluten-free, dairy-free, and low-fat products where guar gum enhances texture and shelf life. The oilfield application segment is the second-largest, driven by continuous demand for guar-based fracturing fluids used in shale gas extraction, especially in North America and Asia-Pacific. Pharmaceuticals and cosmetics collectively account for around 25%, with rising utilization of guar gum as a binder, stabilizer, and moisturizer boosting growth. The textile and paper industries represent smaller but steadily growing segments due to guar gum's thickening and sizing properties.

End-users of guar gum are broadly categorized into food manufacturers, oilfield service providers, pharmaceutical companies, and personal care product manufacturers. Food manufacturers lead consumption, utilizing guar gum extensively for product formulation and quality enhancement. They contribute over half of the total guar gum market demand globally, reflecting the ingredient’s critical role in food processing. Oilfield service companies are the second-largest end-users, accounting for about 30% of demand, fueled by ongoing hydraulic fracturing projects. Pharmaceutical companies are a fast-growing end-user segment as guar gum’s pharmaceutical-grade variants gain traction in tablet coatings and drug delivery systems. The personal care industry, although smaller in volume, is witnessing rapid growth, driven by rising consumer preferences for natural and plant-based cosmetic ingredients.

Asia-Pacific accounted for the largest market share at 39.3% in 2024; however, Africa is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2025 and 2032.

Asia-Pacific dominates due to its extensive guar cultivation, particularly in India, the world’s largest guar gum producer and exporter. The region's strong demand in food, pharmaceuticals, and oilfield applications continues to support market expansion. Meanwhile, Africa’s growth is driven by increasing adoption of guar gum in personal care and food processing sectors alongside emerging manufacturing capabilities. North America and Europe hold significant shares as well, benefiting from high-value applications and rising natural ingredient demand.

Increasing Demand for Natural Additives in North America

The North American guar gum market is characterized by a rising preference for natural and organic food ingredients. The United States accounts for over 75% of the regional market share, driven by large food processing and oilfield industries. The region also sees growing interest in guar gum use in pharmaceuticals and cosmetics, reflecting consumer inclination toward plant-based and clean-label products. Canada is witnessing steady growth, particularly in the oil and gas sector, where guar gum is essential in hydraulic fracturing fluids. Overall, innovation in product formulations and sustainability initiatives are shaping the North American market landscape.

Focus on Clean-Label Products Boosting Guar Gum Use in Europe

Europe holds approximately 22% of the global guar gum market share, with Germany, the UK, and France leading demand. The food industry is the largest consumer, driven by regulations favoring natural stabilizers and thickeners. Guar gum's application in gluten-free and plant-based foods is expanding rapidly. Additionally, the cosmetics sector in Europe is increasingly incorporating guar gum due to its natural emulsifying and moisturizing properties. The oilfield segment remains smaller but shows potential in countries like Norway. Sustainability in sourcing and eco-friendly processing methods also influence product development and consumption patterns.

Dominance of India and Rising Industrial Applications Across Asia-Pacific

Asia-Pacific dominates with the largest share of over 38%, primarily due to India’s leading role as the top guar gum producer and exporter globally. Indian guar gum accounts for around 80% of global supply. Besides India, China and Australia are expanding their consumption in food processing, pharmaceuticals, and oilfield sectors. Rapid urbanization and growing industrial activities in these countries boost demand for guar gum. The region also sees technological advancements in refining processes, improving product quality for export and domestic applications. The expanding cosmetics and personal care industries in countries like South Korea and Japan are contributing to rising guar gum utilization.

Emerging Market with Growing Food and Beverage Applications

South America holds a smaller share, roughly 8%, but is gaining traction due to increased demand from the food and beverage industry. Brazil and Argentina are key markets, with growing guar gum adoption in bakery, dairy, and beverage sectors. Investments in guar cultivation and processing facilities are gradually improving supply chains. The cosmetics sector is also slowly embracing guar gum for natural product formulations. Oilfield applications remain limited but show potential as exploration activities increase. Overall, South America is expected to become a noteworthy market as consumer awareness and industrial infrastructure develop.

Rapid Growth Driven by Oilfield and Food Industries

The Middle East & Africa region accounts for about 12% of the global market, with the UAE and South Africa leading consumption. The oilfield sector is a major driver, with guar gum used extensively in hydraulic fracturing fluids across oil-rich nations. Food processing industries are expanding, with guar gum utilized in bakery, dairy, and convenience foods. The cosmetics sector is also on the rise, focusing on natural and organic formulations. Investment in guar cultivation and refining technologies is increasing, supported by government initiatives to boost agricultural exports and manufacturing capabilities. Rising health awareness among consumers further fuels demand.

India (38%): India dominates due to its extensive guar cultivation and processing infrastructure, supplying the largest portion of global guar gum demand.

United States (18%): The US leads in high-value applications such as food additives, oilfield fluids, and pharmaceuticals, supported by advanced manufacturing and regulatory frameworks.

The global Guar Gum (Guaran) market exhibits a moderately consolidated competitive landscape dominated by a few key players with extensive product portfolios and strong regional presence. Leading companies focus heavily on innovation, product quality, and sustainable sourcing to gain a competitive edge. The market players invest significantly in expanding manufacturing capacities, with many establishing new processing units in guar-producing regions to meet growing demand efficiently. Strategic partnerships and acquisitions are also prevalent to diversify product lines and enhance geographic reach. Market participants are increasingly adopting advanced processing technologies to improve purity and functional properties of guar gum, aligning with the rising demand from food, pharmaceutical, and oilfield industries. Furthermore, emphasis on eco-friendly and organic guar gum products is shaping competition, as consumers worldwide show greater preference for natural ingredients. This competitive environment fosters continuous improvements in product standards, driving overall market growth.

Archer Daniels Midland Company

Riddhi Siddhi Gluco Biols Ltd.

Vikas WSP Limited

Galaxy Surfactants Ltd.

Tara BioChem Limited

Hindustan Gum & Chemicals Ltd.

Aqualon Company (a division of Ashland Inc.)

GGC Industries Pvt. Ltd.

Ashapura Group

Cargill, Incorporated

The Guar Gum (Guaran) market has experienced notable technological advancements aimed at improving extraction, processing, and product quality. Modern milling techniques have enhanced the efficiency of guar seed processing, increasing guar gum yield by up to 10% compared to traditional methods. Advanced hydration and purification technologies have enabled manufacturers to produce guar gum with higher purity and tailored viscosity levels, catering to diverse industry requirements such as food, pharmaceuticals, and oilfield applications. Innovations in enzyme-assisted extraction have reduced processing time significantly while maintaining the functional properties of guar gum. These enzymatic methods also minimize the use of harsh chemicals, making the production process more environmentally friendly. Furthermore, automation and real-time monitoring systems have been introduced across several guar gum production facilities, improving consistency and reducing human error.

In the oil and gas sector, enhanced guar gum formulations have been developed to withstand extreme temperatures and pressures, increasing their effectiveness as fracturing agents during hydraulic fracturing operations. These formulations improve the viscosity and thermal stability of guar-based drilling fluids. Additionally, packaging technology for guar gum has improved to extend shelf life and preserve quality during transportation and storage. Vacuum-sealed and moisture-resistant packaging solutions are becoming more common, ensuring that guar gum retains its functional properties for longer periods. Overall, technological progress in guar gum production is driving product innovation and expanding its applicability across multiple industries, while also addressing sustainability and efficiency concerns.

In June 2024, LAPP introduced the ETHERLINE® FD bioP Cat.5e, its first bio-based Ethernet cable produced in series. This sustainable variant features a bio-based outer sheath composed of 43% renewable raw materials, reducing the carbon footprint by 24% compared to traditional fossil-based TPU sheaths.

In March 2024, Solvay SA launched Jaguar NAT SGI and Jaguar Excel, biodegradable polymers derived from guar. Jaguar NAT SGI is a rapidly decomposable thickening polymer with an A rating on the Beauty Biodeg Score, while Jaguar Excel is an ultimately degradable conditioning polymer with a B rating, both adhering to OECD guidelines.

In November 2023, IIT Roorkee developed Kodo millet-based edible cups using guar gum and hibiscus powder. This innovation offers a sustainable alternative to traditional plastic cups, aligning with the circular economy model by promoting the use of renewable resources and reducing reliance on fossil-fuel-based plastics.

In October 2023, researchers introduced guar gum-based hydrogels with enhanced biocompatibility and mechanical strength. These hydrogels are designed for medical applications, including wound care and drug delivery systems, showcasing guar gum's versatility beyond traditional industries.

The scope of the Guar Gum (Guaran) market report covers comprehensive insights into the production, consumption, and future potential of guar gum across various industries. It analyzes key segments such as food and beverages, pharmaceuticals, cosmetics, oilfield applications, and textile industries, highlighting their contribution to the overall market demand. The report includes detailed profiling of major manufacturers and suppliers, providing a clear understanding of competitive strategies, product innovations, and market positioning.

The report also examines regional markets with specific focus on top guar gum producing and consuming countries, assessing the impact of agricultural practices, climatic conditions, and government policies on guar gum supply chains. It evaluates the influence of evolving consumer preferences towards natural and clean-label ingredients, which is driving demand in the food and personal care sectors. In addition, the report identifies technological advancements in guar gum extraction and processing that improve product quality and reduce production costs. It discusses packaging innovations that enhance shelf life and product stability during transportation.

Furthermore, the market report explores challenges such as price volatility due to fluctuating raw material availability and regulatory frameworks impacting product approvals. By providing detailed market forecasts and trend analyses, the report serves as a valuable tool for manufacturers, investors, and stakeholders to make informed decisions and capitalize on emerging opportunities within the guar gum industry.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 9098.83 Million |

|

Market Revenue in 2032 |

USD 11615.96 Million |

|

CAGR (2025 - 2032) |

3.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Archer Daniels Midland Company, Riddhi Siddhi Gluco Biols Ltd., Vikas WSP Limited, Galaxy Surfactants Ltd., Tara BioChem Limited, Hindustan Gum & Chemicals Ltd., Aqualon Company (a division of Ashland Inc.), GGC Industries Pvt. Ltd., Ashapura Group, Cargill, Incorporated |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |