Reports

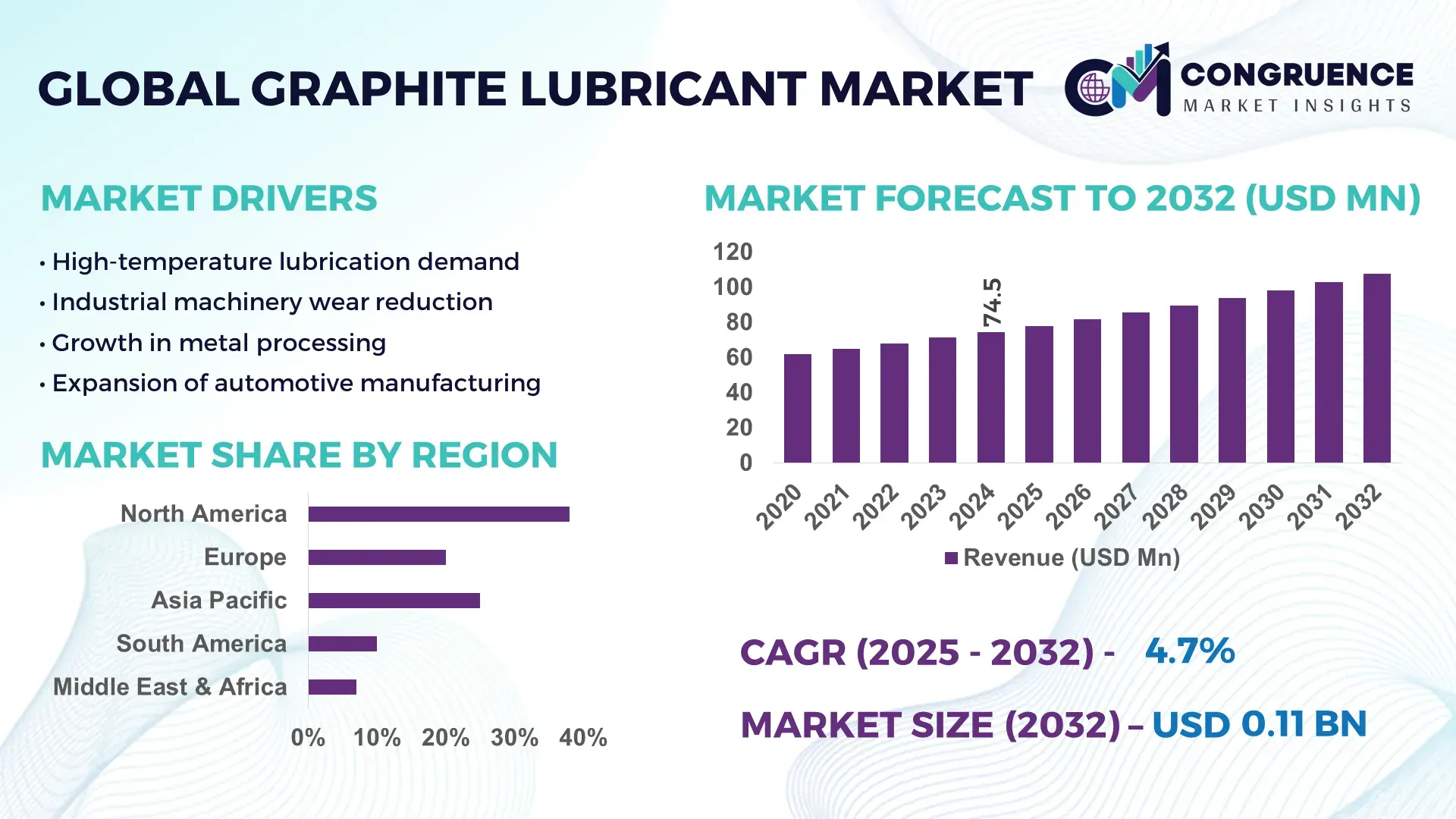

The Global Graphite Lubricant Market was valued at USD 74.54 Million in 2024 and is anticipated to reach a value of USD 107.64 Million by 2032 expanding at a CAGR of 4.7% between 2025 and 2032. This growth is driven by increasing demand for high-temperature, dry, and maintenance-reducing lubrication solutions across industrial manufacturing, automotive, and heavy engineering applications.

China represents the dominant country in the global graphite lubricant landscape, supported by its extensive graphite production base and vertically integrated processing ecosystem. The country accounts for over 65% of global natural graphite output, with annual production exceeding 800,000 metric tons, ensuring stable raw material availability for lubricant formulations. Significant capital investments exceeding USD 1.5 billion over recent years have been directed toward advanced graphite purification, micronization, and surface-treatment technologies. Graphite lubricants in China are widely deployed across steelmaking, cement kilns, railways, automotive components, and power generation equipment. Technological advancements such as high-purity synthetic graphite blends, nano-graphite dispersions, and environmentally compliant water-based formulations have accelerated domestic adoption, with industrial users accounting for more than 70% of graphite lubricant consumption.

Market Size & Growth: USD 74.54 Million in 2024, projected to reach USD 107.64 Million by 2032 at a CAGR of 4.7%, supported by rising demand for high-load, high-temperature lubrication.

Top Growth Drivers: Equipment lifespan improvement by ~25%, maintenance cost reduction by ~18%, and industrial uptime enhancement by ~20%.

Short-Term Forecast: By 2028, graphite lubricant adoption is expected to deliver average friction reduction of ~15% in heavy-duty machinery.

Emerging Technologies: Nano-graphite dispersions, water-based graphite lubricants, and hybrid synthetic-graphite formulations.

Regional Leaders: Asia-Pacific projected at ~USD 46 Million by 2032 with strong industrial adoption, Europe ~USD 28 Million driven by regulatory-compliant formulations, North America ~USD 22 Million supported by automotive and aerospace usage.

Consumer/End-User Trends: Industrial manufacturing and automotive sectors together account for over 60% of total consumption, favoring dry and semi-dry lubrication systems.

Pilot or Case Example: In 2024, a steel plant deployment reduced unplanned downtime by ~22% using high-purity graphite lubricants.

Competitive Landscape: Market leader holds approximately 18% share, followed by 3–5 established global lubricant and specialty graphite suppliers.

Regulatory & ESG Impact: Increased adoption of low-VOC and solvent-free graphite lubricants aligned with industrial emission standards.

Investment & Funding Patterns: Recent cumulative investments exceed USD 900 Million, focused on processing capacity expansion and formulation R&D.

Innovation & Future Outlook: Integration of graphite lubricants with automated lubrication systems and smart maintenance platforms is shaping future demand.

The graphite lubricant market serves critical roles across metallurgy, automotive manufacturing, power generation, mining, and construction equipment, with industrial applications contributing over 55% of total demand. Ongoing innovations include high-purity synthetic graphite lubricants, nano-enhanced formulations for improved wear resistance, and environmentally compliant water-based products. Regulatory pressure to reduce volatile emissions, combined with energy-efficiency mandates, is accelerating adoption. Asia-Pacific leads consumption due to large-scale manufacturing activity, while Europe emphasizes sustainable formulations. Future growth is expected to be supported by increased automation, demand for maintenance-free machinery, and expanding use in electric vehicle manufacturing and renewable energy infrastructure.

The Graphite Lubricant Market holds strategic relevance as industries increasingly prioritize equipment reliability, operational continuity, and regulatory compliance under high-load and high-temperature operating conditions. Graphite-based lubricants are integral to steelmaking, automotive components, railways, power generation, and cement production, where operating temperatures frequently exceed 400°C and conventional oil-based lubricants underperform. From a competitive strategy perspective, advanced graphite lubricant formulations support maintenance optimization, with plant operators reporting up to 20% longer component service intervals and 15–25% reductions in unplanned downtime. Nano-graphite dispersion technology delivers approximately 18% improvement in wear resistance compared to conventional flake-graphite lubricants, enabling higher asset utilization in heavy-duty applications. Asia-Pacific dominates in volume due to extensive industrial manufacturing capacity, while Europe leads in adoption with nearly 58% of large industrial enterprises integrating dry or water-based graphite lubricants into standardized maintenance protocols. By 2027, AI-enabled predictive maintenance platforms integrated with graphite lubricant systems are expected to improve equipment availability by around 22% through optimized lubrication cycles and condition monitoring. From an ESG standpoint, firms are committing to sustainability improvements such as 30% reduction in lubricant-related volatile emissions and 25% increase in recyclable or water-based formulations by 2030. In 2024, Germany-based industrial manufacturers achieved a 17% reduction in maintenance-related energy losses through deployment of high-purity graphite lubricants combined with digital monitoring initiatives. Looking ahead, the Graphite Lubricant Market is positioned as a pillar of industrial resilience, regulatory alignment, and sustainable growth, supporting long-term productivity across energy-intensive sectors.

Rising demand for high-temperature and heavy-load industrial operations is a primary driver of the Graphite Lubricant Market, as graphite remains stable and lubricious at temperatures exceeding 500°C where conventional lubricants fail. Steel plants, for example, operate continuous casting and rolling equipment under extreme thermal stress, creating strong reliance on graphite-based solutions. Industrial users report friction reduction of 15–20% and component life extension of up to 30% when graphite lubricants are applied in kilns, furnaces, and conveyor systems. Automotive manufacturing also contributes, with graphite lubricants increasingly specified for metal forming, die casting, and brake components. The driver is reinforced by cost-control strategies, as improved lubrication directly lowers maintenance frequency, spare-part consumption, and energy losses across asset-intensive facilities.

Raw material price volatility represents a notable restraint for the Graphite Lubricant Market, particularly due to fluctuations in natural and synthetic graphite supply. Concentration of graphite mining and processing in a limited number of countries exposes lubricant producers to supply disruptions and cost instability. Purification and micronization processes are energy-intensive, contributing to higher production costs and limiting price flexibility for end users. In addition, formulation constraints exist where graphite lubricants are incompatible with certain precision or low-load applications, restricting their universal substitution for oil-based products. Industrial buyers also face challenges in standardizing graphite lubricant usage across diverse equipment types, which can slow adoption despite technical advantages.

Sustainable manufacturing and industrial automation trends present significant opportunities for the Graphite Lubricant Market. As industries pursue lower environmental impact, demand is increasing for water-based and low-emission graphite lubricants that comply with stricter occupational safety and environmental standards. Automated lubrication systems integrated into smart factories create opportunities for precisely metered graphite lubricant application, reducing waste by up to 20% and improving consistency. Growth in renewable energy infrastructure, including wind turbines and thermal power components, further expands application scope. Emerging economies investing in heavy industrial capacity also represent untapped demand, particularly where equipment durability and low maintenance are strategic priorities.

Regulatory complexity and operational integration challenges continue to impact the Graphite Lubricant Market, especially for multinational manufacturers and end users. Compliance with varying chemical safety, environmental, and workplace exposure regulations across regions increases testing, certification, and documentation requirements. Operationally, integrating graphite lubricants into existing maintenance regimes requires equipment-specific adaptation, staff training, and process validation. In automated or high-precision environments, improper application can lead to contamination or inconsistent performance, raising operational risk. These challenges increase implementation timelines and require coordinated technical support, which can constrain faster adoption despite the long-term performance benefits of graphite lubricants.

Rise in Modular and Prefabricated Construction Driving Precision Equipment Lubrication Demand

The growing adoption of modular and prefabricated construction is reshaping demand patterns in the Graphite Lubricant market, particularly for high-precision and automated machinery. Around 55% of new modular construction projects have reported measurable cost benefits through reduced on-site labor and faster project execution. Pre-bent and pre-cut structural components are increasingly manufactured off-site using CNC machines, robotic presses, and automated conveyors that operate under high load and repetitive cycles. Graphite lubricants are favored in these systems due to their ability to reduce friction by nearly 18% and extend component service life by approximately 25%, supporting higher machine uptime in Europe and North America.

Shift Toward High-Temperature and Dry Lubrication in Heavy Industry Operations

Industrial users are increasingly shifting toward dry and semi-dry graphite lubrication systems to address high-temperature operating environments exceeding 400°C. More than 60% of steel, cement, and foundry operators now deploy graphite lubricants in furnace doors, molds, chains, and kiln components. These applications report wear reduction levels of 20–30% compared to conventional oil-based lubricants. The trend is particularly visible in Asia-Pacific, where large-scale continuous operations prioritize thermal stability and reduced lubricant degradation to maintain consistent production cycles.

Integration of Graphite Lubricants with Automated and Smart Maintenance Systems

Automation in industrial maintenance is accelerating the adoption of graphite lubricants compatible with centralized and automated lubrication systems. Approximately 42% of large manufacturing plants have implemented automated lubrication or condition-monitoring solutions, enabling precise graphite lubricant dosing. This integration has resulted in lubricant consumption optimization of nearly 15% and unplanned equipment downtime reduction of around 22%. Smart factories increasingly prefer consistent, non-drip graphite formulations that perform reliably under variable load and speed conditions.

Growing Preference for Environmentally Compliant and Water-Based Formulations

Environmental and workplace safety considerations are driving a measurable shift toward water-based and low-emission graphite lubricant formulations. Nearly 35% of industrial buyers now specify solvent-free or water-based graphite lubricants in procurement standards. These products support reductions of up to 30% in volatile emissions and improve handling safety without compromising lubrication performance. Adoption is strongest in Europe, where over 50% of enterprises using graphite lubricants have transitioned part of their operations to environmentally compliant formulations aligned with internal ESG targets.

The Graphite Lubricant market is segmented based on type, application, and end-user, reflecting diverse performance requirements across industrial environments. Product segmentation highlights variations in physical form and formulation, each optimized for temperature tolerance, load-bearing capacity, and application method. Application-based segmentation underscores strong concentration in heavy-duty and high-friction industrial processes, while end-user segmentation reveals dependence on asset-intensive industries with continuous operations. Adoption patterns show that industrial manufacturing and process industries account for the majority of graphite lubricant usage, supported by increasing automation and stricter maintenance standards. Regional industrialization levels, equipment age profiles, and compliance norms further influence how different segments contribute to overall demand, making segmentation analysis critical for strategic planning and product positioning.

Graphite Lubricants are primarily categorized into powdered graphite lubricants, colloidal graphite lubricants, and graphite-based grease and dispersions. Powdered graphite lubricants currently account for approximately 46% of total adoption due to their simplicity, cost efficiency, and suitability for extremely high-temperature applications such as foundries, kilns, and metal forging. Colloidal graphite lubricants represent around 32% of adoption, offering better adhesion and uniform surface coverage, making them preferred in automotive components, chains, and industrial bearings. However, graphite-based greases and advanced dispersions are the fastest-growing type, expanding at an estimated CAGR of 6.1%, driven by demand for cleaner application, compatibility with automated lubrication systems, and improved load-carrying performance. These advanced formulations are increasingly specified in precision manufacturing environments. Other niche types, including hybrid graphite-synthetic blends and specialty coatings, collectively contribute nearly 22% of the market, serving aerospace, rail, and specialty engineering needs.

By application, metal processing and forming operations lead the Graphite Lubricant market, accounting for approximately 38% of total usage due to continuous exposure to high friction and thermal stress. Automotive manufacturing follows with nearly 26% adoption, supported by applications in die casting, brake components, and metal stamping. However, power generation and energy infrastructure applications are the fastest-growing, expanding at an estimated CAGR of 5.8%, driven by rising installation of thermal power units, wind turbines, and heavy rotating equipment requiring dry and high-load lubrication. Construction machinery and mining equipment applications together contribute about 20%, where graphite lubricants help reduce downtime in harsh operating environments. Remaining applications, including railways, aerospace components, and specialty industrial equipment, collectively represent around 16% of demand.

Industrial manufacturing companies represent the leading end-user segment, accounting for approximately 44% of total graphite lubricant consumption due to their reliance on continuous, high-load machinery. Steel, cement, and chemical processing operators are the largest adopters within this group. Automotive OEMs and component suppliers follow with about 29% adoption, benefiting from graphite lubricants’ ability to improve tooling life and consistency in forming operations. The fastest-growing end-user segment is the energy and utilities sector, expanding at an estimated CAGR of 6.0%, fueled by increased investment in power generation assets and renewable infrastructure requiring low-maintenance lubrication solutions. Mining and construction companies, along with transportation and rail operators, collectively contribute nearly 27% of demand, with adoption rates exceeding 60% among large-scale mining operations.

Asia-Pacific accounted for the largest market share at 46.8% in 2024 however, Europe is expected to register the fastest growth, expanding at a CAGR of 5.9% between 2025 and 2032.

Asia-Pacific dominance is supported by high industrial output, with over 62% of global steel and 58% of cement production concentrated in this region, driving sustained demand for high-temperature graphite lubricants. Europe’s accelerated growth outlook is linked to rapid adoption of environmentally compliant and water-based graphite lubricants, with more than 54% of industrial enterprises transitioning away from solvent-based products. North America holds approximately 24.6% market share, driven by advanced manufacturing and automotive production exceeding 15 million vehicles annually. South America and the Middle East & Africa collectively account for nearly 28.6% of global consumption, supported by expanding mining, energy, and infrastructure investments exceeding USD 300 billion in combined announced projects.

How is advanced manufacturing accelerating adoption of high-performance lubrication solutions?

North America accounts for nearly 24.6% of the Graphite Lubricant Market, supported by strong demand from automotive manufacturing, aerospace components, steel processing, and power generation. The region operates more than 5,000 large-scale manufacturing facilities that rely on continuous, high-load equipment, creating consistent demand for dry and semi-dry graphite lubricants. Regulatory emphasis on workplace safety and reduced chemical emissions has increased adoption of low-VOC and water-based graphite formulations, now specified by over 48% of large enterprises. Digital transformation is also shaping the market, with around 41% of plants integrating automated lubrication and condition-monitoring systems. A leading local lubricant manufacturer has expanded graphite-based product lines tailored for robotic assembly and high-temperature bearings. Regional consumer behavior shows higher enterprise adoption in automotive, aerospace, and energy sectors where uptime and compliance are critical.

Why are sustainability mandates reshaping industrial lubrication choices across manufacturing hubs?

Europe holds approximately 21.3% share of the Graphite Lubricant Market, with Germany, the UK, and France collectively contributing over 65% of regional demand. Stringent environmental and chemical safety regulations have driven more than 56% of industrial users toward solvent-free and water-based graphite lubricants. Sustainability initiatives across manufacturing clusters have accelerated adoption of lubricants that reduce particulate emissions by up to 30%. Emerging technologies such as nano-graphite dispersions and precision dosing systems are increasingly deployed, with nearly 38% of facilities using automated lubrication solutions. A major European specialty chemicals producer has invested in advanced graphite processing facilities to support low-emission formulations. Regional consumer behavior reflects regulatory-driven purchasing, where compliance and traceability strongly influence graphite lubricant selection.

How is large-scale manufacturing intensity sustaining long-term lubrication demand?

Asia-Pacific is the largest regional market by volume, accounting for approximately 46.8% of global graphite lubricant consumption. China, India, and Japan together represent more than 70% of regional demand, supported by extensive steelmaking, automotive manufacturing, and heavy engineering activities. The region hosts over 60% of global graphite processing capacity, ensuring stable supply for lubricant production. Infrastructure expansion, including rail networks and power plants, continues to drive usage in high-load and high-temperature equipment. Regional innovation hubs are advancing synthetic graphite and nano-dispersion technologies, with adoption rates above 40% among large industrial operators. Consumer behavior is characterized by cost efficiency and durability priorities, favoring powdered and colloidal graphite lubricants for continuous operations.

What role do mining and energy investments play in shaping lubrication demand?

South America accounts for approximately 10.4% of the Graphite Lubricant Market, led by Brazil and Argentina. Mining, cement production, and energy infrastructure projects represent over 65% of regional demand, with heavy machinery operating under abrasive and high-load conditions. Government-backed infrastructure programs and cross-border trade agreements have supported increased industrial activity, particularly in rail and port development. Local lubricant suppliers are expanding graphite-based offerings for mining conveyors and crushers to reduce wear by nearly 20%. Regional consumer behavior reflects strong dependence on durability and extended service intervals, with industrial buyers prioritizing products that reduce maintenance frequency in remote operations.

How are industrial diversification and infrastructure modernization influencing lubricant adoption?

The Middle East & Africa region represents roughly 8.2% of global graphite lubricant demand, driven by oil & gas operations, construction, and power generation. Key growth countries include the UAE, Saudi Arabia, and South Africa, where large-scale industrial and infrastructure projects continue to expand. Technological modernization efforts have increased adoption of graphite lubricants in drilling equipment, kilns, and heavy transport systems, with reported friction reductions of up to 18%. Trade partnerships and industrial localization policies have encouraged regional blending and distribution of specialty lubricants. Consumer behavior varies by sector, with energy operators prioritizing thermal stability while construction firms focus on cost efficiency and reliability.

China – 34.2% market share: Dominance supported by extensive graphite processing capacity and large-scale industrial consumption across steel, automotive, and energy sectors.

United States – 18.7% market share: Strong position driven by advanced manufacturing, high automation levels, and stringent performance and safety standards in industrial operations.

The Graphite Lubricant market is characterized by a moderately fragmented competitive structure, with more than 45 active manufacturers and specialty lubricant suppliers operating globally. Competition is primarily shaped by product performance under extreme conditions, formulation expertise, and the ability to meet tightening environmental and safety standards. The top five companies collectively account for approximately 48–52% of total market activity, indicating partial consolidation alongside a long tail of regional and niche players. Strategic initiatives increasingly focus on expanding high-purity and water-based graphite lubricant portfolios, with over 35% of leading players having launched low-emission or solvent-free products in the past three years. Partnerships between lubricant producers and industrial OEMs are rising, particularly in automotive, steel, and power generation sectors, to co-develop application-specific solutions. Innovation trends include nano-graphite dispersions, hybrid graphite–synthetic blends, and formulations compatible with automated lubrication systems, now adopted by nearly 40% of large industrial facilities. Mergers and capacity expansions are concentrated in Asia-Pacific and Europe, where manufacturers aim to secure raw material access and reduce supply-chain risks. Overall, competitive positioning is increasingly driven by technological differentiation, regulatory readiness, and long-term supply reliability rather than price alone.

FUCHS Group

Shell Plc

ExxonMobil Corporation

TotalEnergies SE

Castrol Limited

SKF Group

Dow Inc.

GrafTech International

The Graphite Lubricant market is witnessing significant technological advancements that are reshaping performance standards and operational efficiency across industrial applications. High-purity synthetic graphite production has increased by over 28% between 2022 and 2024, enabling consistent particle size, improved thermal stability, and superior load-bearing capacity. Nano-graphite dispersions are emerging as a transformative technology, offering up to 18% higher wear resistance and friction reduction compared to conventional flake-based lubricants, particularly in high-speed and high-temperature manufacturing equipment. Water-based and solvent-free graphite formulations now account for approximately 35% of global adoption, driven by regulatory mandates for low-VOC emissions and increasing industrial sustainability targets.

Automation and smart maintenance technologies are closely linked with graphite lubricant innovation. About 41% of large manufacturing plants have implemented automated lubrication systems, integrating sensors and AI-driven predictive maintenance tools that optimize lubrication cycles and reduce unplanned downtime by 20–22%. Advanced coatings combining graphite with polymer or synthetic additives are enhancing surface adhesion, reducing abrasive wear by 15–20% in metal processing and heavy machinery components.

Emerging trends also include hybrid graphite-synthetic lubricants for automotive stamping, rail, and aerospace applications, which improve high-load performance and minimize contamination risks. Research in nanostructured graphite is enabling finer dispersions that improve penetration into micro-gaps in bearings, chains, and molds. Collectively, these technological advancements are enabling operational cost reductions, extending equipment life, and aligning the Graphite Lubricant market with broader sustainability, digital transformation, and industrial efficiency goals.

The scope of the Graphite Lubricant Market Report encompasses comprehensive coverage of product types, application segments, end‑user industries, and regional insights. It analyzes powdered graphite, colloidal dispersions, and graphite‑enhanced greases, detailing performance characteristics, operational suitability, and technical differentiation across temperature, load, and environmental compliance requirements. The report includes segmentation by application such as metal processing, automotive manufacturing, energy generation, construction machinery, and specialty industrial equipment, providing quantitative indicators of consumption patterns and deployment scenarios.

Regional coverage spans Asia‑Pacific, North America, Europe, South America, and Middle East & Africa, offering in‑depth market volume distribution, infrastructure and industrial trends, and demand drivers across mature and emerging markets. Geographic insight includes insights into high‑adoption countries, production hubs, and infrastructure investments influencing graphite lubricant utilization. Technology focus areas highlight solid and dry lubrication innovations, nano‑graphite dispersions, water‑based and low‑emission formulations, and integration with automated and predictive maintenance systems. The report also examines regulatory influences such as environmental, safety, and workplace standards shaping product specifications and procurement practices.

Industry focus areas include heavy manufacturing, mining, rail and transportation, power plants, and construction, supported by usage metrics and operational performance indicators. The report identifies emerging niche segments such as additive manufacturing machine lubrication, aerospace component lubrication, and high‑temperature forging processes. By combining segmentation detail with measurable deployment data and technology trends, the report equips decision‑makers with actionable insights for strategic planning, product development prioritization, and competitive benchmarking within the Graphite Lubricant market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 74.54 Million |

|

Market Revenue in 2032 |

USD 107.64 Million |

|

CAGR (2025 - 2032) |

4.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

FUCHS Group , Shell Plc , ExxonMobil Corporation , TotalEnergies SE , Castrol Limited , SKF Group , Dow Inc. , GrafTech International |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |