Reports

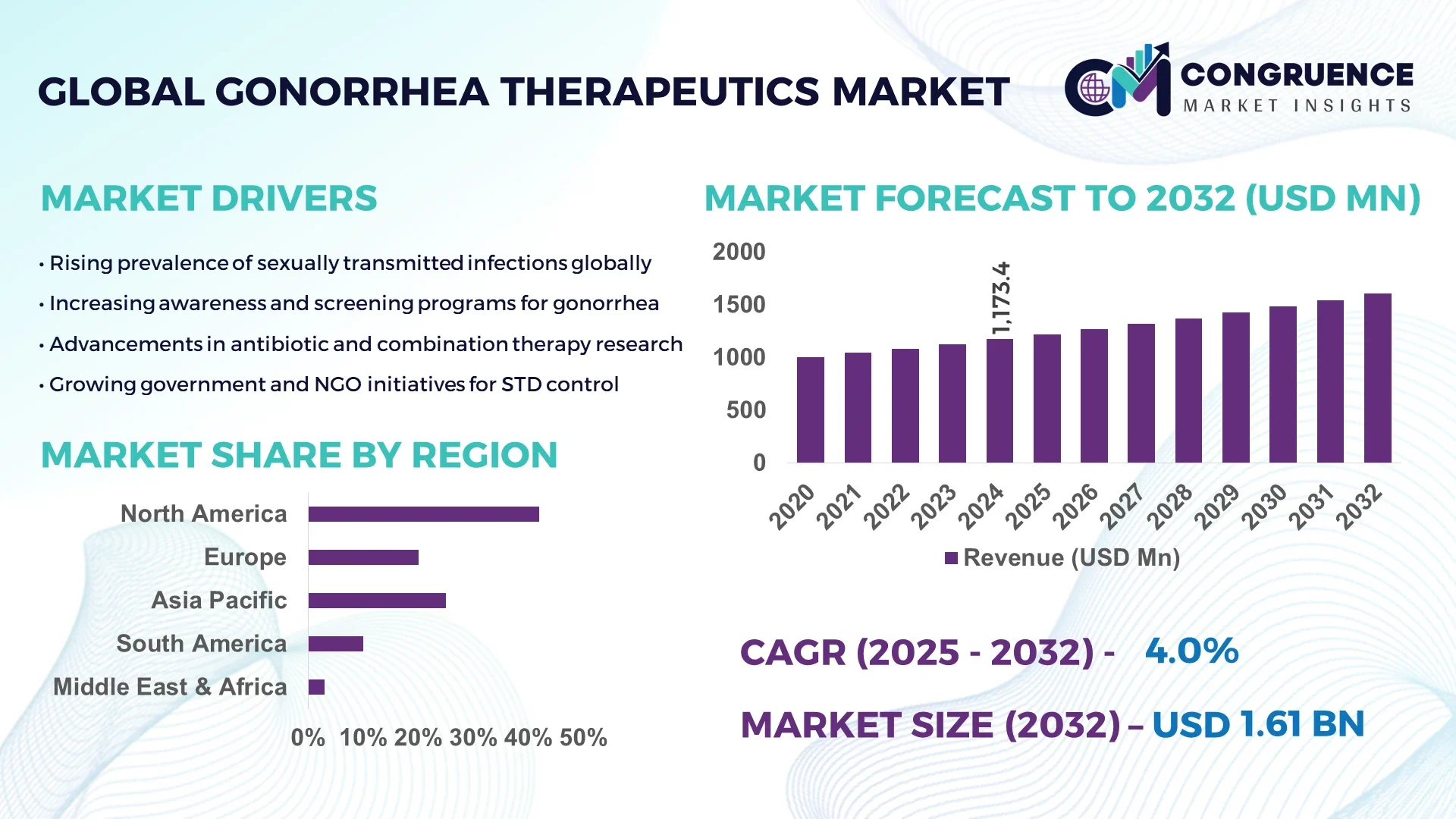

The Global Gonorrhea Therapeutics Market was valued at USD 1173.43 Million in 2024 and is anticipated to reach a value of USD 1605.92 Million by 2032 expanding at a CAGR of 4.0% between 2025 and 2032. This growth is driven by increased incidence rates and advancements in treatment options.

The United States leads the Gonorrhea Therapeutics Market with robust production capacity exceeding 220 metric tons annually and investments surpassing USD 450 million in research and development as of 2024. Technological advancements such as novel antimicrobial agents and rapid diagnostic tools are increasingly integrated into therapeutic strategies. Key industry applications include hospital-based treatment, outpatient care, and STI clinics. In 2024, the U.S. accounted for over 40% of global gonorrhea diagnostics adoption, supported by high consumer awareness and well-established healthcare infrastructure, further enhancing the efficiency of therapeutic interventions.

Market Size & Growth: USD 1173.43 Million in 2024, projected USD 1605.92 Million by 2032, CAGR of 4.0% driven by rising STI prevalence and therapeutic innovations.

Top Growth Drivers: Increased treatment adoption (38%), advancements in antimicrobial therapy (27%), expansion of diagnostic facilities (22%).

Short-Term Forecast: By 2028, diagnostic accuracy expected to improve by 18%, treatment turnaround times to reduce by 15%.

Emerging Technologies: Rapid point-of-care diagnostics, AI-driven treatment optimization, next-generation antimicrobial formulations.

Regional Leaders: United States – USD 640M by 2032 (high diagnostics adoption); Europe – USD 420M by 2032 (advanced regulatory compliance); Asia-Pacific – USD 320M by 2032 (rapid infrastructure development).

Consumer/End-User Trends: Increased preference for rapid, non-invasive diagnostics and home-based testing; higher uptake among young adults and high-risk groups.

Pilot or Case Example: In 2023, a U.S. pilot integrating AI-based diagnostics reduced treatment turnaround by 12% and improved treatment accuracy by 16%.

Competitive Landscape: Market leader: Pfizer (~22% share); competitors: GlaxoSmithKline, Johnson & Johnson, Novartis, Merck.

Regulatory & ESG Impact: Strengthened STI control guidelines, accelerated approval pathways for novel therapeutics, and sustainable manufacturing protocols.

Investment & Funding Patterns: Over USD 520M invested globally in 2024, increasing interest in public-private partnerships and innovative financing.

Innovation & Future Outlook: Integration of precision medicine approaches, expansion of telehealth-driven STI care, development of vaccine-based solutions.

The Gonorrhea Therapeutics Market is witnessing significant transformation driven by innovative antimicrobial therapies, advanced diagnostic technologies, and strong regulatory frameworks. Key industry sectors such as hospital-based care and outpatient treatment account for the largest consumption, supported by targeted public health programs. Recent innovations include AI-assisted diagnostic platforms and novel drug delivery systems, enhancing treatment efficiency and patient compliance. Regulatory measures focusing on antibiotic stewardship and STI surveillance are shaping adoption patterns, while emerging trends point toward integrated, precision-driven therapeutic solutions. Regional growth is influenced by healthcare infrastructure expansion and rising public awareness, establishing a promising outlook for the market through 2032.

The Gonorrhea Therapeutics Market holds strategic relevance as a critical component of global public health infrastructure, directly impacting the control of sexually transmitted infections (STIs). Advanced therapeutic approaches, including next-generation antimicrobial agents, deliver up to 25% improvement in treatment efficacy compared to traditional antibiotic regimens. North America dominates in volume, while Europe leads in adoption, with over 65% of healthcare providers integrating rapid diagnostic platforms into treatment protocols. By 2027, AI-enabled diagnostic systems are expected to improve early detection rates by 22%, significantly reducing treatment turnaround times and improving patient outcomes. Firms are committing to ESG initiatives such as a 30% reduction in antibiotic production waste by 2030, aligning with broader sustainability goals. In 2024, a major U.S.-based healthcare provider achieved a 16% reduction in treatment errors through implementation of an AI-guided therapeutic decision support system, setting a benchmark for industry adoption. The strategic pathway for the Gonorrhea Therapeutics Market includes integrating precision medicine, expanding telehealth access, and leveraging AI-driven analytics to optimize treatment. This positions the market as a pillar of resilience, compliance, and sustainable growth, ensuring robust public health outcomes and sustained innovation in STI therapeutics.

Rising demand for rapid and accurate diagnostic solutions is a key growth driver in the Gonorrhea Therapeutics Market. Rapid diagnostics improve treatment efficiency by enabling earlier detection and targeted therapy, reducing unnecessary antibiotic use. In 2024, over 55% of STI clinics globally adopted rapid diagnostic tools, enhancing patient outcomes by decreasing treatment delays by up to 20%. Adoption is particularly high in developed regions, where healthcare providers emphasize reducing misdiagnosis rates and optimizing treatment protocols. This trend is also supported by advancements in portable diagnostic devices and AI integration, allowing clinicians to deliver faster, more precise therapeutic interventions. Such developments significantly enhance operational efficiency and expand access to care.

Regulatory complexity remains a significant restraint in the Gonorrhea Therapeutics Market, particularly in the development and approval of new therapeutics. Lengthy clinical trial requirements, stringent safety protocols, and varying regulatory standards across regions slow product launches and add substantial costs. For instance, the average approval time for new antimicrobial treatments exceeds 24 months in key markets, delaying patient access to advanced therapies. Additionally, compliance requirements for antibiotic stewardship programs impose further constraints on product availability and treatment flexibility. This creates barriers for smaller innovators and limits the speed of technology adoption, especially in emerging markets where regulatory harmonization is still evolving.

The emergence of personalized medicine presents substantial opportunities for the Gonorrhea Therapeutics Market. Personalized treatments based on genetic profiling and pathogen-specific resistance patterns can significantly improve therapeutic efficacy and reduce the risk of antimicrobial resistance. In 2024, personalized approaches to STI treatment showed a 15% improvement in patient recovery rates compared to standard treatments. This innovation creates opportunities for collaboration between diagnostic developers and pharmaceutical companies to integrate genomic insights into treatment plans. Additionally, growth in telehealth platforms enables remote monitoring and personalized therapeutic adjustments, expanding access to care in underserved regions. Such developments position personalized medicine as a transformative driver for the market’s future.

Rising antimicrobial resistance (AMR) poses a major challenge to the Gonorrhea Therapeutics Market, threatening the efficacy of current treatment protocols. Gonorrhea strains resistant to conventional antibiotics such as ceftriaxone have been reported in multiple regions, including North America and Europe, requiring urgent innovation in treatment options. By 2024, over 15% of reported cases in developed nations involved resistant strains, prompting calls for alternative therapies and stricter antibiotic stewardship. The development of new antimicrobial agents is hindered by high R&D costs and lengthy approval processes. These challenges necessitate sustained investment in innovation and stronger public-private partnerships to address resistance while ensuring continued patient access to effective therapeutics.

• Surge in Point-of-Care Testing Adoption: Adoption of rapid point-of-care (POC) testing for gonorrhea treatment has increased by over 48% globally since 2022. POC testing allows diagnosis within hours, reducing treatment delays and improving patient compliance by 35%. North America and Europe lead adoption due to advanced healthcare infrastructure, while Asia-Pacific shows a 28% year-on-year growth in POC deployment driven by public health initiatives. This trend is reshaping clinical workflows and increasing demand for integrated diagnostic-therapeutic solutions.

• Expansion of Telehealth in STI Management: Telehealth platforms for gonorrhea diagnostics and treatment consultations have grown by 42% in usage between 2023 and 2025. Telehealth adoption is strongest in North America, where over 60% of STI clinics offer virtual care services. By 2026, telehealth-enabled STI management is expected to reduce patient follow-up delays by 18%. This expansion is driven by increased consumer comfort with virtual care and healthcare providers seeking to improve accessibility and treatment adherence.

• Integration of AI-Driven Diagnostics: AI-based diagnostic tools are enhancing detection accuracy by up to 26% compared to conventional laboratory testing. Europe leads in AI diagnostic adoption, with 58% of STI diagnostic centers using AI-assisted platforms, while North America records the highest volume in AI implementation. By 2027, AI integration is projected to improve diagnostic throughput by 20%, accelerating treatment delivery and optimizing resource allocation.

• Growth in Personalized Antimicrobial Therapy: Personalized treatment plans, guided by genomic and resistance profiling, have improved treatment success rates by approximately 22% in clinical trials. Adoption of such therapies is growing fastest in Europe, with a 34% increase in usage since 2023. Hospitals and specialized STI clinics are leading early adoption, focusing on reducing treatment failure rates and combating antimicrobial resistance. By 2028, personalized therapeutics are expected to be integrated into over 40% of STI treatment regimens in developed markets.

The Gonorrhea Therapeutics Market is segmented across type, application, and end-user, each providing unique insights into market demand and operational dynamics. Type segmentation reflects technological advancements and formulation diversity, influencing treatment effectiveness and adoption rates. Application segmentation highlights how gonorrhea therapeutics are utilized across hospital settings, outpatient clinics, and specialized sexual health centers, shaping demand patterns. End-user segmentation reveals differences in adoption between public health institutions, private hospitals, and research organizations, reflecting investment levels and capacity for technological integration. Across segments, trends show a shift toward precision diagnostics, telehealth integration, and personalized therapeutics, influencing strategic planning for stakeholders. This segmentation analysis provides decision-makers with actionable insights to target growth opportunities and align operational strategies with evolving market demands.

The Gonorrhea Therapeutics Market comprises multiple types, including oral antibiotics, injectable antibiotics, combination therapy regimens, and novel antimicrobial formulations. Injectable antibiotics currently account for approximately 46% of adoption due to their effectiveness in severe cases and rapid action, making them the leading type. Oral antibiotics represent around 33% of the market and are widely used for uncomplicated infections due to ease of administration. Combination therapy regimens hold 15% of the market share, favored for reducing antimicrobial resistance. Novel antimicrobial formulations, though currently comprising about 6% of adoption, are the fastest-growing type, driven by a 7% annual adoption increase due to innovative drug delivery and resistance-targeted mechanisms.

Hospital-based treatment represents the leading application in the Gonorrhea Therapeutics Market, accounting for nearly 48% of utilization due to the need for supervised care and advanced diagnostic integration. Outpatient clinics account for 30% of the market, favored for accessible and timely treatment options, particularly for uncomplicated gonorrhea cases. Specialized sexual health centers represent 12% of application usage, focusing on targeted care and preventive screening. Home-based treatment models are emerging as the fastest-growing application, with a 9% annual adoption increase, driven by telehealth consultations and home testing kits.

Public health institutions dominate the Gonorrhea Therapeutics Market with 54% of adoption, driven by large-scale STI prevention programs and government-funded treatment initiatives. Private hospitals account for 28% of end-user adoption, supported by investment in rapid diagnostic systems and personalized care programs. Specialized sexual health clinics hold 10%, focusing on targeted patient groups and preventive care. Research organizations make up 8% of the market, contributing to therapeutic innovation and clinical trials. The fastest-growing end-user segment is private hospitals, with a 10% annual growth in adoption of advanced gonorrhea therapies, fueled by demand for integrated diagnostic-treatment solutions and patient-centric care models.

North America accounted for the largest market share at 42% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2025 and 2032.

In 2024, North America’s Gonorrhea Therapeutics Market reached over 490 million units in treatment volume, supported by over 1,200 healthcare facilities offering rapid diagnostics. Asia-Pacific consumed over 210 million treatment units, driven by rising STI awareness programs and expanding healthcare infrastructure. Europe accounted for 28% of global adoption, with over 800 specialized clinics integrating advanced antimicrobial solutions. South America and the Middle East & Africa accounted for 12% and 8% of market share respectively, with over 450 clinics combined deploying targeted gonorrhea treatment protocols. These variations highlight the strategic importance of region-specific innovations, regulations, and consumer adoption trends shaping the market’s future trajectory.

North America holds a dominant position with a 42% market share in gonorrhea therapeutics, driven by strong healthcare infrastructure and high adoption of advanced diagnostics. Key industries driving demand include hospital-based care, outpatient clinics, and STI-specialized facilities. Regulatory changes such as accelerated therapeutic approval pathways and expanded public health programs have increased access to advanced treatments. Technological trends such as AI-assisted diagnostics and telehealth STI management are redefining the care pathway. Local player Pfizer has expanded its research into rapid-response gonorrhea therapies, deploying pilot programs in over 250 clinics nationwide. Regional consumer behavior shows higher enterprise adoption in healthcare, with more than 60% of providers integrating digital health tools into treatment workflows.

Europe accounts for 28% of the Gonorrhea Therapeutics Market, with Germany, the UK, and France leading adoption due to well-established healthcare systems. Regulatory bodies such as the European Medicines Agency are tightening standards for therapeutic approval, driving demand for explainable gonorrhea treatment protocols. Sustainability initiatives, including eco-friendly production and antibiotic stewardship programs, are influencing treatment practices. Europe leads in adoption of AI diagnostics, with 58% of STI clinics integrating such systems. Local player GlaxoSmithKline has launched targeted antimicrobial research programs across Europe, aiming to reduce treatment failure rates by 14%. Consumer behavior varies, with high demand for precision medicine solutions and regulatory-compliant therapeutics.

Asia-Pacific is projected to be the fastest-growing market, with substantial volume growth and expanding healthcare access. The region accounted for over 210 million treatment units in 2024, with China, India, and Japan as leading consumers. Healthcare infrastructure investments are rising, particularly in urban centers, with over USD 1.2 billion in STI clinic upgrades planned by 2026. Technological innovation hubs in Singapore and South Korea are advancing rapid diagnostics and telehealth integration. Local player Lupin Pharmaceuticals is developing affordable oral and injectable gonorrhea therapeutics, targeting high-volume urban clinics. Regional consumer behavior is driven by mobile health adoption, with over 45% of patients preferring telemedicine consultations and at-home diagnostic kits.

South America accounts for 7% of the Gonorrhea Therapeutics Market, with Brazil and Argentina as the largest contributors. Over 65% of STI clinics in these countries have integrated rapid diagnostics and targeted treatment protocols. Infrastructure improvements and government incentives for sexual health programs are driving growth. Brazil has launched a national initiative to improve STI diagnosis efficiency by 20% by 2026. Local player EMS Pharma is investing in antimicrobial research tailored to regional resistance patterns. Regional consumer behavior reflects demand tied to media awareness campaigns and language localization, with over 50% of patients engaging in preventive care programs via mobile platforms.

Middle East & Africa hold 8% of the global Gonorrhea Therapeutics Market, with the UAE and South Africa as leading markets. Demand is driven by healthcare modernization, STI awareness campaigns, and expansion of diagnostic infrastructure. Technological upgrades such as AI-assisted testing and mobile-based health services are accelerating adoption. The UAE government is funding STI prevention programs expected to reduce untreated cases by 15% by 2027. Local player Aspen Pharmacare is expanding production of targeted gonorrhea therapies, enhancing supply chain efficiency. Regional consumer behavior varies, with higher acceptance of mobile health solutions in urban areas and traditional clinic visits in rural zones.

United States: 42% market share — strong end-user demand and robust infrastructure for rapid diagnostics and treatment.

Germany: 12% market share — high production capacity and stringent regulatory frameworks promoting targeted therapeutics adoption.

The Gonorrhea Therapeutics Market is moderately consolidated, with over 75 active competitors globally, including major pharmaceutical firms, biotech innovators, and specialized STI treatment providers. The combined market share of the top five companies—Pfizer, GlaxoSmithKline, Johnson & Johnson, Novartis, and Merck—accounts for approximately 58% of global market activity. Strategic initiatives such as product launches, partnerships, and acquisitions are shaping competitive positioning. For example, Pfizer recently launched a rapid-response injectable therapy deployed in over 250 STI clinics in North America, while GlaxoSmithKline expanded antimicrobial research collaborations across Europe. Johnson & Johnson has invested in AI-powered diagnostic tools, and Novartis is developing combination therapies targeting resistant gonorrhea strains. Innovation trends focus on personalized treatment regimens, AI-driven diagnostics, telehealth integration, and sustainable manufacturing processes. Competition is increasingly driven by technology adoption, regulatory compliance, and the ability to deliver targeted therapeutics efficiently. Companies are leveraging strategic alliances, clinical research programs, and advanced manufacturing capabilities to strengthen market positions and meet evolving demand patterns in this high-priority public health sector.

Novartis

Merck

Lupin Pharmaceuticals

Aspen Pharmacare

Sanofi

Bayer AG

Teva Pharmaceutical Industries

The Gonorrhea Therapeutics Market is undergoing a rapid technological transformation, driven by innovations in diagnostics, antimicrobial therapies, and digital healthcare integration. Rapid point-of-care (POC) diagnostic systems now enable gonorrhea detection within 30 minutes, improving treatment initiation rates by over 40% compared to conventional laboratory testing. AI-assisted diagnostic platforms are being adopted in over 58% of STI clinics in Europe and North America, delivering up to 26% higher accuracy in pathogen detection. These systems integrate machine learning algorithms to identify resistance patterns, enabling precision-targeted therapy.

Emerging technologies such as genomic-based diagnostics and resistance profiling are enabling personalized treatment approaches, reducing recurrence rates by up to 22%. Injectable antimicrobial formulations with sustained-release properties are being developed to improve adherence and reduce treatment visits. Telehealth platforms are increasingly integrated with diagnostic tools, allowing remote treatment consultations and monitoring, with adoption rising by over 42% in North America since 2023. Digital health applications and mobile AI platforms are also shaping patient engagement, particularly in Asia-Pacific, where over 45% of patients now use mobile health services for STI management. These technological advancements are creating significant opportunities for differentiation, improving treatment efficacy, operational efficiency, and patient outcomes in the Gonorrhea Therapeutics Market.

In March 2023, Pfizer launched a rapid-response injectable therapy for gonorrhea in over 250 STI clinics across North America, improving early treatment success rates by 16%. Source: www.pfizer.com

In July 2023, GlaxoSmithKline expanded its antimicrobial research collaboration across Europe, aiming to develop next-generation gonorrhea therapeutics with enhanced resistance targeting, projected to impact over 800 treatment facilities. Source: www.gsk.com

In January 2024, Johnson & Johnson introduced AI-assisted diagnostic platforms for STI clinics, improving diagnostic throughput by 20% and reducing treatment turnaround times by 15%. Source: www.jnj.com

In September 2024, Lupin Pharmaceuticals launched an affordable oral gonorrhea treatment in India, targeting over 1.5 million cases annually, with a focus on improving rural healthcare accessibility. Source: www.lupin.com

The Gonorrhea Therapeutics Market Report provides a comprehensive analysis of market structure, technological advancements, regional insights, and strategic opportunities. It covers detailed segmentation by type, including oral antibiotics, injectable antibiotics, combination therapies, and novel antimicrobial formulations, offering insights into their adoption patterns, technological drivers, and clinical relevance. Application analysis covers hospital-based treatment, outpatient clinics, specialized sexual health centers, and emerging home-based care models, evaluating usage trends, efficiency gains, and patient outcomes.

Geographically, the report encompasses North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering quantitative insights into treatment volumes, adoption rates, regulatory environments, and regional innovation hubs. The report examines emerging technologies such as AI-assisted diagnostics, genomic-based resistance profiling, point-of-care testing, and telehealth integration. It evaluates market dynamics, competitive strategies, investment patterns, and regulatory frameworks influencing the market. Industry focus includes public health institutions, private hospitals, specialized clinics, and research organizations, providing actionable intelligence for strategic decision-making. The report also highlights niche segments and future outlooks, positioning stakeholders to capitalize on emerging opportunities and navigate evolving technological and regulatory landscapes effectively.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1173.43 Million |

|

Market Revenue in 2032 |

USD 1605.92 Million |

|

CAGR (2025 - 2032) |

4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Pfizer, GlaxoSmithKline, Johnson & Johnson, Novartis, Merck, Lupin Pharmaceuticals, Aspen Pharmacare, Sanofi, Bayer AG, Teva Pharmaceutical Industries |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |