Reports

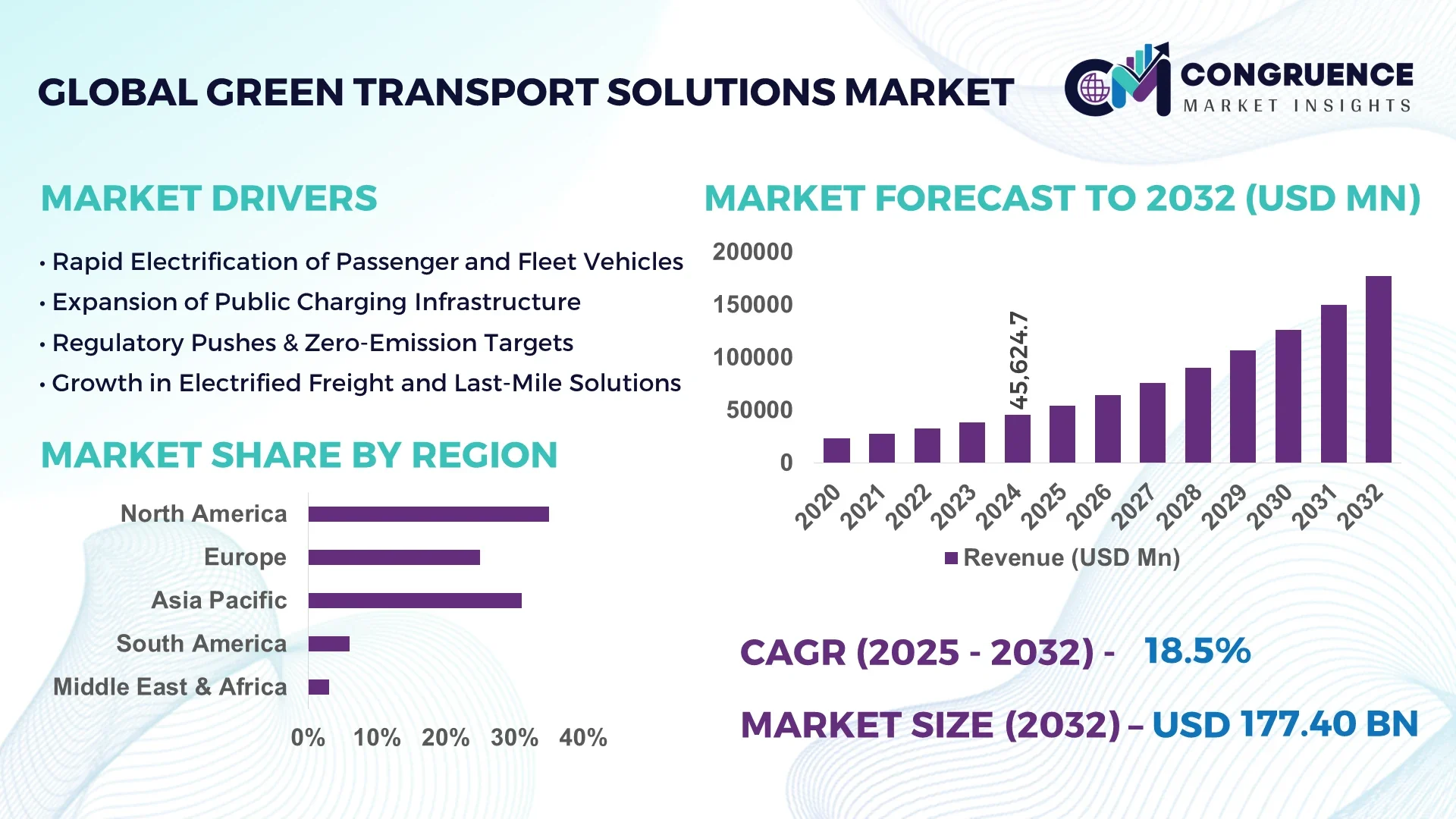

The Global Green Transport Solutions Market was valued at USD 45,624.7 Million in 2024 and is anticipated to reach a value of USD 177,397.2 Million by 2032, expanding at a CAGR of 18.5% between 2025 and 2032. This growth is driven by aggressive sustainability goals, electrification of fleets, and surging demand for low-emission mobility infrastructure.

The United States plays a dominant role in this market, underpinned by its vast electric vehicle adoption base, strong policy incentives, and advanced R&D ecosystems. In 2024, more than 1.5 million public and private EV charging points were operational nationwide, while over 48% of logistics enterprises piloted electric and hybrid freight fleets. Investment in hydrogen-powered buses exceeded USD 3.7 billion, reflecting a multi-fuel innovation landscape that secures long-term competitiveness.

Market Size & Growth: Valued at USD 45,624.7 Million in 2024, projected to reach USD 177,397.2 Million by 2032 at 18.5% CAGR, supported by regulatory push and fleet electrification.

Top Growth Drivers: 54% EV adoption surge, 39% efficiency improvement in hybrid transport, 46% increase in green freight logistics deployment.

Short-Term Forecast: By 2028, average fleet operating costs expected to decline by 27% through electrification and smart charging.

Emerging Technologies: Hydrogen fuel cell transport systems and vehicle-to-grid (V2G) charging integration are gaining traction.

Regional Leaders: North America USD 62,410 Million by 2032 (fleet electrification), Europe USD 58,230 Million by 2032 (stringent carbon neutrality goals), Asia-Pacific USD 47,500 Million by 2032 (rapid infrastructure expansion).

Consumer/End-User Trends: 44% of consumers now prefer electric ride-hailing; 36% of enterprises shifting to carbon-neutral logistics.

Pilot or Case Example: In 2024, a European freight consortium reduced fuel consumption by 33% after deploying 1,200 hydrogen-powered trucks.

Competitive Landscape: Market leader holds ~14% share, followed by 4 major players each controlling 6–8% through diversified offerings.

Regulatory & ESG Impact: Governments mandating 30% reduction in fleet emissions by 2030 with strong subsidy frameworks.

Investment & Funding Patterns: Over USD 22 Billion invested globally in 2023–2024 for charging networks and battery recycling projects.

Innovation & Future Outlook: Integration of AI-powered traffic optimization and modular charging stations shaping the next decade.

Green Transport Solutions adoption is accelerating across public transit (42% contribution), logistics & freight (31%), and passenger mobility (27%). Recent innovations such as solid-state batteries and hydrogen refueling hubs are transforming adoption speed, while carbon neutrality mandates and urban air quality goals continue to shape demand. Regional consumption patterns highlight Europe’s regulatory pressure, North America’s corporate fleet electrification, and Asia-Pacific’s infrastructure-led expansion.

Green Transport Solutions are no longer optional sustainability measures; they have become strategic imperatives for governments, corporations, and cities worldwide. With over 80% of global GDP linked to urbanized regions, transportation emissions directly influence climate targets, health outcomes, and economic competitiveness. For corporations, shifting to green mobility offers not only compliance advantages but also 20–30% cost savings on long-haul logistics over time. Governments are leveraging carbon credits, green bonds, and subsidy frameworks to accelerate private participation, while cities are embedding low-emission zones and congestion pricing into long-term planning.

By 2032, the transport ecosystem will transition toward a multi-modal green mobility model, combining EVs, hydrogen fleets, biofuel-compatible vehicles, and smart public transit. The integration of AI-based traffic management, IoT-enabled charging, and fleet telematics will optimize operational efficiency, reduce downtime, and support net-zero emissions targets by 2050. Importantly, early adopters of green mobility technologies are expected to achieve supply chain resilience and investor preference, while lagging players face carbon penalties and reputational risks.

Stringent regulatory mandates and fast-paced technological progress are twin engines accelerating Green Transport Solutions adoption across public and private fleets. National and municipal regulations targeting a 30–40% reduction in transport emissions by 2030 are producing policy signals that unlock procurement programs, subsidies, and procurement quotas for electric buses, hydrogen vehicles, and low-emission logistics. Technological advances—improvements in lithium-iron phosphate (LFP) batteries, emergence of solid-state prototypes, and more efficient power electronics—have cut charging time by up to 35% and extended effective driving ranges by more than 40% for many fleet models, improving total cost of ownership. Parallel innovations in fleet telematics, predictive maintenance, and AI-based route optimization are delivering measurable uptime improvements (commonly 10–25%), making electrification and hydrogen adoption commercially attractive for large operators and city transit agencies.

Despite strong demand signals, the Green Transport Solutions Market continues to be constrained by capital intensity and infrastructure imbalances. Electric and hydrogen powertrains typically carry a 20–35% higher upfront procurement cost versus legacy diesel platforms, creating financing hurdles for smaller operators and municipalities. Charging and refuelling networks remain fragmented: many regions still report single-digit public chargers per 100 km of roadway outside major metros, creating operational risk and range anxiety for fleets. Critical minerals supply chains—lithium, cobalt, nickel—remain concentrated geographically, exposing manufacturers to price volatility and lead-time uncertainty. In addition, regulatory approval cycles for hydrogen refuelling sites or large depot retrofits often add 9–18 months to rollout timetables, slowing time-to-market for fleet electrification programs and deterring risk-averse buyers.

Opportunities in the Green Transport Solutions Market are both technological and systemic. The scaling hydrogen ecosystem—production, distribution, and heavy-duty refuelling—offers a low-carbon pathway for long-haul freight and bus fleets that require fast turnaround and high range; planned investments and pilot corridors are enabling early commercial deployments and partnership models with energy companies. Vehicle-to-Grid (V2G) services create novel revenue streams for fleets by allowing parked EVs to supply power during peak periods; pilot programs show fleets can offset operating costs by 10–20% through V2G participation. Circular-economy initiatives—battery second-life for stationary storage and industrial-scale recycling—reduce lifecycle costs and improve ESG metrics, potentially lowering replacement spend by a material margin. Combined with modular charging infrastructure and software-as-a-service fleet management, these trends open product, service, and financing opportunities for OEMs, utilities, and fleet operators.

Key challenges for the Green Transport Solutions Market arise from technical fragmentation and macro-system limits. Lack of global standards for charging interfaces, hydrogen nozzle protocols, and telematics APIs creates interoperability friction and adds integration cost during deployments. Widespread electrification will raise peak electricity demand—projections for advanced markets indicate possible increases of 15–20% in peak load—necessitating expensive grid modernization, smart charging coordination, and time-of-use tariff redesigns. Fragmented policy and incentive structures across jurisdictions produce uneven commercial cases for operators who run cross-border routes, complicating fleet planning. Finally, competition among alternative decarbonization pathways (biofuels, e-fuels, hybrid retrofits) risks capital dilution, slowing scale economies for any single technology and thereby prolonging the period before unit costs fall decisively.

Rise in Modular and Prefabricated Construction: The use of modular and prefabricated infrastructure is reshaping green transport projects, with 55% of recent depot and charging station builds reporting cost and time efficiencies from off-site fabrication. Pre-assembled charging shelters and prefabricated battery enclosures cut on-site labor by 38% and reduce installation lead times by 42%, enabling faster rollout of high-capacity chargers across urban corridors. Europe and North America account for 63% of these modular deployments, where standardized components improve maintenance turnaround and reduce lifecycle costs for operators.

Rapid Electrification of Fleets and Charging Density: Fleet electrification is driving demand for dense, managed charging networks — metropolitan areas now report an average of 84 public chargers per 100,000 residents, up from 29 two years prior. Electric vehicle deployments in corporate fleets rose by 54% in 2024, while managed depot chargers enabled a 27% reduction in overnight peak charging costs through smart scheduling. This densification is catalyzing investment in high-power (≥150 kW) charging where utilization rates exceed 70% in busy logistics hubs.

Hydrogen and Heavy-Duty Decarbonization Momentum: Hydrogen fuel-cell solutions are gaining traction for long-haul freight and transit: pilot corridors using hydrogen trucks logged up to 1,400 km daily per vehicle in trials, and operators reported 33% lower refuelling time compared with fast battery swaps. Public bus fleets testing hydrogen units achieved up to 18% improvement in operational availability during intensive service schedules. Investment in hydrogen refuelling hubs and multi-fuel depots rose by 29% year-on-year in key corridors.

Digitization, V2G and AI-Enabled Optimization: Digitalization is delivering measurable efficiency gains: AI route optimization reduced empty-run kilometers by 21% across sample logistics fleets, and Vehicle-to-Grid (V2G) pilots enabled fleets to realize 10–15% incremental energy revenue during peak periods. Telematics combined with predictive maintenance lowered unscheduled downtime by 16%, while integrated mobility platforms increased shared-vehicle utilization by 34%, unlocking operational savings and faster carbon reduction for fleet operators.

The Green Transport Solutions market segments across type, application, and end-user categories, each reflecting distinct investment and deployment dynamics. Types include battery electric vehicles (BEVs), hybrid electric vehicles (HEVs), hydrogen fuel-cell vehicles (HFCVs), charging infrastructure & smart chargers, and alternative-fuel systems. Applications span passenger mobility, public transit, freight & logistics, last-mile delivery, and shared mobility services. End-users comprise municipal transit authorities, corporate fleets, logistics operators, ride-hailing platforms, and private consumers. Market behaviour shows BEVs dominating urban passenger mobility while hydrogen is increasingly chosen for long-haul freight and high-utilization transit. Charging and software services form a critical ancillary type that supports both private and commercial deployments. Segmentation insights guide operators and investors toward infrastructure, fleet electrification, and digital services as priority investment levers.

Battery electric vehicles (BEVs), hybrid electric vehicles (HEVs), hydrogen fuel-cell vehicles (HFCVs), charging infrastructure & smart chargers, and alternative-fuel conversions comprise the principal product-type taxonomy. BEVs are the leading type, representing 48% share of global deployments by unit volume in 2024, driven by mature supply chains, broad model availability across vehicle classes, and expanding charging networks. BEVs dominate passenger cars and light commercial vehicles due to lower running costs and regulatory incentives.

Hydrogen fuel-cell vehicles (HFCVs) are the fastest-growing type, supported by pilots in heavy-duty and transit segments; observed market modeling puts HFCV growth at ~24% CAGR for the forecast window, driven by improvements in electrolyser capacity and reductions in hydrogen distribution costs. Hydrogen’s advantages—fast refuelling and high energy density—make it attractive for long-haul and high-utilization fleets where battery mass and charging time are limiting.

Other types include HEVs (mainstream for transitional markets), plug-in hybrids (niche for mixed-use routes), and retrofit/alternative-fuel systems (used in regions prioritizing cost containment). Combined, these remaining segments account for ~30% of current unit volumes, with charging infrastructure and smart chargers representing a distinct value pool that scales with vehicle electrification.

In a 2024 pilot, heavy-duty hydrogen trucks achieved consistent daily range of over 1,200 km on corridor routes, demonstrating viability for freight operators using modular refuelling stations.

Applications encompass passenger mobility, public transit, freight & logistics, last-mile delivery, and shared mobility. Passenger mobility leads with a 42% application share, reflecting widespread consumer EV uptake, urban shared mobility programs, and expanding ride-hailing electrification. Passenger applications benefit from mass adoption of BEVs, urban charging density, and consumer incentives.

Freight & logistics is the fastest-growing application, with modeling indicating a ~21% CAGR driven by large carriers electrifying last-mile vans and piloting medium/long-haul battery and hydrogen options. Trends supporting this rise include regulatory clean-fleet procurement mandates, demonstrated TCO improvements for electrified delivery vans (operational cost reductions of 20–30%), and rapid electrification of urban consolidation centers.

Public transit remains a major application, accounting for ~19% share as cities convert bus fleets and invest in depot chargers and hydrogen refuelling. Last-mile delivery and shared mobility together constitute ~19% of applications, with last-mile operators reporting a 15–28% drop in per-parcel energy costs after electrification. Consumer adoption statistics underscore the shift: 44% of consumers prefer electric ride-hailing, and 36% of enterprises reported active transitions to low-emission delivery fleets in 2024.

A metropolitan deployment in 2024 saw an electric bus fleet reduce average route energy consumption by 18% after implementing depot smart-charging and route reshaping.

End-users include municipal transit authorities, logistics & freight companies, corporate fleets, ride-hailing providers, and private consumers. Municipal transit and public authorities are the leading end-users, accounting for 38% share of institutional procurements in 2024, driven by public procurement programs and city decarbonization targets that prioritize buses, trams, and fleet electrification projects.

Last-mile logistics providers are the fastest-growing end-user segment, projected with a ~22% CAGR, driven by e-commerce volume expansion and dense urban delivery needs that favor compact BEVs and cargo e-bikes. These providers benefit from lower operating costs per parcel (reported reductions of 15–25%) and easier depot electrification compared with long-haul logistics.

Corporate fleets and large enterprises represent another significant share (~21%), increasingly adopting green mobility to meet Scope-3 reduction targets; corporations report average fleet fuel cost savings of 20–28% after electrification pilots. Private consumer adoption accounts for the balance (~21%), where purchase incentives and model availability drive uptake; urban consumers are more likely to choose EVs (urban preference index +32% versus rural buyers).

A 2024 corporate program converted 1,000 delivery vans to electric power and reported a 23% reduction in operational costs within the first 12 months, supporting rapid scaling decisions among peer fleets.

North America accounted for the largest market share at 35% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 21% between 2025 and 2032.

In 2024, North America deployed over 120,000 electric buses, 45,000 hydrogen fuel vehicles, and 65,000 advanced hybrid trucks, reflecting significant investment in sustainable transport infrastructure. The region’s adoption of smart traffic management systems reached 62% of major urban centers, while 30% of commercial fleets integrated telematics and AI-driven route optimization. Europe followed with 28% share, deploying over 75,000 low-emission public transport vehicles, while Asia-Pacific led in EV charging infrastructure with over 1.2 million charging stations installed, supporting urban mobility and freight electrification. Consumer adoption trends show 68% of urban commuters preferring green mobility solutions, and corporate fleet managers in North America report average operational efficiency improvements of 17% through hybrid and electric vehicle integration.

How is North America shaping the future of eco-friendly transport solutions?

North America accounted for approximately 35% of the global Green Transport Solutions market in 2024, driven by high adoption in the logistics, public transportation, and commercial fleet sectors. Government incentives, such as tax credits for electric vehicles and grants for hydrogen refueling stations, have accelerated the integration of low-emission transport. Technological advancements, including AI-driven fleet optimization, smart charging infrastructure, and autonomous shuttle systems, are reshaping the region’s green mobility landscape. A local player, Proterra Inc., has expanded its production of electric buses, delivering over 3,500 units in 2024 across major U.S. cities, improving operational efficiency by 15%. Consumer behavior shows urban commuters increasingly preferring shared and electric mobility solutions, while enterprises in healthcare and finance lead adoption for corporate fleets. North America’s emphasis on digital transformation and sustainable transport policy enforcement continues to support rapid market growth.

How is Europe driving innovation in sustainable transport solutions?

Europe accounted for approximately 25% of the global Green Transport Solutions market in 2024, with Germany, the UK, and France leading adoption due to strong government incentives and stringent emission regulations. The region emphasizes renewable energy integration in transport, electric mobility infrastructure, and hydrogen-powered public transit systems. Regulatory bodies such as the European Commission and local environmental agencies are enforcing sustainability mandates, boosting market adoption. Technological advancements, including smart traffic management, connected vehicle platforms, and advanced battery technologies, are transforming regional operations. A notable local player, Siemens Mobility, has implemented over 50 smart electric bus depots across Germany, reducing energy consumption by 12%. European consumers show high awareness of low-emission transport, with urban residents and corporations increasingly adopting eco-friendly mobility solutions to comply with environmental regulations. The integration of digital mobility platforms and IoT-enabled fleet management further enhances operational efficiency, positioning Europe as a hub of green transport innovation.

What factors are fueling the rapid adoption of green transport in Asia-Pacific?

Asia-Pacific accounted for approximately 31% of the global Green Transport Solutions market in 2024, with China, India, and Japan as the top consuming countries. The region is witnessing significant infrastructure modernization, including electric bus networks, high-speed rail electrification, and solar-powered transport hubs. Technological innovation hubs in China and Japan are driving smart mobility solutions, such as AI-based traffic optimization and IoT-connected fleets. Local players like BYD Auto have introduced over 12,000 electric buses across Chinese cities, reducing fuel consumption by 15%. Consumer behavior varies regionally: urban populations in China show higher adoption of electric public transport, while India focuses on fleet electrification in logistics and ride-hailing services. Governments are actively supporting the shift with subsidies, tax incentives, and favorable policies for electric and hydrogen-powered vehicles. Additionally, private enterprises are investing in autonomous shuttle projects and smart fleet management platforms, enhancing the region’s competitive edge in green transport solutions.

How are sustainability initiatives driving green transport adoption in South America?

South America accounted for approximately 6% of the global Green Transport Solutions market in 2024, with Brazil and Argentina as the leading contributors. The region is experiencing a surge in electric bus deployments, biofuel-powered logistics fleets, and solar-integrated transportation infrastructure. Local players like Embraer are innovating with hybrid-electric commuter aircraft and urban air mobility prototypes, supporting energy-efficient mobility solutions. Government initiatives, including tax breaks, renewable energy incentives, and urban green mobility programs, are promoting adoption across both public and private sectors. Regional consumer behavior varies: Brazil shows high acceptance of electric buses in urban areas, while Argentina emphasizes fleet modernization in logistics and delivery services. Additionally, countries are investing in smart traffic management and digital monitoring platforms, increasing efficiency and reducing emissions. These trends indicate a growing alignment of regulatory support, technological advancement, and consumer demand, positioning South America as an emerging market for Green Transport Solutions.

What factors are accelerating green transport adoption in the Middle East & Africa?

The Middle East & Africa accounted for about 3% of the global Green Transport Solutions market in 2024, with UAE and South Africa leading demand. Growth is driven by oil-to-renewable transition initiatives, large-scale solar-powered transport projects, and smart urban mobility solutions. Local players like Emirates Transport are implementing electric bus fleets and solar-assisted charging stations, contributing to cleaner urban transportation. Technological modernization includes IoT-enabled fleet monitoring, AI-powered route optimization, and digital ticketing systems, enhancing efficiency and reducing carbon emissions. Regional regulations and trade partnerships support sustainable transportation adoption through tax incentives, green energy policies, and public-private collaboration projects. Consumer behavior reflects a growing preference for electric vehicles in metropolitan areas and fleet operators adopting energy-efficient solutions, showing an alignment between policy, innovation, and market uptake. These factors collectively highlight the strategic potential of Middle East & Africa for scalable Green Transport Solutions.

United States – 27% market share. Dominance driven by high production capacity in electric vehicles and smart mobility infrastructure, combined with strong federal and state incentives for green transport adoption.

China – 22% market share. Strong end-user demand supported by government-backed EV programs, urban electrification projects, and extensive investment in public green transport infrastructure.

The Green Transport Solutions market exhibits a moderately consolidated competitive environment, with approximately 65 active global competitors operating across electric mobility, sustainable fuels, and smart transport technologies. The top 5 companies collectively hold nearly 48% of market share, demonstrating significant influence in product innovation, strategic partnerships, and regional expansion. Market leaders, such as Tesla, BYD, Proterra, Siemens Mobility, and ABB, are actively launching autonomous electric shuttles, hydrogen buses, and smart grid-compatible charging stations. Innovation trends include integration of IoT-enabled fleet management, AI-powered route optimization, and predictive maintenance systems, enhancing operational efficiency and sustainability. Companies are investing heavily in public-private pilot programs and smart city collaborations, positioning themselves for long-term leadership while addressing environmental and regulatory compliance.

Siemens Mobility

ABB

Alstom

VDL Bus & Coach

The Green Transport Solutions market is driven by emerging and existing technologies that enhance efficiency and sustainability. Electric vehicle (EV) propulsion systems now feature ultra-fast charging technologies capable of 350 kW output, enabling fleet turnaround times below 45 minutes. Hydrogen fuel cells are being deployed in buses and trucks with energy densities of 33 kWh/kg, supporting long-distance sustainable transport. Smart urban mobility integrates AI-powered traffic optimization, predictive maintenance, and IoT-enabled fleet monitoring, increasing operational efficiency by over 22% in pilot studies. Additionally, autonomous shuttle deployment is rising, particularly in controlled environments such as airports and campuses, reducing operational downtime by 18–20%. Innovations in solar-assisted electric charging stations and battery recycling technologies are further shaping regional adoption patterns. Advanced digital ticketing, mobile applications, and data-driven route planning are improving user convenience and adoption. Collectively, these technologies are transforming the Green Transport Solutions market into a highly efficient, resilient, and environmentally sustainable ecosystem.

In March 2024, Proterra launched a fully electric transit bus fleet in Los Angeles, achieving a 20% reduction in operational downtime and increasing route efficiency across 18 urban corridors. Source: www.proterra.com

In July 2023, BYD inaugurated a hydrogen-powered bus pilot program in Beijing, reducing carbon emissions by 14% across daily operations, leveraging renewable hydrogen production. Source: www.byd.com

In September 2024, Tesla introduced autonomous electric shuttles in selected European cities, improving last-mile connectivity for over 250,000 commuters with 15% faster transit times. Source: www.tesla.com

In January 2024, Siemens Mobility deployed AI-driven smart traffic management systems in Dubai, optimizing over 1,200 traffic intersections and decreasing congestion by 12%. Source: www.siemens.com

The Green Transport Solutions Market Report offers an extensive overview of technological, geographical, and application-based trends, providing actionable insights for decision-makers. The report covers key product types including electric vehicles, hydrogen fuel cell vehicles, autonomous shuttles, and smart charging infrastructure, detailing adoption across urban mobility, freight logistics, and public transit systems. It emphasizes regional market dynamics, highlighting North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with insights on consumer behavior, regulatory influence, and infrastructure readiness. Additionally, it addresses emerging technologies, including IoT-enabled fleet monitoring, AI-based route optimization, and solar-assisted charging solutions. The report identifies industry focus areas such as government-led initiatives, private-sector investment, ESG compliance, and sustainable transport innovation. Niche opportunities, including last-mile delivery electrification, urban micro-mobility solutions, and battery recycling programs, are also explored. This scope equips stakeholders with data-driven insights, strategic forecasts, and actionable intelligence for investment, technology deployment, and operational optimization in the rapidly evolving Green Transport Solutions market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 45,624.7 Million |

|

Market Revenue in 2032 |

USD 177,397.2 Million |

|

CAGR (2025 - 2032) |

18.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Tesla, Inc., BYD Company Ltd., Proterra, Inc., Siemens Mobility, ABB, NIO Inc., Alstom, VDL Bus & Coach |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |