Reports

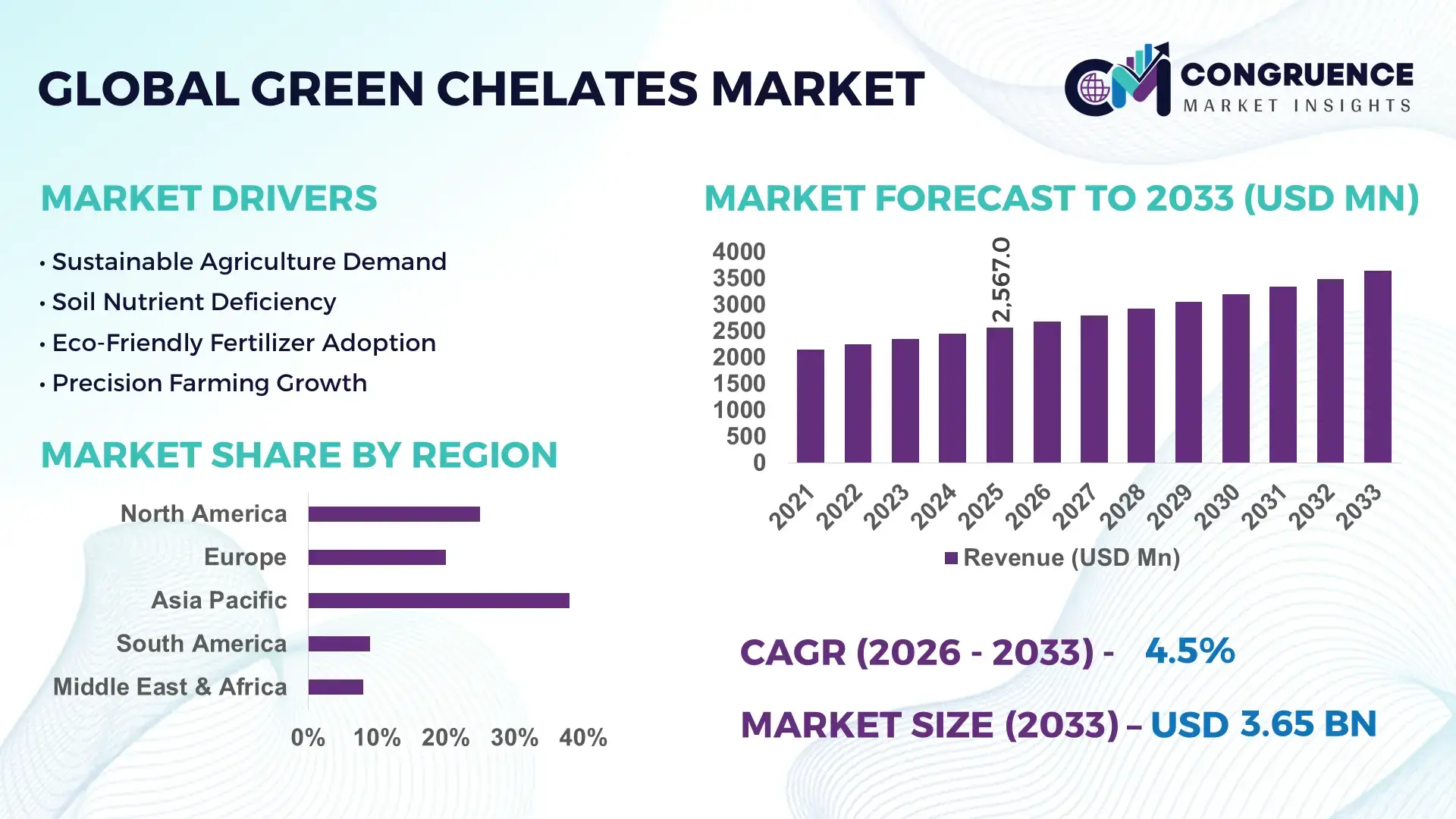

The Global Green Chelates Market was valued at USD 2567 Million in 2025 and is anticipated to reach a value of USD 3650.53 Million by 2033 expanding at a CAGR of 4.5% between 2026 and 2033. Growth is supported by rising adoption of sustainable micronutrient formulations across agriculture, pharmaceuticals, and specialty chemicals.

China represents the most prominent country-level presence in the Green Chelates market. In 2024, China accounted for over 38% of Asia-Pacific green chelate production capacity, supported by more than 120 large-scale specialty chemical manufacturing facilities. Annual investments exceeding USD 420 million have been directed toward biodegradable chelating agents, particularly EDTA alternatives and amino acid-based chelates. Green chelates are widely applied in micronutrient fertilizers, representing nearly 55% of domestic consumption, followed by animal nutrition and water treatment. Technological advancements include continuous chelation processing, bio-based ligand synthesis, and process automation, improving output efficiency by approximately 18% year-over-year.

Market Size & Growth: USD 2567 Million in 2025, projected to reach USD 3650.53 Million by 2033, growing at a CAGR of 4.5%, driven by sustainability-led reformulation across agrochemicals and nutrition products

Top Growth Drivers: Sustainable fertilizer adoption 46%, micronutrient bioavailability improvement 32%, regulatory substitution of conventional chelates 27%

Short-Term Forecast: By 2028, production costs expected to decline by 14% through process optimization and bio-based raw material integration

Emerging Technologies: Amino acid chelation chemistry, biodegradable ligand engineering, low-temperature continuous chelation systems

Regional Leaders: Asia-Pacific USD 1420 Million by 2033 with agriculture-led adoption; Europe USD 980 Million by 2033 driven by regulatory compliance; North America USD 870 Million by 2033 supported by specialty nutrition demand

Consumer/End-User Trends: Increasing use among precision agriculture operators, feed formulators, and water treatment facilities emphasizing eco-certified inputs

Pilot or Case Example: A 2025 large-scale agricultural pilot in Southeast Asia reported 21% micronutrient uptake improvement using bio-based chelates

Competitive Landscape: BASF holds approximately 18% share, followed by Nouryon, Akzo Nobel, Dow, and Van Iperen

Regulatory & ESG Impact: Stricter discharge norms and fertilizer sustainability mandates accelerating replacement of synthetic chelating agents

Investment & Funding Patterns: Over USD 1.1 billion invested globally since 2023, focused on capacity expansion and green chemistry R&D

Innovation & Future Outlook: Advancements in plant-specific chelation, circular feedstock use, and smart nutrient delivery systems shaping long-term growth

The Green Chelates market serves agriculture (approximately 52% of demand), animal nutrition (21%), pharmaceuticals and nutraceuticals (15%), and industrial water treatment (12%). Recent innovations include amino acid-based chelates with enhanced solubility, lignin-derived ligands, and low-residue formulations that improve nutrient efficiency by up to 25%. Regulatory pressure to limit heavy metal discharge and promote biodegradable inputs is accelerating adoption, particularly in Europe and Asia-Pacific. Consumption growth remains strongest in high-intensity farming regions, while emerging trends include precision micronutrient delivery, integration with controlled-release fertilizers, and increased use in organic-certified production systems, positioning the market for steady, sustainability-driven expansion.

The Green Chelates Market holds growing strategic relevance as industries transition toward environmentally compliant input materials while maintaining performance efficiency. Green chelates are increasingly embedded in agricultural micronutrients, animal nutrition, pharmaceuticals, and water treatment due to their higher biodegradability and lower ecological persistence. For instance, amino acid–based chelation technology delivers approximately 28% higher micronutrient uptake efficiency compared to conventional EDTA-based standards, enabling optimized resource utilization across end-use sectors.

From a regional perspective, Asia-Pacific dominates in volume, driven by large-scale agricultural consumption and fertilizer manufacturing, while Europe leads in adoption with nearly 62% of enterprises integrating biodegradable chelating agents into regulated formulations. Strategic alignment with sustainability mandates is accelerating enterprise-level adoption, particularly where discharge limits and soil health indicators are tightly monitored.

Short-term pathways emphasize digital and process innovation. By 2028, AI-enabled formulation optimization and process automation are expected to improve production efficiency by 17%, reducing waste and batch variability. Compliance and ESG considerations are now embedded into corporate strategies, with firms committing to 30% reduction in non-biodegradable chelating residues by 2030 through raw material substitution and closed-loop processing.

A measurable micro-scenario highlights this shift: In 2025, China achieved a 19% reduction in chelate-related effluent load through continuous chelation and bio-ligand integration initiatives across specialty chemical facilities. Looking ahead, the Green Chelates Market is positioned as a pillar of industrial resilience, regulatory compliance, and sustainable growth, supporting long-term value creation across agriculture, nutrition, and environmental management ecosystems.

The expansion of sustainable agriculture is a primary driver for the Green Chelates Market. Over 40% of intensively cultivated farmland globally now relies on micronutrient supplementation to address soil degradation and yield variability. Green chelates enhance nutrient absorption efficiency by up to 25%, reducing application frequency and input losses. Their compatibility with organic and eco-certified farming standards further accelerates adoption, particularly in high-value crop segments such as fruits, vegetables, and horticulture. Governments and agricultural cooperatives are increasingly promoting low-toxicity inputs to protect soil microbiomes and groundwater quality. As a result, fertilizer formulators are reformulating portfolios to include biodegradable chelates, directly increasing demand volumes and long-term procurement contracts across agricultural value chains.

Despite their advantages, green chelates face adoption restraints due to higher formulation and transition costs compared to conventional chelating agents. Bio-based ligands and amino acid derivatives can cost 18–25% more than synthetic alternatives, impacting price-sensitive markets. Additionally, manufacturers often require process modifications, new quality controls, and regulatory revalidation when switching formulations. Smaller producers, particularly in emerging economies, face capital constraints that limit rapid conversion. Variability in raw material availability for bio-based inputs also affects supply stability. These factors collectively slow penetration in cost-driven segments, especially where regulatory enforcement remains uneven or sustainability incentives are limited.

Regulatory reform presents significant opportunities for the Green Chelates Market as authorities tighten restrictions on persistent and toxic chemical inputs. More than 60 countries have introduced or updated fertilizer and industrial discharge guidelines favoring biodegradable components. This creates opportunities for suppliers to partner with formulators in agriculture, feed, and water treatment to redesign compliant product lines. Additionally, demand is emerging for customized chelation solutions tailored to specific crops, water chemistries, or nutrient profiles. Technological advances in ligand engineering allow performance differentiation, opening premium segments. These factors enable suppliers to expand value-added offerings while strengthening long-term client relationships through compliance-driven demand.

Scalability remains a key challenge for the Green Chelates Market due to dependence on specialized bio-based raw materials and complex synthesis processes. Large-scale production requires consistent quality inputs, yet agricultural or biomass-derived feedstocks can fluctuate by season and region. Logistics complexity increases as manufacturers attempt to localize supply chains to meet sustainability targets. Furthermore, maintaining uniform chelation performance across high-volume batches demands advanced process control and skilled technical oversight. These challenges increase operational risk and constrain rapid capacity expansion, particularly for new entrants attempting to compete with established specialty chemical producers.

Expansion of Modular and Prefabricated Production Facilities: The adoption of modular and prefabricated construction is reshaping demand dynamics in the Green Chelates Market, particularly for fertilizer blending units and specialty chemical plants. Approximately 55% of newly commissioned green chelate facilities reported cost efficiency gains through modular construction approaches. Pre-engineered reactors and pre-calibrated dosing systems reduce installation time by 30–35%, supporting faster capacity scaling. Demand for precision-compatible green chelate formulations has increased by 22% in regions prioritizing rapid deployment, notably Europe and North America.

Shift Toward Amino Acid–Based and Bio-Ligand Chelates: Manufacturers are increasingly transitioning from synthetic chelating agents to amino acid and bio-ligand alternatives. These formulations demonstrate 20–28% higher micronutrient uptake efficiency in agricultural applications and reduce residual metal accumulation by up to 34%. Adoption has accelerated in regulated markets, with nearly 48% of newly launched micronutrient products in 2025 incorporating biodegradable chelates, reflecting a clear shift toward environmentally optimized performance inputs.

Integration of Digital Process Control and Automation: Digitalization is becoming a defining trend across green chelate manufacturing. Automated chelation reactors and AI-assisted process controls have improved batch consistency by 18% and reduced material waste by 15%. Around 42% of mid-to-large-scale producers have implemented real-time monitoring systems to optimize ligand-metal binding efficiency. This trend supports tighter quality tolerances required by pharmaceutical-grade and specialty nutrition applications.

Rising Adoption in Precision Agriculture and Controlled-Environment Farming: The use of green chelates is expanding rapidly in precision agriculture, hydroponics, and greenhouse farming systems. Controlled-environment growers report 24% lower micronutrient dosage requirements when using advanced green chelate formulations, alongside yield uniformity improvements of 17%. Adoption rates in high-value crop cultivation have increased by 31% over the last two years, positioning green chelates as a critical input for resource-efficient, technology-driven farming models.

The Green Chelates Market is segmented by type, application, and end-user, reflecting differences in chemical composition, performance requirements, regulatory exposure, and sustainability alignment. By type, segmentation is driven by ligand chemistry and biodegradability, which directly influence nutrient stability and absorption efficiency. Application-based segmentation highlights agriculture as the dominant use case, supported by soil health management and micronutrient optimization, while animal nutrition, water treatment, and pharmaceutical uses add diversification. End-user segmentation further clarifies demand concentration among fertilizer producers, commercial farms, and feed manufacturers, alongside emerging uptake from regulated industrial users. These segmentation layers collectively illustrate how volume-driven demand and innovation-led adoption coexist within the Green Chelates Market, shaping strategic investment and product development priorities.

The Green Chelates Market by type includes amino acid chelates, organic acid chelates, lignosulfonate-based chelates, and other bio-based or hybrid chelating agents. Amino acid chelates represent the leading type, accounting for approximately 44% of total adoption, due to their high bioavailability, low environmental persistence, and compatibility with organic-certified formulations. Organic acid chelates hold around 27% adoption, supported by balanced cost structures and stability across multiple soil and water conditions. Bio-ligand and next-generation biodegradable chelates are the fastest-growing type, expanding at an estimated 6.8% annually, driven by regulatory substitution of persistent chelators and increasing demand for fully biodegradable inputs. Lignosulfonate-based and other niche chelates together contribute a combined 29% share, serving cost-sensitive markets and region-specific agronomic practices.

Application-based segmentation shows agriculture as the primary application area, accounting for approximately 52% of total usage, reflecting widespread deployment in micronutrient fertilizers to address soil depletion and yield variability. Animal nutrition follows with about 21% adoption, where green chelates improve mineral absorption efficiency and reduce nutrient excretion losses. Water treatment and pharmaceutical applications together contribute nearly 18%, driven by strict toxicity and discharge standards. Controlled-environment agriculture, including hydroponics and greenhouse farming, is the fastest-growing application segment, expanding at an estimated 7.2% annually due to precision dosing requirements and resource efficiency targets. Other applications, including specialty industrial uses, account for the remaining 9% of demand.

From an end-user perspective, large-scale agricultural producers and fertilizer manufacturers form the leading segment, representing approximately 47% of total market usage. These users prioritize input efficiency, regulatory compliance, and consistent agronomic performance. Feed manufacturers account for around 24% adoption, using green chelates to enhance mineral bioavailability and reduce environmental loading. Industrial water treatment operators and pharmaceutical manufacturers together contribute about 19%, driven by compliance with stringent effluent and purity standards. Organic and specialty crop producers represent the fastest-growing end-user group, with adoption increasing at an estimated 7.5% annually, supported by certification requirements and premium crop economics. Other end-users collectively account for the remaining 10%, including specialty chemical processors and research institutions.

Asia-Pacific accounted for the largest market share at 38% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2026 and 2033.

Asia-Pacific benefits from high agricultural input consumption, accounting for over 45% of global micronutrient fertilizer usage, with green chelates increasingly replacing synthetic agents. Europe’s accelerated growth trajectory is supported by stringent environmental compliance frameworks, where more than 60% of fertilizer and feed formulations now require biodegradable inputs. North America holds approximately 27% market share, driven by precision agriculture and regulated water treatment adoption. South America and the Middle East & Africa together represent nearly 14%, supported by expanding commercial farming, export-oriented crop production, and sustainability-aligned trade policies. Regional differences in regulation, crop intensity, industrial usage, and sustainability mandates create varied adoption speeds and technology preferences across the global Green Chelates Market.

How is sustainability-driven innovation reshaping input adoption patterns?

North America accounts for approximately 27% of the global Green Chelates Market, supported by advanced agricultural practices and regulated industrial usage. Demand is primarily driven by precision agriculture, animal nutrition, and water treatment industries, where nutrient efficiency and low-toxicity inputs are prioritized. Government-supported soil health initiatives and water discharge regulations have accelerated adoption of biodegradable chelating agents, with over 48% of large-scale farms integrating eco-certified micronutrient formulations. Technological advancements include digital nutrient management platforms and automated fertilizer blending, improving application efficiency by nearly 18%. Local players are investing in amino acid chelate expansion to meet organic certification standards. Consumer behavior reflects higher enterprise-level adoption among commercial farms and regulated industrial operators seeking compliance-ready solutions.

Why are regulatory frameworks accelerating formulation transitions?

Europe represents around 25% of global market share, with Germany, France, and the UK collectively contributing more than 60% of regional demand. Regulatory bodies promoting sustainable agriculture and industrial emissions control have driven rapid substitution of persistent chelating agents. Over 62% of fertilizer and feed producers in the region have transitioned to biodegradable chelates to align with environmental compliance requirements. Adoption of emerging technologies such as bio-ligand synthesis and low-residue formulations is expanding, supported by circular economy initiatives. Local specialty chemical producers are focusing on certified green chelate portfolios to serve organic farming and regulated feed markets. Consumer behavior is strongly compliance-driven, with buyers prioritizing traceability, biodegradability, and regulatory alignment.

What factors sustain volume leadership and manufacturing scale?

Asia-Pacific ranks as the largest regional market by volume, contributing approximately 38% of global consumption. China, India, and Japan are the top consuming countries, collectively accounting for over 70% of regional usage. High crop intensity, expanding fertilizer production capacity, and growing awareness of soil micronutrient depletion support sustained demand. Manufacturing trends emphasize large-scale continuous chelation processes and cost-optimized bio-based inputs. Regional innovation hubs are increasingly focusing on amino acid and hybrid chelate technologies to improve efficiency under diverse soil conditions. Local producers are expanding capacity to meet domestic agricultural demand. Consumer behavior reflects high-volume adoption driven by yield optimization and input cost efficiency.

How is export-oriented agriculture shaping demand patterns?

South America accounts for approximately 8% of the global Green Chelates Market, with Brazil and Argentina leading regional consumption. Demand is closely tied to large-scale commercial farming and export-oriented crop production, particularly soybeans, corn, and horticulture. Infrastructure investments in agricultural logistics and irrigation have improved access to advanced micronutrient inputs. Government incentives supporting sustainable farming practices and trade alignment with eco-certified markets have increased adoption of biodegradable chelates. Regional players are integrating green chelates into fertilizer blends to meet export quality standards. Consumer behavior is influenced by crop productivity targets and compliance with international residue requirements.

Why are efficiency and resource optimization gaining importance?

The Middle East & Africa region contributes around 6% of global demand, supported by growing adoption in agriculture, water treatment, and industrial processing. Key growth countries include the UAE and South Africa, where controlled-environment farming and water reuse systems are expanding. Technological modernization efforts emphasize efficient nutrient delivery and reduced metal discharge in water-scarce environments. Trade partnerships and sustainability-focused agricultural programs are encouraging adoption of low-toxicity chelating agents. Regional producers are focusing on import substitution and formulation adaptation for arid conditions. Consumer behavior prioritizes durability, efficiency, and compliance with evolving environmental standards.

China – Market share: 21%; Dominance driven by large-scale agricultural input consumption, extensive specialty chemical production capacity, and widespread adoption of micronutrient fertilizers

United States – Market share: 16%; Leadership supported by advanced precision agriculture practices, strong regulatory compliance requirements, and high adoption across agriculture and water treatment sectors

The Green Chelates market exhibits a moderately fragmented competitive structure, characterized by a mix of large multinational specialty chemical companies and a broad base of regional producers. More than 45 active manufacturers are commercially engaged in producing biodegradable and bio-based chelating agents for agriculture, animal nutrition, water treatment, and specialty applications. The top five companies collectively account for approximately 52% of total global supply, reflecting growing consolidation around technology capability, certification readiness, and distribution reach, while leaving room for innovation-driven mid-sized players.

Competition is increasingly shaped by product differentiation rather than price, with over 60% of leading players investing in amino acid chelates, lignin-derived ligands, and next-generation bio-ligand systems. Strategic initiatives include long-term supply agreements with fertilizer formulators, joint development partnerships with agritech firms, and targeted capacity expansions near high-consumption agricultural regions. Between 2023 and 2025, more than 30 new green chelate formulations were commercially launched, many optimized for precision agriculture and organic-certified applications. Digital process optimization and low-residue performance benchmarks are emerging as competitive differentiators, with manufacturers reporting 15–20% improvements in batch consistency after automation upgrades. Overall, competitive intensity is expected to remain high as regulatory alignment, sustainability credentials, and application-specific performance increasingly determine supplier selection.

BASF SE

Nouryon

Dow

Van Iperen International

Akzo Nobel

Syngenta Group

Haifa Group

Aries Agro Limited

Nufarm

ATP Nutrition

Technological advancement is a core driver shaping the evolution of the Green Chelates Market, with innovation focused on improving biodegradability, metal-binding efficiency, and application precision. One of the most impactful developments is the shift toward amino acid–based and bio-ligand chelation technologies, which deliver up to 28% higher micronutrient uptake efficiency compared to conventional synthetic chelators. These technologies also reduce residual metal accumulation in soil and water systems by 30–35%, aligning with tightening environmental compliance requirements. Manufacturing technologies are also advancing rapidly. Continuous chelation reactors and low-temperature synthesis processes have improved production yields by approximately 18%, while reducing energy consumption per batch by nearly 22%. Automation and real-time process control systems are increasingly deployed, with more than 40% of mid-to-large-scale producers integrating sensor-driven monitoring to maintain consistent ligand-to-metal ratios and minimize formulation variability.

In application technology, integration with precision agriculture platforms is gaining momentum. Smart nutrient delivery systems using chelated micronutrients enable 20–25% reductions in application volumes while maintaining crop performance. In animal nutrition, encapsulated green chelates are being adopted to improve mineral bioavailability, reducing mineral excretion rates by up to 26%.

Emerging technologies include lignin-derived chelating agents, enzymatic ligand synthesis, and hybrid chelate formulations designed for controlled-release behavior. Digital formulation modeling and AI-assisted chelation optimization are expected to further enhance process efficiency and customization, positioning technology as a critical competitive lever in the Green Chelates Market.

• In January 2025, Nouryon received International Sustainability and Carbon Certification (ISCC PLUS) at its Herkenbosch facility, enabling production of biodegradable chelates with up to 100% renewable carbon index using bio-based and bio-circular feedstocks, enhancing its sustainable product portfolio.

• In August 2024, CHS Inc. launched Trivar EZ, a granular chelated micronutrient fertilizer incorporating its patented Levesol chelating agent, designed to improve crop nutrient accessibility and support higher yields in major agricultural regions. (Knowledge Sourcing)

• In July 2025, Yara International launched its Digital Agronomy Platform featuring AI-based micronutrient chelate dose recommendations, connecting field sensors with fertigation systems to reduce nutrient waste and increase consistency in crop performance.

• In July 2025, BASF launched Trilon® G, a bio-based GLDA chelating agent with high renewable carbon content that maintains strong metal complexing while reducing environmental persistence, expanding its sustainable chelate offerings for agricultural and industrial use.

The Green Chelates Market Report provides a comprehensive examination of the global landscape of biodegradable and bio-based chelating agents across multiple segments, geographies, applications, and technologies. The report covers detailed segmentation by product type, including amino acid chelates, organic acid chelates, lignosulfonate-based chelates, and next-generation bio-ligand systems, offering insights into performance attributes and end-use suitability. It analyzes application sectors such as agriculture (soil, foliar, fertigation), animal nutrition, water treatment, and specialty industrial applications, highlighting functional roles and performance metrics like micronutrient uptake efficiency and soil compatibility.

Geographically, the report examines key regions: North America, Europe, Asia-Pacific, South America, and Middle East & Africa, providing regional demand patterns, regulatory environments, and adoption trends. It also assesses technology trends, such as continuous chelation synthesis, low-temperature processes, digital nutrient management tools, and AI-assisted formulation optimization that influence production efficiency and product consistency.

Additionally, the report explores industry focus areas including sustainability drivers, compliance with environmental standards, supply chain and distribution channels, and strategic leadership profiles. Emerging or niche segments—such as controlled-environment agriculture, precision nutrient delivery platforms, and integrated feed-grade chelates—are also addressed, providing actionable insights for decision-makers evaluating growth opportunities and competitive strategies. By integrating factual data across segments and regions, the report equips industry professionals with a holistic view of market breadth, technical innovation fronts, and adoption dynamics shaping the future of green chelating solutions.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

BASF SE, Nouryon, Dow, Van Iperen International, Akzo Nobel, Syngenta Group, Haifa Group, Aries Agro Limited, Nufarm, ATP Nutrition |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |